- Metalworking & Fabrication

- Fabricated Metal Products Market

Fabricated Metal Products Market Size, Share, and Growth Forecast, 2026 - 2033

Fabricated Metal Products Market by Product Type (Structural Metal Products, Ornamental and Architectural Metal Products, Others), Material Type (Steel, Aluminum, Others), Fabrication Process (Welding, Casting, Others), End-user, and Regional Analysis for 2026 - 2033

Fabricated Metal Products Market Size and Trends Analysis

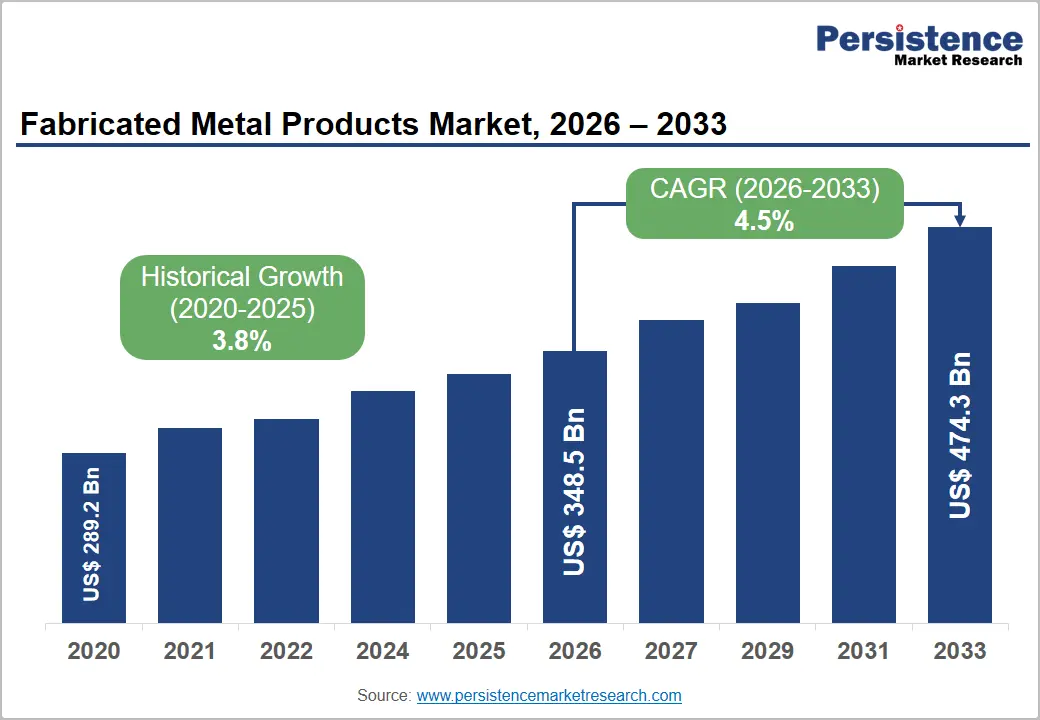

The global fabricated metal products market size is likely to be valued at US$348.5 billion in 2026 and is expected to reach US$474.3 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033, driven by industrialization, infrastructure modernization, and manufacturing investments.

Rising demand from the construction, transportation, energy, industrial machinery, and aerospace sectors continues to strengthen the need for fabricated metal components with greater precision, durability, and operational efficiency.

Key Industry Highlights:

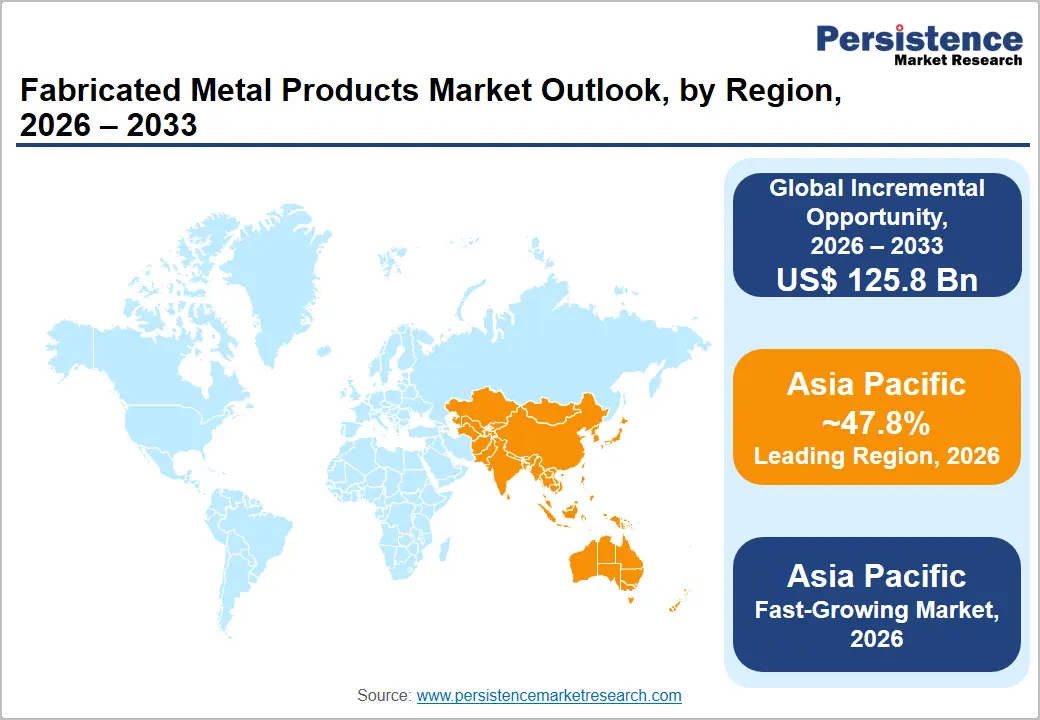

- Leading Region: Asia Pacific is anticipated to account for approximately 47.8% of the market share in 2026, driven by large-scale manufacturing, infrastructure development, expanding automotive production, and strong investments in renewable energy and industrial facilities.

- Fastest-growing Region: Asia Pacific is projected to register the highest regional CAGR, supported by rapid industrialization, manufacturing expansion across China, India, and ASEAN, and increasing adoption of advanced fabrication technologies.

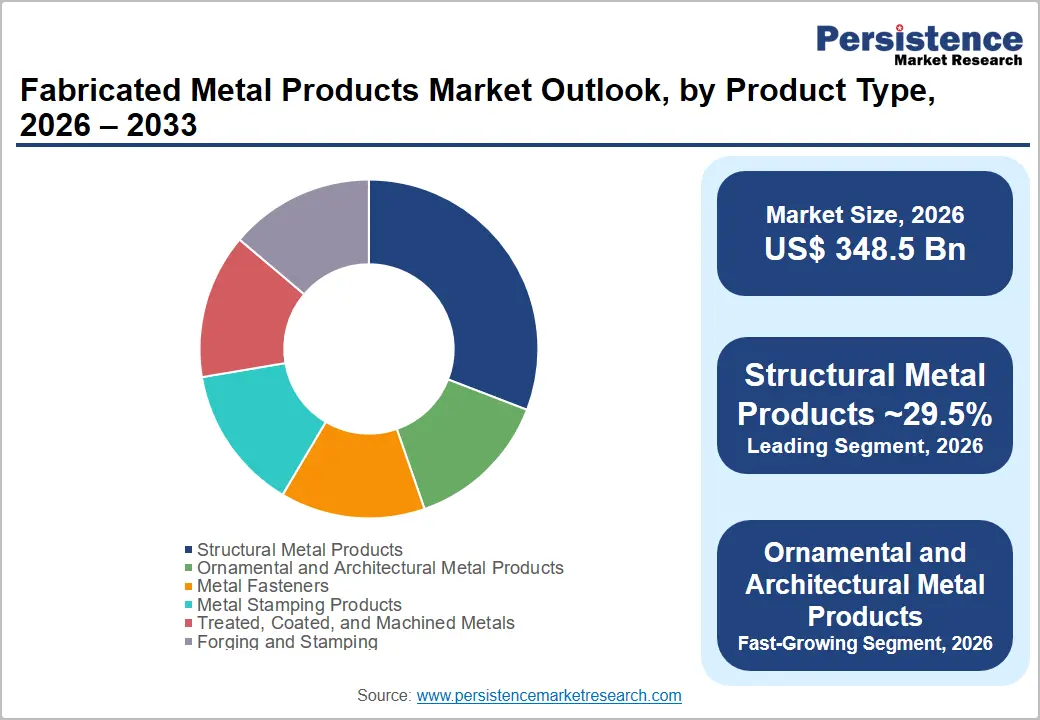

- Dominant Product Type: Structural metal products are anticipated to hold approximately 29.5% of the market share in 2026, supported by sustained demand from commercial construction, bridges, highways, industrial facilities, transmission towers, and other infrastructure development projects.

- Leading Material Type: Steel is anticipated to account for approximately 61.4% of market share in 2026, owing to its superior strength, cost-efficiency, recyclability, and extensive use across construction, automotive, industrial machinery, energy infrastructure, and heavy engineering applications.

DRO Analysis

Driver - Expanding Infrastructure and Industrial Construction Investments

Growing investments in commercial buildings, industrial facilities, transportation networks, renewable energy projects, and public infrastructure remain the primary growth catalyst for fabricated metal products worldwide. Structural steel components, fabricated beams, bridges, pipelines, metal roofing systems, utility towers, and reinforcement assemblies continue to experience strong demand as governments prioritize economic development through infrastructure modernization. Large-scale investments in highways, rail networks, airports, ports, manufacturing facilities, and logistics centers require significant volumes of fabricated steel products throughout construction and maintenance phases.

Private sector investment also supports sustained demand as warehouse construction, semiconductor manufacturing plants, electric vehicle production facilities, and industrial expansion projects increase globally. Infrastructure spending not only stimulates demand for structural metal products but also creates opportunities for value-added fabrication services, including welding, machining, coating, precision cutting, and assembly. These long-term capital expenditure programs provide stable order pipelines for manufacturers while encouraging continuous investment in production capacity and advanced fabrication technologies.

Manufacturing Automation and Industrial Localization

Manufacturing companies are increasingly adopting automation to improve operational efficiency, address skilled labor shortages, and enhance product quality. Automated welding systems, robotic material handling, digital quality inspection, laser cutting equipment, and CNC machining centers enable manufacturers to achieve higher productivity with improved dimensional accuracy and reduced production waste. These technological improvements have significantly enhanced production flexibility across fabricated metal operations.

Industrial localization initiatives across North America, Europe, and Asia Pacific further strengthen market demand. Governments continue to support domestic manufacturing through industrial policies designed to reduce supply chain dependence while improving national manufacturing competitiveness. Growing investments in renewable energy infrastructure, defense manufacturing, electric vehicles, heavy machinery, and industrial equipment are increasing demand for fabricated metal assemblies, precision components, and engineered structural products. These trends encourage manufacturers to expand fabrication capacity while integrating smart manufacturing technologies throughout production facilities.

Restraint - Raw Material Price Volatility and Skilled Workforce Shortages

Despite favorable long-term demand fundamentals, fabricated metal manufacturers continue to face considerable challenges from volatile steel, aluminum, stainless steel, copper, and alloy prices. Fluctuating raw material costs reduce profit margins, complicate long-term procurement planning, and increase pricing uncertainty for manufacturers operating under fixed-price contracts. Global geopolitical uncertainties, energy price fluctuations, trade policies, and transportation costs further contribute to supply chain instability.

The industry also faces persistent shortages of experienced welders, machinists, fabrication technicians, and industrial engineers. An aging workforce combined with insufficient vocational training limits production capacity across many regions. Labor shortages increase operating expenses, extend production lead times, and encourage greater investments in automation. Small and medium-sized fabricators are particularly vulnerable because they often have fewer financial resources to modernize facilities while competing against larger manufacturers with advanced automated production capabilities.

Opportunities - Renewable Energy and Grid Modernization Projects

Global expansion of renewable energy infrastructure presents one of the most significant long-term opportunities for fabricated metal manufacturers. Wind turbines, solar mounting structures, transmission towers, substations, battery storage systems, and utility-scale renewable energy facilities require extensive quantities of fabricated steel and aluminum products. As governments continue expanding electricity generation capacity while modernizing aging transmission infrastructure, demand for fabricated structural components is expected to increase steadily.

Power utilities also require fabricated products for substations, transformers, support structures, communication towers, and electrical distribution networks. Companies capable of producing corrosion-resistant, high-strength, and precision-engineered components are well positioned to benefit from increasing investment in renewable energy and power transmission infrastructure. This opportunity also supports expansion into engineering, installation support, and integrated fabrication services.

Digital Manufacturing and High-Value Fabrication

The rapid adoption of Industry 4.0 technologies creates substantial opportunities for manufacturers offering precision fabrication solutions. Digital manufacturing platforms, artificial intelligence-assisted quality inspection, predictive maintenance systems, robotic welding cells, and automated material handling significantly improve production efficiency while reducing operational costs.

Industrial customers increasingly prefer suppliers capable of providing complete manufacturing solutions that integrate engineering, machining, welding, surface finishing, coating, assembly, and logistics under one contract. This transition toward full-service manufacturing enables fabricators to generate higher margins while strengthening long-term customer relationships. Companies investing in advanced automation and digital production systems are expected to achieve stronger competitive positioning throughout the forecast period.

Category-wise Analysis

Product Type Insights

Structural metal products are anticipated to account for approximately 29.5% of the market share in 2026, making them the leading product segment. Demand is driven by commercial construction, transportation infrastructure, manufacturing facilities, and utility projects. These products include structural steel beams, bridge components, industrial frameworks, transmission towers, and warehouse structures. Continued investment in smart cities, airports, logistics hubs, and renewable energy projects supports sustained growth, while their high strength, durability, and load-bearing capacity make them essential across major infrastructure applications.

Ornamental and architectural metal products represent the fastest-growing segment, supported by increasing demand for premium residential, commercial, and hospitality developments. Decorative façades, staircases, railings, fencing systems, aluminum curtain walls, and customized metal cladding are becoming increasingly popular in modern building designs. Growth is further supported by CNC machining, laser cutting, and robotic welding technologies that enable highly customized, aesthetically appealing, and sustainable architectural solutions.

Material Type Insights

Steel is anticipated to account for approximately 61.4% of the market share in 2026, making it the leading material type. Its superior strength, cost-effectiveness, and versatility make it the preferred choice for structural steel beams, industrial equipment frames, bridges, pipelines, utility towers, and automotive chassis. Well-established supply chains, extensive recycling infrastructure, and compatibility with welding, machining, and coating processes continue to reinforce steel's market leadership across construction, manufacturing, and energy sectors.

Aluminum is the fastest-growing material type, driven by increasing demand for lightweight, corrosion-resistant materials in automotive, aerospace, and transportation applications. Electric vehicle battery enclosures, aircraft structural components, railcars, solar panel mounting systems, and modular building structures increasingly utilize aluminum to improve energy efficiency and reduce overall weight. Growing investments in sustainable mobility and advanced manufacturing continue to accelerate adoption, while stainless steel, iron, and copper alloys remain essential for applications requiring superior durability, corrosion resistance, and electrical conductivity.

Regional Insights

North America Fabricated Metal Products Market Trends

North America maintains a significant share of the global fabricated metal products market, supported by its mature industrial base, advanced manufacturing capabilities, and continuous investment in infrastructure modernization. The region benefits from strong demand across construction, transportation, energy, aerospace, automotive, and industrial machinery sectors. Ongoing adoption of robotic welding, CNC machining, laser cutting, and digital manufacturing technologies is improving productivity while helping manufacturers address skilled labor shortages.

U.S. Fabricated Metal Products Market Trends

The U.S. dominates the North American market due to substantial investments in commercial construction, transportation infrastructure, renewable energy projects, defense manufacturing, and industrial automation. Demand remains particularly strong for fabricated structural steel, bridges, transmission towers, utility poles, pipelines, industrial equipment, and warehouse construction.

The expansion of semiconductor manufacturing facilities, electric vehicle production plants, logistics centers, and data centers further supports demand for precision-fabricated metal components. Continuous investments in automation, robotic welding, and digital manufacturing strengthen the country's competitive position.

Canada Fabricated Metal Products Market Trends

Canada contributes significantly through mining, oil & gas, energy infrastructure, transportation projects, and industrial manufacturing. Demand for fabricated metal products is driven by pipeline infrastructure, power generation facilities, commercial construction, and mining equipment manufacturing. Increasing investments in renewable energy projects and sustainable industrial development are creating additional opportunities for structural steel fabricators and precision metal component manufacturers.

Europe Fabricated Metal Products Market Trends

Europe represents a technologically advanced fabricated metal products market supported by strong engineering expertise, highly developed manufacturing industries, and comprehensive environmental regulations. The region continues investing in industrial modernization, railway expansion, renewable energy infrastructure, electric vehicle production, and smart manufacturing technologies.

Germany Fabricated Metal Products Market Trends

Germany represents the largest fabricated metal products market in Europe owing to its leadership in automotive manufacturing, industrial machinery, precision engineering, heavy equipment production, and advanced manufacturing technologies. Demand remains strong for structural steel products, precision-fabricated components, industrial equipment, and high-performance engineered assemblies used across manufacturing and export industries.

U.K. Fabricated Metal Products Market Trends

The U.K. continues investing in commercial construction, transportation infrastructure, defense manufacturing, offshore wind projects, and industrial modernization. Growing adoption of advanced fabrication technologies and increasing infrastructure upgrades support demand for structural steel fabrication, architectural metal products, and precision-engineered industrial components.

France Fabricated Metal Products Market Trends

France maintains robust demand through aerospace manufacturing, transportation infrastructure, renewable energy installations, commercial construction, and industrial equipment production. Investments in rail modernization, energy transition projects, and advanced manufacturing continue to support the country's fabricated metal products industry.

Europe benefits from highly skilled engineering talent, advanced research capabilities, and strong industrial innovation. Although higher energy costs and stringent environmental regulations present operational challenges, they also encourage manufacturers to invest in energy-efficient fabrication technologies, sustainable production processes, and higher-value engineered metal products.

Asia Pacific Fabricated Metal Products Market Trends

Asia Pacific is anticipated to remain the largest regional market, accounting for approximately 47.8% of the global market share in 2026, while also registering the fastest growth throughout the forecast period. The region's leadership is supported by rapid industrialization, expanding manufacturing capacity, competitive production costs, extensive infrastructure development, and strong domestic consumption.

China Fabricated Metal Products Market Trends

China remains the largest manufacturing hub globally and the dominant contributor to regional demand. Extensive investments in transportation infrastructure, industrial parks, renewable energy projects, smart manufacturing, shipbuilding, heavy machinery, and commercial construction continue to support consumption of fabricated structural steel, industrial components, and precision metal assemblies. The country's large domestic manufacturing ecosystem also strengthens export-oriented fabricated metal production.

Japan Fabricated Metal Products Market Trends

Japan maintains leadership in precision engineering, robotics, automotive manufacturing, aerospace technologies, and advanced industrial production. Demand is driven by high-value fabricated components used in automotive systems, industrial machinery, electronics manufacturing equipment, and precision-engineered structural assemblies. Continuous investment in factory automation and advanced manufacturing technologies further supports market growth.

India Fabricated Metal Products Market Trends

India is emerging as one of the fastest-growing markets within the region, supported by rapid urbanization, industrial corridor development, infrastructure expansion, manufacturing investments, and government initiatives promoting domestic production. Large-scale investments in highways, metro rail networks, airports, renewable energy facilities, industrial parks, and smart cities continue to increase demand for structural steel fabrication, transmission towers, fabricated bridges, and industrial equipment.

Competitive Landscape

The global fabricated metal products market remains fragmented, comprising numerous regional fabricators alongside large multinational manufacturers. Major companies compete through production capacity, technological expertise, integrated manufacturing capabilities, product quality, geographic reach, customer relationships, and value-added engineering services. Larger manufacturers continue strengthening their market positions through acquisitions, automation investments, and expansion into higher-margin fabricated products, while regional companies maintain competitiveness through customized manufacturing, shorter lead times, and specialized fabrication expertise.

Leading manufacturers continue prioritizing automation, digital manufacturing, strategic acquisitions, geographic expansion, sustainable production, and value-added fabrication services. Companies are increasingly differentiating themselves through engineering expertise, integrated manufacturing solutions, advanced production technologies, supply chain optimization, and environmentally responsible operations.

Key Industry Developments:

- In January 2026, Worthington Steel announced a Business Combination Agreement to acquire Klöckner & Co, aiming to create one of the leading steel service centers and metal processing companies across North America and Europe while significantly expanding its value-added processing portfolio and geographic footprint.

- In June 2026, Worthington Steel completed its acquisition of Klöckner & Co after satisfying all closing conditions, establishing a stronger global metal processing platform with an expanded product portfolio, broader end-market exposure, and enhanced operational scale across Europe and North America.

Companies Covered in Fabricated Metal Products Market

- Nucor Corporation

- ArcelorMittal

- Worthington Steel, Inc.

- Ryerson Holding Corporation

- Olympic Steel, Inc.

- Valmont Industries, Inc.

- Howmet Aerospace Inc.

- Parker Hannifin Corporation

- Mueller Industries, Inc.

- thyssenkrupp AG

- JFE Holdings, Inc.

- China Steel Corporation (CSC)

- BlueScope Steel Limited

- Russel Metals Inc.

- Klöckner & Co SE

- voestalpine AG

Frequently Asked Questions

The global fabricated metal products market is anticipated to be valued at US$ 348.5 billion in 2026.

The fabricated metal products market is projected to reach US$ 474.3 billion by 2033.

Key market trends include the increasing adoption of robotic welding and smart manufacturing technologies, growing investments in renewable energy and electrical grid infrastructure, expansion of electric vehicle manufacturing, rising demand for lightweight aluminum components, greater use of digital fabrication technologies, and increasing focus on sustainable, low-carbon metal production.

Structural metal products are anticipated to remain the leading product type segment, accounting for approximately 29.5% of the global market, supported by strong demand from commercial construction, transportation infrastructure, industrial facilities, bridges, and utility projects.

The global fabricated metal products market is expected to expand at a CAGR of 4.5% between 2026 and 2033.

Some of the leading companies include Nucor Corporation, ArcelorMittal, Worthington Steel, Howmet Aerospace, and Parker Hannifin Corporation.