- Metalworking & Fabrication

- Solid Welding Wires Market

Solid Welding Wires Market Size, Share, and Growth Forecast, 2026 - 2033

Solid Welding Wires Market by Material Type (Steel Solid Wires, Stainless‑Steel Welding Wires, Others), Application (Heavy Engineering, Automotive & EV, Others), Wire Type, and Regional Analysis for 2026 - 2033

Solid Welding Wires Market Size and Trends Analysis

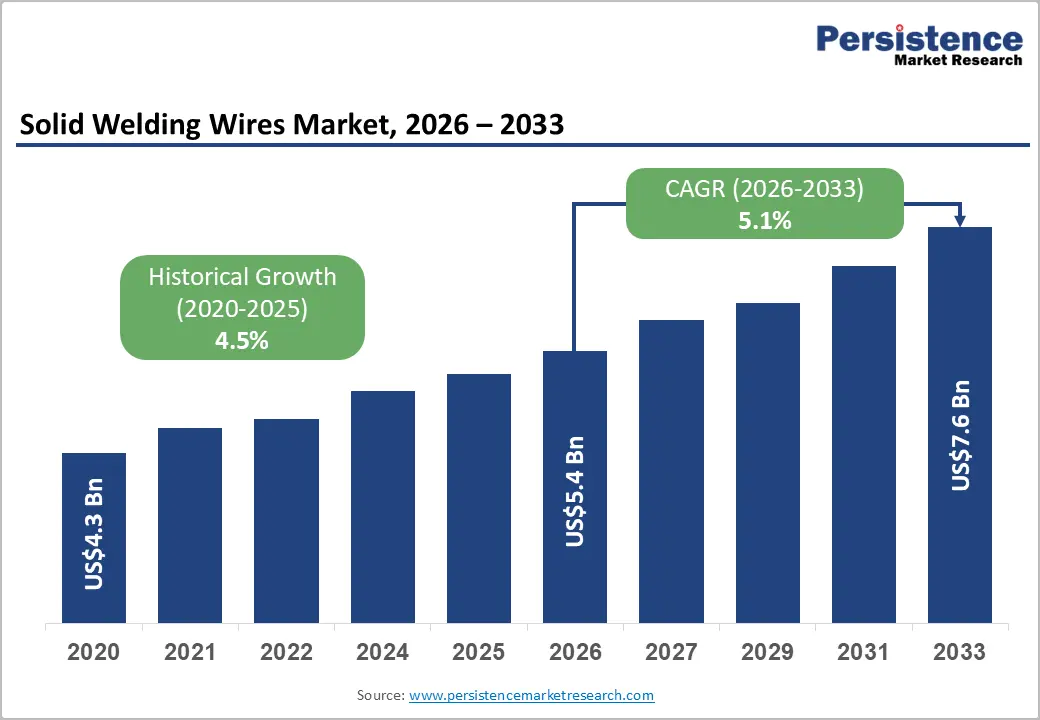

The global solid welding wires market size is likely to be valued at US$ 5.4 billion in 2026 and is expected to reach US$7.6 billion by 2033, growing at a CAGR of 5.1% during the forecast period from 2026 to 2033, driven by rising fabrication activities across heavy engineering, automotive manufacturing, infrastructure development, shipbuilding, and industrial machinery production.

Growing deployment of robotic welding systems and automated fabrication lines is increasing the demand for high-consistency welding consumables with superior arc stability and feed performance. Electric vehicle manufacturing and battery infrastructure investments are further supporting the consumption of premium-grade solid welding wires. Steel-based solid wires continue to dominate overall market volume, while Asia Pacific remains the largest manufacturing and consumption hub.

Key Industry Highlights:

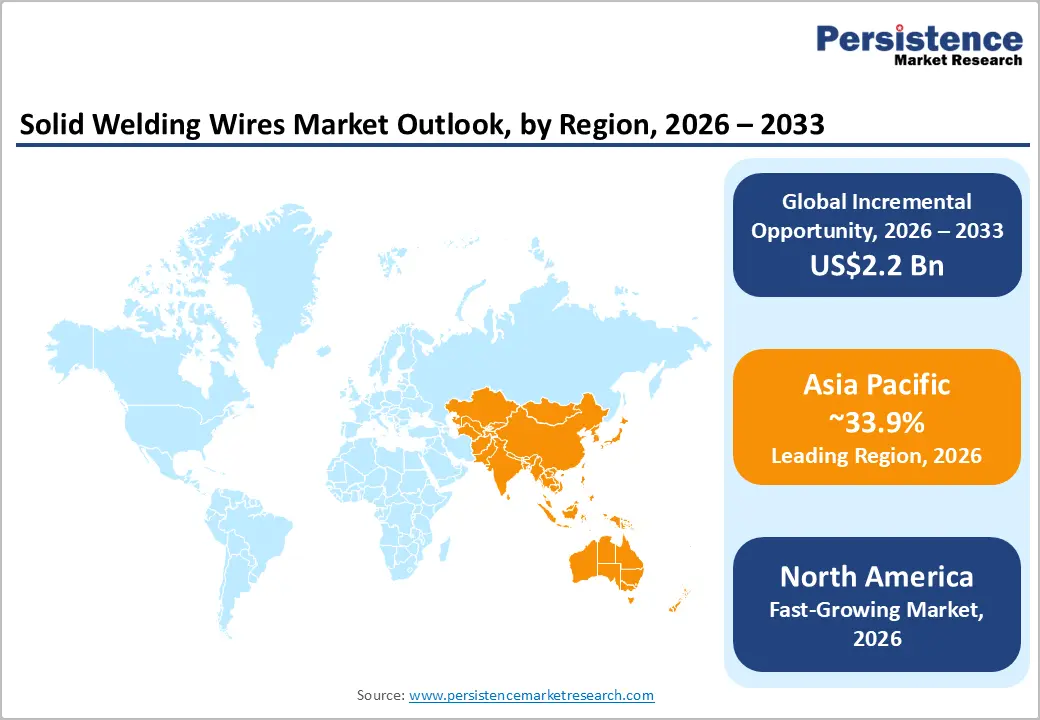

- Leading Region: Asia Pacific is projected to account for approximately 33.9% of the market share in 2026, supported by strong manufacturing activity across China, Japan, India, South Korea, and ASEAN economies.

- Fastest-growing Region: North America is projected to register the fastest growth during the forecast period, driven by rising investments in EV manufacturing, battery gigafactories, industrial automation, and robotic welding systems.

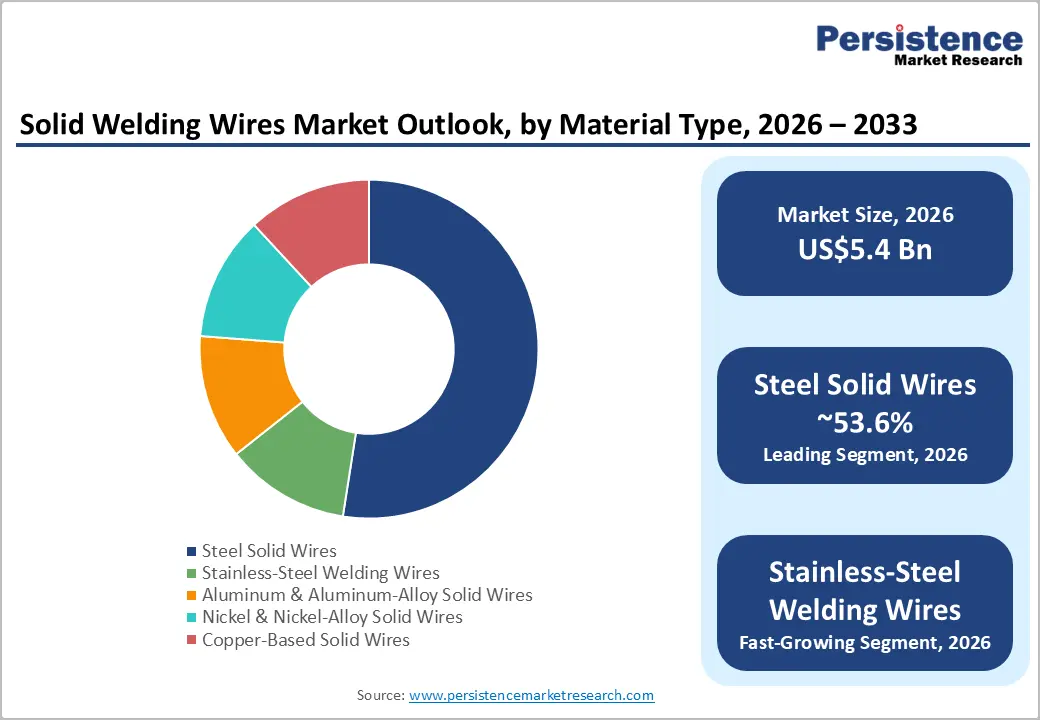

- Dominant Material Type: Steel solid wires are anticipated to account for 53.6% of the market share in 2026, due to extensive usage across construction, automotive, heavy engineering, pipelines, and industrial fabrication.

- Leading Application: Heavy engineering represents the largest application segment with an anticipated 37.3% market share in 2026, supported by continuous demand from industrial machinery, mining equipment, structural fabrication, and infrastructure development projects.

DRO Analysis

Driver - Industrial Automation and Robotic Welding Expansion Strengthens Demand for High-Performance Solid Wires

Industrial automation continues to accelerate the adoption of solid welding wires across manufacturing-intensive sectors. Automated and semi-automated welding systems require stable wire feeding, predictable metallurgical properties, and consistent arc performance, making solid welding wires highly suitable for robotic welding applications. Industrial robot installations surpassed 540,000 units globally in 2024, with Asia accounting for the majority of deployments due to rapid industrial modernization in China, Japan, South Korea, and India. Automotive manufacturers remain among the largest users of robotic welding systems, particularly for high-volume body-in-white and structural assembly operations.

This transition toward automation directly benefits producers of premium copper-coated and low-spatter solid wires. Manufacturers increasingly prioritize productivity optimization, weld repeatability, and reduced downtime in automated fabrication environments. As a result, demand is shifting toward technologically advanced welding consumables capable of supporting continuous production cycles and tighter quality tolerances.

Electric Vehicle Manufacturing and Infrastructure Expansion Increase Welding Consumables Consumption

The rapid expansion of electric vehicle manufacturing is creating sustained demand for solid welding wires across vehicle assembly, battery pack fabrication, charging infrastructure, and supporting industrial facilities. Global electric vehicle sales exceeded 17 million units in 2024 and are expected to continue rising as governments strengthen electrification targets and emissions regulations. EV manufacturing requires extensive welding across lightweight body structures, battery enclosures, mounting systems, and structural components.

Automotive OEMs are also increasing investments in robotic welding systems to improve production efficiency and consistency. This trend supports the consumption of gas-shielded solid wires capable of delivering precision welds in automated production environments. Beyond vehicle assembly, the construction of battery plants, semiconductor facilities, and EV component manufacturing sites is expanding demand for industrial fabrication services, thereby supporting broader market growth for welding consumables globally.

Restraint - Raw Material Price Volatility and Process Substitution Limit Market Expansion

Volatility in steel, nickel, aluminum, and alloy metal prices remains a major operational challenge for solid welding wire manufacturers. Welding consumable producers operate within a highly price-sensitive industrial supply chain, where fluctuations in base metal costs can directly compress margins and disrupt procurement planning. Price instability also affects purchasing behavior among fabrication companies, particularly in cost-sensitive construction and heavy engineering projects.

The market additionally faces competitive pressure from alternative welding consumables such as flux-cored wires and coated electrodes, which may provide advantages in positional welding, penetration characteristics, or productivity under certain operating conditions. Skilled labor shortages across the manufacturing and construction industries further complicate adoption in smaller fabrication facilities. Occupational health regulations related to welding fumes and hazardous emissions also require end users to invest in ventilation systems, extraction technologies, and safety compliance infrastructure, increasing the total cost of welding operations.

Opportunity - Rising Demand for Corrosion-Resistant Welding Solutions Creates Premium Product Opportunities

Stainless-steel and specialty-alloy solid welding wires represent one of the most commercially attractive growth opportunities within the market. Industrial sectors such as oil and gas, food processing, petrochemicals, marine engineering, and chemical manufacturing increasingly require corrosion-resistant and high-temperature welding materials capable of extending equipment life cycles and reducing maintenance costs.

Demand for stainless-steel solid wires is rising due to their superior resistance to oxidation, chemical exposure, and thermal stress. Manufacturers capable of offering application-specific wire chemistries and certification support are expected to gain competitive advantages in high-value industrial applications. This trend also supports pricing improvements and margin expansion, particularly in industries where operational reliability and weld integrity outweigh raw material cost considerations.

Localization of Manufacturing Capacity across Emerging Markets Supports Long-Term Growth

Industrial localization initiatives across India, Southeast Asia, and the Middle East are creating favorable conditions for regional production expansion. Governments are encouraging domestic manufacturing through infrastructure investments, industrial policy reforms, and local sourcing initiatives. Fabrication-intensive industries, including construction equipment, automotive manufacturing, shipbuilding, and industrial machinery, are expanding production footprints in emerging economies.

Several global welding consumables manufacturers are increasing investments in local manufacturing facilities to reduce lead times, strengthen distribution networks, and improve customer responsiveness. Localized production also helps companies mitigate import dependence and logistics disruptions. Rising industrialization across ASEAN economies and India is expected to create sustained long-term demand for welding consumables, particularly in automation-ready fabrication environments.

Category-wise Analysis

Material Type Insights

Steel solid wires are anticipated to account for 53.6% of market share during the forecast period, supported by extensive use across automotive manufacturing, construction, pipelines, shipbuilding, and industrial machinery fabrication. Mild-steel and low-alloy steel structures continue to dominate industrial production, making steel-based solid wires the preferred consumable category for high-volume welding operations.

For example, structural steel fabrication projects in commercial buildings and bridge construction heavily rely on gas-shielded steel MIG wires for continuous welding efficiency. Steel solid wires remain widely adopted because of their cost-effectiveness, consistent weld quality, and compatibility with automated MIG/MAG welding systems. Demand is particularly strong in heavy engineering and infrastructure projects where manufacturers require reliable consumables for repetitive fabrication work.

Stainless-steel solid wires are projected to be the fastest-growing material segment due to rising demand for corrosion-resistant and high-temperature welding applications. Industries such as petrochemicals, offshore oil and gas, marine engineering, pharmaceutical processing, and food manufacturing increasingly require durable weld performance in aggressive operating environments.

For instance, stainless-steel welding wires are extensively used in refinery piping systems, food-grade processing tanks, and chemical storage vessels. The segment is benefiting from stricter industrial quality standards and growing investments in long-life industrial infrastructure. Stainless-steel solid wires reduce maintenance requirements and improve operational reliability, making them increasingly attractive for critical industrial applications.

Application Insights

Heavy engineering is anticipated to account for 37.3% of market share in 2026, making it the leading end-use segment in the solid welding wires market. The segment includes mining equipment, agricultural machinery, industrial systems, cranes, pressure vessels, and large-scale structural fabrication. These industries require continuous welding operations and high-strength weld performance for thick metal assemblies. For example, construction equipment manufacturers and industrial machinery fabricators extensively use solid welding wires for chassis, frames, and load-bearing structures.

Growth in infrastructure modernization, industrial equipment manufacturing, and maintenance activities continues to support recurring demand for welding consumables. Heavy engineering companies prioritize high-productivity welding solutions capable of minimizing downtime and supporting large-volume fabrication environments, reinforcing long-term demand stability for solid welding wires.

Automotive and electric vehicle manufacturing are projected to be the fastest-growing application segments due to accelerating vehicle electrification and robotic welding adoption. EV production requires precision welding for battery enclosures, lightweight body structures, brackets, and underbody assemblies.

Automotive OEMs are increasingly integrating automated MIG welding systems to improve consistency and production efficiency. For example, EV battery plants and robotic vehicle assembly lines extensively utilize low-spatter solid wires for high-speed welding operations. The expansion of EV infrastructure and battery manufacturing facilities is also increasing demand for industrial fabrication services. High-performance solid welding wires capable of supporting automated production environments are gaining stronger adoption among automotive suppliers and Tier-1 component manufacturers.

Regional Insights

North America Solid Welding Wires Market Trends

North America is projected to be the fastest-growing regional market during the forecast period due to rising investments in electric vehicle production, robotic welding systems, battery manufacturing, and industrial reshoring initiatives. The region benefits from advanced manufacturing capabilities, high automation penetration, and strong adoption of premium welding consumables across automotive, aerospace, heavy engineering, and energy industries.

U.S. Solid Welding Wires Market Trends

The U.S. dominates the North American market because of its large industrial manufacturing base and extensive deployment of robotic welding systems. Automotive OEMs, aerospace manufacturers, and industrial machinery producers continue investing in automated welding lines to improve operational efficiency and reduce labor dependency. EV assembly plants, battery gigafactories, and semiconductor manufacturing projects are further strengthening demand for solid welding wires. Infrastructure modernization projects, including bridges, transportation systems, and industrial construction, also contribute to recurring welding consumables demand.

Canada Solid Welding Wires Market Trends

Canada represents an important market driven by energy infrastructure, mining equipment manufacturing, and heavy industrial fabrication activities. Oil sands operations, pipeline maintenance, and renewable energy projects continue generating demand for corrosion-resistant and low-alloy welding consumables. Canadian manufacturers are increasingly adopting automated welding technologies to improve productivity and comply with stricter occupational safety standards.

Europe Solid Welding Wires Market Trends

Europe remains a strategically important market supported by advanced industrial engineering, automotive manufacturing leadership, infrastructure modernization, and energy transition investments. The region maintains a strong demand for premium solid welding wires due to strict quality standards, occupational safety regulations, and widespread adoption of automated welding technologies. European manufacturers increasingly prioritize high-performance welding consumables capable of supporting precision fabrication and reduced emissions in industrial production environments.

Germany Solid Welding Wires Market Trends

Germany represents the largest market in Europe due to its dominant automotive, machinery manufacturing, and industrial engineering sectors. The country maintains one of the highest industrial robot adoption rates globally, particularly across automotive production facilities. German manufacturers prioritize high-consistency welding consumables for robotic welding systems used in vehicle assembly, heavy machinery, and precision industrial fabrication. Infrastructure upgrades and renewable energy projects also contribute to stable welding wire demand.

U.K. Solid Welding Wires Market Trends

The U.K. supports market growth through aerospace manufacturing, industrial refurbishment, transportation infrastructure, and offshore energy projects. Welding consumables are widely used across rail modernization, ship repair, and heavy fabrication industries. Manufacturers are increasingly adopting cleaner and lower-emission welding technologies to comply with occupational safety and environmental standards.

Italy Solid Welding Wires Market Trends

Italy remains an important contributor to the regional market due to its strong industrial machinery, metal fabrication, and automotive component manufacturing sectors. Italian fabrication companies continue investing in automated welding systems to improve operational efficiency and export competitiveness. Demand for solid welding wires remains stable across industrial equipment and precision manufacturing applications.

Asia Pacific Solid Welding Wires Market Trends

Asia Pacific represents the largest regional market, accounting for approximately 33.9% of global revenue. The region benefits from large-scale industrial manufacturing, rapid urbanization, infrastructure expansion, and strong automotive production across China, Japan, India, South Korea, and ASEAN countries. Rising adoption of robotic welding systems and industrial automation is significantly increasing demand for automation-compatible solid welding wires throughout the region.

China Solid Welding Wires Market Trends

China dominates the Asia Pacific market because of its extensive automotive production, shipbuilding capacity, construction activity, and heavy engineering industries. The country remains the world’s largest EV manufacturing center, generating substantial demand for welding consumables used in battery enclosures, lightweight body structures, and industrial equipment fabrication. Large-scale infrastructure and transportation projects continue to support recurring demand for steel solid wires across structural fabrication applications.

Japan Solid Welding Wires Market Trends

Japan maintains a strong position in high-precision manufacturing and robotic welding adoption. Automotive manufacturers and industrial machinery producers rely heavily on automated MIG/MAG welding systems that require high-consistency welding consumables. Demand for premium low-spatter and high-feedability solid wires remains strong across automotive assembly, robotics manufacturing, and precision engineering applications.

India Solid Welding Wires Market Trends

India is emerging as one of the fastest-growing markets in the region due to infrastructure development, industrial expansion, railway modernization, and increasing automotive manufacturing investments. Government-supported domestic manufacturing initiatives are encouraging localization of fabrication and industrial production activities. Demand for steel solid wires is rising across construction equipment manufacturing, transportation infrastructure, and industrial fabrication sectors.

Competitive Landscape

The global solid welding wires market remains highly fragmented, with competition distributed across multinational welding consumables manufacturers, regional suppliers, and specialized industrial welding companies. Market leadership is generally determined by technological capability, product portfolio breadth, automation compatibility, and distribution reach rather than pure production scale alone.

Leading companies are increasingly focusing on automation-compatible welding consumables, localized manufacturing expansion, and premium product development. Competitive differentiation is being achieved through application engineering support, technical certifications, stronger distributor networks, and strategic investments in robotic welding technologies. Suppliers are also transitioning toward solution-based business models combining welding consumables, equipment integration, and productivity optimization services.

Key Industry Developments:

- In April 2025, voestalpine Böhler Welding announced the launch of its EMK Ultra copper-coated solid wire portfolio for non- and low-alloy steel applications, designed to improve arc stability, wire feed reliability, and productivity across manual and fully automated welding environments.

- In June 2025, ESAB Corporation announced the acquisition of EWM GmbH, a German welding automation and heavy industrial welding technology company, to strengthen its automation, robotics, and advanced welding solutions portfolio for industrial fabrication markets.

Companies Covered in Solid Welding Wires Market

- Lincoln Electric

- ESAB Corporation

- voestalpine Böhler Welding

- Kobe Steel (KOBELCO Welding)

- Illinois Tool Works (Hobart Brothers)

- Hyundai Welding Co., Ltd.

- Kiswel Ltd.

- Ador Welding Ltd.

- Panasonic Welding Systems Co., Ltd.

- Tianjin Bridge Welding Materials Group Co., Ltd.

- Nippon Steel Welding & Engineering Co., Ltd.

- Chosun Welding Co., Ltd.

- Gedik Welding

- Fronius International GmbH

- Welding Alloys Group

- Daihen Corporation

Frequently Asked Questions

The global solid welding wires market is anticipated to be valued at US$5.4 billion in 2026.

The solid welding wires market is expected to reach approximately US$7.6 billion by 2033.

Key trends include the growing adoption of automated MIG/MAG welding systems, increasing EV and battery manufacturing activities, rising demand for low-spatter and high-feedability welding consumables, expansion of localized manufacturing facilities, and stronger adoption of stainless-steel and low-alloy welding wires for high-performance industrial applications.

Steel solid wires remain the leading material segment, accounting for an anticipated 53.6% market share, due to widespread usage across construction, automotive, heavy engineering, pipelines, and structural fabrication applications.

The solid welding wires market is projected to grow at a CAGR of 5.1% between 2026 and 2033.

Major companies include Lincoln Electric, ESAB Corporation, voestalpine Böhler Welding, Kobe Steel (KOBELCO), and Illinois Tool Works (ITW/Hobart).