- Metalworking & Fabrication

- Structural Steel Fabrication Market

Structural Steel Fabrication Market Size, Share, and Growth Forecast, 2026 - 2033

Structural Steel Fabrication Market by Service (Metal Welding, Metal Cutting, Others), Product (Carbon Steel, Alloy Steel, Others), Application, and Regional Analysis for 2026 - 2033

Structural Steel Fabrication Market Size and Trends Analysis

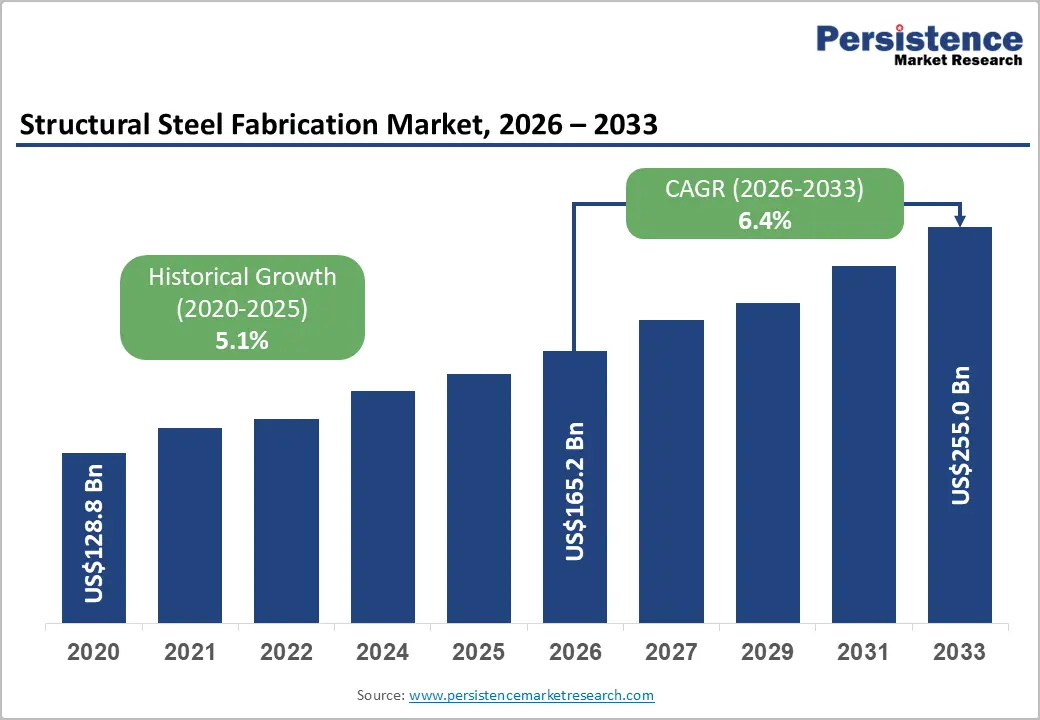

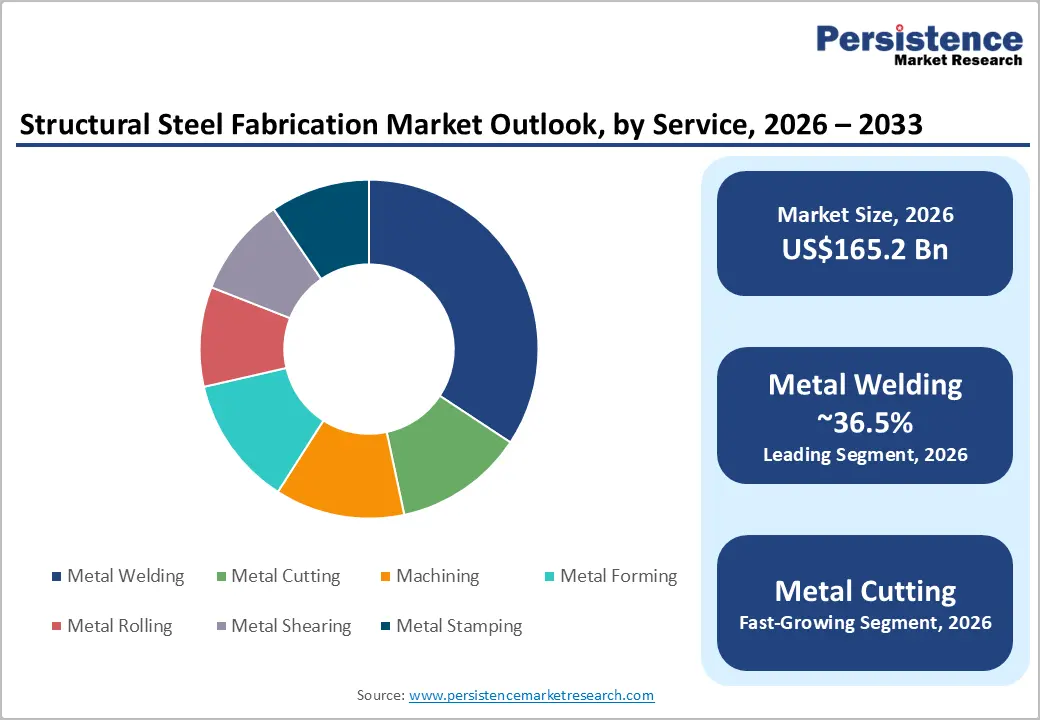

The global structural steel fabrication market size is likely to be valued at US$165.2 billion in 2026 and is expected to reach US$255.0 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033, driven by rising investments in transportation infrastructure, renewable energy facilities, industrial manufacturing plants, and logistics networks.

The market outlook is also supported by the stabilization of global steel demand and increasing public-sector investments in construction and grid modernization. Expanding electricity transmission infrastructure, data centers, transportation corridors, and industrial facilities are increasing demand for fabricated beams, trusses, frames, and engineered steel assemblies.

Key Industry Highlights:

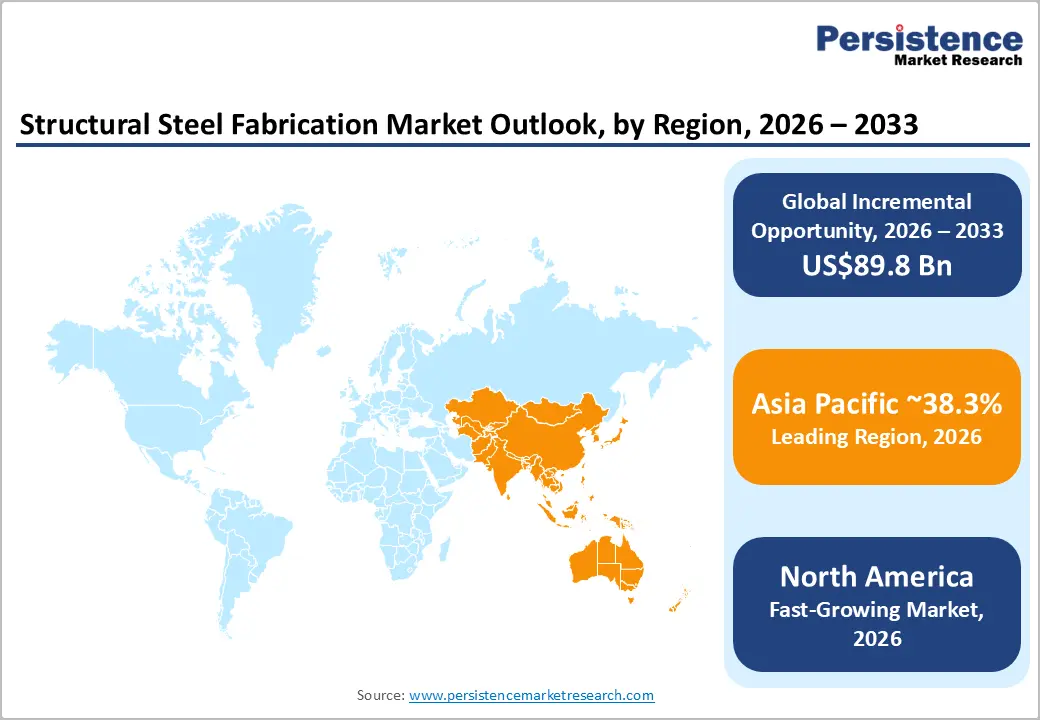

- Leading Region: Asia Pacific is projected to account for approximately 38.3% of the market share in 2026, supported by large-scale infrastructure development, manufacturing expansion, and rapid urbanization across China, India, and Southeast Asia.

- Fastest-growing Region: North America is projected to register the fastest growth during the forecast period, driven by rising investments in transportation infrastructure, renewable energy facilities, semiconductor plants, and industrial reshoring initiatives.

- Dominant Service: Metal welding is estimated to account for approximately 36.5% of the market share in 2026, due to its critical role in structural integrity, assembly strength, and infrastructure construction applications.

- Leading Product: Carbon steel is anticipated to dominate with 51.6% of market share in 2026, supported by its cost-effectiveness, high weldability, mechanical strength, and widespread use across commercial, industrial, and infrastructure projects.

DRO Analysis

Driver - Infrastructure Spending Continues to Sustain Structural Steel Demand

Large-scale infrastructure investments remain one of the strongest growth drivers for the structural steel fabrication market. Public works projects involving bridges, highways, airports, rail systems, ports, and utilities require substantial volumes of fabricated steel components due to their durability, load-bearing capability, and construction efficiency. Government-backed transportation modernization programs across North America, Europe, and Asia Pacific are expanding the addressable market for fabricators specializing in beams, columns, trusses, and connection systems.

In the U.S., infrastructure modernization programs and transportation funding continue to support steel-intensive projects, while industrial expansion in India and Southeast Asia is increasing demand for prefabricated steel systems. Structural steel also enables faster project completion compared with conventional materials, making it attractive for time-sensitive infrastructure projects. Fabricators with advanced detailing, erection, and project management capabilities are increasingly securing large contracts as project owners are prioritizing execution reliability, schedule certainty, and cost efficiency.

Electrification and Industrial Expansion Are Increasing Steel Intensity

The global transition toward electrification, grid expansion, and industrial modernization is significantly increasing demand for fabricated structural steel. Transmission towers, substations, battery manufacturing facilities, renewable energy plants, industrial warehouses, and data centers all rely heavily on fabricated steel frameworks. Rapid growth in electricity consumption and increasing investments in transmission infrastructure are driving demand for engineered steel structures capable of supporting complex industrial operations.

The market is also benefiting from rising investments in manufacturing facilities, logistics parks, semiconductor plants, and industrial automation centers. Structural steel fabrication is increasingly shifting from conventional building frames toward specification-driven industrial applications that require precision welding, automated cutting, and advanced machining capabilities. As manufacturing companies prioritize operational scalability and energy-efficient construction, demand is growing for high-strength steel assemblies and prefabricated structural systems that improve installation speed while reducing lifecycle costs.

Restraint - Excess Steel Capacity and Pricing Volatility Are Pressuring Margins

Global steel overcapacity remains a significant challenge for the structural steel fabrication market. Excess production capacity in major steel-producing regions has intensified pricing competition, creating margin pressure across fabrication activities. Volatile raw material prices frequently disrupt procurement planning and reduce profitability, particularly for fabricators operating under fixed-price contracts. When upstream steel producers lower prices to maintain utilization rates, fabricators may temporarily benefit from reduced material costs; however, aggressive pricing competition often compresses operating margins across the value chain.

The market also faces rising labor costs, transportation expenses, and compliance requirements related to emissions, workplace safety, and quality standards. Smaller fabricators with limited automation capabilities are particularly vulnerable as they lack the scale advantages required to absorb cost fluctuations efficiently. As a result, profitability increasingly depends on operational efficiency, supply chain management, automation investments, and value-added engineering services rather than commodity-driven fabrication volumes alone.

Opportunity - Low-Carbon Fabrication Is Creating Premium Market Segments

The transition toward low-carbon construction and environmentally compliant procurement practices is creating significant opportunities for structural steel fabricators. Governments and developers are increasingly prioritizing sustainable construction materials, lifecycle transparency, and lower embodied carbon in large-scale infrastructure and commercial projects. Regulatory frameworks related to emissions reporting and carbon accountability are encouraging the adoption of traceable, low-emission steel supply chains.

Fabricators capable of providing certified low-carbon steel solutions, digital material traceability, and lifecycle performance documentation are gaining access to premium infrastructure and commercial projects. Demand is particularly strong in Europe and North America, where sustainability-linked procurement requirements are influencing project awards. Companies investing in energy-efficient manufacturing systems, recycling integration, and advanced fabrication technologies are expected to strengthen their competitive positioning as environmentally focused construction standards become more widespread.

Industrialization in Emerging Economies Is Expanding Fabrication Demand

Rapid industrialization in emerging economies is generating substantial opportunities for structural steel fabrication companies. Expanding manufacturing bases, urban infrastructure development, logistics facilities, industrial parks, and renewable energy installations are increasing demand for fabricated steel structures across Asia Pacific, the Middle East, and selected African economies. India, in particular, continues to experience strong growth in industrial construction, warehousing, transportation infrastructure, and factory investments.

China is also shifting toward higher-value manufacturing activities and advanced industrial infrastructure, which is increasing demand for engineered structural steel systems. Industrial buildings, prefabricated warehouses, renewable energy facilities, and transportation networks require large volumes of fabricated steel components capable of supporting complex operational requirements. Fabricators that can localize production, shorten delivery timelines, and provide integrated design-to-installation services are expected to capture significant growth opportunities across developing markets.

Category-wise Analysis

Service Insights

Metal welding is anticipated to account for approximately 36.5% of the market share during the forecast period. Welding remains essential for joining beams, columns, trusses, and steel frames used in commercial towers, bridges, airports, and industrial plants. Major fabricators such as SteelFab and Canam continue investing in robotic submerged-arc welding and automated precision systems to improve throughput, weld consistency, and structural reliability. The segment also benefits from rising demand for prefabricated construction and large-scale infrastructure projects where weld quality directly affects load-bearing performance and safety standards.

Metal cutting is projected to be the fastest-growing service segment due to increasing adoption of CNC plasma cutting, laser cutting, and automated beam-processing technologies. Companies such as Kirby Building Systems and Pebsteel are expanding digitally controlled fabrication capabilities to improve production accuracy and reduce material waste. Demand for precision-cut steel components is rising across data centers, renewable energy facilities, modular construction, and advanced manufacturing plants, where faster turnaround times and tighter tolerances are becoming critical project requirements.

Product Insights

Carbon steel is anticipated to hold approximately 51.6% of the market share during the forecast period, maintaining its position as the leading product segment. Its dominance is supported by cost-effectiveness, high weldability, mechanical strength, and broad availability across construction and infrastructure projects. Carbon steel is widely used in warehouses, bridges, industrial facilities, and commercial buildings, with producers such as ArcelorMittal, JSW Steel, and Nippon Steel supplying standardized structural grades for large-scale applications. The material remains the preferred choice for high-volume projects requiring durability and efficient fabrication.

Alloy steel is expected to be the fastest-growing product segment owing to increasing demand for high-strength, corrosion-resistant, and performance-oriented structural materials. Companies including POSCO and Hyundai Steel are expanding advanced alloy steel offerings for marine infrastructure, industrial plants, long-span bridges, and seismic-resistant structures. Rising investments in energy infrastructure, transportation modernization, and heavy industrial projects are supporting stronger adoption of alloy steel, where enhanced durability and lifecycle performance are critical.

Regional Insights

North America Structural Steel Fabrication Market Trends

North America is expected to be the fastest-growing regional market during the forecast period, supported by infrastructure modernization, industrial reshoring initiatives, and investments in logistics, manufacturing, and energy infrastructure. Rising adoption of automation technologies, modular steel systems, and digitally integrated fabrication processes is strengthening regional fabrication capabilities. Demand for fabricated beams, trusses, columns, and engineered steel assemblies continues to increase across transportation, industrial, commercial, and energy projects.

U.S. Structural Steel Fabrication Market Trends

The U.S. dominates the North American market due to large-scale investments in highways, bridges, airports, rail systems, industrial facilities, and grid modernization projects. Infrastructure funding programs and manufacturing reshoring initiatives are increasing demand for fabricated structural steel across logistics hubs, semiconductor plants, electric vehicle facilities, and renewable energy projects.

The country is also experiencing rapid expansion in data centers and warehouse construction, creating strong demand for precision-engineered steel systems. U.S.-based fabricators are increasingly adopting robotic welding systems, CNC automation, and digital fabrication technologies to improve production efficiency and reduce labor dependency.

Canada Structural Steel Fabrication Market Trends

Canada is witnessing growing demand for fabricated structural steel in transportation infrastructure, commercial construction, mining projects, and renewable energy developments. Investments in urban transit systems, industrial facilities, and clean energy infrastructure are supporting market expansion. Canadian fabricators are also benefiting from increasing demand for prefabricated steel systems that improve construction efficiency in harsh climatic conditions.

Europe Structural Steel Fabrication Market Trends

Europe’s structural steel fabrication market is increasingly influenced by sustainability-focused regulations, low-carbon construction initiatives, and industrial modernization programs. The region is emphasizing environmentally optimized fabrication processes, energy-efficient buildings, and traceable steel supply chains. Demand for fabricated structural steel remains strong across transportation infrastructure, industrial retrofitting, renewable energy installations, and commercial construction projects.

Germany Structural Steel Fabrication Market Trends

Germany remains the largest regional market owing to its advanced industrial base, engineering expertise, and strong infrastructure investment activity. The country is heavily focused on industrial automation, renewable energy expansion, rail modernization, and sustainable construction practices. Demand for fabricated steel structures is increasing across manufacturing facilities, logistics centers, and energy infrastructure projects.

U.K. Structural Steel Fabrication Market Trends

The U.K. continues to generate substantial demand for fabricated structural steel across commercial construction, transportation infrastructure, and offshore wind projects. Urban redevelopment initiatives, railway modernization programs, and logistics infrastructure investments are supporting market growth. The country is also emphasizing low-carbon construction standards and modular building systems.

Asia Pacific Structural Steel Fabrication Market Trends

Asia Pacific remains the leading regional market, accounting for approximately 38.3% of global demand due to rapid urbanization, industrial expansion, manufacturing strength, and large-scale infrastructure development. The region benefits from integrated steel supply chains, cost-competitive manufacturing ecosystems, and strong government investment in transportation, industrial, and energy infrastructure. Structural steel fabrication demand continues to rise across industrial buildings, logistics parks, renewable energy facilities, airports, and urban commercial developments.

China Structural Steel Fabrication Market Trends

China remains the largest market in Asia Pacific due to extensive infrastructure construction, industrial expansion, and steel-intensive manufacturing operations. The country is increasingly shifting toward advanced manufacturing, industrial automation, and higher-value infrastructure projects that require engineered steel systems. Demand remains strong across transportation networks, logistics infrastructure, industrial facilities, and renewable energy installations.

India Structural Steel Fabrication Market Trends

India is projected to be one of the fastest-growing markets in the region due to rapid urban development, industrial corridor projects, renewable energy investments, and transportation infrastructure expansion. Government-backed infrastructure initiatives, warehousing growth, and rising manufacturing investments are significantly increasing demand for fabricated steel structures. Industrial zones, logistics parks, and commercial developments continue to support long-term market growth.

Competitive Landscape

The global structural steel fabrication market remains fragmented at the fabrication level but relatively consolidated upstream within steel production. Regional fabrication specialists compete alongside integrated steelmakers and engineered building solution providers.

Competition is based primarily on fabrication capacity, automation capabilities, project execution efficiency, engineering expertise, pricing, and geographic reach. Larger players continue to strengthen their positions through automation investments, vertical integration, and expansion into value-added industrial applications. Competitive intensity remains high due to excess steel production capacity, which continues to pressure pricing and operating margins across multiple regions.

Leading companies are prioritizing automation, digital fabrication, sustainability, and geographic expansion to strengthen market positioning. Firms are increasingly investing in CNC systems, robotic welding, modular construction capabilities, and integrated engineering services to improve operational efficiency and project execution. Emerging strategies also include low-carbon steel solutions, prefabricated construction systems, and integrated industrial infrastructure offerings.

Key Industry Developments:

- In April 2026, Vertiv announced the acquisition of BMarko Structures to expand its in-house structural fabrication capabilities for manufactured and prefabricated infrastructure solutions supporting AI-driven data center projects across North America.

- In January 2026, Steel Dynamics, Inc. partnered with SGH to pursue the acquisition of BlueScope Steel’s North American operations, aiming to strengthen domestic steelmaking and structural fabrication capabilities amid rising infrastructure and industrial demand in the U.S. market.

Companies Covered in Structural Steel Fabrication Market

- ArcelorMittal

- Nucor Corporation

- Steel Dynamics, Inc.

- Canam Group Inc.

- Severfield plc

- SteelFab, Inc.

- Tata Steel Limited

- JSW Steel Ltd.

- POSCO Holdings Inc.

- Hyundai Steel Company

- Nippon Steel Corporation

- Kirby Building Systems

- Pebsteel Buildings Co., Ltd.

- Zamil Steel Holding Company Ltd.

- BTD Manufacturing, Inc.

- Schuff Steel Company, LLC

Frequently Asked Questions

The global structural steel fabrication market is anticipated to reach US$165.2 billion in 2026.

The structural steel fabrication market is projected to reach approximately US$255.0 billion by 2033.

Key market trends include increasing adoption of automated welding and CNC cutting technologies, growth in modular and prefabricated construction, rising investments in renewable energy infrastructure, expansion of industrial manufacturing facilities, and growing demand for low-carbon and sustainable steel fabrication solutions.

Metal welding is the leading service segment, accounting for approximately 36.5% of the market share, due to its critical role in structural assembly, load-bearing performance, and infrastructure construction.

The structural steel fabrication market is projected to grow at a CAGR of 6.4% between 2026 and 2033.

Major companies include ArcelorMittal, Nucor/Kirby Building Systems, Steel Dynamics, Tata Steel, POSCO Group, and Canam Group.