- Inks, Coatings, Adhesives & Sealants (ICAS)

- EVA Resins & Films Market

EVA Resins & Films Market Size, Share, and Growth Forecast 2026 - 2033

EVA Resins & Films Market by Product Type (Vinyl Acetate Modified Polyethylene, Thermoplastic Ethylene Vinyl Acetate, Ethylene Vinyl Acetate Rubber), Application (Packaging, Solar Panel Encapsulation, Laminated Glass, Adhesives, Sports & Footwear, Automotive & Electronics, Other), Industry (Packaging, Renewable Energy, Construction, Footwear, Other), and Regional Analysis for 2026 - 2033

EVA Resins & Films Market Size and Trend Analysis

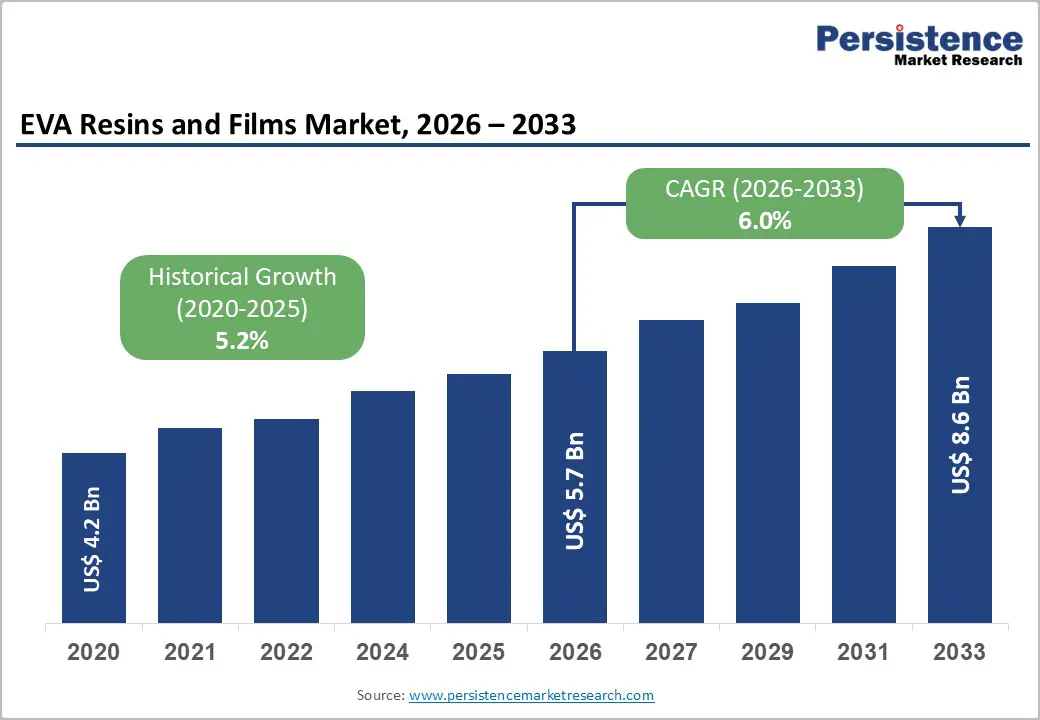

The global EVA resins & films market size is valued at US$ 5.7 billion in 2026 and is projected to reach US$ 8.6 billion by 2033, growing at a CAGR of 6.0% between 2026 and 2033.

This robust growth trajectory is primarily driven by three converging macro-forces: the global acceleration of solar photovoltaic (PV) installations, sustained expansion in flexible packaging demand, and rising adoption of EVA interlayer films in architectural and automotive laminated safety glass. According to the International Energy Agency (IEA), global solar PV capacity additions reached a record of approximately 420 GW in 2023, with each gigawatt of installed capacity requiring approximately 0.5-0.7 million square meters of EVA encapsulant film. Simultaneously, the global flexible packaging sector, one of the largest downstream consumers of EVA resins, continues to grow at a steady 3.5-4.0% annual rate, driven by urbanization, e-commerce growth, and regulatory-compliant, lightweight packaging formats across food and consumer goods industries worldwide.

Key Industry Highlights:

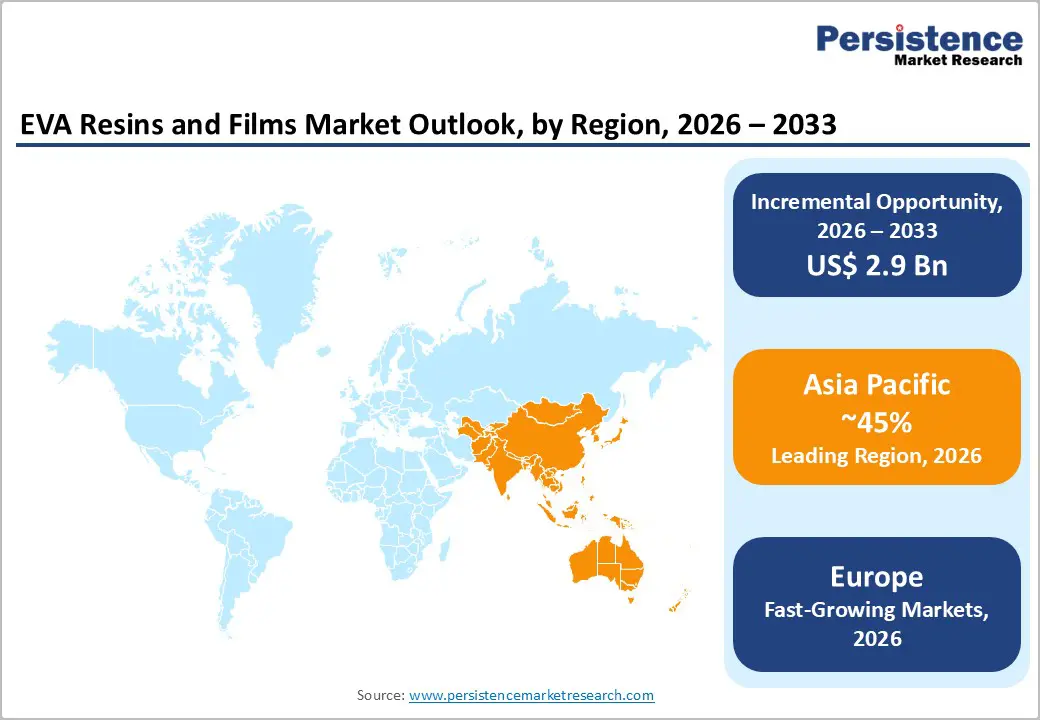

- Leading Region: Asia Pacific commands the largest share of the global EVA Resins & Films market, with 45% market share, driven by China’s record 217 GW solar capacity addition in 2023, large-scale packaging demand, and a cost-competitive, vertically integrated polymer manufacturing ecosystem spanning South Korea, Japan, India, and Southeast Asia.

- Fastest Growing Region: Europe is the fastest-growing region, with a highly regulated and sustainability-driven market, where environmental compliance and circular-economy alignment are increasingly central to EVA resin and film procurement.

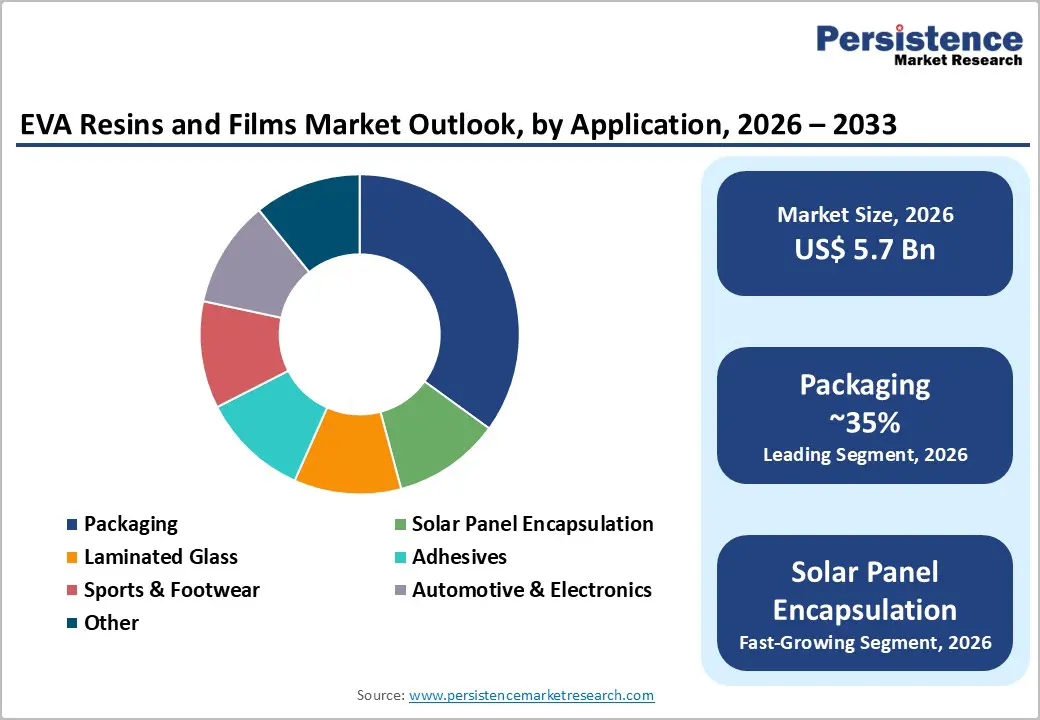

- Dominant Segment: The Packaging application segment leads with approximately 35% share, underpinned by EVA resins’ dual food-contact compliance (FDA 21 CFR 177.1350 and EU Regulation 10/2011) and superior low-temperature seal performance across flexible food, beverage, and consumer goods packaging formats globally.

- Fastest Growing Segment: Solar Panel Encapsulation is the fastest-growing application segment, fueled by record global PV capacity additions, stringent IEC 61215/61730 module durability standards, and growing demand for high-transparency, rapid-cure EVA encapsulant films for advanced bifacial and heterojunction solar modules.

- Key Market Opportunity: Development and commercialization of ISCC PLUS-certified, bio-attributed EVA grades aligned with the EU PPWR mandate and corporate SBTi decarbonization commitments represent a high-value premium opportunity for technology-forward producers to differentiate and capture margin uplift through the forecast period.

| Key Insights | Details |

|---|---|

| EVA Resins & Films Size (2026E) | US$ 5.7 Bn |

| Market Value Forecast (2033F) | US$ 8.6 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.0% |

| Historical Market Growth (2020 - 2025) | 5.2% |

DRO Analysis

Drivers - Surging Solar PV Installations Driving EVA Encapsulant Film Demand

EVA encapsulant films function as essential protective lamination layers in photovoltaic modules, securing the front glass, solar cells, and backsheet while safeguarding the system from moisture intrusion, UV degradation, and mechanical stress over an operational lifespan exceeding 25 years. The rapid global expansion of solar energy installations is generating sustained structural demand for these specialized films.

In 2023, the International Energy Agency reported approximately 507 GW of new renewable electricity capacity, with solar PV representing more than three-quarters of total additions. China alone installed 217 GW of new solar capacity, reinforcing its position as the primary driver of EVA film consumption. In the United States, the Inflation Reduction Act and, in Europe, the REPowerEU initiative are further accelerating long-term demand for high-quality encapsulant films.

Rising Flexible Packaging Demand Across Food and Consumer Goods Sectors

The flexible packaging sector constitutes the largest end-use market for EVA resins globally, owing to EVA’s combination of optical clarity, low heat-seal initiation temperatures, moisture resistance, and validated food-contact safety. These attributes make EVA a preferred material for blown films, stand-up pouches, lidding films, and multilayer laminates. EVA grades used in food packaging comply with FDA 21 CFR 177.1350 in the United States and EU Regulation 10/2011, enabling broad regulatory acceptance across major markets.

According to the Flexible Packaging Association, this segment represents nearly 19% of total U.S. packaging shipment value. Expanding urban populations, rising e-commerce activity, and demand for single-serve, resealable formats continue to support volume growth. Additionally, the EU’s Packaging and Packaging Waste Regulation, targeting 65% recyclability by 2040, is accelerating the adoption of advanced EVA-based mono-material solutions.

Restraints - Volatility in Ethylene and Vinyl Acetate Monomer (VAM) Feedstock Prices

EVA resins are produced through high-pressure copolymerization of ethylene and vinyl acetate monomer (VAM), both petrochemical derivatives susceptible to crude oil price cycles and supply chain disruptions. The U.S. Energy Information Administration (EIA) recorded crude oil price fluctuations exceeding 40% between 2022 and 2023, significantly compressing margins across the EVA production value chain.

Producers face structural difficulty passing cost increases downstream, particularly in price-sensitive packaging and footwear markets where buyers maintain strict procurement discipline. Prolonged feedstock volatility deters long-term capital investment planning and constrains capacity expansion by smaller regional manufacturers, limiting industry responsiveness to demand surges during peak solar installation cycles and packaging seasonality.

Emergence of Polyolefin Elastomer (POE) Encapsulants as Competitive Substitutes

In the critical solar panel encapsulation application, EVA’s dominance is increasingly challenged by polyolefin elastomer (POE) films, which offer superior resistance to potential-induced degradation (PID), lower moisture vapor transmission rates, and enhanced durability in humid tropical climates. Major module manufacturers, including LONGi Green Energy and JA Solar, have progressively shifted material specifications toward POE or POE/EVA hybrid laminates for premium product lines.

POE’s share in encapsulant film demand is projected to grow from approximately 15% in 2023 to over 25% by 2028, representing a material substitution risk for EVA film producers that fail to innovate in next-generation anti-PID or ultra-rapid-cure EVA encapsulant formulations.

Opportunities - Bio-Based and Recyclable EVA Development Aligned with Circular Economy Policies

Stringent circular economy regulations and corporate net-zero commitments are creating a substantial premium-market opportunity for manufacturers of bio-based and chemically recyclable EVA grades. The EU Green Deal and the Packaging and Packaging Waste Regulation (PPWR 2025/40) require all plastic packaging sold in the European Union to be fully recyclable or reusable by 2030, significantly accelerating demand for sustainable EVA solutions.

In September 2024, Dow Inc. and Mitsui Chemicals introduced an ISCC PLUS mass-balance-certified biomass-attributed EVA resin, marking the industry’s first commercially viable bio-circular alternative across all vinyl acetate content ranges. Concurrently, Arkema S.A. expanded its Evatane™ bio-attributed EVA portfolio for customers pursuing low-carbon materials. Producers demonstrating verified emissions reductions and recyclability performance now receive preferential supplier status from multinational brands aligned with SBTi pathways.

Growing EV Adoption Expanding Demand for Laminated Glass and Battery Applications

The global shift toward electric vehicles (EVs) is generating expanding, structural demand for EVA films beyond traditional solar and packaging applications. EVA-based interlayer films are increasingly specified for automotive laminated safety glass, such as windshields, side windows, and panoramic roof panels, due to their superior optical clarity, UV absorption, acoustic damping, and strong adhesion.

According to the IEA Global EV Outlook 2024, EV sales surpassed 17 million units in 2024, representing approximately 18% of global vehicle sales, with adoption expected to accelerate throughout the decade. Each EV incorporates an estimated 4-8 square meters of laminated glass, a requirement that is being amplified by the growing use of panoramic roof designs. Additionally, emerging battery pack encapsulation and thermal management applications are creating new high-growth opportunities. Leading suppliers such as Kuraray Co., Ltd. and 3M Company continue to invest in advanced automotive-grade EVA interlayer technologies to capture this expanding market.

Category-wise Analysis

Product Type Insights

Vinyl Acetate Modified Polyethylene maintains the leading position among the three product type segments, representing nearly 48% of total EVA resins and films volume in 2025. Its dominance stems from extensive utilization in flexible packaging, blown films, agricultural films, and industrial coatings, where its lower vinyl acetate content (typically 9-18%) offers an optimal combination of clarity, flexibility, processability, and cost efficiency. These properties align closely with the high-volume needs of the food and consumer goods packaging industry, the largest downstream market for EVA.

Its compatibility with existing LDPE extrusion infrastructure minimizes capital investment for film converters. Furthermore, regulatory approvals under FDA 21 CFR 177.1350 and EU Regulation 10/2011 reinforce its market leadership. Ongoing capacity expansions by Celanese Corporation and LyondellBasell Industries are expected to support their continued dominance through 2033.

Application Insights

The Packaging segment remains the largest application area for EVA resins and films, accounting for approximately 35% of global consumption in 2025. This leadership is driven by the alignment of EVA’s inherent properties, such as low heat-seal initiation temperatures, strong moisture-barrier performance, optical clarity, and broad food-contact regulatory compliance, with the core technical requirements of flexible packaging. According to the Flexible Packaging Association, this segment represents nearly 19% of total U.S. packaging shipment value, underscoring its substantial scale.

The Solar Panel Encapsulation segment is the fastest-growing application, supported by record global photovoltaic capacity additions and stringent durability standards. IEC 61215 and IEC 61730 require encapsulant materials to maintain optical and mechanical stability for at least 25 years, prompting continuous EVA innovation for advanced PV module technologies.

Industry Insights

The packaging industry represents the largest share of global EVA resins and films consumption, accounting for approximately 38% in 2025. Its dominance is driven by EVA’s superior sealing performance, effective barrier properties, and broad regulatory compliance across modern retail, food service, and pharmaceutical packaging supply chains, all of which are essential. The Renewable Energy sector is the fastest-growing end-use category, supported by unprecedented global investment in solar power.

According to IRENA, renewable energy investment reached USD 1.8 trillion in 2023, with solar PV receiving the largest share of capital. The Construction industry ranks third, leveraging EVA films as interlayers in architectural laminated safety glass. The EU’s Energy Performance of Buildings Directive, mandating near-zero energy standards by 2030, is further stimulating demand for high-performance laminated glazing systems.

Regional Insights

North America EVA Resins & Films Trends

North America represents a mature yet steadily expanding market for EVA resins and films, with the United States serving as the principal center for both production and consumption. The region benefits from a highly developed petrochemical infrastructure along the Gulf Coast, where ExxonMobil Corporation, Dow Inc., and Celanese Corporation operate large-scale and cost-efficient EVA manufacturing facilities.

The Inflation Reduction Act (IRA) of 2022 has significantly accelerated domestic solar panel manufacturing and installation, contributing to sustained growth in demand for EVA encapsulant films. This trend is reinforced by ongoing U.S.-China trade tensions, which are prompting greater localization of solar supply chains. Regulatory oversight from the EPA and FDA, including food-contact authorization under 21 CFR 177.1350, ensures broad market access. Additionally, H.B. Fuller’s 2024 partnership with Shanghai HIUV New Materials reflects strategic alignment with reshoring initiatives, while innovation in rapid-cure and anti-PID film grades remains a key competitive focus for regional suppliers.

Europe EVA Resins & Films Trends

Europe represents a highly regulated and sustainability-driven market, where environmental compliance and circular-economy alignment are increasingly central to EVA resin and film procurement. Germany, France, Spain, and the U.K. form the region’s core markets, supported by ambitious targets under the EU REPowerEU program, which aims to deploy 600 GW of solar capacity by 2030.

Arkema S.A. continues to strengthen regional leadership through its Evatane™ bio-attributed EVA portfolio, while Kuraray Co., Ltd. supplies high-performance Trosifol™ EVA interlayer films for architectural and automotive safety glass in line with the Energy Performance of Buildings Directive. The EU’s PPWR and Green Deal are accelerating the adoption of ISCC PLUS-certified and bio-based EVA grades, while the Carbon Border Adjustment Mechanism, effective from 2026, is expected to benefit lower-carbon domestic production. Emerging module assembly hubs in Spain and Poland are further expanding regional demand.

Asia Pacific EVA Resins & Films Trends

Asia Pacific remains the dominant regional market for EVA resins and films, accounting for an estimated 45% of global consumption. China serves as both the largest producer and consumer, driven by its extensive solar module manufacturing base, flexible packaging sector, and sizeable footwear export industry. In 2023, the National Energy Administration reported over 217 GW of new solar capacity additions, positioning China as the most influential market for EVA encapsulant films.

Leading domestic suppliers such as Hangzhou First Applied Material Co. and Shanghai HIUV New Materials continue expanding multi-country production across Thailand and Vietnam to meet rising domestic and export demand. India and ASEAN markets represent the next major growth front, supported by India’s 500-GW renewable energy target by 2030. South Korea and Japan further strengthen regional leadership through advanced EVA technologies and high-value specialty grades, solidifying Asia Pacific’s competitive position through 2033.

Competitive Landscape

The global EVA resins and films market displays a moderately consolidated structure at the resin production level, dominated by a core group of large petrochemical companies, including Dow Inc., ExxonMobil Corporation, LyondellBasell Industries, Celanese Corporation, and Hanwha Solutions Corporation, which collectively command a substantial share of global capacity. In contrast, the film conversion segment is more fragmented, comprising numerous regional manufacturers specializing in solar encapsulants, flexible packaging, and laminated glass applications. Competitive differentiation is driven by proprietary processing technologies such as Lupotech™, versatility in vinyl acetate content, sustainability certifications including ISCC PLUS, and innovations in rapid-cure and anti-PID film formulations. Strategic capacity expansions in Southeast Asia, targeted mergers and acquisitions, and partnerships between resin producers and converters are shaping the sector’s competitive trajectory through the forecast period.

Key Developments:

- October 2025: Dow USA launched next-generation Ethylene Vinyl Acetate resins with improved flexibility, adhesion, and transparency specifically for packaging and solar panel applications, enhancing product performance and sustainability credentials across key end-use markets.

- March 2025: Scottish start-up EVA Biosystems successfully engineered a biodegradable EVA polymer integrating enzyme-producing bacteria, triggering material breakdown in seawater while maintaining standard EVA performance during use, a breakthrough in end-of-life polymer management.

- September 2024: Mitsui Chemicals introduced a next-generation EVA resin formulation with significantly reduced VOC emissions and enhanced recyclability, catering to rising regulatory pressure across the EU and North America and reinforcing sustainability credentials among key global packaging and film buyers.

Top Companies in EVA Resins & Films

- Hanwha Solutions Corporation (Seoul, South Korea) is one of the world’s largest integrated producers of EVA resin and encapsulant films, operating advanced materials divisions that manufacture solar-grade EVA sheets at a significant industrial scale. Its vertically integrated production model, advanced materials R&D capabilities, and established relationships with global module manufacturers underpin its top-tier competitive standing in the global EVA market.

- Dow Inc. (Midland, Michigan, U.S.) is a global chemical and materials science leader and a major EVA copolymer resin producer serving packaging, adhesives, wire and cable, and solar applications across all geographies. Dow’s broad application coverage, global manufacturing network, deep specialty EVA formulation expertise, and commitment to circular chemistry position it as a definitive market leader across both commodity and premium EVA segments.

- Celanese Corporation (Irving, Texas, U.S.) is a premier EVA copolymer resin supplier renowned for its technical depth in specialty grades for hot-melt adhesives, coatings, solar encapsulants, and high-performance flexible films. Celanese’s global distribution network, multi-sector application coverage across packaging, construction, and renewable energy, and its commitment to sustainable-grade development make it a pivotal supplier for film converters and brand owners worldwide.

Companies Covered in EVA Resins & Films Market

- Hanwha Solutions Corporation

- Dow Inc.

- Celanese Corporation

- 3M Company

- ExxonMobil Corporation

- LyondellBasell Industries

- Arkema S.A.

- Hangzhou First Applied Material Co.

- Kuraray Co., Ltd.

- Mitsui Chemicals Inc.

- H.B. Fuller Company

- Shanghai HIUV New Materials Co.

- Jiangsu Sveck Photovoltaic New Material Co.

- LG Chem Ltd.

- Bridgestone Corporation

Frequently Asked Questions

The global EVA Resins & Films market is valued at US$ 5.7 Bn in 2026 and is projected to reach US$ 8.6 Bn by 2033, expanding at a forecast CAGR of 6.0% over the 2026-2033 period. The market recorded a historical CAGR of 5.2% between 2020 and 2025, growing from a base of US$ 4.2 Bn in 2020, reflecting consistent demand growth across solar, packaging, and specialty film end-use sectors globally.

The primary demand drivers include the global acceleration of solar photovoltaic installations, with the IEA reporting record renewable capacity additions of approximately 507 GW in 2023, of which solar PV constituted over three-quarters, and sustained flexible packaging demand growth at approximately 3.5-4.0% annually, supported by evolving food safety regulations, e-commerce expansion, and the global shift toward lightweight, convenient packaging formats.

The Packaging application segment holds the largest share at approximately 35% of total EVA consumption globally, driven by the widespread use of EVA resins in flexible food packaging, where low heat-seal initiation temperatures, moisture resistance, and dual compliance with FDA 21 CFR 177.1350 and EU Regulation 10/2011 food contact standards make EVA the preferred material for film converters and brand owners serving the food, beverage, and pharmaceutical industries.

Asia Pacific holds the largest regional share, estimated at 45% of global EVA resins and films consumption, driven by China’s world-leading solar PV installations exceeding 217 GW in 2023, an expansive flexible packaging industry, large-scale footwear manufacturing, and a deeply integrated polymer supply chain ecosystem spanning South Korea, Japan, India, and Southeast Asia, all supported by strong national renewable energy targets.

The development and commercialization of ISCC PLUS-certified, bio-attributed EVA resins and films aligned with the EU’s Packaging and Packaging Waste Regulation (PPWR) mandate represents the most significant strategic opportunity, further reinforced by corporate SBTi net-zero commitments and growing demand from multinational brand owners for verifiable, low-carbon polymer solutions across packaging and solar encapsulant applications throughout the 2026-2033 forecast period.

The leading companies operating in the global EVA Resins & Films market include Hanwha Solutions Corporation, Dow Inc., Celanese Corporation, 3M Company, ExxonMobil Corporation, LyondellBasell Industries, Arkema S.A., Hangzhou First Applied Material Co., Kuraray Co., Ltd., Mitsui Chemicals Inc., and H.B. Fuller Company, among others.