- Specialty & Fine Chemicals

- Compressor Oil Market

Compressor Oil Market Size, Share, and Growth Forecast, 2026 - 2033

Compressor Oil Market by Base Oil Type (Synthetic, Semi-Synthetic/Bio-Based, Others), Compressor Type (Positive Displacement, Dynamic, Others), End-user Industry, and Regional Analysis for 2026 - 2033

Compressor Oil Market Size and Trends Analysis

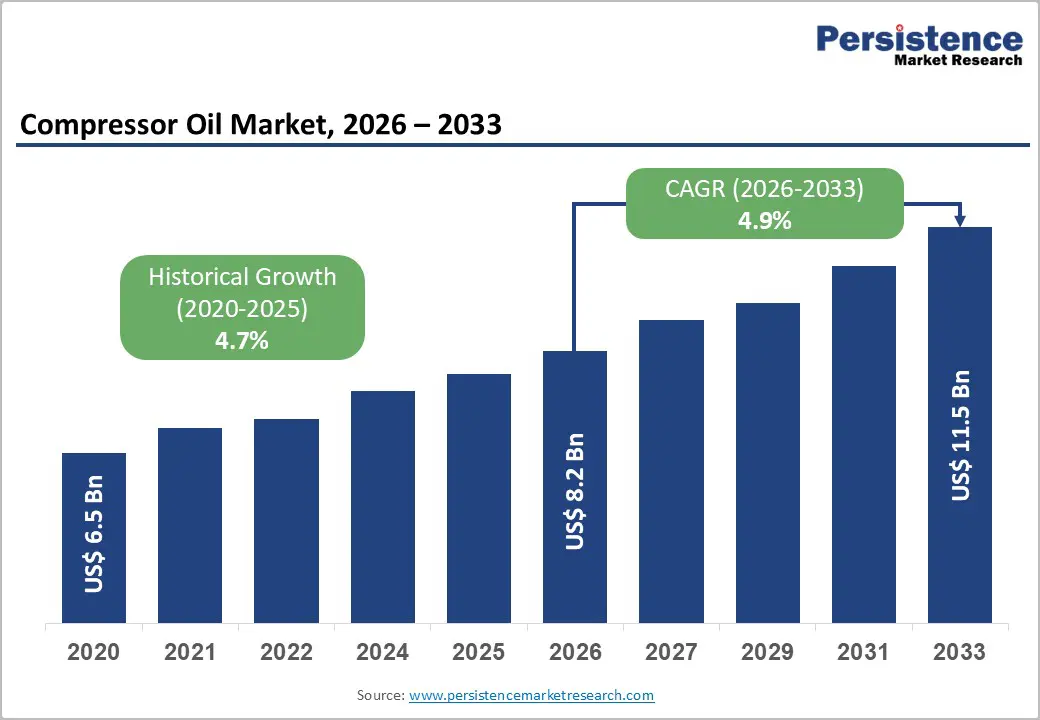

The global compressor oil market size is likely to be valued at US$8.2 billion in 2026 and is expected to reach US$11.5 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033, driven by the rising installed base of compressors across manufacturing, energy, chemicals, and process industries, where lubrication quality directly impacts equipment uptime, operational efficiency, and asset longevity.

Energy-efficiency initiatives across industrial facilities are further elevating the importance of high-performance lubricants, as optimized compressor systems can significantly reduce power consumption.

Key Industry Highlights:

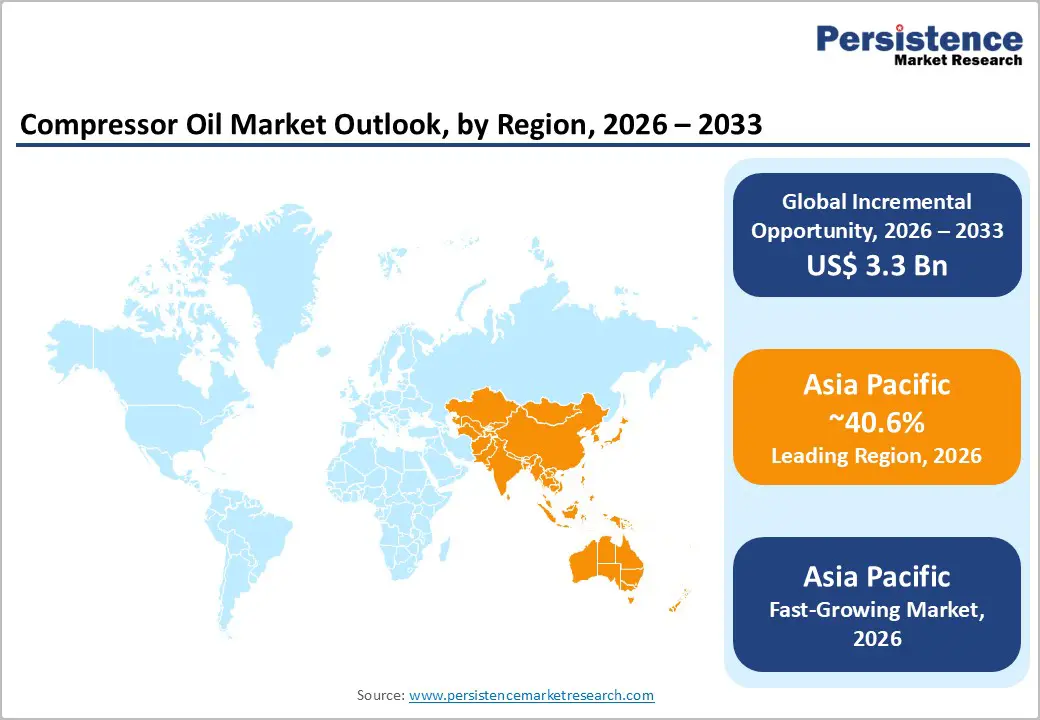

- Leading Region: Asia Pacific is projected to account for approximately 40.6% of market share, driven by strong manufacturing activity in China, India, and Southeast Asia.

- Fastest-growing Region: Asia Pacific, supported by rapid industrialization, infrastructure expansion, and increasing adoption of advanced compressor systems across emerging economies.

- Investment Plans: Strategic investments are focused on expanding regional production capacity, developing synthetic and bio-based lubricants, and integrating digital monitoring solutions, with key players such as Exxon Mobil Corporation and Shell plc strengthening their presence in Asia and North America.

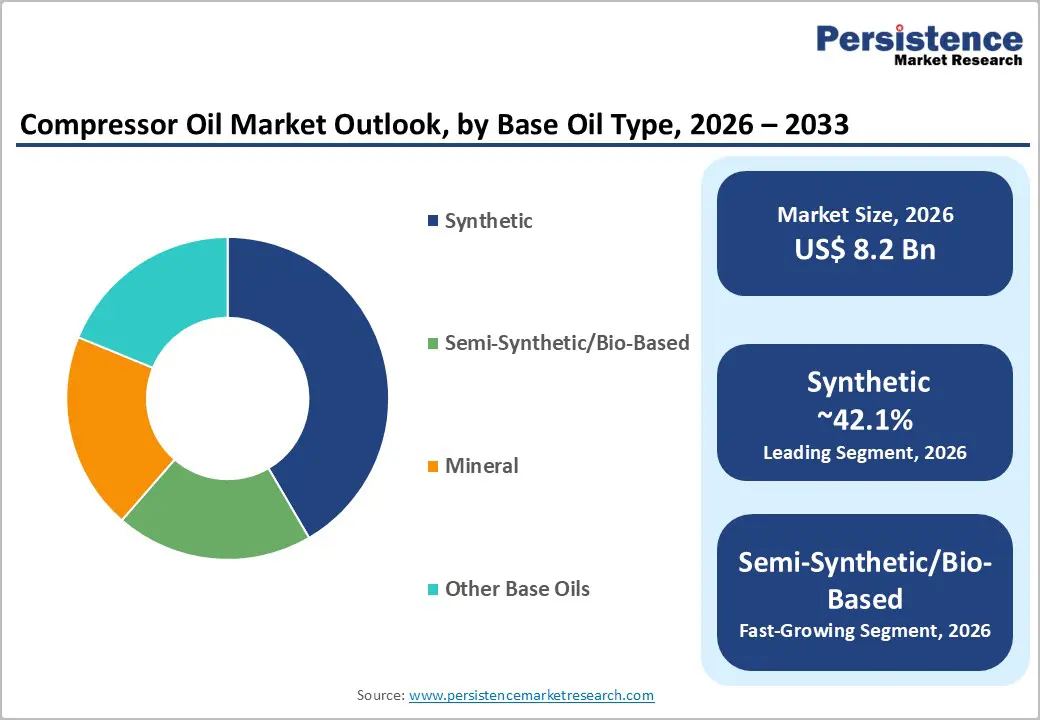

- Dominant Base Oil Type: Synthetic compressor oils are anticipated to lead with 42.1% market share, driven by superior performance in high-load and high-temperature applications.

- Leading Application: Air compressors are estimated to hold 71.3% market share, supported by widespread usage across manufacturing, industrial utilities, and automation processes.

| Key Insights | Details |

|---|---|

| Compressor Oil Market Size (2026E) | US$8.2 Bn |

| Market Value Forecast (2033F) | US$11.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

DRO Analysis

Driver Analysis - Industrial Automation and Compressed-Air Dependence in Manufacturing

Manufacturing remains the primary demand driver for compressor oils due to the widespread reliance on compressed-air systems in production processes. Compressors are integral to assembly lines, packaging units, material handling, and plant utilities. Industrial studies indicate that compressed-air systems can account for nearly 10% of total electricity consumption in developed industrial economies, with optimization potential of 15% to 30%. Improved compressor performance through high-quality lubrication reduces friction losses, minimizes wear, and enhances system efficiency. As manufacturers continue to automate operations and scale production, the need for reliable compressor performance is increasing, directly boosting demand for premium compressor oils.

Shift toward Premium Synthetic Lubricants

Synthetic compressor oils are gaining traction due to their superior thermal stability, oxidation resistance, and ability to perform under extreme operating conditions. These lubricants are particularly effective in rotary screw, reciprocating, gas, and refrigeration compressors, where high temperatures and pressures are common. Longer oil life reduces maintenance frequency and unplanned downtime, lowering the total cost of ownership for end users. The increasing focus on operational efficiency and predictive maintenance is accelerating the transition from conventional mineral oils to advanced synthetic formulations. This shift is structurally improving the value profile of the compressor oil market.

Energy-Transition Infrastructure and Gas Compression Demand

The expansion of natural gas infrastructure, LNG facilities, and energy-transition assets is creating new demand for compressor oils. Gas compressors operate under demanding conditions, requiring specialized lubricants that ensure reliability and minimize emissions. Regulatory frameworks targeting methane emissions and volatile organic compounds are further emphasizing the need for high-performance lubrication solutions. As investments in gas processing, transportation, and storage infrastructure continue to rise, compressor oil demand is expected to grow in tandem, particularly in high-value applications.

Restraint Analysis - Price Sensitivity and Preference for Low-Cost Alternatives

A key restraint in the compressor oil market is the continued preference for low-cost mineral oils among price-sensitive customers. Many end users still perceive compressor oil as a consumable expense rather than a strategic investment in performance and efficiency. In less demanding applications, mineral oils may meet basic requirements, reducing the urgency to switch to premium alternatives. This creates a two-tier market structure, where high-end users adopt advanced lubricants while cost-conscious buyers prioritize affordability. Such dynamics can limit overall value growth, particularly during periods of reduced industrial investment.

Regulatory Complexity and Compliance Costs

The increasing complexity of environmental and safety regulations presents a significant challenge for both manufacturers and end users. Compliance with evolving standards related to biodegradability, emissions, and chemical composition requires substantial investment in formulation, testing, and certification. These requirements can increase product development timelines and operational costs, particularly for smaller manufacturers. Regulatory uncertainty also creates barriers to market entry and limits the availability of certain chemical components, impacting product innovation and supply chain flexibility.

Opportunity Analysis - Growth of Bio-Based and Environmentally Acceptable Lubricants

The transition toward sustainable industrial practices is creating strong opportunities for bio-based and environmentally acceptable compressor oils. These products are designed to offer high performance while minimizing environmental impact through biodegradability and reduced toxicity. Industries operating in environmentally sensitive areas, such as marine, offshore, and food processing sectors, are increasingly adopting such lubricants to meet regulatory requirements and sustainability goals. Suppliers that can deliver both performance reliability and environmental compliance are well positioned to capture this growing segment.

Expansion of Manufacturing in Asia Pacific

Rapid industrialization and manufacturing growth in Asia Pacific are creating significant opportunities for compressor oil suppliers. Countries such as China, India, Japan, and those in Southeast Asia are witnessing strong demand for compressors across diverse industries, including automotive, electronics, chemicals, and food processing. The region’s cost advantages, expanding infrastructure, and supportive government policies are attracting global investments. As a result, lubricant manufacturers are strengthening their regional presence through local production and distribution networks to capitalize on this demand.

Rising Demand in Gas Compression and Hydrogen Infrastructure

The increasing focus on cleaner energy sources is driving investments in gas compression and hydrogen infrastructure. These applications require advanced compressor oils capable of handling high pressures, temperatures, and chemical exposure. The need for reliable and efficient lubrication in such critical systems creates opportunities for high-margin specialty products. As hydrogen and LNG projects scale globally, compressor oil suppliers can benefit from increased demand for technologically advanced formulations tailored to these applications.

Category-wise Analysis

Base Oil Type Insights

Synthetic compressor oils are anticipated to maintain their leadership, accounting for 42.1% of the market share in 2026. This dominance is driven by their superior performance characteristics, particularly in high-demand industrial environments. These oils are extensively used in rotary screw and reciprocating compressors across industries such as automotive manufacturing, petrochemicals, and heavy engineering, where continuous operation is critical. For instance, large-scale automotive plants and steel processing units rely on synthetic oils to ensure minimal downtime and extended maintenance intervals. Formulations based on PAO, PAG, and ester technologies provide enhanced resistance to oxidation, thermal degradation, and deposit formation, making them ideal for high-load and high-temperature conditions. Their ability to improve compressor efficiency, reduce energy consumption, and extend equipment life continues to position them as the preferred choice for high-performance applications.

Semi-synthetic and bio-based compressor oils are anticipated to witness accelerated adoption. This growth is supported by increasing environmental regulations and corporate sustainability initiatives. These oils are gaining traction in sectors such as food processing, marine operations, and pharmaceuticals, where environmental compliance and safety are critical. For example, food and beverage manufacturing facilities often adopt bio-based lubricants to minimize contamination risks, while marine operators use biodegradable oils to comply with environmental discharge regulations. Semi-synthetic oils offer a balanced performance profile, combining the durability of synthetic oils with the cost-effectiveness of mineral oils. Advancements in renewable base oil technologies are further improving their oxidation stability and load-bearing capacity, making them a viable alternative for a broader range of industrial applications.

Application Insights

Air compressors are anticipated to continue dominating the application segment, holding 71.3% of market share 2026. Their widespread use across manufacturing plants, construction sites, and industrial utilities ensures consistent demand for compressor oils. Air compressors are critical in applications such as powering pneumatic tools in assembly lines, operating conveyor systems in packaging facilities, and supporting HVAC systems in commercial buildings. For instance, automotive assembly plants and electronics manufacturing units rely heavily on compressed air systems for precision operations. The large installed base, combined with continuous usage, leads to regular oil replacement cycles, making this segment the backbone of the compressor oil market. The demand is further supported by increasing automation and the expansion of industrial infrastructure globally.

Gas compressors are anticipated to register the fastest growth. This growth is driven by rising investments in natural gas infrastructure, LNG terminals, and emerging hydrogen energy projects. Gas compressors are widely used in upstream oil & gas operations, gas transmission pipelines, and petrochemical processing plants. For example, LNG export facilities and cross-country gas pipeline networks require high-performance compressors operating under extreme pressure and temperature conditions. These applications demand specialized compressor oils with superior oxidation stability, low volatility, and excellent sealing properties to prevent gas leakage. Increasing regulatory focus on emission control and operational efficiency is further accelerating the adoption of advanced compressor oils in this segment.

Regional Insights

North America Compressor Oil Market Trends - High-Performance and Digitally Monitored Compressor Oils Driven by Industrial and Emission Standards

North America represents a mature yet high-value market for compressor oils, supported by a strong industrial base and an advanced regulatory framework, with steady growth projected over the forecast period. The U.S. dominates regional demand, driven by its extensive manufacturing sector, well-established oil & gas industry, and strong technological capabilities. High compressor utilization across sectors such as aerospace, automotive, chemicals, and food processing continues to sustain lubricant consumption.

The region’s regulatory environment plays a critical role in shaping market dynamics. Strict environmental and safety standards related to emissions, leak detection, and equipment efficiency are encouraging the adoption of high-performance compressor oils. For instance, regulatory enforcement around methane emissions in compressor stations has pushed operators to adopt advanced lubrication solutions that improve sealing efficiency and reduce leakage. This has directly benefited premium lubricant portfolios offered by companies such as Chevron Corporation and Exxon Mobil Corporation, which have introduced high-performance compressor oils designed for gas compression and emission-sensitive applications.

Investment trends in North America are increasingly focused on advanced lubricant technologies, including synthetic and environmentally acceptable oils. Companies are also integrating digital monitoring and predictive maintenance services into their offerings. For example, Shell plc has expanded its digital lubrication services, enabling real-time monitoring of lubricant performance and equipment health. This shift toward service-based models enhances customer value and strengthens long-term supplier relationships. The presence of leading lubricant manufacturers, combined with strong R&D capabilities, continues to position North America as a hub for innovation in compressor oil formulations.

Europe Compressor Oil Market Trends - Sustainable and Specialty Compressor Oils Shaped by Strict Environmental Regulations

Europe is characterized by a strong emphasis on sustainability, regulatory compliance, and technological innovation. Key markets include Germany, the U.K., France, and Spain, all of which have well-established industrial and manufacturing sectors. Demand for compressor oils in the region is closely tied to advance engineering industries, automotive production, and process manufacturing.

The regulatory landscape in Europe is among the most stringent globally, with a strong focus on environmental protection and energy efficiency. Policies promoting biodegradable, low-toxicity, and energy-efficient lubricants are accelerating the transition toward sustainable compressor oils. This regulatory push has encouraged companies such as FUCHS SE and TotalEnergies SE to expand their portfolios of environmentally acceptable lubricants. For example, FUCHS has continued to develop refrigeration compressor oils compatible with hydrocarbon refrigerants, aligning with Europe’s push toward low-global-warming-potential (GWP) cooling systems.

European companies are also investing heavily in research and development to enhance lubricant performance while meeting environmental standards. The region serves as a hub for specialty lubricants, particularly in refrigeration, food-grade applications, and high-precision industrial processes. Klüber Lubrication, for instance, focuses on high-performance specialty oils tailored for niche industrial applications where reliability and compliance are critical. These developments are reinforcing Europe’s position as a leader in sustainable and technically advanced lubricant solutions, while also creating opportunities for premium product differentiation.

Asia Pacific Compressor Oil Market Trends - Rapid Industrialization Driving Volume Growth and Shift toward Synthetic Compressor Oils

Asia Pacific is the largest and fastest-growing market for compressor oils, accounting for approximately 40.6% of market share. The region’s growth is driven by rapid industrialization, expanding manufacturing sectors, and increasing infrastructure development. Major markets include China, India, Japan, and Southeast Asian economies such as Indonesia and Vietnam.

The region benefits from cost advantages, a large labor force, and supportive government policies, making it a global manufacturing hub. This drives strong demand for compressors across industries such as automotive, electronics, chemicals, and food processing. For example, China’s large-scale industrial production and India’s “Make in India” initiative are significantly increasing the deployment of compressed-air systems, thereby boosting demand for compressor oils.

Investment in local manufacturing and supply chain development is accelerating as global players aim to strengthen their regional presence. A notable development is the expansion of lubricant production facilities by Exxon Mobil Corporation in India, aimed at meeting rising domestic and regional demand. Similarly, PETRONAS Lubricants International continues to expand its footprint across Asia, leveraging its regional base to supply high-performance industrial lubricants.

The adoption of advanced lubricant technologies is also rising, particularly in high-performance and export-oriented manufacturing sectors. Japanese manufacturers, known for precision engineering, are increasingly using synthetic compressor oils to enhance equipment reliability and efficiency. As industries in Asia Pacific move up the value chain, demand is shifting from basic mineral oils to premium and sustainable formulations. This transition creates significant growth opportunities for both global and regional players, particularly in synthetic and bio-based compressor oil segments.

Competitive Landscape

The global compressor oil market is fragmented, with numerous global and regional players competing across different segments. While large multinational companies dominate the premium segment, regional manufacturers play a significant role in supplying cost-effective solutions. Competition is driven by product performance, pricing strategies, distribution networks, and technical support capabilities. Companies differentiate themselves through innovation, OEM approvals, and value-added services.

Key players are focusing on product innovation, sustainability, and global expansion. Strategies include developing high-performance synthetic and bio-based lubricants, strengthening OEM partnerships, and offering technical services to enhance customer value. Companies are also investing in regional production facilities and digital solutions to improve supply chain efficiency and customer engagement.

Key Industry Developments:

- In May 2025, Lubrication Engineers, Inc. announced the acquisition of RSC Bio Solutions, aiming to strengthen its portfolio of environmentally acceptable lubricants and expand its presence in marine and industrial compressor applications focused on sustainability-driven demand.

Companies Covered in Compressor Oil Market

- Shell plc

- Exxon Mobil Corporation

- Chevron Corporation

- TotalEnergies SE

- FUCHS SE

- BP p.l.c.

- PETRONAS Lubricants International

- Idemitsu Kosan Co., Ltd.

- Klüber Lubrication

- Indian Oil Corporation Limited

- China Petroleum & Chemical Corporation (Sinopec)

- Lukoil

- Phillips 66

- Valvoline Inc.

- Lubrication Engineers, Inc.

- RSC Bio Solutions

Frequently Asked Questions

The global compressor oil market is estimated to be valued at US$ 8.2 billion in 2026.

The compressor oil market is projected to reach US$ 11.5 billion by 2033.

Key trends include the shift toward synthetic and bio-based lubricants, increasing focus on energy efficiency and longer drain intervals, and rising demand from gas compression and LNG infrastructure. There is also growing adoption of environmentally compliant and low-emission lubricant solutions.

By base oil type, synthetic compressor oils lead the market with a 42.1% share, driven by their superior thermal stability and performance in demanding industrial environments.

The compressor oil market is expected to grow at a CAGR of 4.9% between 2026 and 2033.

Some of the major players include Shell plc, Exxon Mobil Corporation, Chevron Corporation, TotalEnergies SE, and FUCHS SE.