- Specialty & Fine Chemicals

- Ultra-high Purity Anhydrous Hydrogen Chloride Gas Market

Ultra-high Purity Anhydrous Hydrogen Chloride Gas Market Size, Share, and Growth Forecast 2026 - 2033

Ultra-high Purity Anhydrous Hydrogen Chloride Gas Market by Product Grade (Electronics, Pharmaceutical), Application (Semiconductors, Flat Panel Display, Photovoltaics, Pharmaceuticals, Specialty Chemicals, Others), Industry (Electronics, Chemicals, Pharmaceuticals, Others), and Regional Analysis for 2026 - 2033

Ultra-high Purity Anhydrous Hydrogen Chloride Gas Market Size and Trend Analysis

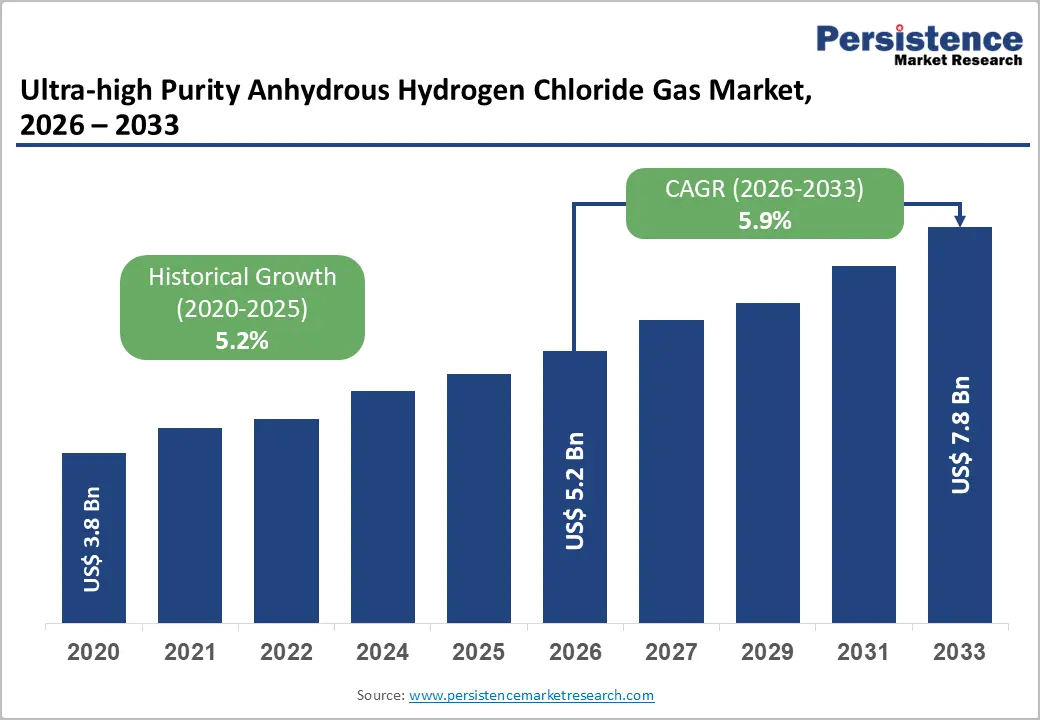

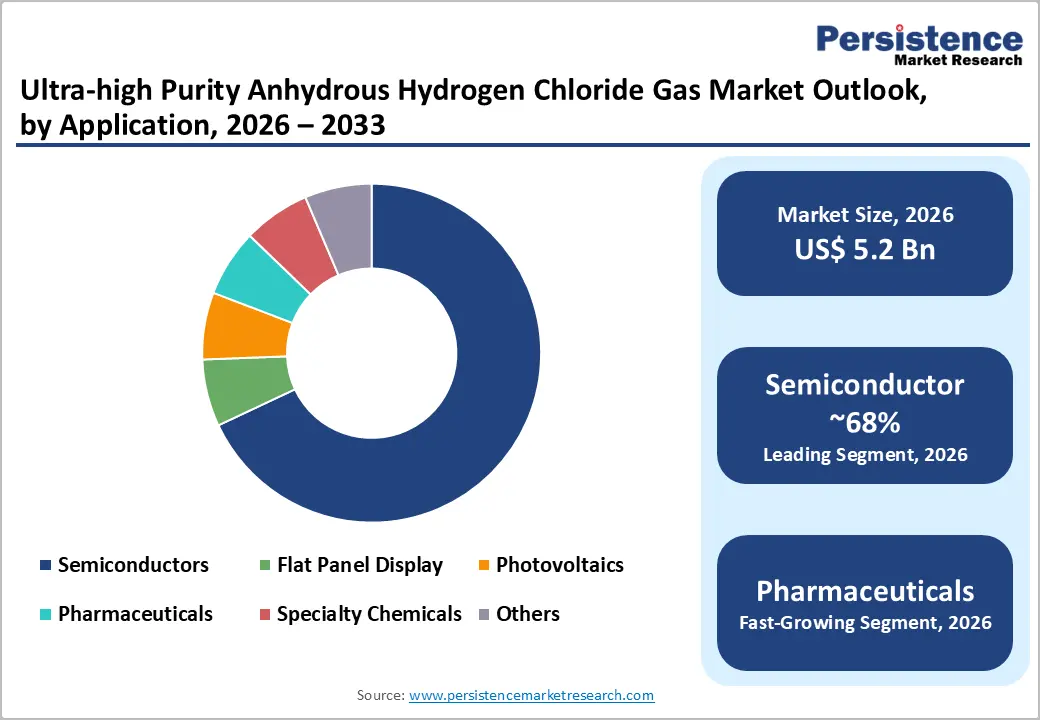

The global ultra-high purity anhydrous hydrogen chloride gas market is valued at US$ 5.2 Bn in 2026 and is projected to reach US$ 7.8 Bn by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

This robust growth trajectory is underpinned by the accelerating global demand for high-precision semiconductor fabrication processes, where ultra-high purity HCl gas is indispensable for silicon wafer etching, chamber cleaning, and epitaxial deposition. The proliferation of advanced node chips, particularly those at 5 nm and below, has significantly elevated the requirement for gas purity levels of 99.999% (5N) and above, since even trace impurities can introduce fatal defects in integrated circuits. Concurrent growth in photovoltaic manufacturing, pharmaceutical-grade synthesis, and specialty chemical applications further sustains the market's upward trajectory over the forecast horizon.

Key Industry Highlights:

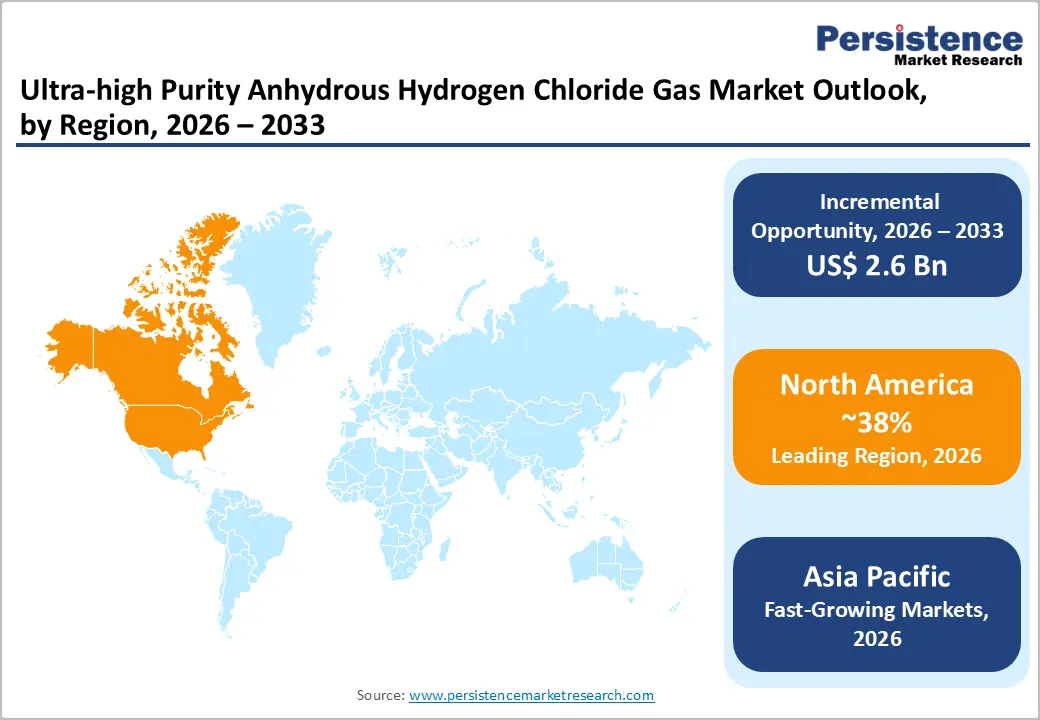

- Leading Region: North America leads the UHP HCl gas market, with 38% market share, driven by the U.S. semiconductor boom catalyzed by the CHIPS Act, which has unlocked over US$ 540 Bn in private fab investments, directly driving specialty gas demand.

- Fastest Growing Region: Asia Pacific is the most dynamic growth frontier, led by semiconductor capacity expansions in South Korea, India's emerging fab ecosystem, and China's self-sufficiency push, expected to drive the fastest regional volume growth through 2033.

- Dominant Segment: Electronics Grade segment commands approximately 68% of total UHP HCl gas revenues, underpinned by insatiable demand from semiconductor fabs consuming ultra-pure 5N-grade HCl for advanced node etching and cleaning processes.

- Fastest Growing Segment: Pharmaceuticals is the fastest growing application segment, with pharmaceutical-grade UHP HCl gas demand accelerating as API synthesis and oncology drug formulation processes require increasingly stringent chemical purity standards.

- Key Market Opportunity: India's semiconductor mission and a 28.7% rise in UHP HCl imports in 2023 present a strategic first-mover opportunity for gas suppliers to establish local production and long-term fab supply agreements in this high-growth market.

| Key Insights | Details |

|---|---|

| Ultra-high Purity Anhydrous Hydrogen Chloride Gas Market Size (2026E) | US$ 5.2 Bn |

| Market Value Forecast (2033F) | US$ 7.8 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.9% |

| Historical Market Growth (2020 - 2025) | 5.2% |

DRO Dynamics

Drivers - Surging Semiconductor Fabrication Demand Catalyzing Ultra-pure Gas Consumption

The single most powerful driver of the ultra-high purity anhydrous hydrogen chloride gas market is the relentless global expansion of semiconductor manufacturing infrastructure. According to the Semiconductor Industry Association (SIA), global semiconductor sales reached approximately US$ 627 Bn in 2024, a 19% year-on-year increase, and are projected to approach US$ 697 Bn by 2026. This surge in chip output directly amplifies the need for ultra-high purity process gases, as UHP HCl gas is critical for plasma etching, silicon wafer cleaning, and chamber passivation in advanced fabrication nodes.

The CHIPS and Science Act alone has catalyzed over US$ 540 Bn in announced private semiconductor investments across 28 U.S. states as of 2025, triggering massive demand for specialty gases throughout the domestic semiconductor supply chain. Major fab expansions by TSMC, Intel, Micron, and Samsung in North America and Europe are generating unprecedented demand for UHP-grade HCl gas, a trend set to intensify through 2033.

Rising Adoption of Ultra-high Purity HCl in Photovoltaic and Flat Panel Display Manufacturing

Beyond semiconductors, the rapid global expansion of solar photovoltaic (PV) manufacturing and flat panel display production is emerging as a significant demand driver. According to the International Energy Agency (IEA), global solar PV installed capacity is on track to grow substantially, with annual installations forecasted to surpass 600 GW in the coming years. Silicon wafer texturing, etching, and surface passivation, essential steps in PV cell fabrication, require ultra-high purity HCl gas to ensure minimal contamination.

Similarly, flat panel display manufacturers employ UHP HCl gas for cleaning indium tin oxide (ITO) layers and removing organic contaminants from OLED and LCD panels. In 2023, flat panel display applications consumed over 11,500 metric tons of ultra-high purity HCl gas globally. As both the photovoltaics and flat panel display sectors pursue higher production efficiencies and greater integration of advanced materials, the demand for ultra-high purity-grade HCl gas will continue to scale proportionately.

Market Restraints

Stringent Safety and Handling Regulations Imposing Significant Compliance Costs

Anhydrous HCl gas is classified as a highly toxic and corrosive substance, subject to rigorous regulatory oversight across all major markets. In the United States, OSHA's Hazard Communication Standard (HazCom 2024) imposes strict requirements for the classification, labeling, and safe handling of compressed toxic gases, including mandatory Safety Data Sheet (SDS) revisions and facility-level exposure controls.

Compliance demands specialized storage infrastructure such as nickel-lined cylinders, pressure-rated containment systems, and real-time leakage detection equipment with sensitivity thresholds below 5 ppm. These safety mandates substantially increase the capital and operational expenditure for both producers and end-users, creating a significant barrier to market entry for smaller enterprises and limiting cost-competitiveness in price-sensitive emerging markets.

High Production Costs and Supply Chain Concentration Risks

The production of UHP anhydrous HCl gas at purity levels of 4.5N (99.995%) and 5N (99.999%) demands sophisticated purification infrastructure, proprietary process technologies, and stringent cleanroom-compatible packaging systems, all of which significantly elevate the cost of manufacture. The supply chain for ultra-pure gases is highly concentrated, with a handful of multinational companies controlling the bulk of global production capacity. This concentration creates vulnerability to supply disruptions caused by geopolitical tensions, trade restrictions, or facility outages. For example, ongoing U.S.-China trade tensions and regional export controls on advanced manufacturing inputs have periodically strained specialty gas supply chains in Asia Pacific, affecting downstream semiconductor fabs. These supply risks remain a persistent restraint on the market's ability to scale seamlessly with demand.

Opportunities - India's Semiconductor Ecosystem Emergence Creating High-Growth Demand Corridor

India represents one of the most compelling emerging opportunities in the ultra-high purity anhydrous hydrogen chloride gas market over the 2026-2033 forecast period. The Government of India has committed substantial incentives under its India Semiconductor Mission (ISM), including production-linked incentive (PLI) schemes designed to attract greenfield semiconductor fab investments. Import volumes of electronic-grade HCl gas into India grew by 28.7% in 2023, reflecting the rapid build-out of semiconductor-adjacent manufacturing.

Domestic chemical companies, including Gujarat Alkalies, are establishing dedicated UHP HCl production units with target capacities of up to 800 metric tons per year. As India progressively builds its semiconductor fabrication and advanced electronics supply chain, it is set to emerge as a high-volume UHP HCl gas market, offering first-mover advantages to gas suppliers who establish early supply relationships and on-site production capabilities in the country.

On-site Gas Generation and Vertical Integration Driving Operational Innovation

A significant opportunity exists for gas producers and semiconductor manufacturers to co-invest in on-site UHP HCl gas generation systems, eliminating reliance on third-party cylinder supply chains and ensuring consistent purity under controlled conditions. The market is witnessing growing adoption of automated gas delivery systems; in 2024, over 130 new semiconductor fabrication plants globally installed robotic cylinder-handling equipment with integrated leakage detection capabilities.

Companies that can offer vertically integrated solutions, from gas synthesis and purification to cleanroom-compatible distribution and real-time purity monitoring, stand to capture significant value. Furthermore, as research in optoelectronics, radio-frequency (RF) devices, and compound semiconductor devices (GaN, GaAs) accelerates, these emerging application areas will require ultra-high purity HCl gas at even more demanding specifications, creating premium-priced, high-margin market segments for suppliers with advanced purification capabilities.

Category-wise Analysis

Product Grade Insights

Electronics grade constitutes the leading segment within the product grade category, accounting for approximately 68% of the global ultra-high purity anhydrous hydrogen chloride gas market in 2025. This dominance is attributable to its critical role in semiconductor fabrication processes, including plasma etching of silicon wafers, deposition chamber cleaning, and the epitaxial growth of compound semiconductors.

Industry estimates indicate that more than 80% of global electronics-grade HCl production is consumed by the semiconductor sector. The minimum required purity for electronics-grade UHP HCl is 4.5N (99.995%), while advanced sub-5 nm applications increasingly necessitate purity levels of 5N (99.999%) or higher. Japan, South Korea, Taiwan, and the United States represent the principal markets, with Japan and South Korea jointly consuming approximately 38,000 metric tons in 2023.

Application Insights

Semiconductors constitute the dominant application segment in the ultra-high purity anhydrous hydrogen chloride gas market, accounting for approximately 68% of total global consumption as of 2025. This leadership is driven by the indispensable and non-substitutable role of UHP HCl gas across critical stages of semiconductor fabrication, including plasma-based dry etching, in-situ chamber cleaning, chemical vapor deposition (CVD), atomic layer deposition (ALD), and selective silicon etching for advanced device architectures such as FinFET and vertical NAND.

In 2024, leading semiconductor fabrication facilities in Taiwan, South Korea, and the United States collectively consumed more than 38,000 metric tons of UHP HCl for wafer cleaning and etching applications. The rapid adoption of 5G, artificial intelligence, and Internet of Things technologies is expected to sustain and further reinforce this segment’s dominance through 2033.

Industry Insights

Electronics represents the dominant end-use industry in the ultra-high purity anhydrous hydrogen chloride gas market, accounting for approximately 65% of total market revenue in 2025. This leadership is driven by a combination of structural demand factors, including the rapid expansion of consumer electronics manufacturing, cloud computing infrastructure, automotive electronics, and artificial intelligence hardware, all of which rely heavily on advanced semiconductor components produced using UHP HCl gas.

The electronics and semiconductor segment accounted for 36.18% of global specialty gas revenues in 2024, underscoring its role as the primary demand source for the highest-purity process gases. Within this sector, integrated circuit and printed circuit board fabrication, alongside emerging applications in monolithic microwave integrated circuits and optoelectronics, are expected to support sustained volume growth. Meanwhile, the chemicals and pharmaceuticals segments, although smaller, are expanding rapidly due to tightening regulatory standards in key regions.

Regional Insights

North America Ultra-high Purity Anhydrous Hydrogen Chloride Gas Market Trends

North America represents the leading regional market for ultra-high purity anhydrous hydrogen chloride gas, with 38% market share, driven primarily by the United States’ advanced semiconductor manufacturing base, extensive pharmaceutical production capacity, and well-established regulatory framework. The CHIPS and Science Act, which allocates US$ 52.7 billion toward semiconductor initiatives, has stimulated more than US$ 540 billion in announced private fabrication investments across 28 U.S. states as of 2025.

Major capacity expansions by TSMC, Intel, and Micron have significantly increased regional demand for specialty process gases, including UHP HCl. In parallel, updated regulatory requirements from the U.S. Environmental Protection Agency and OSHA’s HazCom 2024 standards are shaping safety and compliance practices. Geopolitical disruptions affecting global petrochemical supply chains have further encouraged investment in resilient, domestically anchored gas production infrastructure.

Europe Ultra-high Purity Anhydrous Hydrogen Chloride Gas Market Trends

Europe is projected to be one of the fastest-growing regional market for ultra-high purity anhydrous hydrogen chloride gas during the 2026-2033 forecast period, driven by semiconductor sovereignty initiatives and stringent environmental and chemical safety regulations. The European Chips Act, which aims to increase Europe’s share of global semiconductor production to 20% by 2030, has catalyzed substantial investments in advanced fabrication capacity. Germany’s Silicon Saxony cluster in Dresden has emerged as a focal point for these investments, significantly strengthening demand for UHP process gases.

In 2025, Air Liquide S.A. committed over €250 million to expand ultra-pure gas production facilities in the region. Additionally, growth in pharmaceutical and specialty chemicals manufacturing across the United Kingdom, France, and Spain is reinforcing regional demand. Geopolitical risks and regulatory frameworks such as REACH and the Net-Zero Industry Act are further supporting localized, sustainable production strategies.

Asia Pacific Ultra-high Purity Anhydrous Hydrogen Chloride Gas Market Trends

Asia Pacific represents the largest consuming region for ultra-high purity anhydrous hydrogen chloride gas globally, supported by its dominant role in semiconductor, flat panel display, and solar photovoltaic manufacturing. China, Japan, South Korea, and Taiwan collectively form the core of global semiconductor fabrication capacity, with South Korea, home to Samsung Electronics and SK Hynix, ranking among the world’s largest consumers of UHP HCl for advanced memory and logic chip production.

China continues to expand its semiconductor ecosystem, targeting 70% integrated circuit self-sufficiency by 2025 through planned government investments exceeding US$ 150 billion, which directly increase demand for high-purity process gases. Geopolitical developments, including U.S.-China technology decoupling, have accelerated domestic specialty chemical supply chain development across the region. India is emerging as a key growth market, while Japan and ASEAN nations continue to set and adopt advanced purity and manufacturing standards.

Competitive Landscape

The global ultra-high purity anhydrous hydrogen chloride gas market is characterized by a moderately consolidated competitive structure, dominated by a limited number of large-scale industrial gas suppliers with advanced purification technologies, expansive global distribution networks, and long-term supply agreements with leading semiconductor manufacturers. Linde Plc, Air Liquide S.A., and Air Products and Chemicals Inc. collectively account for a substantial share of global revenues, leveraging scale advantages, robust research and development capabilities, and expertise in on-site gas generation. Key competitive strategies include investments in proximity manufacturing near semiconductor fabrication facilities, vertical integration across purification and delivery operations, and collaborative development of next-generation gas delivery systems.

Key Developments:

- July 2025: Air Liquide S.A. announced an investment of over €250 million to build new air separation units and ultra-high purity gas production infrastructure in Silicon Saxony, Dresden, Germany, specifically to supply a major semiconductor customer with ultra-pure nitrogen, oxygen, argon, hydrogen, and related process gases, marking the company's largest-ever European electronics investment.

- December 2025: Air Liquide announced the acquisition of NovaAir in October 2025 to expand its footprint across India, enhancing supply of industrial and high-purity specialty gases for sectors including electronics, automotive, and healthcare, strengthening its regional production and distribution capabilities.

- April 2025: Linde plc announced the expansion of ultra-high purity gas supply to Samsung Electronics in South Korea by building a new air separation unit, strengthening semiconductor-grade gas capacity, with operations expected by mid-2026.

Top Companies in Ultra-high Purity Anhydrous Hydrogen Chloride Gas Market

- Linde Plc (Woking, United Kingdom) is the world's largest industrial gas company. The company is a premier supplier of ultra-high purity specialty gases for the electronics, semiconductor, and pharmaceutical sectors, operating through its HiQ brand. Linde's competitive edge lies in its proprietary gas purification technology, globally unmatched liquid hydrogen production capacity, and a pipeline network of approximately 1,000 km for high-purity gas distribution.

- Air Liquide S.A. (Paris, France), positioning it as the world's leading supplier of ultra-high purity gases and advanced materials for the semiconductor, photovoltaics, and flat panel display industries. The company's strategy centers on proximity manufacturing, co-locating ultra-pure gas production units at or near major customer fabs, to guarantee supply reliability and purity consistency.

- Air Products and Chemicals Inc. (Allentown, U.S.) is a globally recognized leader in industrial gases, with significant market presence in the supply of ultra-high purity process gases to the semiconductor and specialty chemicals industries. The company's electronics gas portfolio encompasses UHP HCl and other critical process gases, supported by advanced purification systems and on-site generation capabilities that meet the stringent requirements of cutting-edge chip fabrication nodes.

Companies Covered in Ultra-high Purity Anhydrous Hydrogen Chloride Gas Market

- Linde Plc

- Air Liquide S.A.

- Air Products and Chemicals Inc.

- Messer Group GmbH

- Matheson Tri-Gas, Inc.

- Sumitomo Seika Chemicals Co., Ltd.

- Gas Innovations Inc.

- Shandong Yanhe Chemical Co., Ltd.

- Shandong Weitai Fine Chemical Co., Ltd.

- Cato Research Chemical Inc.

- Taiyo Nippon Sanso Corporation

- Gujarat Fluorochemicals Ltd.

Frequently Asked Questions

The global Ultra-high Purity Anhydrous Hydrogen Chloride Gas market is valued at US$ 5.2 Bn in 2026 and is projected to reach US$ 7.8 Bn by 2033, expanding at a CAGR of 5.9% over the forecast period, driven by robust semiconductor fab expansions, increasing photovoltaic manufacturing, and growing pharmaceutical synthesis demand.

The primary growth drivers include the global surge in semiconductor fabrication activity, amplified by the U.S. CHIPS and Science Act and analogous policies in Europe and Asia, as well as rising demand from photovoltaic cell manufacturing, flat panel display production, and pharmaceutical API synthesis. The escalating need for sub-5 nm process node gases at extreme purity levels is a particularly strong structural driver.

Electronics grade is the dominant product grade segment, accounting for approximately 68% of total market revenues in 2025. Its dominance is driven by the critical role of 5N-purity (99.999%) HCl gas in semiconductor wafer etching, chamber cleaning, and doping processes at leading-edge chip fabs, where even parts-per-trillion impurity levels can cause device defects.

North America currently leads the global market, with 38% market share, underpinned by the U.S.'s world-class semiconductor ecosystem, over US$ 540 Bn in CHIPS Act-driven fab investments, and the presence of leading gas suppliers such as Linde Plc, Air Products and Chemicals, and Matheson Tri-Gas. Asia Pacific is the fastest-growing region, led by semiconductor expansions in South Korea, Taiwan, and India's rapidly emerging fab infrastructure.

Key opportunities include the rapid build-out of India's semiconductor ecosystem, where HCl import volumes grew 28.7% in 2023, on-site gas generation and vertical integration models that ensure purity consistency and supply resilience, and expanding applications in optoelectronics, RF devices, and compound semiconductor manufacturing (GaN, GaAs), all of which require ultra-high purity-grade HCl gas at premium specifications.

The leading companies in the global UHP anhydrous HCl gas market include Linde Plc, Air Liquide S.A., Air Products and Chemicals Inc., Messer Group GmbH, Matheson Tri-Gas, Inc., Sumitomo Seika Chemicals Co., Ltd., Taiyo Nippon Sanso Corporation, Gujarat Fluorochemicals Ltd., and Shandong Yanhe Chemical Co., Ltd., among others.