- Aerospace & Defense

- Connected Aircraft Market

Connected Aircraft Market Size, Share, and Growth Forecast 2026 - 2033

Connected Aircraft Market by Application (Commercial: Narrow Body, Wide Body, Business Jet, General Aviation Aircraft; Military: Fighter Aircraft, Military Transport Aircraft, Military Helicopter), Connectivity (In-Flight Connectivity, Air-to-Air Connectivity, Air-to-Ground Connectivity), Frequency (Ka-Band, Ku-Band, L-Band), Product Type (System, Solutions), and Regional Analysis for 2026 - 2033

Connected Aircraft Market Size and Trend Analysis

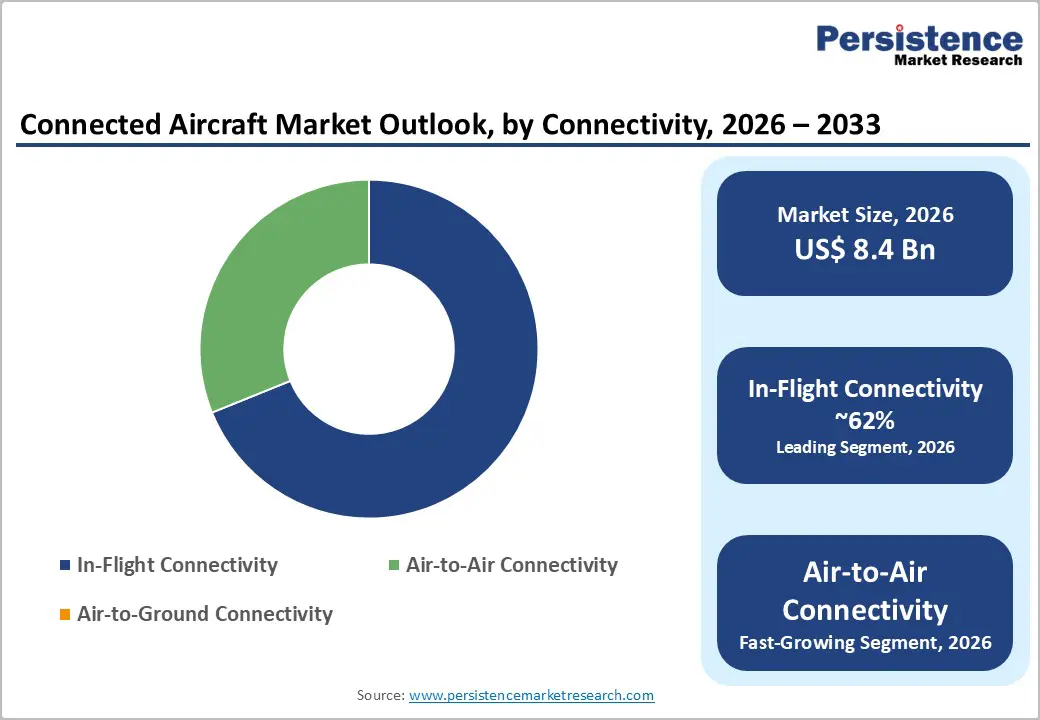

The global connected aircraft market is valued at US$ 8.4 Bn in 2026 and is projected to reach US$ 21.7 Bn by 2033, growing at a CAGR of 14.5% between 2026 and 2033.

This high-growth trajectory is driven by surging passenger expectations for in-flight internet services, rapid expansion of next-generation Low Earth Orbit (LEO) and High-Throughput Satellite (HTS) networks, and the aviation industry's accelerating adoption of data-driven operations, including predictive maintenance, fuel optimization, and real-time fleet management.

The proliferation of connected services across both commercial and military aircraft platforms, combined with strategic consolidations such as Viasat's acquisition of Inmarsat in May 2023, is further concentrating technology leadership and expanding addressable markets across the global connected aviation ecosystem.

Key Market Highlights

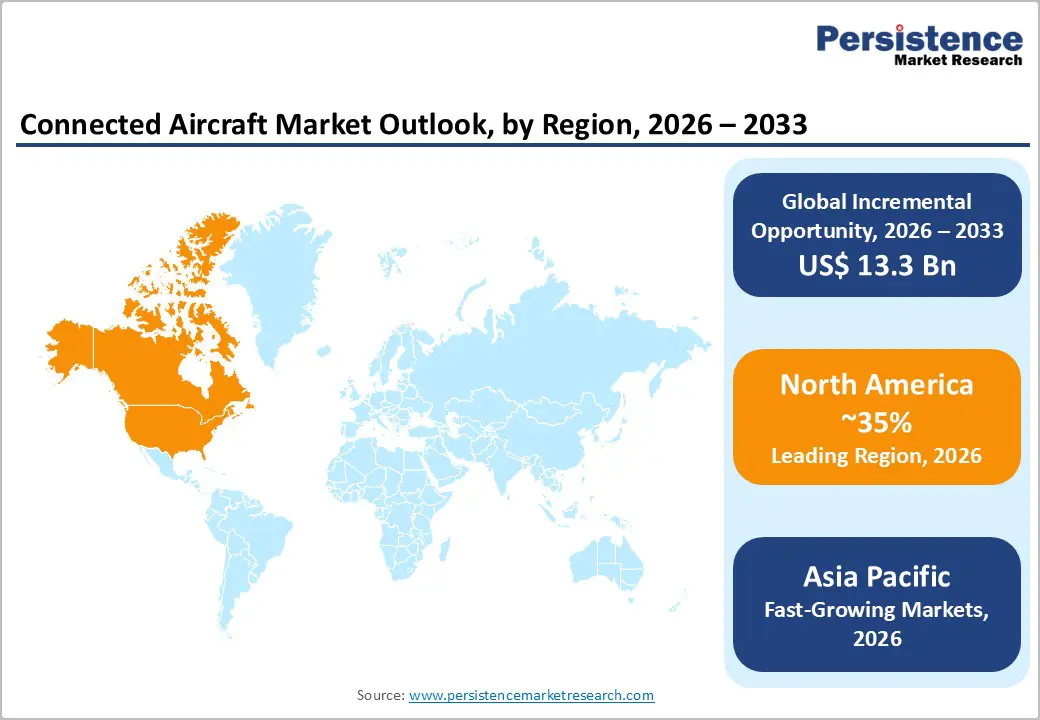

- Leading Region - North America leads the global connected aircraft market with over 80% of regional aircraft equipped with IFC systems, anchored by Viasat, GOGO, Honeywell, and the world's six largest connected commercial fleets operating from U.S. hubs.

- Fastest-Growing Region - Asia Pacific is the fastest-growing region, driven by surging air travel in India, China, and ASEAN nations, rapidly expanding airline fleets, and government infrastructure investment, accelerating demand for next-generation connected aircraft solutions.

- Leading Connectivity Segment - In-flight connectivity, with approximately 62% of total connectivity deployment share, driven by universal airline investment in passenger Wi-Fi as a core service standard and competitive differentiator globally.

- Fastest Growing Frequency Segment - Ka-Band is the fastest growing frequency segment, outpacing established Ku-band systems due to its superior bandwidth capacity and lower latency, enabling high-speed passenger streaming and LEO satellite integration on next-generation IFC platforms.

- Key Market Opportunity - SpaceX Starlink covered approximately 2,500 aircraft by September 2025, with forecasts projecting it could capture 40% of global IFC share by 2034, creating transformative retrofit and integration opportunities for antenna and terminal manufacturers.

| Key Insights | Details |

|---|---|

| Connected Aircraft Market Size (2026E) | US$ 8.4 Bn |

| Market Value Forecast (2033F) | US$ 21.7 Bn |

| Projected Growth CAGR (2026 - 2033) | 14.5% |

| Historical Market Growth (2020 - 2025) | 12.4% CAGR |

DRO Analysis

Drivers - Surging Passenger Demand for High-Speed In-Flight Connectivity and Digital Services

Rising global air travel volumes and passenger expectations for seamless in-flight digital experiences are the most powerful demand drivers in the Connected Aircraft market. In November 2024, Eurostat reported that EU air travel surged in 2023 to 973 million passengers, marking a 19.3% increase from 2022. This recovery has accelerated airline investment in connectivity upgrades, with carriers retrofitting 40+ aircraft per month across regional and mainline fleets.

Starlink, SpaceX's LEO broadband platform, had secured contracts covering approximately 2,500 aircraft by September 2025, with installations on over 100 aircraft and growing. Airlines, including Air France, United Airlines, Hawaiian Airlines, and Qatar Airways, have committed to full fleet rollouts. The in-flight connectivity segment accounted for approximately 62.40% of total connectivity deployments in 2024, reflecting the centrality of passenger Wi-Fi to airline competitive strategy and brand differentiation.

Military Modernization and Défense Connectivity Investments Expanding Addressable Market

Military aviation's transformation toward networked, data-centric operations is creating a significant and growing demand base for advanced connected aircraft systems. Défense agencies worldwide are investing in real-time ISR (Intelligence, Surveillance, and Reconnaissance) data links, encrypted communications, and mission-critical connectivity for fighter aircraft, military transports, and unmanned aerial systems (UAS).

Honeywell International Inc. is developing its JetWave X satcom system, the first capable of connecting to Ka-band satellites in MEO, HEO, and GEO orbits simultaneously, targeting military government operators and large UAS. The system was selected by L3Harris to upgrade the U.S. Army's Airborne Reconnaissance and Electronic Warfare System (ARES), enabling higher data transmission rates and multi-network resilience.

Restraints - High Capital Investment Requirements for Satellite Connectivity Retrofits

The high cost of installing and upgrading in-flight connectivity systems remains a meaningful barrier to accelerating adoption, particularly for smaller and regional carriers. Retrofitting aircraft with next-generation Ka-band or LEO terminals involves substantial hardware costs, installation downtime, and FAA/EASA certification requirements.

Viasat offered incentives of up to US$ 140,000 per aircraft in October 2025 to encourage business aviation customers to transition from legacy Ku-band systems to its next-generation JetXP platform, underscoring the financial friction involved in system migration. For cost-sensitive operators, these upfront investments create extended payback periods and delay fleet-wide connectivity deployment timelines.

Cybersecurity Risks and Spectrum Regulatory Complexity

As connected aircraft systems grow more sophisticated and internet-facing, they become increasingly exposed to cybersecurity threats targeting avionics, passenger data, and operational systems. Regulatory bodies including the U.S. Federal Aviation Administration (FAA) and European Union Aviation Safety Agency (EASA) are developing more stringent cybersecurity frameworks for airborne networks, which create compliance overhead and lengthen product certification timelines.

Additionally, spectrum access and coordination across international boundaries add complexity to global service deployment, particularly for operators serving Asia-Pacific regions where frequency licensing requirements vary significantly across jurisdictions.

Opportunities - LEO Satellite Constellation Deployment Unlocking New Latency and Throughput Standards

The commercial rollout of Low Earth Orbit (LEO) satellite constellations represents the single most transformative opportunity in the Connected Aircraft market over the forecast period. LEO networks dramatically reduce signal latency compared to traditional GEO-based Ka-band and Ku-band systems, making real-time applications such as video conferencing, cloud computing, and live streaming genuinely viable during flight.

SpaceX Starlink already has contracts covering approximately 2,500 commercial aircraft as of September 2025, with market forecasts suggesting it could hold nearly 40% of global in-flight connectivity share by 2034 if adoption trends continue. Honeywell's JetWave X is designed to integrate with LEO networks through Electronically Scanned Antennas (ESAs), while Viasat has entered into agreements with the European Space Agency (ESA) and Mobile Satellite Services Association (MSSA) to develop an open-architecture LEO constellation.

Predictive Maintenance and Flight Operations Digitalization as a High-Value Solutions Growth Frontier

Beyond passenger connectivity, the digitalization of aircraft health monitoring, predictive maintenance, and flight operations represents a high-value, recurring revenue opportunity for connected aircraft solution providers. Airlines leveraging connected systems to optimize fuel burn, schedule maintenance proactively, and enable real-time crew management can achieve measurable reductions in operational costs.

Garmin's July 2023 launch of the Plane Sync system, enabling wireless communication and remote system monitoring via 4G LTE or Wi-Fi, exemplifies the operational connectivity frontier. Connected aircraft solutions that combine hardware platforms with advanced analytics and AI-driven predictive maintenance software are emerging as a high-margin business model, converting one-time hardware revenue into recurring service subscriptions. As IATA projects the global airline fleet size to approach 48,000 aircraft by 2043, the addressable market for operational connectivity solutions will expand substantially.

Category-wise Analysis

Application Insights

The commercial aircraft segment is the dominant application category, accounting for approximately 70% of total market revenue. Within the commercial segment, wide-body aircraft represent the leading platform for in-flight connectivity deployments due to their use on long-haul international routes, which generate the highest per-aircraft revenue potential for IFC providers.

Emirates announced plans in May 2024 to retrofit an additional 43 A380s and 28 Boeing 777 wide-body aircraft as part of an ongoing overhaul program covering 191 aircraft in total. The commercial IFC aircraft fleet of Viasat grew approximately 13% year-over-year during its most recent reported period, with business jets growing at 18% YoY. The military segment is the fastest growing application sub-category, driven by defence modernization budgets and the expanding use of connected platforms in ISR, transport, and rotary-wing operations.

Connectivity Insights

The In-Flight Connectivity (IFC) segment leads the connectivity category, commanding approximately 62% of total market share in 2024. This dominance reflects airlines' prioritization of passenger Wi-Fi as a core service offering and competitive differentiator. IFC systems encompass satellite communication terminals, onboard routers, wireless access points, and content delivery platforms that collectively enable broadband access for passengers and crew.

The expansion of IFC is accelerating across all aircraft categories, with retrofits representing the primary installation pathway across existing fleets. Air-to-Ground (ATG) connectivity is the fastest-growing sub-segment, particularly in North America, where GOGO LLC has historically dominated ground-based networks and is transitioning its fleet toward 5G ATG infrastructure. Air-to-Air connectivity, while currently a smaller share, is gaining traction in military applications where low-latency, resilient peer communications are essential for coordinated operations.

Frequency Insights

The Ku-Band frequency segment holds the largest share in the Connected Aircraft market, accounting for approximately 50% of frequency-based revenue, owing to its widespread adoption and established ground and space infrastructure across global aviation markets. Operating at 11-14 GHz, Ku-band offers a balance of coverage, capacity, and cost-effectiveness that has made it the workhorse of commercial airline IFC since the early 2000s.

However, the Ka-Band segment is the fastest-growing, driven by its significantly higher bandwidth capacity and lower latency, attributes increasingly demanded by passengers seeking to stream video or conduct video calls at altitude. Ka-band is particularly prominent in Viasat and Inmarsat (now combined) deployments, with Delta Air Lines selecting Viasat's Ka-band system for over 300 mainline narrow-body aircraft.

Product Type Analysis

The Systems segment is the dominant product type in the Connected Aircraft market, capturing approximately 62% of total market revenue in 2024. Systems encompass the full suite of hardware and infrastructure required for aircraft connectivity, including satellite communication terminals, antenna systems, modems, onboard routers, wireless access points, and electronic control units. Antenna systems represent the largest hardware sub-component as they are the critical enabler for maintaining communication at cruising altitudes and are subject to regular technology refresh cycles as satellite network architectures evolve.

The Solutions segment is growing at the fastest rate, reflecting the industry's pivot from one-time hardware procurement to recurring, software-enabled service models encompassing flight operations analytics, passenger engagement platforms, predictive maintenance, and cybersecure network management. Providers combining hardware systems with managed connectivity and data services are capturing increasing per-aircraft revenue through multi-year service agreements.

Regional Insights

North America Connected Aircraft Market Trends

North America is the largest regional market for Connected Aircraft, with the United States leading globally due to the world's largest commercial airline fleet, mature satellite communication infrastructure, and early mass adoption of in-flight Wi-Fi. Over 80% of aircraft flying out of North America are equipped with IFC systems, supported by major connectivity providers including Viasat, GOGO LLC, Panasonic Avionics Corporation, and Collins Aerospace. The region is home to six of the world's largest connected commercial fleets. The U.S. FAA provides the regulatory framework for airborne connectivity certification, while the Federal Communications Commission (FCC) manages spectrum allocation critical to ATG and satellite-based IFC services.

North America is also the primary deployment geography for emerging LEO connectivity through Starlink, which had secured contracts covering approximately 2,500 aircraft by September 2025. GOGO LLC is transitioning its ATG network from legacy 4G to a new 5G ATG platform targeting business aviation, while major U.S. carriers including Delta Air Lines and United Airlines are investing in next-generation Ka-band and LEO upgrade programs.

Asia Pacific Connected Aircraft Market Trends

Asia Pacific is the fastest-growing regional market in the global Connected Aircraft market, driven by explosive growth in air travel across China, India, Japan, and ASEAN nations. The region is seeing the largest volume of new aircraft deliveries globally, with India and China driving particularly strong demand for IFC-equipped platforms. Viasat successfully activated its Swift Broadband and Fleet Broadband services on its I-6 F1 satellite over the Asia Pacific region in 2024, significantly increasing network capacity for aviation customers. The company also expanded to a full-fleet agreement with STARLUX Airlines in the Asia Pacific region, reflecting the region's rapid adoption of premium connected services.

India is emerging as a pivotal growth market, with the government's UDAN scheme expanding regional aviation infrastructure and the Directorate General of Civil Aviation (DGCA) progressively updating in-flight connectivity regulations. Vietnam, Indonesia, and India are actively investing in expanding aviation infrastructure, fueling demand for advanced connected aircraft systems.

Europe Connected Aircraft Market Trends

Europe is the second-largest regional market for Connected Aircraft, led by Germany, the United Kingdom, France, and Spain as the primary consumption hubs. European aviation's regulatory environment, governed by EASA and increasingly harmonized with ICAO standards, drives structured procurement of certified connected aviation systems. The European Aviation Network (EAN), combining S-band satellite coverage with a Deutsche Telekom ground network, represents a uniquely European IFC infrastructure.

The European Space Agency (ESA) is actively supporting connected aircraft infrastructure through its agreement with the Mobile Satellite Services Association (MSSA) and Viasat to develop standards-based open-architecture LEO constellations. In February 2024, Air India selected Thales to retrofit its Boeing 777 and 787 aircraft with the AVANT Up IFE system under a USD 400 million contract covering 40 aircraft. Nordic European airlines are also emerging as fast adopters of LEO services, with Icelandair and SAS among the early IFC expansion customers of Viasat following the Inmarsat integration.

Competitive Landscape

The connected aircraft market exhibits a moderately consolidated competitive structure, with a small number of vertically integrated technology leaders, Honeywell International Inc., Viasat (incorporating Inmarsat), Panasonic Avionics Corporation, Collins Aerospace, and Thales, commanding dominant market positions through long-term OEM and airline supply agreements.

Key differentiators include satellite network coverage breadth, frequency-band diversity (Ka, Ku, L, S), integration with ADAS and avionics platforms, and the ability to offer managed connectivity solutions that combine hardware, software, and service-level agreements. Emerging business model trends include performance-based connectivity contracts, free passenger Wi-Fi models subsidized by airline commercial revenues, and AI-driven operational analytics platforms that monetize flight data beyond traditional IFC hardware margins.

Key Developments:

- 2024: Viasat expanded its commercial IFC fleet by approximately 13% year-over-year, adding airline customers including Korean Airlines, Etihad Airways, Ethiopian Airlines, and Qantas, while activating its I-6 F1 satellite over Asia Pacific to expand regional network capacity.

- October 2025: Viasat, Inc. launched incentive programs of up to US$ 140,000 per aircraft to support business aviation operators in transitioning from legacy Ku-band to its JetXP next-generation Ka-band IFC service, accelerating fleet-wide connectivity upgrades.

- November 2025: Honeywell International Inc. unveiled the JetWave X satcom system for military and government UAS operations, integrating multi-orbit Ka-band connectivity (GEO, MEO, HEO) and announcing a planned 2026 delivery with special military-government frequency support.

Companies Covered in Connected Aircraft Market

- Anuvu (Global Eagle Entertainment, Inc.)

- BAE Systems PLC

- Cobham PLC

- Collins Aerospace (Raytheon Technologies)

- GOGO LLC

- Honeywell International Inc.

- Inmarsat Global Limited

- Kontron (S&T)

- Panasonic Avionics Corporation

- Thales

- Viasat, Inc.

Frequently Asked Questions

The global Connected Aircraft market is valued at US$ 8.4 Bn in 2026 and is projected to reach US$ 21.7 Bn by 2033, growing at a CAGR of 14.5% over the forecast period.

The primary drivers are surging passenger demand for in-flight Wi-Fi with the IFC segment representing 62% of all connectivity deployments in 2024rapid deployment of LEO satellite constellations such as SpaceX Starlink that improve latency and bandwidth and growing military modernization budgets investing in mission-critical data links for ISR, transport, and UAS platforms. Air travel growth with EU passenger numbers rising 19.3% in 2023 per Eurostat is also accelerating airline fleet expansion and connectivity upgrade investments.

The Ku-Band segment currently holds the dominant position in the Connected Aircraft market with approximately 50% frequency share, owing to its widespread established infrastructure across commercial aviation globally.

North America is the leading region in the global Connected Aircraft market, with over 80% of North American aircraft equipped with IFC systems. The United States drives this dominance through the world's largest connected commercial fleet, an advanced satellite ground infrastructure, and the headquarters of leading providers including Viasat, GOGO LLC, Panasonic Avionics Corporation, and Honeywell International Inc. Asia Pacific is the fastest-growing regional market, driven by fleet expansion in China, India, and ASEAN economies.

The leading companies in the Connected Aircraft market include Viasat, Inc. (incorporating Inmarsat), Honeywell International Inc., Panasonic Avionics Corporation, Collins Aerospace (Raytheon Technologies), Thales Group, GOGO LLC, BAE Systems PLC, Anuvu (Global Eagle Entertainment), Cobham PLC, Kontron (S&T), and Iridium Communications Inc.