- Specialty & Fine Chemicals

- Surfactants Market

Surfactants Market Size, Share, and Growth Forecast 2026 - 2033

Surfactants Market by Source (Petroleum, Biobased), Product Type (Non-Ionic Surfactants Amphoteric Surfactants, and Others), Application (Homecare, Personal Care, I&I Cleaners, Food Processing, and Others), and Regional Analysis for 2026 - 2033

Surfactants Market Size and Trend Analysis

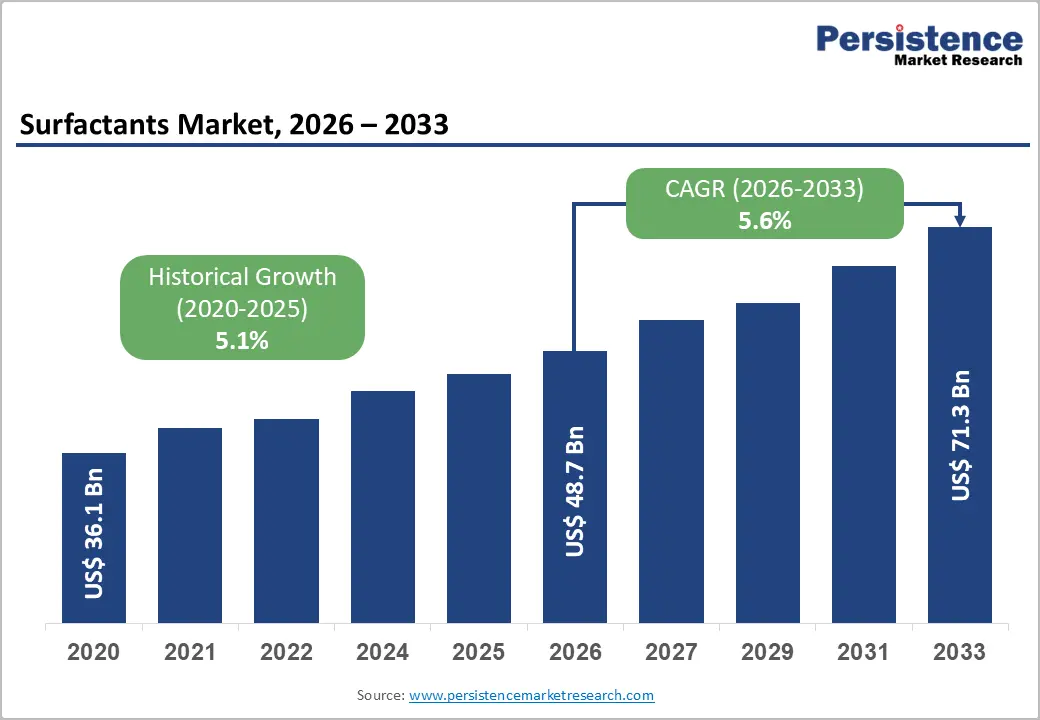

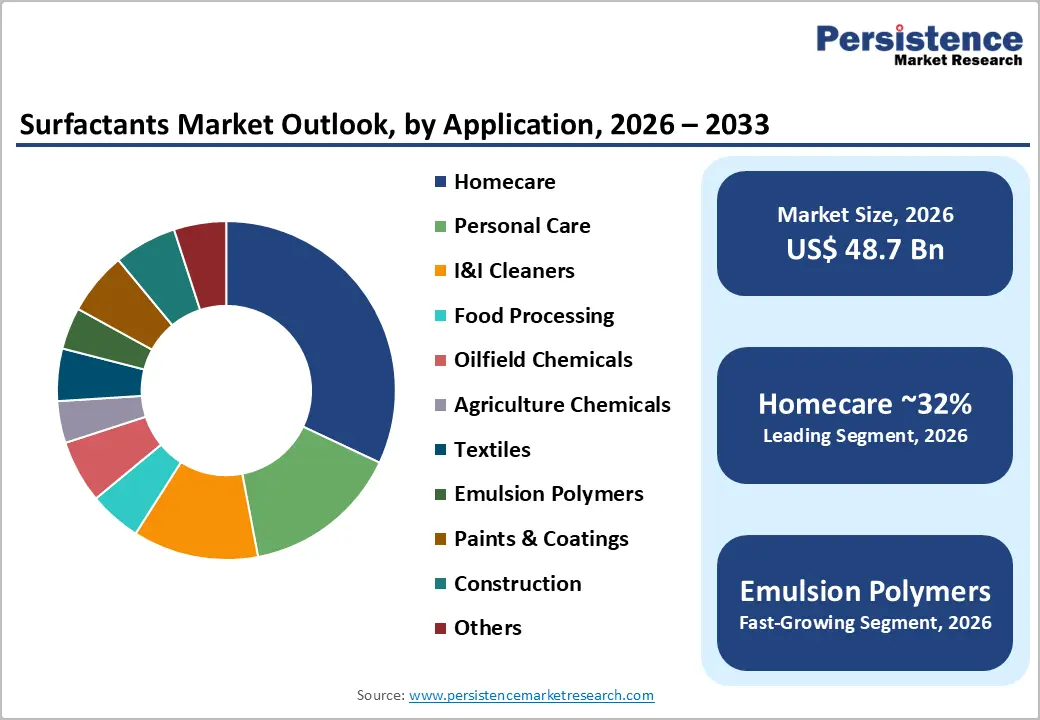

The global Surfactants Market size is estimated to be valued at US$ 48.7 Bn in 2026 and is projected to reach US$ 71.3 Bn by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

This sustained growth trajectory reflects the essential role of surfactants as critical formulation enablers across household cleaning products, personal care formulations, industrial processing applications, and agricultural chemical delivery systems. Regulatory-driven product reformulation toward bio-based alternatives, coupled with emerging applications in enhanced oil recovery and precision agriculture, ensures multi-year consumption momentum across both mature and developing economies.

Key Industry Highlights:

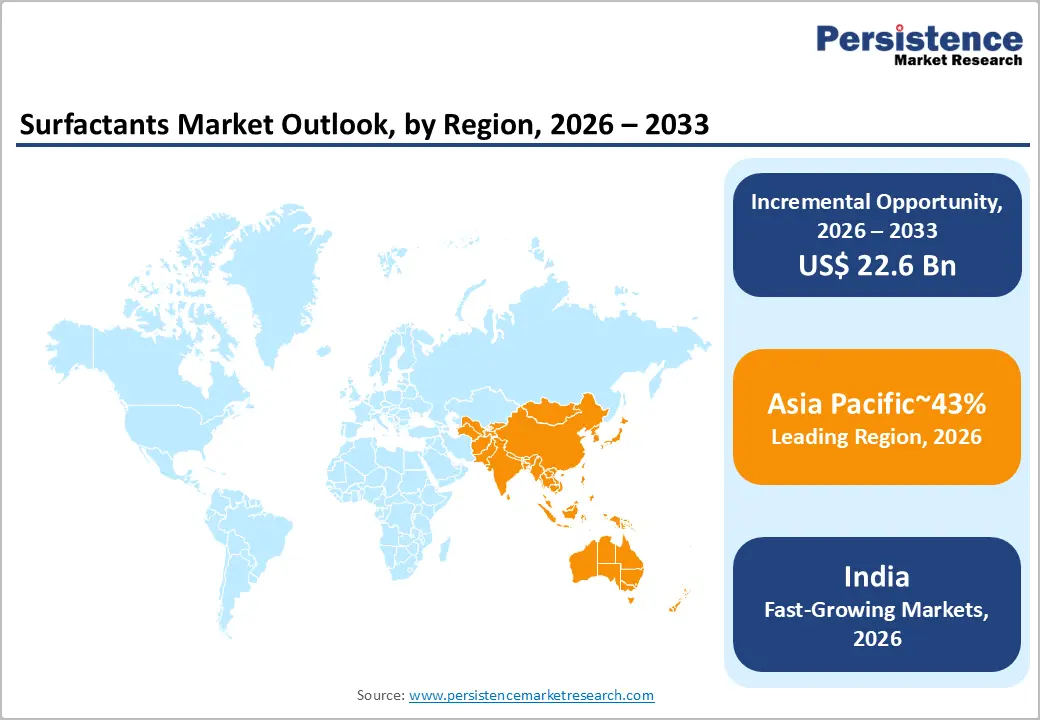

- Leading Region: Asia Pacific leads the global Surfactants Market, driven by China, India, and Indonesia representing 65% of regional volume with Sinopec and Godrej Industries adding 450,000 metric tons of capacity since 2022.

- Growing Country: India is the fastest-growing region, exhibiting 6.6% CAGR driven by urbanization elevating household cleaning penetration from 45% toward mature market 85% benchmarks.

- Dominant Product Type: Non-Ionic Surfactants dominate the Product Type segment at 43% revenue share in 2026, led by alcohol ethoxylates (AE) representing 28% of global non-ionic consumption per CESIO statistics.

- Leading Application: Homecare applications lead at 32% of Application revenue, consuming 14.5 billion pounds annually in U.S. cleaning products per ACI, with concentrated formulations elevating surfactant loading to 22% per unit.

- Key Market Opportunity: Bio-based surfactants represent the key opportunity, with EU Green Deal mandating 65% household products containing 50%+ bio-content by 2030 and Unilever documenting 25% sales premium for bio-based formulations.

| Key Insights | Details |

|---|---|

|

Surfactants Market Size (2026E) |

US$ 48.7 Bn |

|

Market Value Forecast (2033F) |

US$ 71.3 Bn |

|

Projected Growth CAGR (2026-2033) |

5.6% |

|

Historical Market Growth (2020-2025) |

5.1% |

DRO Analysis

Drivers - Consumer Goods Volume Expansion and Household Cleaning Penetration Driving Surfactant Demand

The structural growth in global household and personal care product consumption represents the most direct and measurable demand driver for the Surfactants Market, as every unit of laundry detergent, dishwashing liquid, shampoo, and body wash requires precisely engineered surfactant blends to achieve wetting, foaming, and cleaning performance targets. This relationship ensures that consumer goods volume growth translates directly into proportional surfactant procurement across all major product categories.

According to cited online studies, global household care product retail sales reached US$ 300 billion in 2023, with laundry care alone representing 45% of total category volume. The International Labour Organization (ILO) estimates that over 2.5 billion people across developing economies have achieved middle-income status since 2000, driving unprecedented household cleaning product adoption and creating structurally additive surfactant demand from emerging markets. In parallel, premiumization trends in North America and Europe have elevated average surfactant loading per unit from 15% to 22% in high-performance formulations, amplifying consumption intensity even as unit volumes remain stable.

Industrial Processing Applications and Enhanced Oil Recovery Expanding Specialty Surfactant Volumes

The proliferation of surfactants in industrial applications, including enhanced oil recovery (EOR), emulsion polymerization, and agricultural adjuvant formulations, represents a high-value, structurally resilient demand vector for the Surfactants Market. These mission-critical applications require precisely engineered surfactant chemistries with performance characteristics unattainable by conventional formulations.

The U.S. Energy Information Administration (EIA) reported that 1.2 million barrels per day of additional U.S. oil production in 2023 was attributable to enhanced recovery techniques, each barrel requiring specialized surfactant-polymer flooding systems. The Food and Agriculture Organization (FAO) documents that surfactant-based adjuvant technology has increased pesticide delivery efficiency by 30-50%, compelling agricultural chemical manufacturers to integrate higher surfactant loadings into formulations. Global emulsion polymerization capacity reached 15 million metric tons in 2024 according to industry capacity disclosures, with anionic and non-ionic surfactants representing 8-12% of total formulation costs across paints, adhesives, and paper coating applications.

Restraints - Regulatory Restrictions on Nonylphenol Ethoxylates and Linear Alkylbenzene Sulfonates Constraining Conventional Formulations

Stringent environmental regulations targeting persistent aquatic toxins have systematically restricted the use of certain high-volume synthetic surfactants, compelling costly reformulation across multiple end-use applications. The U.S. Environmental Protection Agency (EPA) banned nonylphenol ethoxylates (NPEs) in all textiles wet processing applications effective 2024, while the European Union's REACH regulation limits NPE concentrations to 0.01% across the supply chain. These restrictions have forced manufacturers to qualify alternative chemistries through 12–18-month stability and performance validation cycles, creating supply chain friction and elevated formulation costs that suppress margin expansion across the conventional surfactant segment.

Petroleum Feedstock Price Volatility Impacting Production Economics

The surfactants market's cost structure remains structurally exposed to petroleum-derived feedstock price fluctuations, such as ethylene oxide, linear alkylbenzene, and fatty alcohol precursors represent 60-75% of total production costs for conventional synthetic surfactants. According to the U.S. Energy Information Administration (EIA), West Texas Intermediate crude oil prices fluctuated between US$ 65-85 per barrel throughout 2024, generating corresponding 15-20% swings in ethylene oxide spot pricing that directly pass through to finished surfactant pricing. This volatility disrupts long-term contract pricing stability, compels working capital investment in inventory buffers, and erodes manufacturer margins during sustained high-cost periods, constraining capacity expansion investments and new product development initiatives.

Opportunities - Bio-Based Surfactant Innovation Addressing Sustainability Mandates and Consumer Premiumization

The convergence of tightening environmental regulations, corporate sustainability commitments, and consumer willingness to pay premiums for "green" cleaning products creates a high-value structural opportunity for next-generation bio-based surfactants within the Surfactants Market. These renewably sourced alternatives deliver equivalent performance with measurably lower lifecycle carbon footprints and aquatic toxicity profiles.

Unilever disclosed that its 100% bio-based surfactant laundry detergent achieved 25% higher sales velocity versus conventional formulations in European test markets during 2024. The European Union's Green Deal mandates that 65% of household cleaning products must contain 50% or more bio-based ingredients by 2030, creating a clear regulatory pathway for market share displacement. Oleochemical-derived methyl ester sulfonates (MES) and alkyl polyglucosides (APG) demonstrate 95% biodegradability within 28 days per OECD 301 testing protocols, positioning them as direct substitutes for synthetic anionics in laundry and personal care applications. Leading producers including BASF SE, Evonik Industries AG, and Cargill have announced multi-year bio-based surfactant capacity expansions targeting this regulatory- and consumer-driven transition opportunity.

Precision Agriculture and Controlled-Release Pesticide Formulations Expanding Agricultural Adjuvant Demand

The agricultural chemicals sector's transition toward precision delivery systems and controlled-release formulations represents a structurally additive, high-margin growth opportunity for specialized surfactant producers serving the global crop protection market. These advanced adjuvant systems enable 30-50% pesticide active ingredient reduction while maintaining equivalent field efficacy.

The Food and Agriculture Organization (FAO) projects that global pesticide consumption will reach 4.2 million metric tons by 2030, with adjuvant surfactants representing 10-15% of total formulation costs. Corteva Agriscience and Syngenta have commercialized microencapsulation technologies requiring amphoteric and polymeric surfactants for controlled-release stability, creating demand for high-performance chemistries beyond conventional tank-mix adjuvants. The U.S. Department of Agriculture (USDA) Section 18 emergency exemption program approved surfactant-enhanced pesticide applications across 15 million acres of specialty crops in 2024, quantifying the scale of near-term agricultural adjuvant demand acceleration.

Category-wise Analysis

Source Insights

Petroleum-based surfactants maintain dominant market position, accounting for approximately 72% of total Source segment revenue in 2026. This leadership reflects decades of optimized manufacturing infrastructure, validated performance across diverse applications, and cost economics that remain unmatched by current bio-based alternatives. According to American Cleaning Institute (ACI) production statistics, petroleum-derived linear alkylbenzene sulfonates (LAS) and alcohol ethoxylates (AE) represent 65% of total U.S. surfactant volume, with LAS alone consuming 11 billion pounds annually for laundry detergent applications. The chemical industry's 99% capacity utilization rates for ethylene oxide and fatty alcohol production ensure supply reliability that bio-based feedstocks cannot currently match at equivalent scale and cost structure.

Product Type Insights

Non-Ionic Surfactants command the leading position within the Product Type segmentation, holding approximately 43% of total Product Type revenue in 2026. This dominance stems from non-ionic surfactants' unparalleled formulation versatility across cleaning, personal care, and industrial applications, where pH-neutral performance, temperature stability, and compatibility with diverse chemical matrices are paramount. Alcohol ethoxylates (AE) alone represent 28% of global non-ionic consumption according to CESIO statistics, with cloud point engineering enabling precise control of detergency, wetting, and emulsification characteristics. The Cloud Point Index (CPI) metric demonstrates that C12-C15 AE with 7-9 moles EO achieves optimal performance across laundry, dishwashing, and hard surface cleaning applications simultaneously.

Application Insights

Homecare applications lead the Application segmentation, accounting for approximately 32% of total Application segment revenue in 2026. Laundry detergents, dishwashing liquids, and household hard surface cleaners represent the highest-volume surfactant consumption categories globally, with the American Cleaning Institute (ACI) reporting that U.S. households consumed 14.5 billion pounds of cleaning products containing surfactants in 2023. High-active concentrated formulations have elevated average surfactant loading from 15% to 22% per unit volume, amplifying consumption intensity. Procter & Gamble and Unilever sustainability disclosures confirm that homecare remains their largest surfactant procurement category, with cold water cleaning formulations requiring non-ionic surfactant blends optimized for low-temperature performance.

Regional Insights

North America Surfactants Trends & Insights

North America maintains leadership in high-performance surfactant innovation and specialty chemical applications, anchored by the world's largest consumer goods companies and most stringent environmental regulations driving product reformulation. The U.S. Environmental Protection Agency (EPA) Safer Choice program has certified over 2,500 cleaning products using approved surfactants since 2015, compelling Procter & Gamble, Unilever, and SC Johnson to qualify bio-based alternatives through rigorous aquatic toxicity and biodegradation testing protocols.

BASF SE's Geismar, Louisiana facility expansion and Dow Inc.'s Freeport, Texas site upgrades have reinforced North American production capacity for alcohol ethoxylates and specialty anionics serving institutional cleaning markets. The American Cleaning Institute (ACI) 2024 Sustainability Report documents that 72% of U.S. laundry detergents now contain bio-based surfactants, with methyl ester sulfonates (MES) gaining traction as LAS replacements in 35 states under state-level environmental procurement guidelines.

Europe Surfactants Trends & Insights

Europe represents the global benchmark for surfactant sustainability and regulatory harmonization, with the European Union's REACH regulation and Green Deal industrial strategy systematically reshaping product chemistry across the entire value chain. Germany, France, and the Netherlands collectively account for 45% of European surfactant consumption, driven by premium personal care exports and institutional cleaning specifications.

The European Chemicals Agency (ECHA) has restricted nonylphenol ethoxylates (NPE) to 0.01% concentration limits across the supply chain, compelling Henkel, Reckitt Benckiser, and Unilever to reformulate 85% of their European cleaning portfolios with alkyl polyglucosides (APG) and alcohol ethoxylates (AE). Clariant AG's Burgkirchen, Germany facility produces fatty acid esters specifically engineered for cold-water detergency performance mandated by EU Ecolabel criteria. The COSMA industry association reports that 62% of Western European laundry formulations now achieve 60% bio-based content, positioning the region as the global innovation leader for sustainable surfactant systems.

Asia Pacific Surfactants Trends & Insights

Asia Pacific drives unmatched volume growth across laundry, personal care, and agricultural chemical applications, anchored by China, India, and Indonesia representing 65% of regional consumption. China's State Council "Beautiful China" environmental action plan has accelerated surfactant production capacity additions, with Sinopec and Wanhua Chemical commissioning 450,000 metric tons of alcohol ether sulfate (AES) capacity since 2022.

India's Godrej Industries reported 18% compound annual revenue growth from surfactants serving Unilever India and Procter & Gamble India, with linear alkylbenzene (LAB) consumption reaching 1.2 million metric tons annually. Japan's Kao Corporation maintains technology leadership in non-ionic surfactant cloud point engineering, while ASEAN markets including Indonesia, Vietnam, and Thailand exhibit 12% annual growth rates driven by urbanization and rising disposable incomes fueling household cleaning product penetration from current levels of 45% toward mature market benchmarks of 85%.

Competitive Landscape

The global Surfactants Market exhibits moderate consolidation at the commodity surfactant tier while remaining highly fragmented across specialty and bio-based formulations. BASF SE, Evonik Industries AG, Solvay S.A., Dow Inc., and Clariant AG form the leadership tier, differentiated by integrated petrochemical-to-surfactant value chains, global application development laboratories, and multi-year customer qualification cycles. These majors prioritize bio-based surfactant R&D, cold-water cleaning technology platforms, and digital formulation design capabilities. Regional players including Godrej Industries and Galaxy Surfactants compete effectively in Asia serving local consumer goods majors. Emerging models encompass surfactant-as-a-service for institutional cleaning and AI-optimized custom blend development.

Key Developments:

- In June 2024, BASF SE launched its Glucopon 600 CSUP alkyl polyglucoside surfactant, achieving 60% bio-based content and 28-day ready biodegradability per OECD 301 standards, targeting premium European laundry detergent formulations.

- In March 2024, Evonik Industries AG commercialized Tegosurf CAD, a new cationic surfactant for hair conditioning applications delivering 40% improved wet combing performance versus conventional quaternary compounds.

- In November 2023, Dow Inc. expanded its alcohol ethoxylate production capacity by 50,000 metric tons at its Freeport, Texas facility to serve growing North American institutional cleaning and agricultural adjuvant demand.

Companies Covered in Surfactants Market

- Akzonobel N.V

- BASF SE

- Evonik Industries AG

- Solvay S.A

- Clariant AG

- Huntsman International LLC

- Dow Inc.

- Kao Corporation

- Henkel Adhesives Technologies India Private Limited

- Bayer AG

- Godrej Industries Limited

- Stepan Company

- Croda International

- Galaxy Surfactants

- Arkema

Frequently Asked Questions

The global Surfactants Market is valued at US$ 48.7 Bn in 2026 and projected to reach US$ 71.3 Bn by 2033, registering a 5.6% CAGR during 2026-2033. The market achieved a historical 5.1% CAGR from 2020-2025, reflecting resilient structural demand from consumer goods and industrial applications.

Euromonitor reports US$ 300 billion in global household care sales, with laundry representing 45% of category volume. 2.5 billion middle-income consumers drive unprecedented cleaning product adoption, while EIA confirms 1.2 million barrels/day additional U.S. oil production from surfactant-enabled enhanced recovery techniques.

Non-Ionic Surfactants lead with 43% Product Type revenue share in 2026. Alcohol ethoxylates (AE) represent 28% of global non-ionic consumption per CESIO statistics, valued for pH-neutral performance across laundry, dishwashing, and industrial cleaning applications.

Asia Pacific leads driven by China, India, and Indonesia representing 65% regional volume. Godrej Industries achieved 18% CAGR serving Unilever India, while Sinopec added 450,000 metric tons AES capacity since 2022 under "Beautiful China" environmental initiatives.

Bio-based surfactants offer maximum opportunity as EU Green Deal mandates 65% household products with 50%+ bio-content by 2030. Unilever achieved 25% sales premium with 100% bio-based detergents, positioning renewably sourced APG and MES for regulatory-driven market displacement.

BASF SE, Evonik Industries AG, Dow Inc., Solvay S.A., Clariant AG, Stepan Company, Godrej Industries, Kao Corporation, Croda International, Galaxy Surfactants, Arkema, Huntsman International, Akzonobel N.V, and Henkel lead across commodity, specialty, and bio-based surfactant platforms globally.