- Clothing, Footwear, & Accessories

- Europe Luxury Watches Market

Europe Luxury Watches Market Size, Share, and Growth Forecast 2026 - 2033

Europe Luxury Watches Market by Mechanism (Mechanical, Quartz, Electronics), Price Range (Below US$ 10,000, US$ 10,000-25,000, Above US$ 25,000), Purchase Type (New, Pre-owned), Distribution Channel (Online Store, Single Brand Store, Multi Brand Store), and Country Analysis, 2026 - 2033

Europe Luxury Watches Market Size and Trend Analysis

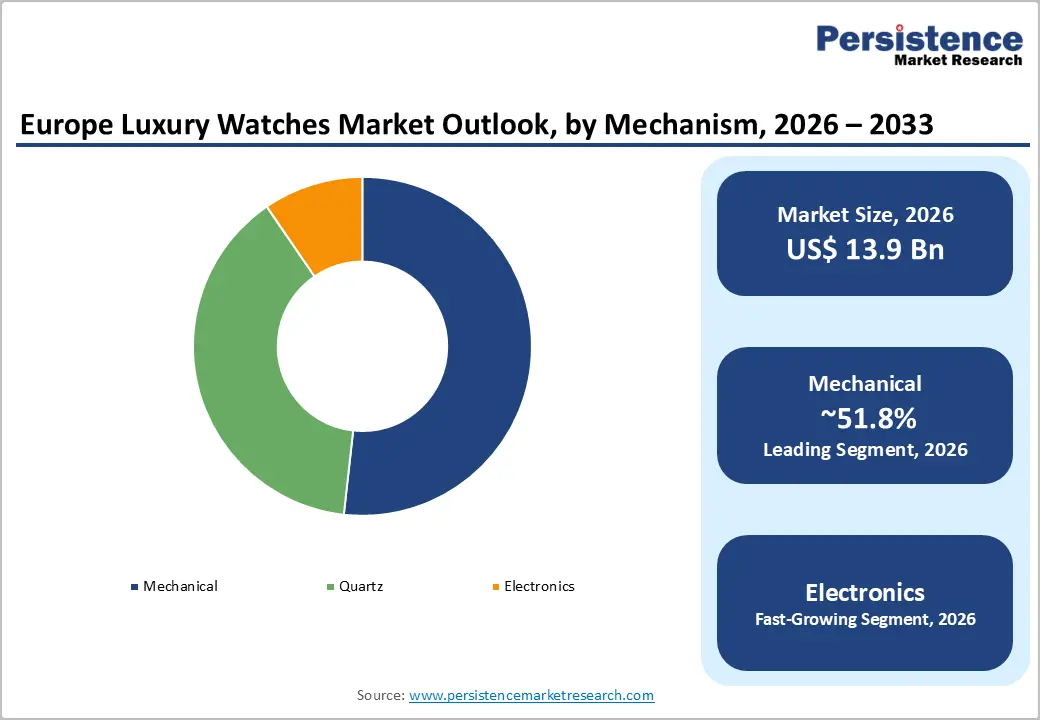

The Europe luxury watches market size is expected to be valued at US$ 13.9 billion in 2026 and projected to reach US$ 17.7 billion by 2033, growing at a CAGR of 3.5% between 2026 and 2033.

The market is gaining momentum on the back of resilient demand for Swiss-made timepieces, sustained appetite from high-net-worth individuals, and a structural shift toward mechanical horology as a wealth-preservation asset. According to the Federation of the Swiss Watch Industry (FH), Swiss watch exports to Europe rose by 5.0% in 2023, reaching CHF 8.4 billion, with the United Kingdom, France, Germany, Italy, and Spain absorbing the bulk of shipments. Coupled with travel-retail recovery and growth of pre-owned watch platforms, these factors are reinforcing long-term demand visibility for European luxury watch retailers.

Key Market Highlights

- Leading Region: Europe accounts for approximately 33% of the global luxury watches market in 2025, supported by Switzerland’s manufacturing leadership and strong retail demand across the U.K., France, Germany, and Italy.

- Leading Mechanism: The mechanical watches segment leads with nearly 52% share in 2026, driven by strong collector preference for high-complication and heritage Swiss timepieces.

- Leading Price Range: The Below US$ 10,000 price category dominates the market with around 52% share in 2026, benefiting from rising demand among aspirational luxury consumers and young professionals entering the premium watch segment.

- Leading Purchase Type: New luxury watches remain the dominant purchase type, accounting for nearly 81.9% share in 2026, supported by demand for authenticity assurance, manufacturer warranties, and limited-edition launches.

- Leading Distribution Channel: Multi-brand stores hold approximately 39% share in 2026, with retailers such as Bucherer, Watches of Switzerland, and Wempe strengthening premium retail accessibility across major European luxury hubs.

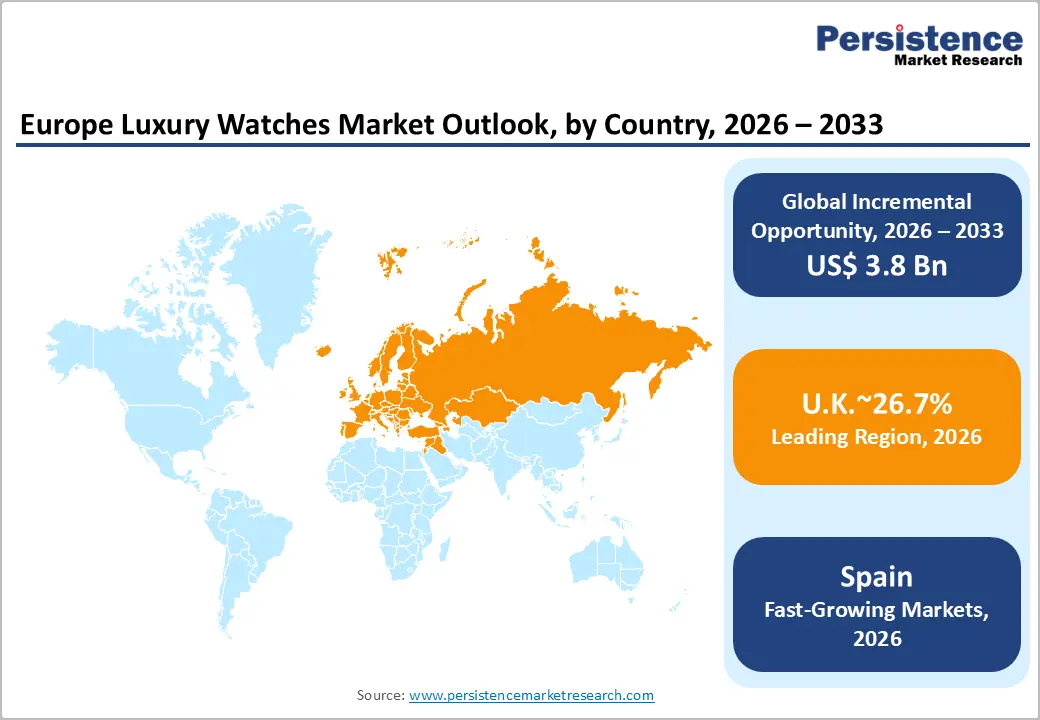

- Leading Country: The U.K. leads the European luxury watches market with a valuation of nearly US$ 3.6 billion in 2025, anchored by London’s strong inbound tourism, HNWI concentration, and flagship luxury retail corridors.

- Fast Growing Country: Spain is projected to be the fastest-growing luxury watches market in Europe in 2025, reaching around US$ 466.9 million, supported by record tourism inflows and the expansion of Swiss luxury watch boutiques in Madrid and Barcelona.

DRO Analysis

Market Growth Drivers

Wealth Concentration and Status-Driven Consumption Anchor Demand

Europe remains home to one of the world’s densest pools of high-net-worth individuals (HNWIs), which underpins consistent absorption of luxury timepieces. Europe accounted for over 5.5 million HNWIs with combined wealth exceeding US$ 18 trillion in 2023.

Switzerland, Germany, France, Italy, and the U.K. dominate this base, where mechanical watches are routinely purchased as heirlooms, gifts, and portfolio assets. With wealth managers increasingly classifying luxury watches alongside fine art and rare wine as alternative stores of value, this status-and-wealth dynamic is firmly entrenching demand for premium horological brands across the continent.

Tourism Recovery and Travel-Retail Channels Reinforce Sales

Europe’s position as the world’s leading inbound tourism region directly supports luxury watch retail. The European Travel Commission (ETC) confirmed that international arrivals in Europe surpassed 742 million in 2024, recovering above pre-pandemic benchmarks.

Hubs such as Geneva, Paris, London, and Milan remain critical sales corridors, with travel retail and tax-refund schemes making luxury timepieces attractive for foreign buyers, particularly from the Middle East, North America, and Asia. According to Global Blue, watches and jewellery represented nearly 31% of tax-free shopping value in Europe in 2024, confirming the channel’s strategic role for premium horology houses.

Market Restraints

Counterfeit Pressure and Grey Market Channels Erode Brand Equity

Counterfeit and parallel-imported watches continue to weigh on the European luxury watches market. The European Union Intellectual Property Office (EUIPO) estimated counterfeit watches and jewellery cost the EU economy approximately EUR 1.9 billion annually in lost sales, with watches alone representing the second-most seized category at EU borders in 2023.

Beyond direct revenue erosion, counterfeits dilute brand exclusivity and complicate pre-owned authentication, prompting maisons such as Audemars Piguet and Patek Philippe to invest heavily in track-and-trace certification programs.

Macroeconomic Pressure and Currency Volatility Squeeze Discretionary Spending

Persistent inflation, elevated interest rates across the eurozone, and a strong Swiss franc are restraining mid-tier luxury watch purchases. According to Eurostat, consumer price inflation across the EU averaged 6.4% in 2023, squeezing aspirational buyers in the below US$ 10,000 bracket. Additionally, the Swiss franc appreciated by nearly 9% against the euro between 2022 and 2024, inflating retail prices and prompting some buyers to defer purchases or migrate toward pre-owned alternatives.

Opportunities - Pre-owned Luxury Watch Segment Unlocks New Revenue Pools

The pre-owned luxury watches segment is emerging as one of the most strategic opportunities for brands and retailers. The Federation of the Swiss Watch Industry (FH) noted that the global pre-owned luxury watches market is projected to expand at nearly twice the pace of the new-watch segment over the coming decade.

In August 2023, Rolex SA acquired Swiss multi-brand retailer Bucherer, operator of more than 100 sales outlets, to formally enter certified pre-owned distribution. Similarly, Audemars Piguet operates its “AP Certified Pre-Owned” program. With younger collectors prioritizing rarity and provenance, certified pre-owned platforms are expected to be a key growth lever across European markets.

Digital Commerce and Single-Brand Boutique Experiences Open Premium Channels

Direct-to-consumer (DTC) digital flagship stores and immersive single-brand boutiques are reshaping luxury watch retail in Europe. The European E-commerce Report 2024 by Ecommerce Europe noted that the European online luxury segment grew by 12% in 2024, with watches and jewellery among the fastest digitizing categories.

In October 2024, Jaeger-LeCoultre expanded its flagship boutique network, while Patek Philippe extended its international warranty from two to five years to support direct-channel trust. These initiatives, combined with virtual try-on tools and augmented reality-based experiences, present long-horizon opportunities for premium watch houses to elevate margins and capture loyalty.

Category-wise Analysis

Mechanism Insights

The mechanical segment dominates Europe luxury watches market with a share of approximately 52% in 2026. Mechanical timepieces remain the cornerstone of European haute horlogerie, anchored by Switzerland’s centuries-old craftsmanship and the cultural prestige attached to in-house calibres.

According to the Federation of the Swiss Watch Industry (FH), mechanical watches accounted for over 80% of Swiss watch export value in 2023, despite representing a smaller share by volume. Brands including Rolex SA, Patek Philippe SA, and Audemars Piguet Holding SA continue to release high-complication mechanical pieces such as the Patek Philippe Cubitus collection unveiled in October 2024, reinforcing mechanical horology as the segment of choice for collectors and investors.

Price Range Insights

Below US$ 10,000 price band is the leading segment, capturing roughly 52% market share in 2026. This bracket benefits from the broadest addressable buyer base, including young professionals and aspirational buyers entering the luxury category through entry-level Swiss timepieces.

According to the Federation of the Swiss Watch Industry (FH), watches priced between CHF 500 and CHF 3,000 in export value drove a substantial share of unit shipments in 2023. Brands such as Longines, Omega SA, and entry-level IWC Schaffhausen models dominate this band, supported by stable retail networks and active marketing partnerships, including Longines’ Mini DolceVita launch in September 2023.

Purchase Type Insights

New purchase segment leads Europe luxury watches market with around 81.9% share in 2026. European consumers continue to favour brand-new timepieces purchased through authorized dealers and brand boutiques, owing to manufacturer warranties, authenticity assurance, and access to limited-edition releases.

According to the Federation of the Swiss Watch Industry (FH), Swiss watchmakers shipped over 16.9 million new units globally in 2023, with Europe absorbing a substantial portion. The strong pipeline of new product launches, such as the Rolex Oyster Perpetual GMT-Master II refresh in September 2024 and Audemars Piguet [RE]Master02 in May 2024 keeps the new-watch segment firmly dominant.

Distribution Channel Insights

Multi-brand stores represent the leading distribution channel in Europe luxury watches market with about 39% share in 2026. European luxury watch buyers continue to value the comparative shopping experience offered by multi-brand authorized dealers, where flagship maisons share floor space and provide concierge-style after-sales servicing.

Networks such as Bucherer, Watches of Switzerland, and Wempe operate flagship locations across Geneva, London, Paris, and Berlin. The Rolex SA acquisition of Bucherer in August 2023, which operates more than 100 global outlets, underscores the strategic relevance of multi-brand retail in distributing premium horology to discerning European clientele.

Regional Insights

Europe Luxury Watches Market Trends and Insights

Europe holds approximately 33% share of the global luxury watches market in 2025, driven by Switzerland’s manufacturing dominance and strong retail demand across the U.K., France, Germany, and Italy. Emerging trends include the rise of certified pre-owned platforms, sustainability-driven sourcing under the Watch & Jewellery Initiative 2030, and the rapid expansion of single-brand flagship boutiques across major European cities.

U.K. Luxury Watches Market Size

The U.K. luxury watches market was valued at approximately US$ 3.6 billion in 2025, driven by London’s position as Europe’s leading luxury retail hub. Strong inbound tourism, robust HNWI demand, and concentration of flagship boutiques along Bond Street and Old Bond Street are anchors. According to the Office for National Statistics (ONS), the U.K. recorded over 38 million inbound visitors in 2023, reinforcing premium watch demand.

France Luxury Watches Market Size

France’s luxury watches market reached around US$ 2.7 billion in 2025, supported by Paris’s status as a global luxury capital and the presence of flagship maisons such as Cartier International SNC. According to Atout France, France welcomed 100 million international tourists in 2023, boosting tax-free luxury watch sales along Avenue Montaigne and Place Vendôme.

Germany Luxury Watches Market Size

Germany’s luxury watches market stood at nearly US$ 2.2 billion in 2025, driven by a deep collector base, strong industrial wealth, and demand for German watchmaking houses such as A. Lange & Söhne and Glashütte Original. According to Destatis, luxury watch and jewellery retail in Germany rose by nearly 4% in 2023, supported by Munich, Frankfurt, and Berlin retail clusters.

Switzerland Luxury Watches Market Size

Switzerland’s luxury watches market reached approximately US$ 1,906.0 million in 2025, anchored by domestic consumption, watch tourism, and proximity to manufacturing hubs in Geneva, La Chaux-de-Fonds, and the Vallée de Joux. The Federation of the Swiss Watch Industry (FH) confirmed that Swiss watch exports surpassed CHF 26.7 billion in 2023, reinforcing the country’s pivotal role.

Spain Luxury Watches Market Size

Spain represents the fastest-growing luxury watches market in Europe, valued at around US$ 466.9 million in 2025. Demand is supported by record tourism inflows, with Turespaña reporting over 85 million international tourists in 2023. Madrid’s Salamanca district and Barcelona’s Passeig de Gràcia are emerging as key luxury watch corridors, supported by expanding retail footprints of Swiss maisons.

Competitive Landscape

Europe luxury watches market is moderately consolidated, with the top tier dominated by Rolex SA, Patek Philippe SA, Audemars Piguet Holding SA, and large groups such as Compagnie Financière Richemont SA and Swatch Group AG. Strategic priorities include vertical integration into retail, expansion of certified pre-owned programs, and capacity additions such as Rolex’s new manufacturing site in Bulle, Switzerland scheduled to open by 2029.

Differentiation rests on in-house calibres, limited-edition releases, and immersive boutique experiences, while emerging models include direct-to-consumer e-commerce and brand-led pre-owned trade-ins.

Key Developments:

- In Sept 2024, Rolex introduced two new Oystersteel versions of the Oyster Perpetual GMT-Master II, featuring a grey and black ceramic Cerachrom bezel with a platinum-coated 24-hour graduation. One model comes with an Oyster bracelet, while the other features a Jubilee bracelet. The watches are powered by calibre 3285, offering dual time zone functionality and Superlative Chronometer certification.

- In May, 2024, Audemars Piguet launched the limited-edition [RE]Master02 Selfwinding, a tribute to the asymmetrical Model 5159BA from 1960, as part of its [RE]Master collection. Limited to 250 pieces and priced at $47,200, the timepiece reflects the avant-garde spirit of the 1960s and marks the revival of the collection after four years.

- In April, 2024, Cartier unveiled a range of innovative timepieces at Watches and Wonders 2024, including the reimagined Tortue Monopoussoir Chronograph, the optical illusion-inspired Reflection de Cartier, the Santos-Dumont Rewind with counter-clockwise movement, and the Santos de Cartier Dual Time for dual-time reading.

Europe Luxury Watches Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 11.5 billion |

| Current Market Value (2026) | US$ 13.9 billion |

| Projected Market Value (2033) | US$ 17.7 billion |

| CAGR (2026 - 2033) | 3.5% |

| Leading Region | United Kingdom, 27% share |

| Dominant Category-1 (Mechanism) | Mechanical, 52% share in 2025 |

| Top-ranking Category-2 (Price Range) | Below US$ 10,000, 52% share in 2025 |

| Incremental Opportunity (2026 - 2033) | US$ 3.6 billion |

Companies Covered in Europe Luxury Watches Market

- Rolex SA

- Cartier International SNC

- Omega SA

- Audemars Piguet Holding SA

- Patek Philippe SA

- Richard Mille SA

- Compagnie des Montres Longines Francillon SA

- Vacheron Constantin SA

- Breitling SA

- IWC Schaffhausen International Watch Co. AG

Frequently Asked Questions

The Europe luxury watches market is expected to be valued at US$ 13.9 billion in 2026, and is projected to reach US$ 17.7 billion by 2033.

The market is primarily driven by sustained wealth concentration among European HNWIs and strong tourism-led travel-retail sales, with the European Travel Commission reporting over 742 million inbound arrivals in 2024.

The United Kingdom leads the Europe luxury watches market in 2025 with a market value of approximately US$ 3.6 billion, driven by London’s status as a global luxury retail hub.

Certified pre-owned watch programs and direct-to-consumer digital flagship boutiques represent the largest opportunity, supported by initiatives such as Rolex SA’s acquisition of Bucherer in 2023.

Major players include Rolex SA, Patek Philippe SA, Audemars Piguet Holding SA, Cartier International SNC, Omega SA, Richard Mille SA, Vacheron Constantin SA, Breitling SA, and IWC Schaffhausen.