- Inks, Coatings, Adhesives & Sealants (ICAS)

- Montan Wax Market

Montan Wax Market Size, Share, and Growth Forecast 2026 - 2033

Montan Wax Market by Product Type (Crude Montan Wax, Refined Montan Wax, Bleached Montan Wax, Modified / Esterified Montan Wax, Industrial Grade Montan Wax), Form (Solid, Liquid, Paste / Dispersion), by Function (Lubricants, Emulsifiers, Coating Agents, Release Agents, Thickening Agents, Dispersants, Anti-corrosion Agents, Processing Aids), Application, End-user, and Regional Analysis, 2026 - 2033

Montan Wax Market Size and Trend Analysis

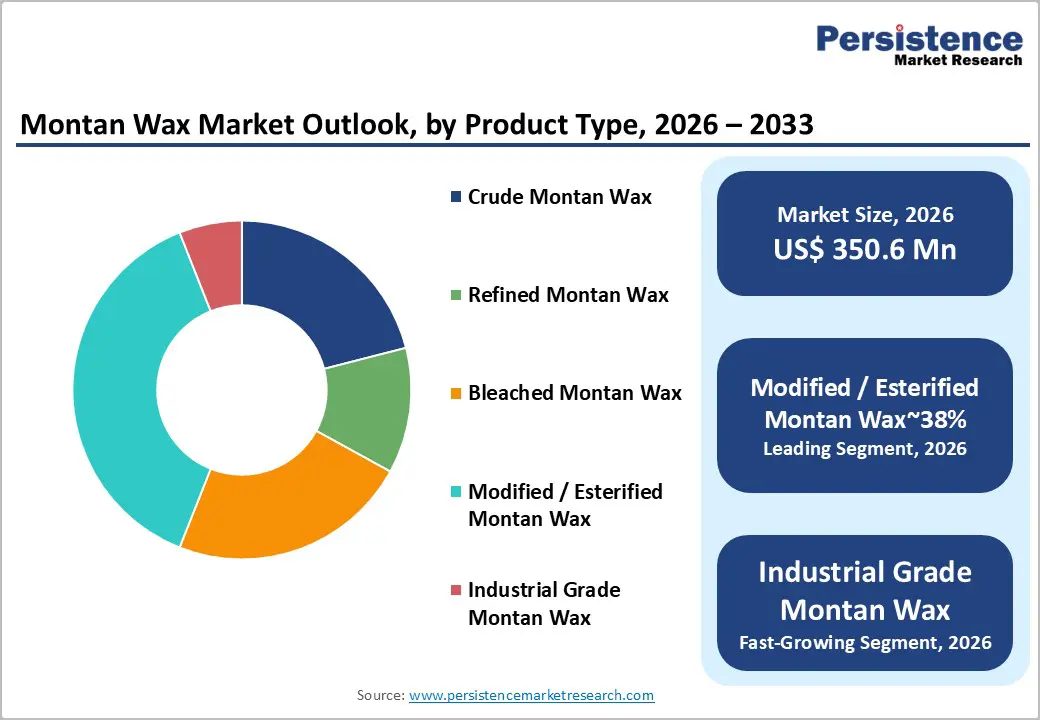

The global montan wax market size is likely to be valued at US$ 350.6 million in 2026 and is expected to reach US$ 486.8 million by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033.

It is experiencing steady and broadening growth, underpinned by the material’s unique combination of high melting point, chemical inertness, excellent lubricity, and natural lignite-derived origin that makes it functionally irreplaceable across polishes, plastics processing, printing inks, and electrical insulation applications.

Key Industry Highlights:

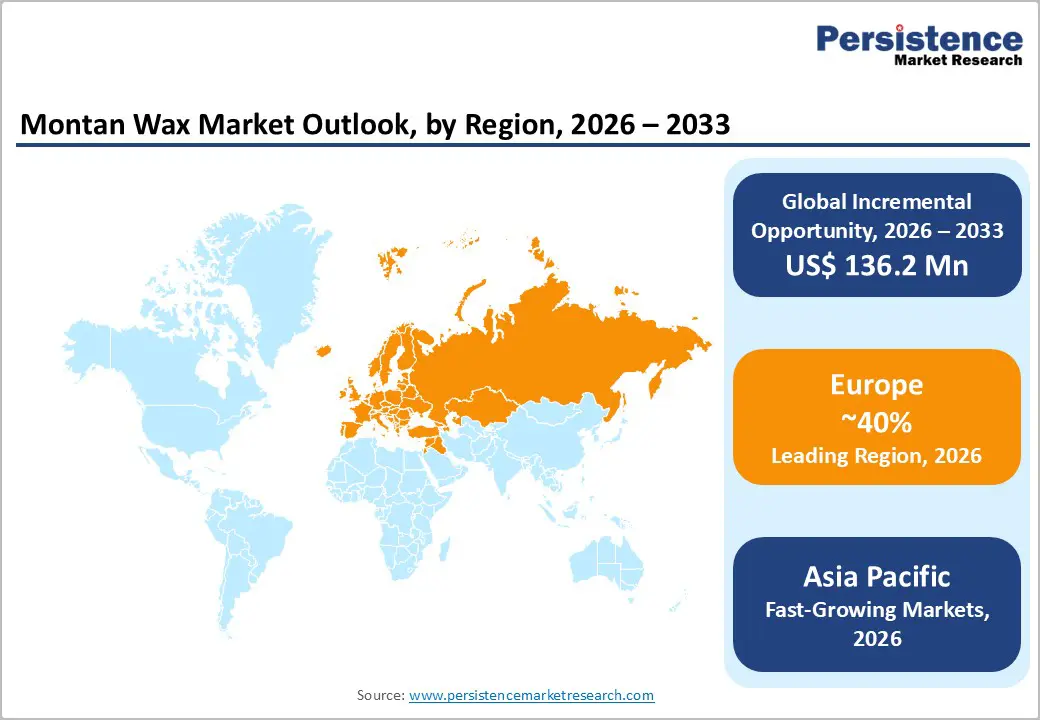

- Leading Region: Europe leads the montan wax market as the global production center holding 40% share, anchored by ROMONTA GmbH’s Amsdorf lignite extraction operation and Clariant AG’s Licowax brand, serving premium cosmetics, printing inks, and plastics processing customers across Europe and worldwide.

- Fastest Growing Region: Asia Pacific is the fastest growing market, led by China’s world-leading plastics processing and electrical cable manufacturing sectors, India’s expanding polymer industry, and Japan’s precision electronics and cosmetics demand for high-specification montan wax grades.

- Dominant Segment: Modified/esterified montan wax leads with approximately 38% revenue share, commanding premium pricing for its superior polymer compatibility, high melting point stability, and dual-function performance in cosmetics and industrial applications globally.

- Fastest Growing End-user Segment: Cosmetics & personal care is the fast-growing segment, driven by the clean beauty trend favoring naturally derived INCI-listed Lignite Wax in lipstick and skin care formulations, and European cosmetics retail exceeding €84 billion annually.

- Key Opportunity: Modified montan wax esters for premium cosmetics leveraging clean beauty natural ingredient positioning, and electrical insulation applications in China’s growing cable manufacturing sector, producing 50%+ of global cable volume, represent the highest-value growth segments through 2033.

Market Dynamics

Drivers - Expanding Plastics & Polymer Processing Applications Requiring High-Temperature Lubricants

The global plastics processing industry is a primary demand driver for montan wax, which serves as a high-performance internal and external lubricant, mold release agent, and anti-blocking additive in PVC, polyolefin, and engineering thermoplastic compounding and extrusion operations. Montan wax esters, produced by esterification of crude montan acid wax with diols or polyols, provide superior compatibility with polar polymer matrices compared to paraffin waxes, commanding premium pricing in demanding polymer processing applications.

Global plastic production has grown consistently over the past decade, with the PlasticsEurope association reporting global plastic production exceeding 400 million tonnes annually. The expanding production of PVC profiles, cables, and rigid packaging in the Asia Pacific and the growth of engineering thermoplastic compounding in automotive lightweighting applications are directly expanding the addressable market for montan wax-based processing aids and lubricants, supporting sustained market growth through the forecast period.

Printing Inks, Toners, and Coatings Industry Adoption

The printing inks and toner industry represents an established and growing application for montan wax, where it functions as a critical slip, scratch-resistance, and matting agent in offset, flexographic, and gravure inks, as well as a key component in laser toner powder formulations for improved fusing and release properties.

The European Printing Ink Association (EuPIA) reports that the European printing ink industry produces approximately 1 million tonnes annually, with functional additives including waxes, representing an essential performance component. The digital printing revolution, particularly the expansion of laser printing and industrial inkjet applications, has created new demand for ultra-fine micronized montan wax powder grades with tightly controlled particle size distributions. Clariant AG and ROMONTA GmbH are the primary global suppliers of printing ink-grade micronized wax products, with both continuously developing new grades for evolving digital and UV-curing ink formulation requirements.

Restraints - Limited and Geographically Concentrated Raw Material Supply

Montan wax is derived exclusively from lignite (brown coal) deposits, with commercially viable extraction concentrated primarily in Germany’s Lusatia region (ROMONTA GmbH) and China’s Yunnan Province. This geographically concentrated supply base creates inherent vulnerability to mining disruptions, energy policy changes, and geopolitical risks.

Germany’s long-term lignite phase-out plans, with coal power generation to end by 2038 per the German Coal Commission, create strategic uncertainty about the long-term availability and cost of European montan wax supply. Supply concentration risk constrains market expansion and introduces pricing volatility that can deter new application development investment.

Competition from Synthetic Waxes and Alternative Processing Aids

Montan wax faces competition from increasingly sophisticated synthetic alternatives including Fischer-Tropsch (FT) waxes, polyethylene waxes, oxidized polyethylene waxes, and amide waxes that can replicate many of its functional properties in specific applications.

Synthetic wax production, from manufacturers including Clariant, Baker Hughes, and Honeywell, offers more consistent quality specifications, scalable supply, and in some cases lower costs compared to naturally derived montan wax. In applications where exact functional equivalence can be achieved, the trend toward synthetic alternatives driven by supply security and regulatory predictability moderates montan wax volume growth.

Opportunities - Modified Montan Wax Esters for Premium Cosmetics and Personal Care

The refined and esterified montan wax segment is experiencing accelerating demand from the cosmetics and personal care industry, where modified montan wax esters serve as high-performance structuring agents, emulsion stabilizers, and film-forming components in lipsticks, mascaras, sun care products, and skin care formulations. The global cosmetics industry has grown consistently, with Cosmetics Europe reporting European cosmetics retail sales exceeding €84 billion annually.

Montan wax esters offer high melting points (82-90°C) that impart excellent heat stability to lipstick formulations and are listed in the INCI (International Nomenclature of Cosmetic Ingredients) as “Lignite Wax” with established safety profiles. The clean beauty trend is driving cosmetic formulators to prefer naturally derived wax ingredients over synthetic alternatives, creating a favorable market environment for premium purified and esterified montan wax grades from suppliers including Clariant’s Licowax E series and ROMONTA’s MONTANAT range.

Electrical Insulation and Electronics Manufacturing Growth in Asia

The global electrical and electronics manufacturing sector, particularly in the Asia Pacific, represents a significant and growing demand opportunity for montan wax in cable insulation, capacitor impregnation, and printed circuit board coating applications. Montan wax provides exceptional electrical insulation properties, moisture resistance, and high thermal stability that make it a preferred ingredient in electrical insulation compounds and cable jacketing formulations.

The International Electrotechnical Commission (IEC) reports that global electrical cable production is growing at over 5% annually driven by infrastructure electrification, renewable energy installation, and data center construction. China’s position as the world’s dominant electrical cable manufacturer, producing over 50% of global cable volume, makes it the largest and fastest-growing single-country end-user of montan wax for electrical insulation applications, representing a compelling market expansion opportunity for producers with established Asian distribution networks.

Category-wise Analysis

By Product Type Insights

Modified/Esterified Montan Wax is the leading product type segment, commanding approximately 38% of total market share. Esterified montan wax, produced by reacting crude or refined montan acid wax with ethylene glycol, butanediol, or other polyols, delivers the highest functional performance characteristics of any montan wax grade, including improved compatibility with polar polymer matrices, superior emulsification properties, and higher melting point stability than unmodified grades.

This premium performance profile commands significant price premiums and drives the segment’s disproportionate revenue share. Key producers including Clariant AG’s Licowax E and OP grades and ROMONTA GmbH’s MONTANAT esters serve demanding cosmetics, plastics processing, and printing ink applications that require the highest-specification montan wax functionality, sustaining premium pricing and market leadership.

By Form Insights

Solid form montan wax is the leading form segment, representing approximately 62% of total market share. Solid montan wax, typically supplied as flakes, granules, or pastilles, is the most versatile commercial form, compatible with direct blending into polymer compounding, ink grinding, and cosmetic manufacturing processes. The solid form offers convenient storage, handling, and dosing characteristics that match the processing equipment configurations of most industrial users.

Solid grades also have the longest shelf life and lowest transportation volume per unit weight of wax functionality, making them the preferred trade form for global distribution. Leading producers supply solid montan wax in standardized 25 kg bags, 200 kg drums, and 1,000 kg intermediate bulk containers (IBCs) that are compatible with standard chemical distribution logistics, supporting the form’s dominant market share across all key application sectors.

By Function Insights

Lubricants is the leading functional segment, accounting for approximately 29% of total market share. The lubricating function of montan wax, encompassing both internal lubrication (reducing melt viscosity and improving flow in polymer processing) and external lubrication (providing mold release and surface slip in extrusion and injection molding), is the single most widely adopted application across the plastics, rubber, and polymer processing industries.

Montan wax’s unique combination of high melting point (78-90°C for refined grades), low melt viscosity, and compatibility with both polar and non-polar polymer matrices makes it functionally superior to paraffin wax as a processing lubricant in demanding thermoplastic and thermoset applications. Industry organizations including PlasticsEurope and Society of Plastics Engineers (SPE) document extensive use of specialty wax lubricants in polymer compounding.

By Application Insights

Rubber & Plastics Processing is the leading application segment, representing approximately 32% of total market share. This segment encompasses the use of montan wax as an internal and external lubricant, anti-blocking agent, and mold release component in the compounding and processing of PVC, polyolefins, ABS, and engineering thermoplastics.

With global plastic production exceeding 400 million tonnes annually per PlasticsEurope data, the scale of industrial polymer processing represents a vast and geographically distributed addressable market for montan wax-based processing aids. PVC compounding for window profiles, pipes, and wire insulation, applications that collectively consume millions of tonnes of PVC globally, are particularly significant montan wax end-use applications due to the material’s thermal stability and lubricity performance at PVC processing temperatures of 160-200°C.

By End-user Insights

Plastics & Polymer is the dominant end-use segment, accounting for approximately 28% of total market share. The plastics and polymer processing sector’s demand for montan wax as a precision lubricant and processing aid across extrusion, injection molding, and calendering operations represents the single largest volume end-use market.

The European Plastics Converters (EuPC) association reports that European plastics converters process approximately 50 million tonnes of plastics annually, with a significant proportion requiring specialty wax lubricants. The Asia Pacific plastics processing industry, particularly in China, India, and ASEAN, is growing rapidly, creating incremental demand for montan wax-based processing additives. The segment’s breadth, spanning packaging, construction, automotive, electrical, and consumer products, provides broad geographic and application diversification that sustains demand resilience.

Regional Insights

North America Montan Wax Market Trends & Analysis

North America represents a mature, premium-driven montan wax market, accounting for approximately 28% of global demand in 2026. Growth is supported by strong demand from cosmetics, printing inks, and plastics processing sectors. Regulatory compliance under FDA frameworks supports high-quality imports, reinforcing reliance on European suppliers and sustaining steady premium pricing dynamics.

- U.S. Montan Wax Market Size

The United States dominates the regional market, contributing nearly 85% of North America’s demand. Strong consumption is driven by the US$ 90+ billion cosmetics industry and advanced printing inks sector. Growth remains moderate, supported by stable industrial demand and high-value personal care applications.

Europe Montan Wax Market Trends, Drivers & Insights

Europe leads the global montan wax market, holding an estimated 40% share, driven by its production dominance and advanced specialty chemicals industry. Sustainability initiatives, including REACH compliance and the EU Green Deal, are accelerating demand for natural wax alternatives, strengthening montan wax positioning in premium and eco-friendly applications.

- Germany Montan Wax Market Size

Germany is the largest market globally, accounting for nearly 50% of Europe’s demand. Its dominance stems from strong domestic production, advanced plastics and coatings industries, and export-oriented supply chains. Growth is steady (~4% CAGR), supported by innovation in specialty wax derivatives.

- U.K. Montan Wax Market Size

The United Kingdom represents approximately 12% of the European market. Demand is driven by cosmetics and printing inks industries, with increasing focus on sustainable raw materials. Moderate growth is expected, supported by clean beauty trends and specialty formulation demand.

- France Montan Wax Market Size

France accounts for nearly 10% of regional demand, led by its globally influential cosmetics and luxury personal care industry. Demand for high-purity wax esters is strong, particularly in premium formulations. Growth is stable, aligned with expansion in organic and natural cosmetic segments.

Asia Pacific Montan Wax Market Drivers & Analysis

Asia Pacific is the fastest-growing region, capturing approximately 27% share. Growth is fueled by rapid industrialization, expanding plastics processing, and rising cosmetics production. Increasing domestic production in China and growing manufacturing ecosystems across India and ASEAN are accelerating regional demand at ~5.6% CAGR.

- China Montan Wax Market Size

China is the largest regional market, contributing nearly 60% of Asia Pacific demand. Strong growth is driven by large-scale PVC processing, cable manufacturing, and expanding cosmetics production, along with domestic montan wax extraction capabilities.

- India Montan Wax Market Size

India accounts for approximately 15% of regional demand. Growth is robust, supported by expanding plastics, packaging, and personal care industries under initiatives like Make in India. Increasing industrialization and consumption of polymer additives are key growth drivers.

- Japan Montan Wax Market Size

Japan represents a mature market with around 12% share. Demand is driven by high-performance applications in electronics, precision coatings, and cosmetics. Growth remains moderate, with emphasis on quality, consistency, and specialty chemical applications.

Competitive Landscape

The global montan wax market is moderately consolidated, dominated by a small number of European producers with captive access to lignite extraction infrastructure and decades of refinement and esterification expertise. ROMONTA GmbH and Clariant AG hold the strongest global market positions through their integrated lignite mining-to-refined wax supply chains, globally recognized product brands (MONTANAT and Licowax), and extensive application development expertise.

Chinese producers, including Yunnan Shangcheng and Yunphos serve primarily domestic and regional Asian markets with standard grades. Key competitive differentiators include purity consistency, particle size control for micronized grades, ester chemistry portfolio breadth, food and cosmetic grade certifications (FDA, REACH, INCI), and technical application support services. Emerging trends include bio-based wax blends incorporating montan wax with plant-derived components for sustainable formulation claims.

Key Developments:

- February 2025: Clariant AG expanded its Licowax portfolio with new ultra-fine micronized montan wax grades targeting digital printing toner and UV-curing ink applications, featuring enhanced particle size distribution control for improved slip and scratch resistance performance.

- September 2024: ROMONTA GmbH announced investment in modernized esterification capacity at its Amsdorf facility, expanding production of MONTANAT modified montan wax esters to meet growing demand from cosmetics and plastics processing customers in Asia Pacific markets.

- April 2024: Paramelt B.V. introduced new montan wax-based hot-melt adhesive formulation components featuring enhanced thermal stability and adhesion performance for packaging and bookbinding applications, targeting the growing e-commerce packaging market.

Montan Wax Market- Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 278.7 Mn |

| Current Market Value (2026) | US$ 2350.6 Mn |

| Projected Market Value (2033) | US$ 486.8 Mn |

| CAGR (2026 - 2033) | 4.8% |

| Leading Region | Europe, 40% share |

| Dominant Product Type | Modified / Esterified Montan Wax, 38% share |

| Top-ranking Form | Solid, 62% |

| Incremental Opportunity | US$ 136.2 Bn |

Companies Covered in Montan Wax Market

- Clariant AG

- ROMONTA GmbH

- Paramelt B.V.

- Völpker Spezialprodukte GmbH

- Poth Hille & Co. Ltd.

- AmeriLubes LLC

- Calwax Corporation

- Carmel Industries

- First Source Worldwide LLC

- Frank B. Ross Co., Inc.

- Mayur Dyes & Chemicals Corporation

- Yunnan Shangcheng Biotechnology Co., Ltd.

- Yunphos

- S. Kato & Co., Ltd.

- TER Hell & Co. GmbH

- Hansen & Rosenthal Group

- Chukyo Yushi Co., Ltd.

Frequently Asked Questions

The global Montan Wax Market is projected to reach US$ 486.8 Million by 2033, growing from US$ 350.6 Million in 2026 at a CAGR of 4.8% during the 2026 - 2033 forecast period. This accelerates from a historical CAGR of 3.9% between 2020 and 2025, driven by expanding plastics processing demand, cosmetics industry adoption, and growing electrical insulation applications in Asia Pacific.

The primary drivers are global plastics production exceeding 400 million tonnes annually per PlasticsEurope requiring high-temperature montan wax lubricants and processing aids, and the printing inks and toners industry, with EuPIA reporting 1 million tonnes of annual European ink production, driving sustained demand for micronized montan wax slip, scratch-resistance, and matting additive grades.

Modified / Esterified Montan Wax leads the By Product Type category with approximately 38% revenue share. Its superior polymer matrix compatibility, high melting point stability, and dual-function performance in cosmetics and industrial polymer processing applications command significant price premiums over unmodified grades, delivered through Clariant’s Licowax® E and ROMONTA’s MONTANAT® product ranges.

Europe leads the global Montan Wax Market as both the dominant production center and a primary consuming region. ROMONTA GmbH in Amsdorf, Germany operates the world’s largest montan wax production facility, while Clariant AG’s Licowax® brand serves global premium cosmetics, printing inks, and plastics processing markets from European manufacturing operations.

The leading opportunities are modified montan wax esters for clean beauty cosmetics leveraging INCI Lignite Wax natural ingredient positioning, with Cosmetics Europe documenting €84B+ European retail sales, and electrical insulation applications serving China’s cable manufacturing sector that produces 50%+ of global cable volume, representing the market’s highest near-term growth segments.

The key market participants include Clariant AG, ROMONTA GmbH, Paramelt B.V., Völpker Spezialprodukte GmbH, Poth Hille & Co. Ltd., AmeriLubes LLC, Calwax Corporation, Carmel Industries, First Source Worldwide LLC, Frank B. Ross Co. Inc., Mayur Dyes & Chemicals Corporation, Yunnan Shangcheng Biotechnology Co. Ltd., Yunphos, S. Kato & Co. Ltd., and TER Hell & Co. GmbH.