- Specialty & Fine Chemicals

- Firestop Foam Market

Firestop Foam Market Size, Share, Trends, Growth, Regional Forecasts, 2026 - 2033

Firestop Foam Market by Product Type (Cementitious Firestop Foam, Polymer-based Firestop Foam, Intumescent Firestop Foam, Acrylic Firestop Foam), Application (Public Buildings, Industrial Buildings, Residential Buildings, Others), End-User (Construction Industry, Industrial & Manufacturing Sector, Energy & Utilities, Aerospace & Specialized Infrastructure), and Regional Analysis for 2026 - 2033

Firestop Foam Market Share and Trends Analysis

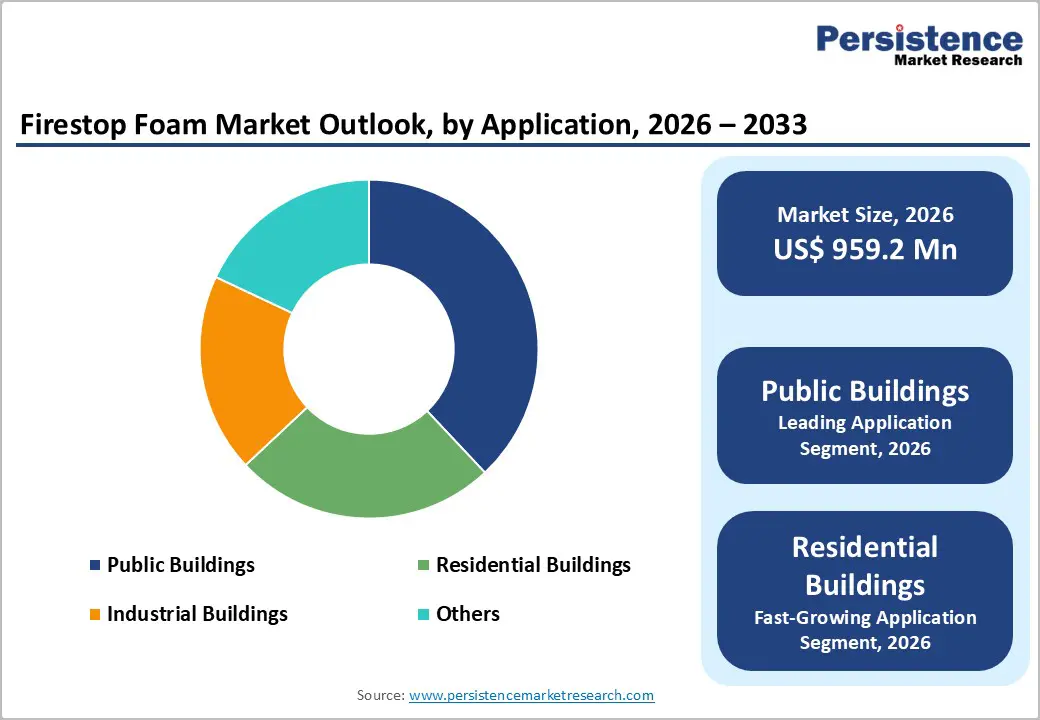

The global firestop foam market size is likely to be valued at US$ 959.2 million in 2026, and is projected to reach US$ 1,253.7 million by 2033, growing at a CAGR of 3.9% during the forecast period 2026−2033. Demand is supported by stricter fire safety compliance and expanding use of passive fire protection systems in modern construction. Building code enforcement drives adoption of certified firestop materials, increasing demand for advanced foam sealing solutions.

Urbanization and infrastructure density create more penetration points for electrical, plumbing, and heating, ventilation, and air conditioning (HVAC) systems, requiring effective fire containment in compartmentalized designs. Growing awareness of fire risk mitigation strengthens adoption across residential and commercial segments. Regulatory guidance from the National Fire Protection Association (NFPA) and International Code Council (ICC) improves compliance among developers and contractors. Technological advancements, including intumescent and low-volatile organic compound (VOC) formulations, enhance performance and sustainability, while digital tools such as building information modeling (BIM) improve specification accuracy and installation efficiency.

Key Industry Highlights

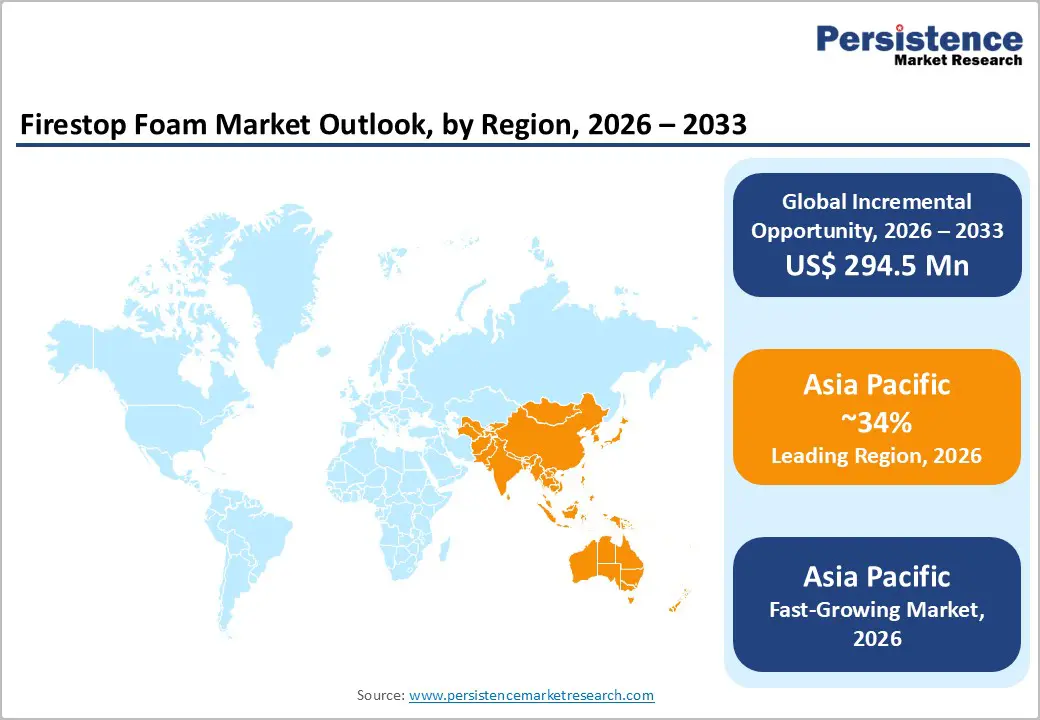

- Regional Leadership: Asia Pacific is likely to lead with about 34% market revenue share, and the market here is slated to register the highest 2026-2033, fueled by high-rise housing trends.

- Leading Product: Intumescent firestop foam is anticipated to secure around 34% of the market revenue share in 2026, driven by high-performance fire resistance.

- Fastest-Growing Product: Acrylic firestop foam is expected to be the fastest-growing 2026-2033 product, owing to its cost efficiency and ease of application.

- Dominant Application: Public buildings are poised to dominate with a forecasted market revenue share of over 38% in 2026 due to strict regulatory compliance.

- Fastest-Growing Application: Residential buildings are estimated to be the fastest-growing from 2026 to 2033, stimulated by skyrocketing rate of urbanization and high safety awareness.

| Key Insights | Details |

|---|---|

|

Firestop Foam Market Size (2026E) |

US$ 959.2 Mn |

|

Market Value Forecast (2033F) |

US$ 1253.7 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

3.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3% |

DRO Analysis

Stringent Regulations to Drive Firestop Foam Adoption

Regulatory frameworks establish mandatory fire performance standards for buildings, which directly enforce the use of certified passive fire protection systems. Fire codes require that every penetration in fire-rated walls or floors must maintain integrity during a fire event, creating a defined need for tested sealing solutions. Firestop systems prevent fire and smoke spread through service openings, ensuring compartmentation effectiveness. The NFPA develops widely adopted codes such as NFPA 101 and NFPA 72, which are integrated into local laws and enforced by authorities. These codes guide installation, inspection, and maintenance practices across building types.

Regulatory updates in 2025 introduced stricter safety planning, improved detection integration, and enhanced performance requirements for building systems. Compliance requires alignment with certified materials and documented installation methods, increasing reliance on advanced sealing technologies. NFPA maintains over 300 codes and standards used globally to reduce fire risk, reflecting continuous regulatory expansion. This regulatory depth compels contractors and developers to prioritize tested fire protection components during construction and retrofit activities. Enforcement by local authorities and inspection bodies strengthens adherence, while liability considerations and insurance requirements reinforce consistent implementation of compliant fire containment solutions across projects.

Advent of Advanced Technology to Improve Product Performance

Performance enhancement through material innovation directly influences reliability, compliance, and lifecycle efficiency in fire protection applications. Advanced intumescent chemistry enables rapid expansion under heat exposure, sealing gaps and limiting flame spread. Improved adhesion and curing properties support consistent application across complex penetration points. Low-emission formulations align with indoor air quality standards, supporting green building certification requirements. Precision-engineered foams reduce installation errors and rework costs. In 2025, the U.S. Fire Administration reported over 9.3 million incident records through national reporting systems, reinforcing the need for high-performance containment solutions in diverse fire scenarios.

Construction practices are evolving toward integrated and data-driven execution models. Digital workflows improve specification accuracy and reduce compliance gaps during installation. High-performance materials support durability under thermal stress, moisture exposure, and structural movement. Enhanced product consistency ensures predictable expansion and sealing behavior across varied substrates. Regulatory alignment requires tested and listed systems, increasing preference for technologically advanced solutions. Performance-driven innovation strengthens trust among contractors, engineers, and inspectors, supporting wider adoption in critical infrastructure and high-occupancy buildings.

Shortage of Skilled Labor to Stifle Market Growth

Precise installation standards govern firestop foam application across penetrations and joints within compartmentalized building structures. Each installation must align with tested and listed system designs, including correct depth, density, substrate compatibility, and curing conditions. Variations in wall assemblies, pipe materials, and cable configurations require on-site judgment and technical interpretation of certification documents. Inadequate application can compromise fire-resistance ratings, creating liability risks for contractors and developers. Inspection protocols demand documented compliance, reinforcing the need for trained professionals capable of executing installations in line with regulatory expectations and project specifications.

Workforce availability remains constrained in many regions, where certified firestop installers represent a limited talent pool. Training programs require time investment and practical exposure to diverse construction scenarios, slowing workforce expansion. Contractors face operational challenges in maintaining consistency across large-scale projects with multiple penetration types. Labor cost premiums increase overall project expenditure, influencing procurement decisions in cost-sensitive environments. Complex coordination between design teams and installation crews further elevates reliance on experienced personnel, particularly in projects integrating mechanical, electrical, and plumbing systems within dense infrastructure layouts.

Growing Competition from Alternatives

Competitive pressure emerges from the availability of substitute firestop solutions such as sealants, wraps, collars, and firestop boards that address similar penetration sealing requirements. These alternatives offer varying performance characteristics aligned with specific applications, including pipe, cable, and duct penetrations. Cost sensitivity in construction projects drives material selection toward lower-priced or multi-purpose options, reducing reliance on foam-based products. Procurement teams often prioritize standardized materials already approved within project specifications, limiting product switching. Established contractor familiarity with traditional firestop systems further reinforces consistent usage patterns across large-scale developments and infrastructure projects.

Material performance perception and application flexibility influence decision-making across stakeholders. Certain alternatives provide higher mechanical strength, reusability, or suitability for complex penetrations, positioning them as preferred solutions in critical installations. Regulatory approvals and third-party testing certifications extend across multiple product categories, allowing substitutes to meet compliance requirements effectively. Distribution networks and supplier relationships also play a role, as widely available alternatives gain stronger market visibility. In large construction ecosystems, specification inertia and risk aversion encourage continued use of proven materials, constraining rapid adoption of newer foam-based firestop technologies despite ongoing product innovation.

Innovation to Enable New Applications

Continuous product innovation expands functional scope across complex construction environments. Advanced formulations support sealing in high-density cable bundles, data centers, and modular structures. Intumescent chemistry enables expansion under heat, improving fire compartment integrity in irregular openings. Low-emission materials align with environmental compliance in green buildings. Flexible foam structures adapt to dynamic joints and mixed-material interfaces. These capabilities allow deployment in retrofits, prefabricated systems, and high-performance infrastructure. According to the NFPA, fire departments responded to 1.38 million fires in 2024, indicating sustained demand for improved containment solutions.

Application diversity increases value across multiple end-use scenarios. Construction complexity continues to rise with integrated electrical and digital systems. This shift requires adaptable sealing solutions across varied substrates and penetration types. Innovation enables compatibility with automation-driven installation practices and digital specification tools. Enhanced durability supports long service life in critical infrastructure. Multi-functional performance, including thermal and acoustic insulation, strengthens adoption across commercial and industrial assets. Regulatory focus on performance-based standards encourages use of tested and certified advanced materials.

Green Construction to Support Adoption

Green building frameworks prioritize low-emission materials and certified safety systems aligned with environmental codes. Buildings account for 34% of global CO2 emissions in 2025, according to a report by the United Nations Environment Programme (UNEP), creating strong regulatory pressure to adopt compliant materials. Firestop foam solutions with low-volatile organic compound formulations align with these sustainability targets. Certification systems such as Leadership in Energy and Environmental Design (LEED) and national green codes require tested fire protection materials that meet both safety and environmental criteria. This alignment increases specification rates during design and procurement phases.

Sustainable construction emphasizes lifecycle performance, material efficiency, and indoor environmental quality. Firestop foam supports airtight sealing, improves energy efficiency, and reduces smoke and toxic emission spread during fire events. These attributes align with green building performance metrics focused on occupant safety and operational efficiency. Digital design tools integrate firestop specifications into energy-efficient building models, improving compliance tracking. Developers prioritize materials that contribute to certification credits and long-term cost efficiency. This shift strengthens adoption of advanced sealing solutions within high-performance construction ecosystems.

Category-wise Analysis

Product Type Insights

Intumescent firestop foam is anticipated to secure around 34% of the firestop foam market revenue share in 2026, reflecting strong adoption driven by advanced fire-resistance properties. These materials expand under elevated temperatures, forming a dense char that blocks flame, heat, and smoke migration through service penetrations. Performance reliability supports use in mission-critical environments such as data centers and healthcare facilities. Compliance with fire-rated assembly requirements strengthens specification by architects and engineers. Ongoing product innovation improves expansion ratios, adhesion strength, and environmental compatibility, supporting sustained demand across complex commercial and industrial construction projects globally.

Acrylic firestop foam is expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by ease of application and cost efficiency. Flexible formulations enable effective sealing across varied joint sizes and penetration types in residential and light commercial construction. Simplified installation processes reduce labor intensity and project timelines, improving contractor productivity. Enhanced formulation stability supports consistent performance across temperature and humidity variations. Compatibility with multiple substrates increases application scope. Growing preference for economical fire protection solutions in emerging markets, along with low-emission product development, supports adoption in sustainable building projects.

Application Insights

Public buildings are poised to dominate with a forecasted market share of over 38% in 2026, powered by stringent safety compliance and high occupancy risk considerations. Regulatory frameworks enforce strict fire protection standards across educational institutions, healthcare facilities, and administrative complexes. High occupant density and continuous usage patterns require reliable compartmentalization and sealing systems. Procurement policies emphasize certified and tested firestop solutions, ensuring compliance with safety codes. Ongoing infrastructure upgrades and renovation programs incorporate advanced fire protection systems, sustaining demand across public sector construction projects.

Residential buildings are estimated to be the fastest-growing segment from 2026 to 2033, fueled by increasing urban housing demand and regulatory expansion. Expansion of urban populations drives development of multi-family housing and high-rise apartments, increasing the need for effective fire containment solutions. Updated residential building codes encourage integration of passive fire protection systems. Growing consumer awareness regarding home safety supports product adoption. Standardized construction practices and prefabrication techniques improve consistency in firestop implementation, while digital platforms enhance product visibility and accessibility across emerging markets.

Regional Insights

Asia Pacific Firestop Foam Market Trends and Insights

Asia Pacific is expected to lead with an estimated 34% of the firestop foam market share, supported by large-scale urban infrastructure pipelines and rising complexity of building systems. High penetration of high-rise developments increases the number of service openings requiring certified sealing solutions. Expansion of data centers, transport hubs, and healthcare infrastructure elevates fire risk profiles, strengthening specification of advanced firestop materials. Growth momentum remains strong in China and India, driven by extensive construction activity and regulatory progression. Mature construction ecosystems in Japan and South Korea reinforce adoption through advanced building standards and compliance frameworks.

Asia Pacific is forecasted to be the fastest-growing market for firestop foam between 2026 and 2033, stimulated by rapid expansion of multi-family housing and vertical construction formats. Increasing integration of mechanical, electrical, and plumbing networks raises the need for effective compartmentalization. Building code evolution introduces stricter fire-resistance requirements across residential developments. Rising construction demand accelerates adoption in China and India through large-scale housing and infrastructure projects. Technological advancement and precision construction practices in Japan and South Korea support consistent implementation of high-performance firestop solutions.

North America Firestop Foam Market Trends and Insights

North America represents a mature and highly regulated market for firestop foam, with widespread adoption across commercial, industrial, and residential construction. Strict building codes enforce use of tested and listed firestop systems, ensuring consistent demand for advanced foam solutions. High-density urban centers and tall buildings increase penetration points requiring effective sealing, particularly in mechanical, electrical, and plumbing networks. Expansion of data centers, healthcare facilities, and educational institutions raises fire risk management priorities, driving preference for certified and performance-verified products. Established local manufacturing and distribution networks ensure rapid availability and cost efficiency. Retrofits and maintenance programs further support recurring demand across construction projects.

Market growth is supported by technological innovation and integration into modern construction practices. Development of intumescent and low-emission foam formulations improves durability, installation efficiency, and environmental compliance. Adoption of digital tools, including building information modeling and project management platforms, enhances specification accuracy and reduces errors. Rising multi-family and high-rise residential construction increases penetration points for firestop solutions. Standardized installation practices and specialized contractor training ensure compliance. Demand for low-VOC and sustainable products drives material preference, while strategic partnerships between manufacturers, distributors, and construction firms expand market accessibility across urban and suburban development projects.

Europe Firestop Foam Market Trends and Insights

Europe maintains a significant market position supported by harmonized fire safety regulations and established construction standards. Firestop foam demand is driven by stringent enforcement of fire-resistance ratings within commercial, industrial, and public infrastructure projects. Countries such as Germany and France demonstrate strong adoption through large-scale renovations and modernization of transport hubs and healthcare facilities. Retrofitting aging structures increases requirements for certified sealing solutions. Insurance and compliance standards influence material selection, encouraging tested firestop systems. Sustainability considerations promote low-emission formulations aligned with environmental performance expectations.

Growth is influenced by modernization of residential and mixed-use developments, where fire protection integration forms a core design requirement. Steady demand persists in United Kingdom and Italy due to regulatory updates and heightened building safety scrutiny. Digital construction workflows enhance specification accuracy and installation traceability. Skilled workforce availability ensures consistent application quality across complex projects. Product innovations focus on durability, acoustic performance, and substrate compatibility. Expansion of green building certifications encourages adoption of environmentally compliant firestop foam solutions across new and refurbished construction projects.

Competitive Landscape

The global firestop foam market demonstrates a moderately fragmented structure with participation from both global and regional manufacturers, creating a diverse competitive landscape. Key players such as 3M Company, Hilti Group, Sika AG, RPM International, BASF SE, and Specified Technologies maintain strong positions through comprehensive certified product portfolios. Established distribution networks enable wide product availability across commercial, industrial, and residential construction sectors. Emphasis on regulatory compliance and performance reliability strengthens their market credibility and adoption across complex infrastructure projects.

Competitive positioning centers on product performance, application efficiency, and compliance capability, ensuring alignment with evolving fire safety standards. Regional manufacturers focus on cost-effective solutions and localized supply chains to capture niche demand segments. Innovation in intumescent and low-emission firestop foams supports differentiation. Contractors and developers prefer suppliers with technical support and training programs, reinforcing partnerships and driving recurring demand for advanced firestop solutions across high-density urban and industrial construction projects.

Key Industry Developments

- In March 2025, AF Systems’ AF Graphit Foam received European Technical Assessment (ETA) certification, validating its performance as a firestop solution for sealing mechanical and electrical penetrations. The graphite-enhanced polyurethane foam delivers up to EI 180 fire resistance and supports complex applications without additional components.

- In April 2025, Specified Technologies Inc. announced the launch of the SpecSeal® 8 Inch Cast-In Device, a rugged welded firestop solution designed for large openings that improves concrete flow and expands under heat to block fire and smoke spread in construction applications.

Companies Covered in Firestop Foam Market

- 3M Company

- Hilti Group

- Sika AG

- RPM International Inc.

- BASF SE

- Specified Technologies Inc.

- H.B. Fuller Company

- Fosroc International

- RectorSeal LLC

- Tremco Incorporated

- Knauf Insulation

- Bostik

- Morgan Advanced Materials

Frequently Asked Questions

The global firestop foam market is projected to reach US$ 959.2 million in 2026.

Rising fire safety regulations and increasing integration of passive fire protection systems are driving the market.

The market is poised to witness a CAGR of 3.9% from 2026 to 2033.

Growing urban infrastructure, high-rise construction, and demand for sustainable fire protection solutions can produce key market opportunities.

Some of the key market players include 3M Company, Hilti Group, Sika AG, RPM International, BASF SE, and Specified Technologies.