- Specialty & Fine Chemicals

- Diamond Coatings Market

Diamond Coatings Market Size, Share, and Growth Forecast, 2026 - 2033

Diamond Coatings Market by Technology (CVD, PVD, Others), Substrates (Metal, Ceramic, Others), End-use Industry, Coating Types, and Regional Analysis for 2026 - 2033

Diamond Coatings Market Size and Trends Analysis

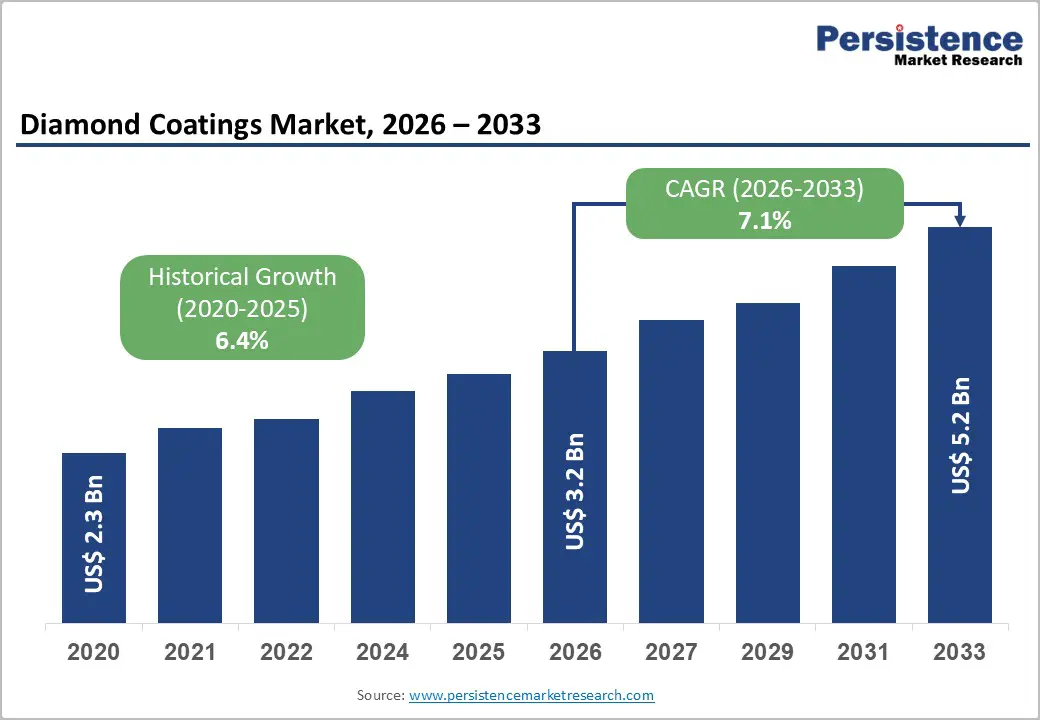

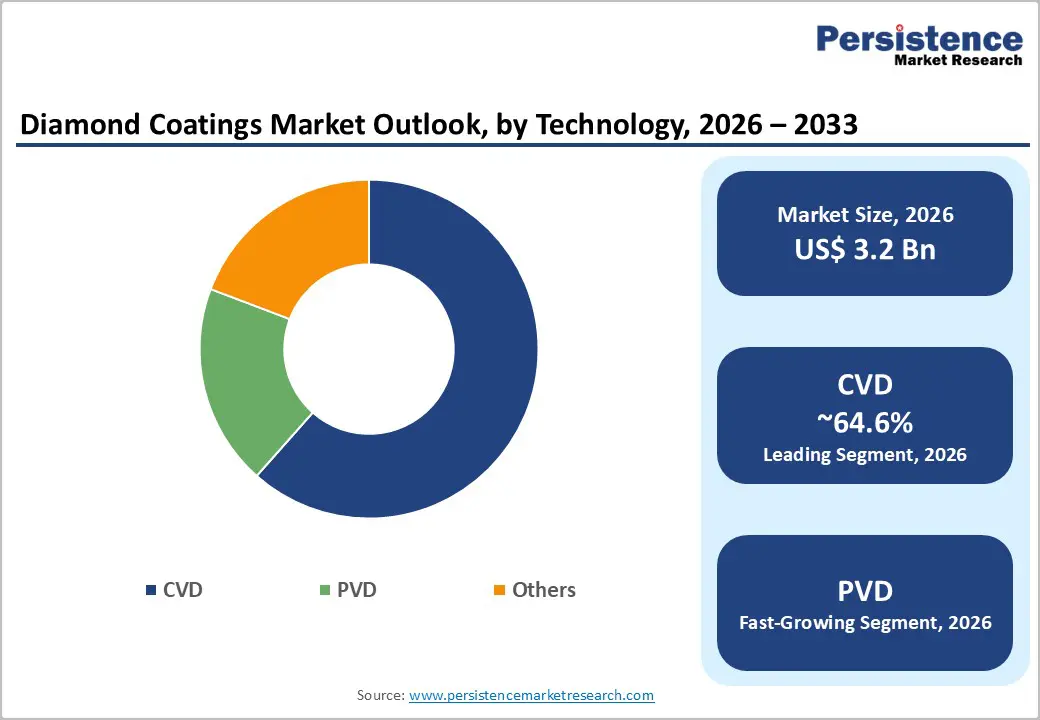

The global diamond coatings market size is likely to be valued at US$3.2 billion in 2026 and is expected to reach US$5.2 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033, driven by rising demand for low-friction, wear-resistant, and thermally stable coatings across semiconductors, electric mobility, precision tooling, and medical devices.

Growth is supported by the superior properties of diamond coatings, including extreme hardness, chemical inertness, corrosion resistance, and high thermal conductivity, enabling broad use across aerospace, electronics, cutting tools, composites, and healthcare applications. Technological advancements in CVD coatings, along with expanding adoption of PVD and hybrid carbon-based coatings, are further shaping market expansion.

Key Industry Highlights:

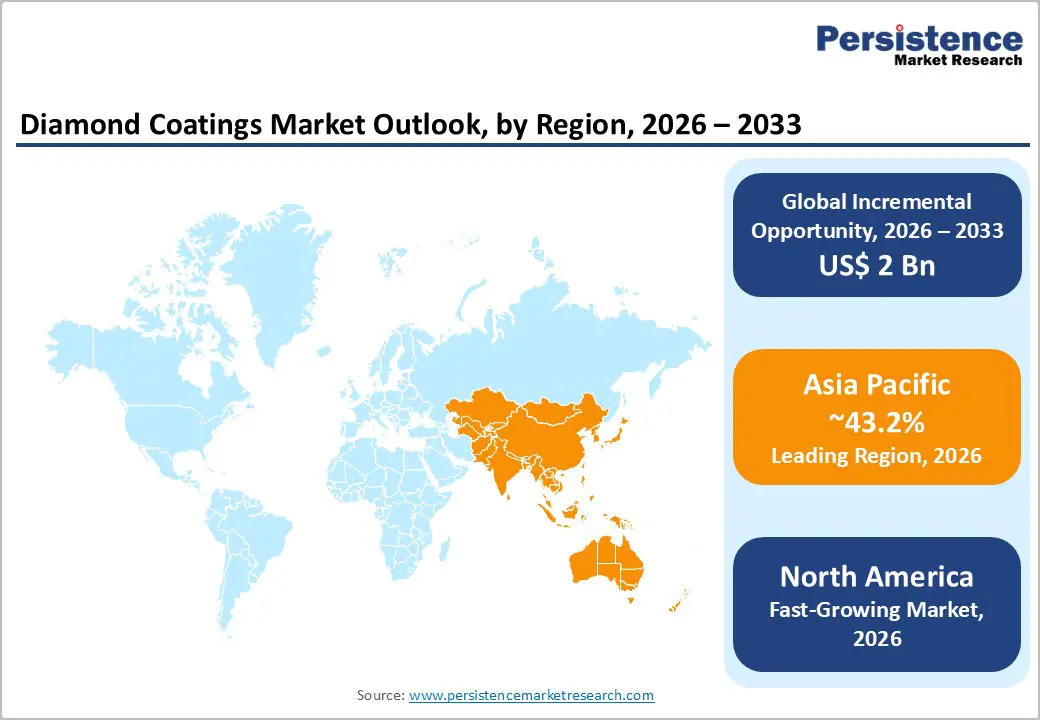

- Leading Region: Asia Pacific is projected to account for approximately 43.2% of the market share, supported by large-scale manufacturing, strong semiconductor production, and rapid expansion in the automotive and electronics industries.

- Fastest-growing Region: North America is the fastest-growing region, driven by rising investments in semiconductor manufacturing, advanced packaging, and electric vehicle production.

- Investment Plans: The market is witnessing increased investments in advanced manufacturing and coating technologies, particularly in semiconductor infrastructure and EV supply chains, with multi-billion-dollar funding initiatives in North America and expanding coating facility investments across the Asia Pacific.

- Dominant Technology: CVD technology leads the market with an estimated 64.6% share, owing to its superior hardness, wear resistance, and suitability for high-performance machining applications involving composites and ceramics.

- Leading Substrate: Metal substrates hold the leading position with an estimated 39.7% share, driven by their extensive use in industrial tools, automotive components, and aerospace applications, where durability and coating compatibility are critical.

| Key Insights | Details |

|---|---|

| Diamond Coatings Market Size (2026E) | US$3.2 Bn |

| Market Value Forecast (2033F) | US$5.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

DRO Analysis

Driver Analysis - Rising Semiconductor Complexity and Advanced Manufacturing Requirements

The semiconductor industry is undergoing rapid transformation, driven by miniaturization and advanced packaging technologies. These developments require high-precision tooling, improved wear resistance, and stable thermal performance, all of which are enabled by diamond coatings. As fabrication processes become more complex, manufacturers rely on coatings that ensure consistent process control and reduced contamination risks. This trend elevates diamond coatings from a supporting material to a critical enabler of semiconductor manufacturing efficiency. As a result, suppliers with capabilities aligned to semiconductor ecosystems are positioned to capture higher-value opportunities.

Expansion of Electric Vehicle Production and Component Durability Needs

The transition toward electric mobility is significantly influencing the demand for diamond coatings. EV components, such as bearings, gears, motor assemblies, and thermal systems, require coatings that reduce friction and enhance durability under high-stress conditions.

Diamond and diamond-like coatings help improve energy efficiency, extend component lifespan, and reduce maintenance requirements. This demand extends beyond automakers to include battery manufacturers, component suppliers, and precision tooling providers. As EV production scales globally, the integration of advanced coatings is expected to increase across the entire value chain.

Growing Adoption in Advanced Material Machining

The increasing use of composites, ceramics, and lightweight materials in aerospace, medical, and industrial applications is driving demand for diamond-coated tools. These materials are difficult to machine using conventional tools due to high wear rates and surface finish requirements. Diamond coatings enable longer tool life, improved cutting precision, and reduced downtime, resulting in measurable productivity gains. This trend is shifting diamond coatings from optional enhancements to essential components in high-performance manufacturing environments.

Restraint Analysis - High Capital Investment and Process Complexity

Diamond coating technologies require specialized deposition equipment, controlled environments, and technical expertise, leading to high initial investment costs. The need for precise process control increases operational complexity, particularly for smaller manufacturers. This cost barrier can delay adoption, especially in price-sensitive markets where the return on investment must be clearly demonstrated through extended tool life and efficiency gains.

Substrate Compatibility and Operational Limitations

Diamond coatings are not universally compatible with all substrates and operating conditions. Variations in temperature tolerance, adhesion properties, and material compatibility require customized coating solutions. This increases development time and testing requirements, particularly in industries with strict certification standards. These limitations can slow market penetration in applications requiring high repeatability and reliability.

Opportunity Analysis - Growth in Semiconductor Packaging and High-Value Electronics Applications

Advancements in semiconductor packaging and electronics manufacturing are creating opportunities for diamond coatings in thermal management, precision tooling, and surface protection. As production volumes increase and designs become more complex, manufacturers are seeking coatings that enhance performance and reliability. This creates a pathway for suppliers to move into higher-margin, application-specific solutions.

Rising Demand across EV Supply Chains

The global expansion of EV production presents a strong opportunity for diamond coatings in powertrain components, battery systems, and manufacturing tools. Coatings that improve efficiency and reduce wear are becoming critical for achieving performance and cost targets. Suppliers that can demonstrate consistent quality and durability are likely to benefit from long-term supply agreements within EV ecosystems.

Increased Use of Composites and Advanced Engineering Materials

Industries such as aerospace and medical devices are rapidly adopting lightweight and high-performance materials, which require specialized machining solutions. Diamond coatings offer the durability and precision needed for these applications, creating opportunities to standardize coated tools in advanced manufacturing processes. This shift is expected to significantly expand the addressable market.

Category-wise Analysis

Technology Insights

CVD technology is expected to dominate the market, accounting for an anticipated 64.6% share in 2026, due to its strong suitability for high-performance industrial applications. CVD coatings provide exceptional hardness, adhesion, and wear resistance, making them ideal for cutting tools used in machining carbon fiber-reinforced polymers (CFRPs), graphite, and advanced ceramics. For instance, CVD diamond-coated drills and end mills are widely used in aerospace manufacturing for machining composite airframe components, where tool wear is a critical constraint. Their ability to produce uniform, high-quality coatings ensures consistent performance in demanding, high-volume production environments.

PVD technology is anticipated to be the fastest-growing segment, driven by its adaptability in precision applications and lower-temperature processing capabilities. PVD and related technologies enable coating complex geometries and temperature-sensitive substrates, expanding their use in semiconductor tooling, surgical instruments, and EV components, such as bearings and fuel injection systems. For example, DLC coatings deposited via PVD are increasingly used in automotive engine parts to reduce friction and improve fuel efficiency. Other technologies, including hybrid carbon-based coatings, are evolving to balance hardness, lubricity, and flexibility, particularly in applications requiring both wear resistance and smooth surface interaction.

Substrates Insights

Metal substrates are expected to lead the market, with an anticipated share of 39.7% in 2026, as they form the foundation for most industrial tools and mechanical components. Metals such as steel, aluminum, and titanium are widely used across the automotive, aerospace, and general manufacturing industries, making them prime candidates for diamond coatings. For example, diamond-coated carbide cutting tools are widely applied in automotive engine block machining and aerospace structural component manufacturing, where durability and precision are essential. Their compatibility with established coating processes further strengthens their dominance in large-scale industrial applications.

Ceramic substrates are likely to be the fastest-growing segment, driven by their increasing use in high-temperature, high-wear, and chemically aggressive environments. Ceramics offer superior thermal stability and hardness, making them suitable for applications such as semiconductor wafer handling components, medical implants, and high-speed cutting tools. Composite substrates are also gaining traction, particularly in aerospace and automotive sectors, where materials such as CFRPs and glass fiber composites require specialized coated tools for efficient machining. This shift toward advanced materials is accelerating the adoption of diamond coatings across non-metal substrates.

Regional Insights

North America Diamond Coatings Market Trends - Semiconductor Expansion and Precision Engineering Demand

North America is expected to be the fastest-growing regional market, driven by strong investments in semiconductor manufacturing, aerospace innovation, and advanced industrial technologies. The U.S. leads the region with a well-established ecosystem spanning aerospace, defense, medical devices, and electronics manufacturing. Government-backed initiatives to strengthen domestic semiconductor production are accelerating demand for high-performance coatings used in wafer fabrication tools, precision machining, and inspection systems. For example, companies such as Applied Materials and Intel Corporation are expanding advanced manufacturing capabilities, indirectly boosting demand for wear-resistant and thermally stable coating solutions used in tooling and production environments.

The region benefits from strong R&D infrastructure and early adoption of advanced materials, enabling faster commercialization of diamond coating technologies. In the automotive sector, companies like Tesla, Inc. are scaling EV production, increasing demand for coatings on drivetrain components and manufacturing tools. In aerospace, Boeing continues to drive demand for diamond-coated tools used in machining lightweight composite structures. While high adoption costs remain a constraint, North America’s focus on performance optimization, precision engineering, and lifecycle cost reduction supports premium pricing and long-term supplier partnerships.

Europe Diamond Coatings Market Trends - Sustainability-Driven Manufacturing and Advanced Engineering Integration

Europe remains a mature and technologically advanced market, supported by strong industrial capabilities, regulatory frameworks, and a deep-rooted engineering base. Countries such as Germany, the U.K., France, and Spain play a central role in driving demand across automotive, aerospace, and precision manufacturing sectors. Germany, in particular, anchors the region’s industrial strength, with companies such as Robert Bosch GmbH and BMW Group integrating advanced coatings into high-performance components and tooling systems.

The region’s emphasis on sustainability and emissions reduction is accelerating EV adoption, thereby increasing demand for diamond coatings in powertrain systems, battery manufacturing tools, and precision components. For instance, Volkswagen AG has expanded its EV production capacity across Europe, driving the need for durable and low-friction coatings in manufacturing processes. In aerospace, Airbus relies heavily on diamond-coated tools for machining advanced composites used in aircraft structures.

Europe also benefits from a strong presence of coating specialists such as OC Oerlikon and Ionbond, which continue to invest in localized coating centers and advanced surface technologies. These developments support innovation in high-precision machining, medical devices, and advanced materials processing, reinforcing Europe’s position as a key technology hub.

Asia Pacific Diamond Coatings Market Trends - High-Volume Manufacturing and Electronics-Led Market Dominance

Asia Pacific leads the global diamond coatings market with an estimated 43.2% share, driven by its position as the world’s largest manufacturing hub. Countries such as China, Japan, India, and Southeast Asian economies are experiencing rapid industrialization and expansion in electronics, automotive, and heavy manufacturing sectors. China remains a dominant force, with companies like BYD Company Ltd. and Huawei Technologies expanding production capabilities in EVs and electronics, both of which require advanced coating solutions for precision components and manufacturing tools.

Japan continues to contribute through advanced materials and precision engineering, with firms such as Sumitomo Electric Industries and Kyocera Corporation focusing on innovations in diamond tooling and coatings. In India, increasing investments in manufacturing and automotive production are creating new opportunities; for example, Tata Motors is expanding its EV portfolio, indirectly driving demand for coatings in component manufacturing and tooling.

The region’s strength lies in high-volume production, cost advantages, and integrated supply chains, which enable rapid adoption of diamond coatings across industries. Coating providers are also expanding local operations; for instance, Oerlikon’s investment in India and Southeast Asia strengthens regional service capabilities. Despite pricing pressures, Asia Pacific continues to attract global investment due to its scale, manufacturing efficiency, and strong demand from the semiconductor and EV industries, ensuring sustained market leadership.

Competitive Landscape

The global diamond coatings market is fragmented, with a mix of global leaders and regional specialists. Leading companies maintain a competitive advantage through technological expertise, broad application portfolios, and global service networks. Smaller players focus on niche applications and regional markets, contributing to a diverse competitive environment.

Key players focus on innovation, geographic expansion, and application-specific solutions. Emphasis is placed on developing advanced coatings, strengthening regional presence, and offering integrated services that combine coating technology with engineering expertise.

Key Industry Developments:

- In June 2025, Oerlikon Balzers announced the launch of BALDIA VARIA, an advanced CVD diamond coating designed for machining composites, ceramics, and graphite materials. The product enhances tool life, enables progressive wear monitoring, and improves machining efficiency across aerospace, medical, and industrial applications, strengthening the company’s high-performance coating portfolio.

- In July 2025, Oerlikon Metco launched Surface Two™, an IIoT-enabled thermal spray platform, designed to enhance automation, scalability, and coating efficiency. While focused on thermal spray, this development complements advanced surface engineering capabilities, including diamond coating applications in industrial manufacturing.

Companies Covered in Diamond Coatings Market

- OC Oerlikon

- Element Six

- Ionbond

- Kyocera Corporation

- Weber Technologies GmbH

- Materion Corporation

- Calico Coatings

- Japan Coating Center Co., Ltd.

- Toyo Advanced Technologies Co., Ltd.

- Beijing Worldia Diamond Tools Co., Ltd.

- Sumitomo Electric Industries

- Geomatec Co., Ltd.

- SP3 Diamond Technologies

- Diamond Materials GmbH

- Advanced Diamond Technologies

- NeoCoat SA

Frequently Asked Questions

The global diamond coatings market is estimated to be valued at US$3.2 billion in 2026.

The diamond coatings market is projected to reach US$5.2 billion by 2033.

Key trends include the rising adoption of CVD diamond coatings in advanced machining, increasing demand from semiconductor and electronics manufacturing, and growing use of diamond-like coatings (DLC) in electric vehicles for friction reduction and durability.

CVD technology is the leading segment, accounting for an estimated 64.6% market share, driven by its superior hardness, wear resistance, and suitability for high-performance industrial applications.

The diamond coatings market is expected to grow at a CAGR of 7.1% from 2026 to 2033.

Some of the major players include OC Oerlikon, Element Six, Ionbond, Kyocera Corporation, and Sumitomo Electric Industries.