- Advanced Materials

- Finished Leather Market

Finished Leather Market Size, Share, and Growth Forecast 2026 - 2033

Finished Leather Market by Product Type (Full-Grain Leather, Top-Grain Leather, Corrected-Grain Leather, Split Leather, Bonded Leather, Exotic Leather), Raw Material (Cowhide, Sheepskin, Goatskin, Pigskin, Exotic Skins, Buffalo Hide), Distribution Channel (Direct Sales, Distributors & Traders, Retail Stores, Online Channels), End-user (Footwear & Apparel, Automotive, Furniture & Interiors, Luxury Goods, Industrial), and Regional Analysis, 2026 - 2033

Finished Leather Market Size and Trend Analysis

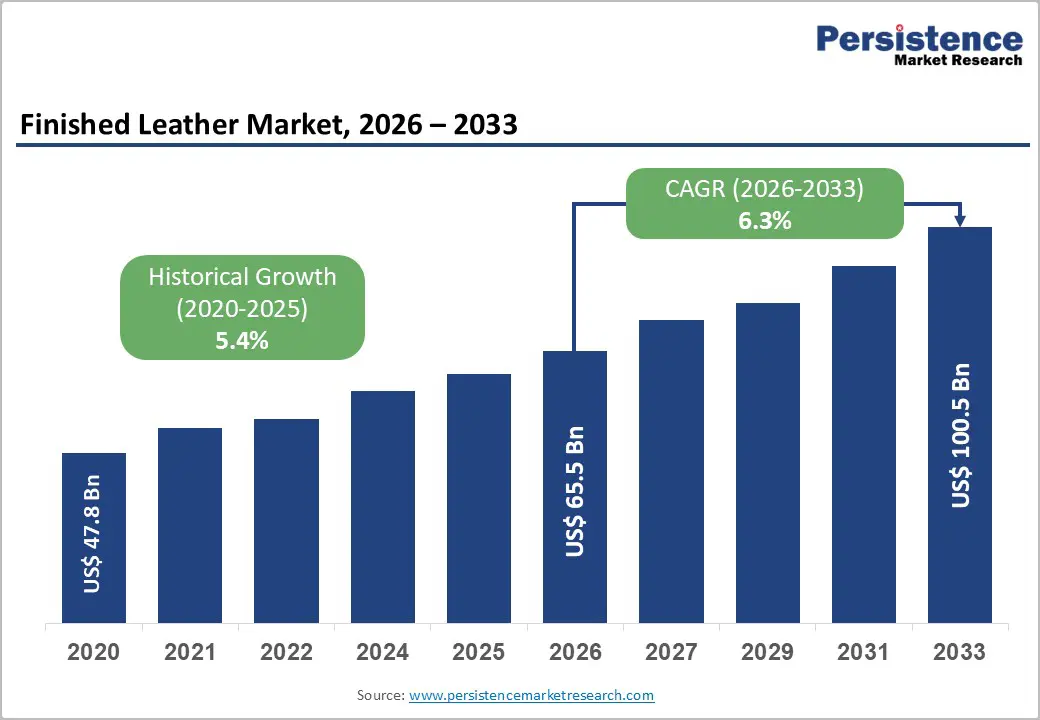

The global finished leather market size is likely to be valued at US$ 65.5 billion in 2026 and is expected to reach US$ 100.5 billion by 2033, growing at a CAGR of 6.3% during the forecast period from 2026 to 2033.

The finished leather market is on a strong and accelerating growth trajectory, driven by rising consumer spending on premium footwear, fashion apparel, and luxury goods, combined with sustained demand from the automotive and furniture industries for high-quality leather interiors.

Key Industry Highlights:

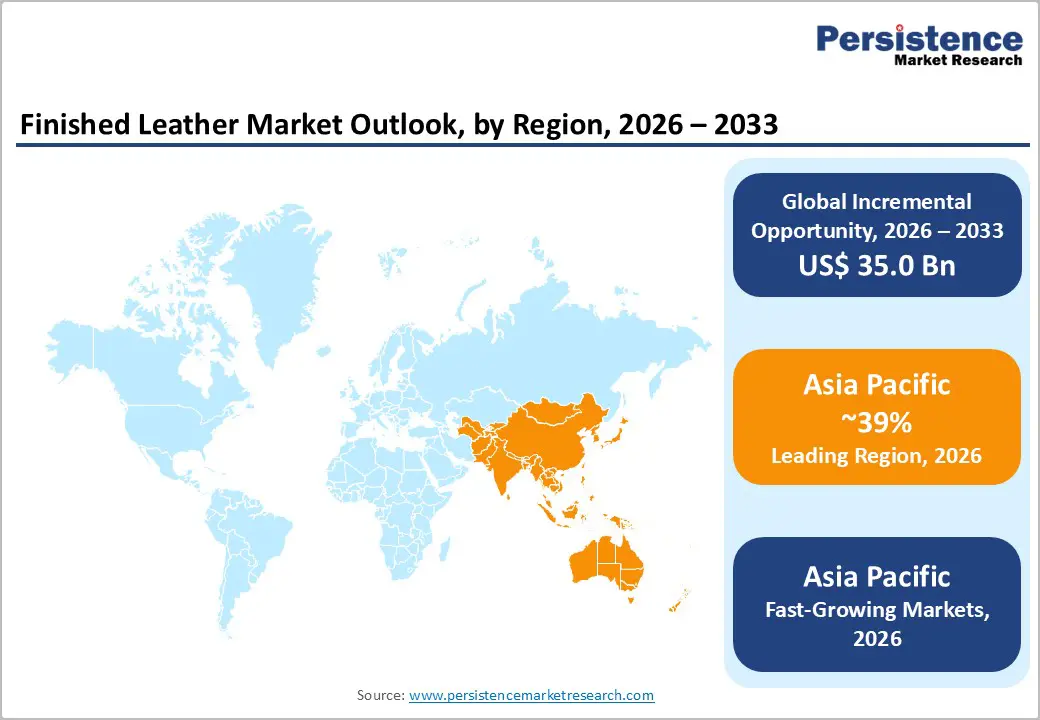

- Leading Region: Asia Pacific dominates the finished leather market with 39% share, driven by China and India, which have strong manufacturing capabilities, abundant raw materials, and significant leather exports. The region's robust footwear and leather goods production further fuels demand.

- Fastest Growing Region: Asia Pacific is the fastest growing region with a positive CAGR driven by China’s expanding luxury consumption projected to reach 40% of global luxury spending by 2030, India’s growing leather exports exceeding US$ 5 billion, and ASEAN’s rapid footwear manufacturing scale-up.

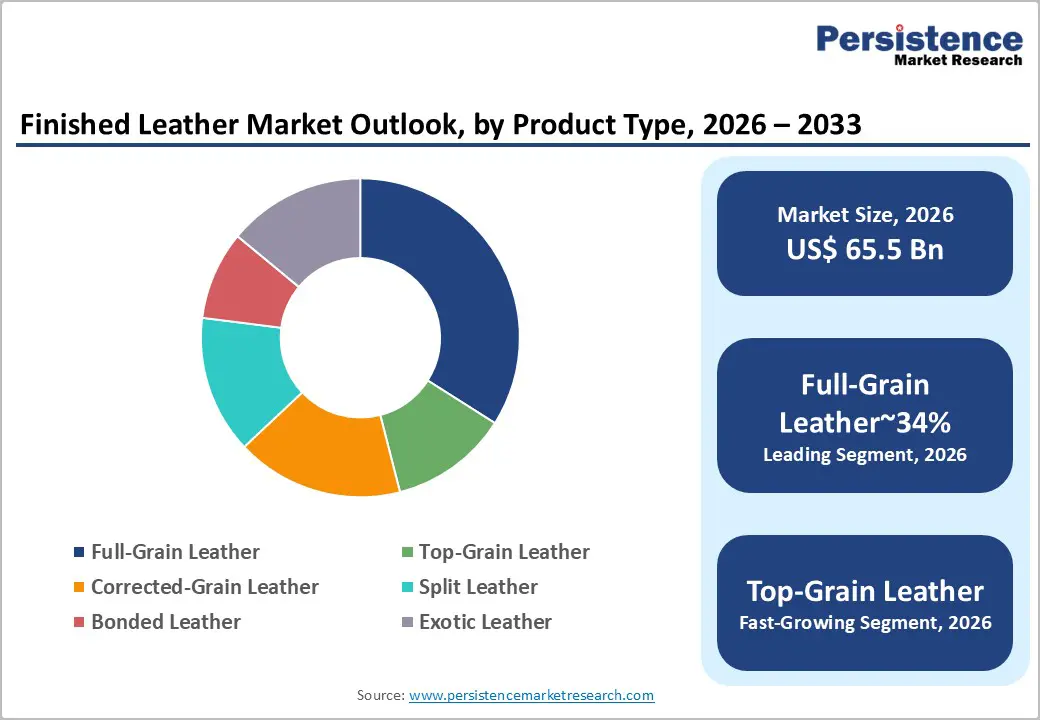

- Dominant Segment: Full-Grain leather leads the product category with approximately 34% market share, preferred for luxury handbags, premium footwear, and bespoke automotive interiors by iconic brands including Hermès, Louis Vuitton, and BMW for its unmatched durability and patina development.

- Fastest Growing Segment: The luxury goods is the fastest growing, fueled by expanding affluent demographics in Asia Pacific and the Middle East, and continued growth of the €362 billion global personal luxury goods market.

- Key Opportunity: Leather Working Group Gold-certified sustainable leather with blockchain-based traceability represents the highest-value growth opportunity, as brands including Nike, Adidas, and BMW commit to sourcing exclusively from LWG-certified tanneries, commanding sourcing preference and premium pricing.

| Key Insights | Details |

|---|---|

| Finished Leather Market Size (2026E) | US$ 65.5 Billion |

| Market Value Forecast (2033F) | US$ 100.5 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.3% |

| Historical Market Growth (2020 - 2025) | 5.4% |

Market Dynamics

Drivers - Surging Global Luxury Goods and Premium Fashion Demand

The global luxury goods industry remains one of the strongest and most consistent drivers of demand for premium finished leather. According to Bain & Company’s annual luxury study conducted with Altagamma, the personal luxury goods market reached approximately €362 billion in 2023. Leather goods, including handbags, small accessories, and luggage, continue to represent one of the largest and most resilient product categories.

Leading luxury brands such as LVMH, Kering, Hermès, and Prada consistently invest in exclusive tannery partnerships and high-quality leather sourcing to preserve craftsmanship and brand value. At the same time, the rapid growth of affluent consumers across China, India, Southeast Asia, and the Gulf region is creating new demand opportunities. This expanding customer base is significantly increasing the need for premium leather goods, thereby driving large-scale production of full-grain and top-grain finished leather globally.

Expanding Automotive Interior Leather Demand Driven by Premium Vehicle Growth

The global automotive industry’s shift toward premium and luxury vehicle interiors is creating strong and long-term demand for high-quality finished leather. Data from organizations such as ACEA and OICA show that premium vehicle brands like BMW, Mercedes-Benz, Audi, Lexus, and Tesla have consistently grown faster than the overall passenger vehicle market. On average, each premium vehicle uses around 15-20 square feet of leather for interiors, including seats, door panels, and steering wheels.

The growing popularity of electric vehicles is not reducing leather usage; instead, it is reshaping demand as manufacturers use premium interiors to differentiate their products. Additionally, the rise of Chinese luxury EV brands such as NIO, Li Auto, and Xpeng is creating a new and rapidly expanding demand base. This trend is further strengthening the role of finished leather in modern automotive design and customer experience.

Restraints - Environmental Regulations and Animal Welfare Concerns

The leather tanning industry is facing increasing regulatory pressure and public scrutiny due to its environmental impact. One of the key concerns is chromium-VI contamination, which can result from traditional chrome tanning processes. Regulations such as the EU’s REACH framework limit hexavalent chromium levels in leather products to 3 mg/kg, increasing compliance costs for tanneries and requiring strict quality checks.

In addition to regulatory challenges, growing awareness around animal welfare is influencing consumer behavior, particularly among younger demographics in Western markets. Many consumers are actively choosing vegan or synthetic alternatives over traditional leather products. This shift in perception is gradually affecting the industry’s growth potential in certain regions. As a result, leather manufacturers must invest in cleaner technologies and transparent sourcing practices to maintain market relevance and address both environmental and ethical concerns effectively.

Competition from Synthetic and Bio-Based Alternative Materials

The finished leather market is experiencing increasing competition from synthetic and bio-based alternatives. Materials such as polyurethane (PU) and polyvinyl chloride (PVC) leather, along with recycled leather composites, are widely used due to their lower cost and consistent quality. In addition, innovative bio-based materials like mushroom leather (Mylo), pineapple fiber leather (Piñatex), and lab-grown collagen leather are gaining attention in premium and eco-conscious markets.

Although these alternatives currently occupy niche segments, their performance, durability, and affordability are improving steadily. At the same time, their strong sustainability positioning appeals to environmentally conscious consumers and brands. As production scales up and costs decrease, these materials are expected to capture a larger share of the footwear and accessories markets. This creates long-term competitive pressure on traditional finished leather manufacturers, pushing them to innovate and differentiate their offerings.

Opportunities - Sustainable and Certified Traceable Leather for ESG-Driven Brand Sourcing

The increasing focus on Environmental, Social, and Governance (ESG) standards is creating significant opportunities for sustainable and traceable finished leather. Global fashion and automotive brands are actively seeking suppliers that meet strict environmental and ethical standards. The Leather Working Group (LWG), which sets the industry benchmark for sustainability, has expanded to over 1,200 member companies across more than 60 countries.

Major brands such as Nike, Adidas, H&M, and BMW have committed to sourcing leather exclusively from LWG-certified tanneries, especially those with Gold ratings. In addition, digital traceability solutions, including blockchain-based systems, are gaining importance for tracking leather from raw hide to final product. Tanneries that invest in sustainability certifications and advanced traceability systems can secure long-term partnerships and command premium pricing. This trend is expected to grow as regulatory requirements and consumer expectations around sustainability continue to strengthen globally.

Rising Demand for Premium Leather in Asian Luxury and Automotive Markets

Asia Pacific is emerging as the fastest-growing region for premium finished leather, driven by rising consumer income and expanding industries. China remains the largest luxury goods market by consumer base, with projections indicating that Chinese consumers could account for over 40% of global luxury spending by 2030. Meanwhile, India’s growing middle class and increasing demand for premium fashion and automobiles are contributing to steady market expansion.

The automotive sector in India is also witnessing strong growth, particularly in the premium segment, further boosting demand for high-quality leather interiors. Additionally, Southeast Asian countries are strengthening their manufacturing capabilities in footwear and leather goods, increasing regional demand for finished leather. Companies that establish strong supply chains, local partnerships, and quality certifications aligned with regional requirements are well-positioned to capture this high-growth, multi-billion-dollar opportunity across Asia Pacific markets.

Category-wise Analysis

By Product Type Insights

Full-grain leather is the leading product type segment, accounting for approximately 34% of the global market share. It is made from the top layer of the hide, retaining its natural grain and undergoing minimal processing. This makes it the highest-quality and most durable type of leather available. Full-grain leather is known for its natural texture, ability to develop a rich patina over time, and excellent breathability, making it highly desirable for premium applications.

It is widely used in luxury handbags, high-end footwear, furniture upholstery, and automotive interiors. Leading brands such as Hermès, Louis Vuitton, and Gucci rely heavily on full-grain leather for their flagship products. Due to its superior quality, it commands significantly higher prices compared to corrected-grain or split leather. This premium positioning allows the segment to generate strong revenue despite relatively lower production volumes in the overall leather market.

By Raw Material Insights

Cowhide is the dominant raw material segment, representing around 65% of the total finished leather market. Its dominance is driven by its wide availability as a by-product of the global beef and dairy industries. Cowhide offers large surface areas, making it ideal for applications such as automotive upholstery, furniture, and large leather goods. It is also highly durable and adaptable to different tanning processes, enhancing its versatility across product categories.

According to the Food and Agriculture Organization (FAO), global cattle population stands at approximately 1 billion, ensuring a consistent and reliable supply of raw materials. Major cowhide-producing countries include Brazil, the United States, China, India, and Argentina, which collectively meet the majority of global demand. This strong supply base, combined with its functional advantages, ensures cowhide remains the preferred raw material for manufacturers across both premium and mass-market segments.

By Distribution Channel Insights

The distributors and traders segment holds the largest share in the distribution channel, accounting for approximately 44% of the global market. These intermediaries play a vital role in connecting tanneries with manufacturers by aggregating supply from different regions and matching it with specific buyer requirements. The leather supply chain is complex due to variations in hide quality, regional price differences, and currency fluctuations. As a result, specialized traders help simplify transactions and ensure efficient supply flow.

Major trading hubs such as Italy, Brazil, India, and China serve as global centers for leather distribution and pricing. These intermediaries also provide value-added services such as quality inspection, grading, and logistics support. Their expertise and market knowledge make them essential participants in the global leather ecosystem, helping both suppliers and buyers manage risks and optimize sourcing strategies effectively.

By End-user Insights

The footwear and apparel segment is the largest end-use category, accounting for approximately 41% of the global finished leather market. Leather footwear, including formal shoes, boots, sandals, and athletic styles, represents the highest volume application globally. According to the World Footwear Yearbook, leather footwear accounts for around 25% of total footwear production by volume but contributes a significantly higher share in terms of value due to its premium pricing.

Leather apparel, such as jackets, coats, gloves, and belts, further supports demand in this segment. The consistent demand across different income groups, from affordable to luxury, ensures stable market growth. Additionally, leather products are valued for their durability, comfort, and aesthetic appeal, making them a preferred choice among consumers worldwide. This broad demand base across regions and price segments strengthens the segment’s leading position in the global market.

Regional Insights

North America Finished Leather Market Trends

North America is a key market for premium and specialty finished leather, with the United States leading regional demand. The market is driven by strong consumption in automotive interiors, luxury goods, and traditional leather products. Domestic players such as Tandy Leather Factory Inc. cater to both industrial and artisan markets, while automotive manufacturers rely on high-quality imported leather. Regulatory frameworks, including the Consumer Product Safety Improvement Act (CPSIA) and California-specific regulations, influence product standards and compliance requirements.

Canada also contributes to demand through its automotive manufacturing and fashion industries. The region’s well-developed e-commerce ecosystem is enabling direct-to-consumer leather brands to access global suppliers more efficiently. This has opened new sourcing opportunities for international tanneries, particularly those offering premium and certified leather products. Overall, North America continues to be a stable and high-value market for finished leather suppliers.

Europe Finished Leather Market Trends

Europe is widely recognized as the global center for high-quality finished leather, known for its craftsmanship, innovation, and sustainability leadership. Italy plays a central role, with renowned tanning districts such as Santa Croce sull’Arno and organizations like the Genuine Italian Vegetable Tanned Leather Consortium. Italian manufacturers are globally respected for producing premium leather used in luxury fashion and automotive applications.

Countries like Germany and France are major consumers due to their strong automotive and luxury fashion industries. The European Union’s regulations, including REACH and the Sustainable Textiles Strategy, set global standards for environmental and chemical safety. These regulations influence sourcing decisions worldwide, requiring international suppliers to meet strict compliance criteria. Companies such as Hulshof Royal Dutch Tanneries demonstrate Europe’s commitment to sustainable production. Overall, Europe remains a benchmark market, driving quality, innovation, and sustainability practices across the global leather industry.

Asia Pacific Finished Leather Market Trends

Asia Pacific is both the largest producer and the fastest-growing consumer of finished leather globally. China leads the region as the largest producer and exporter, with massive footwear manufacturing capacity and strong domestic consumption. The country’s leather industry produces billions of pairs of shoes annually, supported by a well-established supply chain. India is the second-largest producer and a key exporter, with leather exports exceeding US$ 5 billion annually.

Indian companies such as Tata International and Super Tannery play an important role in global supply. Southeast Asian countries, including Vietnam and Indonesia, are rapidly expanding their manufacturing capabilities, especially in footwear and leather goods. This growth is driven by global brands diversifying supply chains beyond China. Increasing regional demand, combined with strong production capabilities, positions Asia Pacific as a critical hub for both supply and consumption in the global finished leather market.

Competitive Landscape

The global finished leather market is highly fragmented, with thousands of tanneries operating across more than 100 countries. No single company holds a dominant market share, making competition intense and diverse. The market is segmented based on quality levels, with European tanneries leading in premium segments, Brazilian producers dominating automotive leather, and Asian manufacturers competing across mid-range and high-volume categories.

Key factors that influence competition include sustainability certifications such as Leather Working Group (LWG) ratings, compliance with environmental regulations, and traceability of raw materials. Technological capabilities in leather finishing and customization also play a critical role. Emerging trends include direct partnerships between tanneries and global brands, co-certification programs, and digital platforms for leather selection and sampling. These developments are improving efficiency and transparency in the supply chain, while also helping manufacturers better meet evolving customer and regulatory requirements in the global market.

Key Developments:

- In March 2025: Gruppo Mastrotto S.p.A. announced the commercial launch of its carbon-neutral certified leather line produced using renewable energy and bio-based tanning agents, targeting premium automotive OEM and luxury goods brand customers with verified Scope 1-3 emission reduction credentials.

- In October 2024: Tata International Limited expanded its LWG Gold-certified tannery capacity in Tamil Nadu, India, increasing finished leather production for automotive and luxury brand export customers across Europe and North America by approximately 20%.

- In May 2024: JBS Couros launched a blockchain-based cattle traceability platform for its Brazilian cowhide supply chain, enabling brand customers to verify zero-deforestation sourcing credentials for all finished leathers purchased from its tannery network.

Companies Covered in Finished Leather Market

- Pittards plc

- Tata International Limited

- Pakiza Tanning & Leather Finishing Ltd.

- SanTrend Inc.

- Jinjiang Guotai Leather Co., Ltd.

- Holly Holding Group

- Couro Azul S.A.

- Guangzhou Jinbairui Leather Co., Ltd.

- Genuine Italian Vegetable Tanned Leather Consortium

- Hulshof Royal Dutch Tanneries B.V.

- JBS Couros

- Gruppo Mastrotto S.p.A.

- Super Tannery Limited

- Prime Asia Leather Company

- Tandy Leather Factory Inc.

- Conceria Walpier S.r.l.

- Bader GmbH & Co. KG

- GST AutoLeather

Frequently Asked Questions

The global Finished Leather Market is projected to reach US$ 100.5 Billion by 2033, expanding from US$ 65.5 Billion in 2026 at a CAGR of 6.3% during the 2026-2033 forecast period.

The primary growth drivers are surging global luxury goods demand , with the personal luxury market reaching €362 billion in 2023 and Chinese consumers projected to account for over 40% of global luxury spending by 2030 , and expanding premium and luxury vehicle production driving automotive leather consumption of 15-20 square feet per vehicle across brands including BMW, Mercedes-Benz, and Tesla.

Full-Grain Leather leads the By Product Type category with approximately 34% of total market share. Its position as the highest-quality, most durable leather category , sourced from the complete outer hide surface with natural grain intact , makes it the material of choice for luxury brands including Hermès and Louis Vuitton and premium automotive interior applications globally.

Europe leads in market quality, prestige, and regulatory standard-setting, anchored by Italy’s world-class tanning districts including Santa Croce sull’Arno, Germany and France’s premium automotive and luxury fashion demand, and the EU’s REACH Regulation establishing the global chemical safety benchmark for leather articles across all consumer markets worldwide.

The leading opportunities are Leather Working Group (LWG) Gold-certified sustainable leather with blockchain traceability as major brands commit to LWG-only sourcing, and the rapidly expanding Asian luxury and premium automotive market, where Chinese consumers approaching 40% of global luxury spending and India’s growing automotive sector represent multi-billion-dollar addressable demand pools for premium finished leather.

The key market participants include Pittards plc, Tata International Limited, Pakiza Tanning & Leather Finishing Ltd., SanTrend Inc., Jinjiang Guotai Leather Co., Ltd., Holly Holding Group, Couro Azul S.A., Guangzhou Jinbairui Leather Co., Ltd., Genuine Italian Vegetable Tanned Leather Consortium, Hulshof Royal Dutch Tanneries B.V., JBS Couros, Gruppo Mastrotto S.p.A., Super Tannery Limited, Prime Asia Leather Company, and Tandy Leather Factory Inc.