- Clothing, Footwear, & Accessories

- Textile Market

Textile Market Size, Share, and Growth Forecast 2026 - 2033

Textile Market by Product Type (Technical, Home, Apparel, Industrial Textiles), Textile Form (Synthetic Fibers, Natural Fibers), Fabric Type (Woven, Non-woven), End-user (Residential, Commercial), and Regional Analysis, 2026 - 2033

Textile Market Size and Trends Analysis

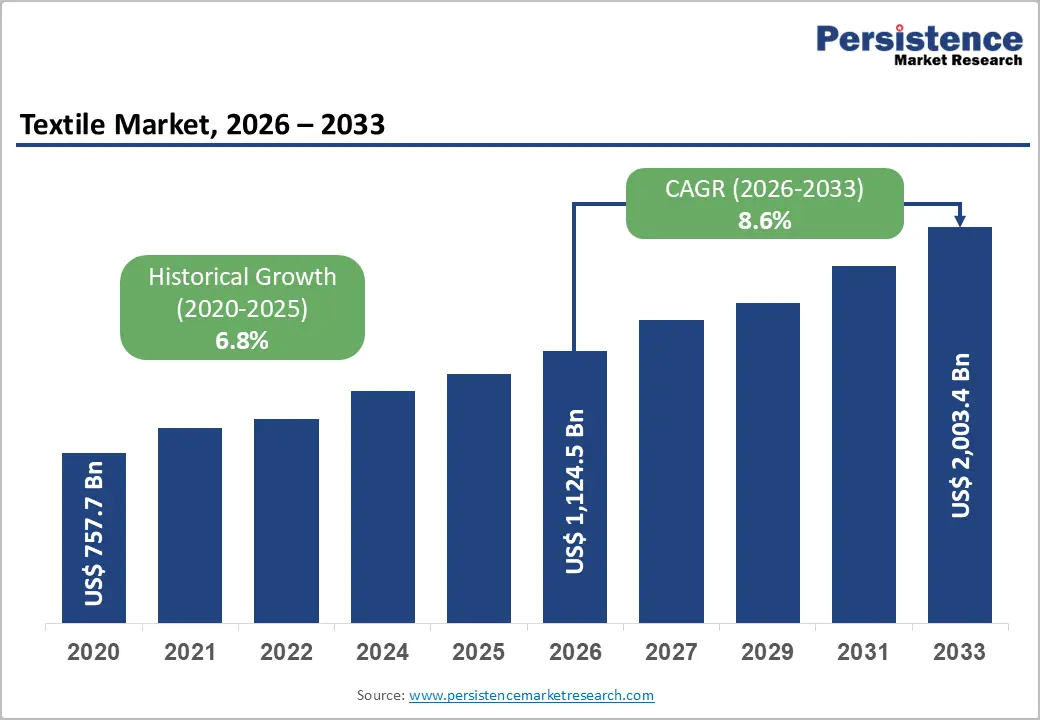

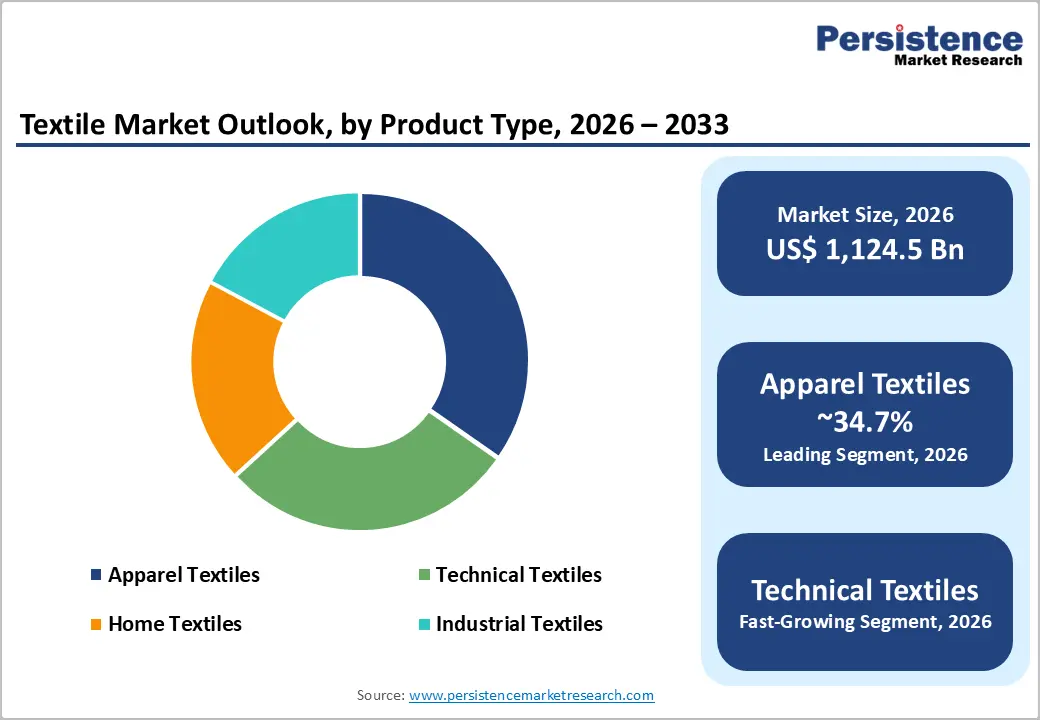

The global textile market size is likely to be valued at US$1,124.5 billion in 2026 and is predicted to reach US$2,003.4 billion by 2033, surging at a CAGR of 8.6% between 2026 and 2033, driven by rising demand for fast fashion and short apparel replacement cycles across urban populations.

The expansion of technical textiles in sectors such as healthcare, automotive, and construction is further boosting market growth.

Key Industry Highlights:

- Leading Product Type: Apparel textiles, approximately 34.7% share in 2026, backed by frequent fashion changes and the rising influence of fast fashion platforms.

- Dominant Textile Form: Synthetic fibers, with a nearly 69.3% share in 2026, spurred by their low production cost and high durability.

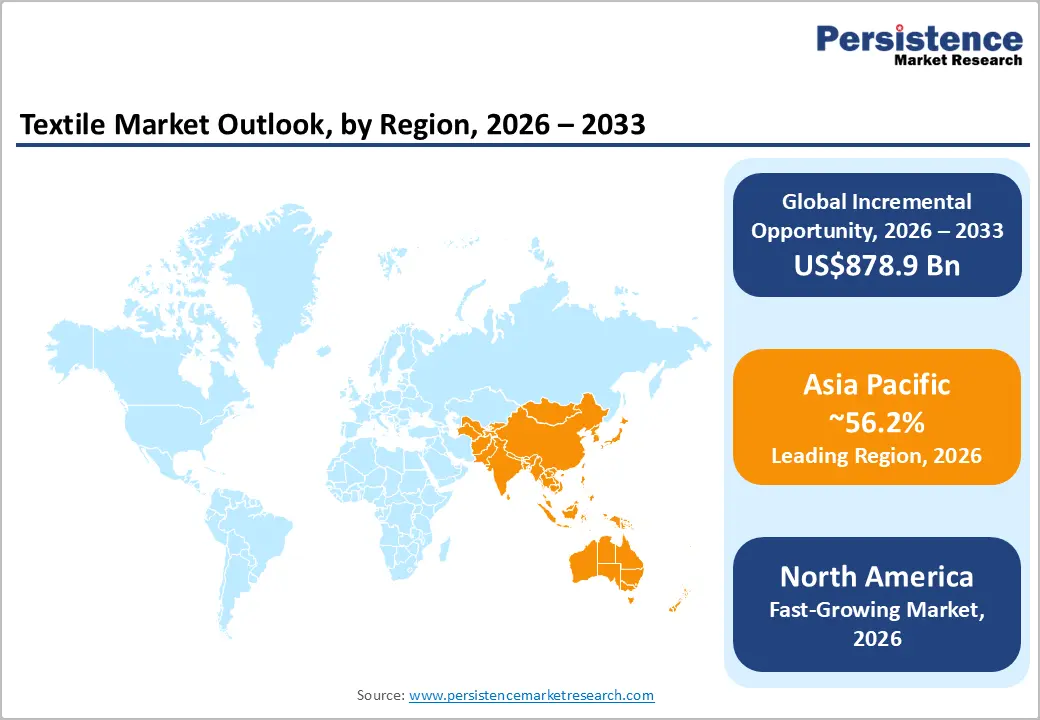

- Leading Region: Asia Pacific, with about a 56.2% share in 2026, boosted by its large-scale manufacturing base and low-cost labor.

- Fast-growing Region: North America, owing to rising demand for sustainable textiles and nearshoring strategies.

- Recycling Initiative: In June 2026, Abdulla bin Touq Al Marri, Minister of Economy and Tourism, UAE, declared that the national Naseej initiative, launched under the directives of the UAE leadership, will contribute to recycling more than 220,000 tons of discarded textiles annually in the UAE. It would help support the country’s efforts to boost industrial circularity, especially in the textile sector.

DRO Analysis

Driver - Boom of E-commerce and Fast Fashion Worldwide

The rise of digital shopping platforms has fundamentally changed how often people buy clothes. Brands no longer follow two seasonal collections a year. Platforms such as Shein now drop thousands of new styles weekly, keeping shoppers in a constant buying loop. TikTok, Instagram, and YouTube played a key role in normalizing viral Shein haul videos, where influencers bulk-purchase items to showcase online.

This behavior directly feeds garment volumes. In 2024, Shein's global apparel market share rose to 1.53%, propelled by ultra-low prices and rapid trend response, growth that came largely at the expense of rivals such as ASOS and boohoo.com, whose sales dropped sharply. The EU has begun responding. In May 2025, the European Parliament ratified a new directive compelling textile manufacturers to finance the collection and recycling of post-consumer garments. It is a sign that regulators see overconsumption as a structural problem associated with fast e-commerce.

Rising Demand for Performance-Oriented Clothing

Specialized fabrics built for protection and not just aesthetics are changing a significant slice of textile demand. The defense sector alone is a key procurement driver. In October 2024, the U.S. Department of Defense awarded a US$32 million contract to PRAK Industries LLC for the production of combat flame-resistant Type II shirts. On the healthcare side, in February 2024, Herculite Products Inc. launched a new e-commerce platform featuring its Sure-Chek antimicrobial healthcare fabric range.

It shows rising institutional interest in hygiene-critical textiles. Material development is also surging. In March 2025, DuPont launched Nomex Nano Flex, a lightweight and breathable flame-resistant fabric delivering 25% higher thermal protection performance, designed specifically for firefighters and industrial workers. As both sectors tighten safety standards, demand for high-performance textiles is increasingly non-discretionary.

Restraint - Industrial Wastewater and Microplastic Contamination

Textile production is one of the most environmentally disruptive manufacturing sectors, and its water footprint is a serious operational and regulatory risk. The European Environment Agency (EEA) has estimated that between 200,000 and 500,000 tons of textile-derived microplastics enter the world's marine environment each year, with around 8% of microplastics released into the oceans across Europe traced back to synthetic textiles. Dyeing and finishing processes are key culprits. They produce chemically loaded effluents that are difficult and costly to treat.

Regulators are now stepping in directly. In April 2023, the U.S. Environmental Protection Agency (EPA) issued its Draft National Strategy to Prevent Plastic Pollution, specifically identifying textile microfibers as a priority concern. It also called for technologies to reduce microplastics discharged from washing machines, along with improved wastewater treatment practices. For manufacturers, compliance with strict environmental standards means high treatment costs. In regions with weak oversight, unchecked pollution creates reputational and legal exposure that increasingly affects sourcing decisions by global brands.

Opportunity - Emergence of Closed-Loop Recycling

For years, recycling blended fabrics, particularly cotton-polyester mixes, was commercially impractical. That is changing steadily. Circ has patented a hydrothermal process that separates and recovers both polyester and cotton from blended fabrics, which reportedly make up 77% of the global market for textiles. Others are moving from pilot to production. In 2024, NBG joined Pesco-Up, an EU-funded project combining multiple technologies to separate mixed textile waste and convert both cotton and polyester fractions into recycled yarn.

Eastman Chemical's molecular recycling plant in Kingsport, Tennessee, also reached on-spec production in March 2024, with capacity to process 110,000 metric tons of plastic waste annually, including polyester from textiles. On the cellulosic side, Renewcell, reborn as Circulose after bankruptcy in 2024, announced plans to restart commercial-level production of cellulosic fiber at its Sundsvall, Sweden, plant. These developments showcase that closed-loop textile recycling is crossing from concept to commercial reality.

Bio-Based Alternatives Move from Niche to Mainstream

Next-generation materials grown from biological sources are gaining traction beyond lab trials. Mycelium (mushroom-derived) leather is the most visible example. Current second-generation sheets from MycoWorks and Bolt Threads now achieve 40,000 Martindale rubs, equivalent to mid-grade cowhide, while remaining plastic-free. Brand adoption is broadening. Bolt Threads currently supplies mycelium materials to Adidas, Lululemon, and Stella McCartney, while Hermès has piloted it in luxury handbags through its Sylvania line.

Regenerated cellulose fibers such as TENCEL Lyocell are also expanding. According to Textile Exchange, polyester currently accounts for 54% of global fiber production and is projected to reach 67% by 2030, yet only 1% is recycled into new textiles. It is pushing brands toward bio-based inputs as a more sustainable baseline. The commercial challenge remains cost. Mycelium leather currently costs around US$25 per square foot versus US$6 for cowhide, though industry roadmaps target cost parity by 2028 through large fermentation facilities.

Category-wise Analysis

Product Type Insights

Apparel textiles are predicted to lead with a share of approximately 34.7% in 2026, as clothing is a daily necessity across all income groups. Demand is not only stable but also repetitive. Consumers now buy more frequently due to changing fashion cycles and social media influence. For example, the European Environment Agency reported that EU consumers bought about 40% more clothing per person in 2022 compared to 1996, showing how consumption has intensified over time. Another key driver is the rise of fast fashion and e-commerce. Brands such as Inditex and Shein release thousands of new designs each year, which makes apparel the most dynamic textile segment.

Technical textiles are estimated to be the fastest-growing segment in the forecast period, as they serve functional uses beyond clothing. These include medical, automotive, defense, and construction applications. Governments are actively promoting this segment. For instance, the Ministry of Textiles, India, launched the National Technical Textiles Mission to boost domestic production and innovation. Healthcare demand is a prominent driver. During and after COVID-19, the use of PPE kits, surgical masks, and medical fabrics increased sharply. According to the World Health Organization (WHO), global PPE demand surged by over 100 times during peak pandemic periods, and several countries continue to maintain stockpiles.

Textile Form Insights

Synthetic fibers are anticipated to dominate with a share of nearly 69.3% in 2026, as they are cost-effective and easy to mass-produce. Polyester, in particular, is widely used due to its durability and low price. Data from Textile Exchange shows that polyester accounts for more than 50% of global fiber production, making it the leading fiber type. Another driver is performance. Synthetic fibers are wrinkle-resistant, quick-drying, and superior. These properties are important for sportswear and outdoor clothing. Brands such as Nike rely heavily on polyester-based fabrics for performance apparel.

Natural fibers are expected to remain in the second position in 2026, owing to their comfort and eco-friendly image. Cotton, wool, and silk are breathable and skin-friendly, which makes them suitable for daily wear. According to the Food and Agriculture Organization, cotton remains one of the most widely cultivated crops globally, supporting millions of farmers. Sustainability concerns are also fostering demand. Consumers are shifting toward biodegradable and renewable materials. The European Commission has introduced policies under the Circular Economy Action Plan that encourage the use of sustainable and recyclable textiles, benefiting natural fibers.

Regional Insights

Asia Pacific Textile Market Trends

Asia Pacific is anticipated to lead in 2026 with a share of nearly 56.2%, as it blends expansion, cost advantage, and deep supply chain integration. China, India, and Bangladesh operate across the full value chain, from fiber production to finished garments. This reduces dependency on imports and improves turnaround time. Bangladesh, for instance, exported over US$47 billion in apparel in 2023, according to its Export Promotion Bureau, making it one of the largest global suppliers. Another key factor is policy support. India’s PLI scheme and PM MITRA mega textile parks aim to create integrated manufacturing clusters.

China Textile Market Trends

In 2026, China will likely lead in Asia Pacific with a share of around 43.6%, as it is slowly moving toward high-value and technology-driven textiles. Under its industrial policies, the country is investing heavily in automation, smart factories, and advanced materials. This shift allows local manufacturers to mass-produce technical textiles, performance fabrics, and specialty fibers. Also, domestic demand is rising in China due to a large middle class and surging sportswear and athleisure markets. This dual advantage of exports and local consumption is boosting steady growth.

India Textile Market Trends

In 2026, India is projected to account for a share of approximately 31.2%, owing to its well-established raw material base and diversified industry structure. The country is one of the largest producers of cotton and also has a key presence in man-made fibers. This reduces reliance on imports and ensures supply stability. The Ministry of Textiles India continues to support the sector through schemes focused on infrastructure, exports, and technical textiles. Another driver is domestic consumption. India’s rising middle class and ongoing urbanization are increasing demand for ready-made garments and home textiles.

North America Textile Market Trends

North America is predicted to be the fastest-growing market in 2026 with a share of approximately 22.3%, as the focus has shifted from low-cost production to high-value textiles. Companies are investing in advanced materials used in healthcare, defense, and industrial applications. The U.S. International Trade Administration highlights rising demand for technical textiles such as medical fabrics, protective gear, and smart textiles. Another prominent factor is supply chain restructuring. After disruptions during the pandemic, brands are adopting nearshoring strategies to reduce dependence on Asia Pacific.

U.S. Textile Market Trends

A share of nearly 38.8% is expected to be held by the U.S. in 2026, as the country is expanding in specialized and innovation-driven segments rather than mass apparel production. Companies are focusing on technical textiles used in defense, healthcare, and sports. The U.S. Department of Defense continues to fund research in advanced fabrics for soldier protection and performance enhancement. Investment in manufacturing is another key factor. According to the National Council of Textile Organizations, the U.S. textile sector has invested over US$20 billion in new plants and technologies since 2013.

Europe Textile Market Trends

Europe will likely witness steady growth in the forecast period, with a share of nearly 15.1% in 2026, backed by its focus on sustainability and premium products. The European Commission is implementing strict regulations under the Circular Economy Action Plan. These include requirements for durability, recyclability, and reduced environmental impact. This is pushing companies to innovate in eco-friendly textiles. The region is also known for high-quality fashion and technical textiles. Italy and France lead in luxury apparel, while Germany focuses on industrial textiles.

Germany Textile Market Trends

Germany is projected to register a substantial share of approximately 33.1% in 2026, backed by its well-established industrial base. The country is a leader in technical textiles used in automotive, construction, and filtration industries. Local companies focus on high-performance materials rather than mass-market apparel. This specialization helps maintain consistent demand. The Federal Ministry for Economic Affairs and Climate Action supports innovation through funding programs linked to Industry 4.0.

U.K. Textile Market Trends

A share of around 20.7% is predicted to be held by the U.K. in 2026, as the country is evolving toward a high-value and innovation-led model. Traditional apparel manufacturing remains limited, but there is steady growth in technical textiles and sustainable materials. Domestic production is becoming competitive due to automation and reduced labor dependency. There is also a shift toward circular economy practices. Companies are investing in fiber recycling and closed-loop systems to reduce waste.

Competitive Landscape

The global textile market is highly fragmented with the presence of thousands of manufacturers, fabric processors, garment producers, and textile brands. Large players such as Toray Industries, Shenzhou International, Inditex, Lenzing AG, and Indorama Ventures are strengthening their positions through integrated operations that span raw materials, yarns, fabrics, and finished products. This allows them to reduce costs, shorten lead times, and respond more quickly to changing demand.

A notable competitive trend is the rising preference of global fashion brands for large and compliant suppliers with multi-country manufacturing footprints. Rising geopolitical risks, trade tariffs, and supply chain disruptions have encouraged buyers to diversify sourcing away from single-country dependence. Hence, manufacturers with facilities across several countries are gaining contracts at the expense of small-scale regional players.

Key Industry Developments:

- In June 2026, VELOR announced the launch of its first fully circular cycling jersey made entirely from recycled textile waste. RELOV, the new product range, is a result of five years of research, testing, and industrial partnerships across Europe.

- In May 2026, the North Eastern Handicrafts and Handlooms Development Corporation (NEHHDC), under the Ministry of Development of North Eastern Region (MDoNER), officially launched Padma Doree. It is a pioneering cross-cultural textile initiative. This unique partnership would bring together the Eri (Ahimsa) silk traditions of Northeast India with the celebrated Chanderi weaving heritage of Madhya Pradesh.

- In March 2026, Cintas announced an agreement to acquire competitor UniFirst in a transaction valued at approximately US$5.5 billion, bringing together two of North America's largest workplace apparel and uniform services providers. The deal is expected to generate approximately US$375 million in operational cost savings in four years, covering materials, production, and other expenses.

Companies Covered in Textile Market

- Hengli Textile

- Shenzhou International Group Holdings Ltd.

- Toray Industries, Inc.

- Chargeurs SA

- Far Eastern New Century Corp.

- Albany International Corp.

- Coats Group plc

- Zhe Jiang Taihua New Material Co., Ltd.

- Alok Industries Ltd.

- The Japan Wool Textile Co., Ltd.

Frequently Asked Questions

The global textile market is projected to be valued at US$1,124.5 billion in 2026.

The textile market is expected to reach US$2,003.4 billion by 2033.

Key market trends include the rising adoption of recycled fibers and increasing investments in technical textiles.

Apparel textiles are expected to be the leading product type with a share of nearly 34.7% in 2026, as the rising urban population is demanding diverse and affordable garments.

The textile market is expected to grow at a CAGR of 8.6% from 2026 to 2033.

Hengli Textile, Shenzhou International Group Holdings Ltd., and Toray Industries, Inc. are a few key market players.