- Aerospace & Defense

- Digital Glass Military Aircraft Cockpit Systems Market

Digital Glass Military Aircraft Cockpit Systems Market Size, Share, and Growth Forecast 2026 - 2033

Digital Glass Military Aircraft Cockpit Systems Market by System Type (Multi-Function Display, Primary Flight Display, Engine Indicating & Crew Alerting System, Head-Up Display, Helmet-Mounted Display, Flight Management System, Sensor Fusion System, Integrated Cockpit System, Standalone Display Unit), Component, Display Technology, Aircraft Type, End-user, and Regional Analysis, 2026 - 2033

Digital Glass Military Aircraft Cockpit Systems Market Size and Trend Analysis

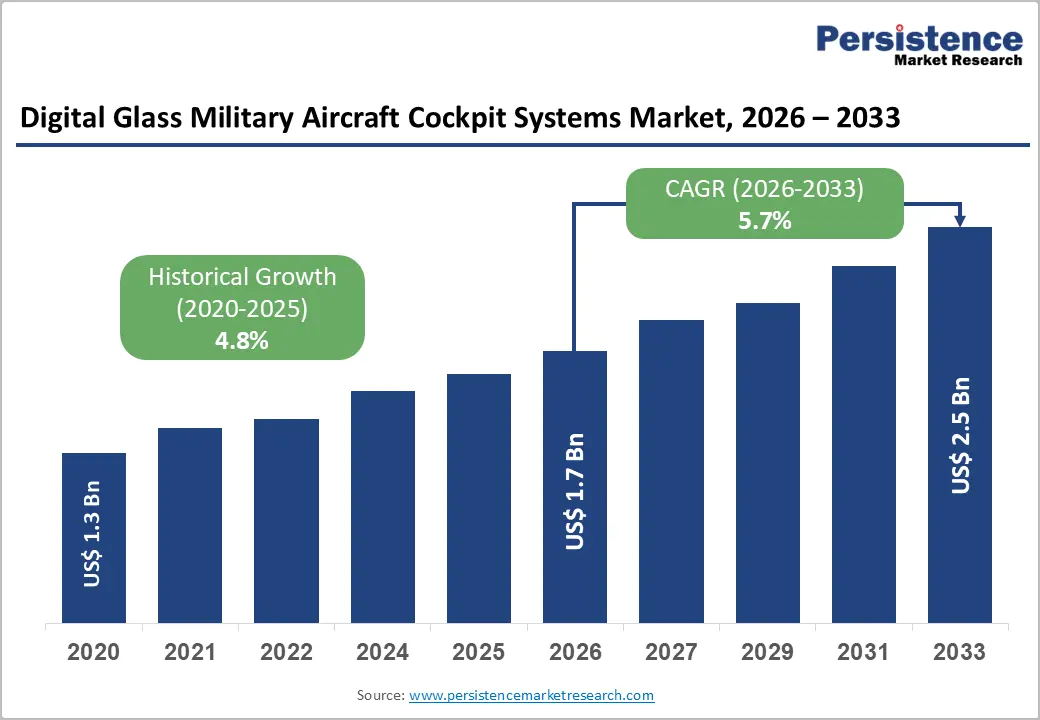

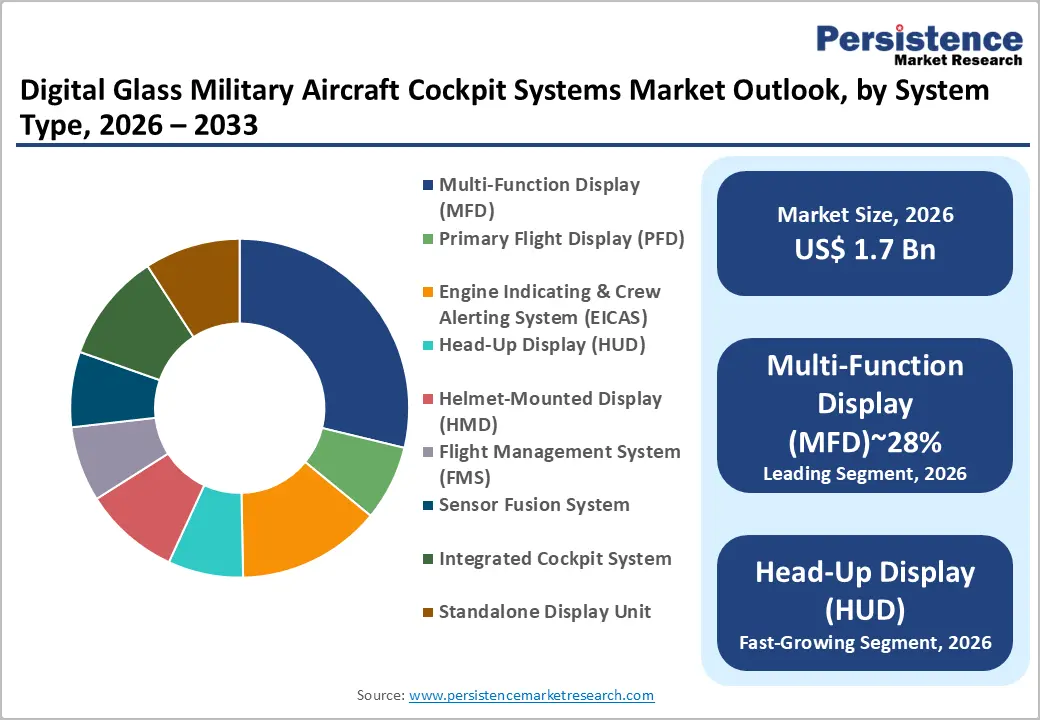

The global digital glass military aircraft cockpit systems market size is likely to be valued at US$ 1.7 billion in 2026 and is expected to reach US$ 2.5 billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033.

The market is being driven by escalating defense modernization programs across major military powers, growing procurement of next-generation fighter jets and multirole aircraft, and rising integration of advanced avionics systems.

Key Industry Highlights:

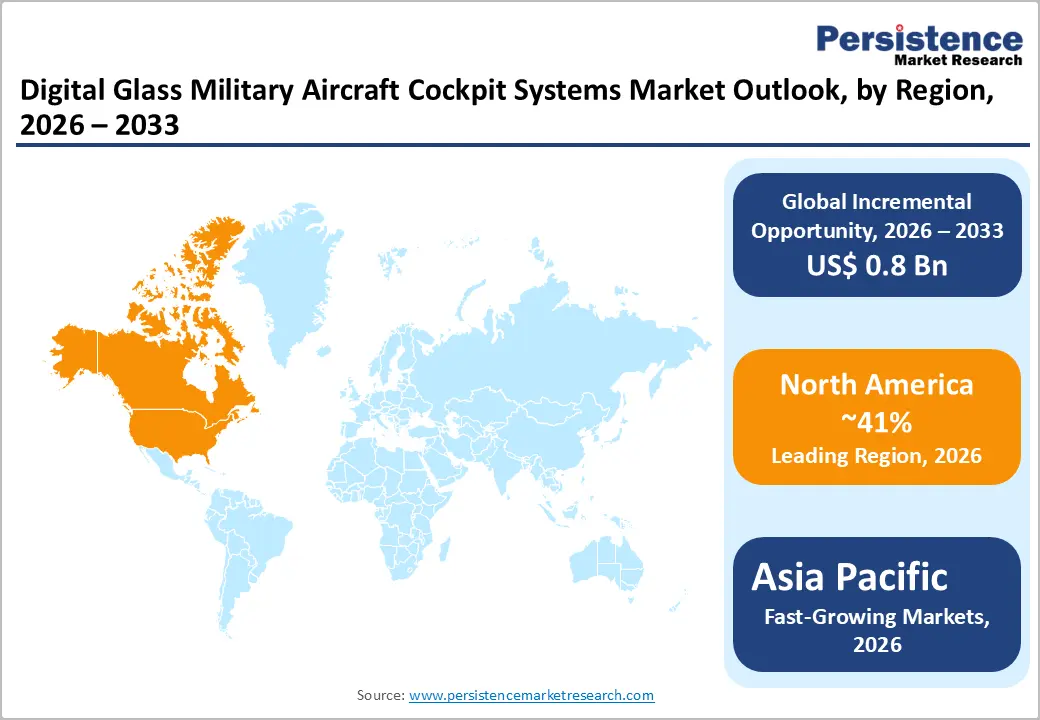

- Leading Region: North America leads the global digital glass military aircraft cockpit systems market, accounting for 41% share, underpinned by the large U.S. defense budget, advanced OEM ecosystem, and major programs including the F-35A and B-21 Raider, driving sustained cockpit technology demand.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market, with a CAGR of 6.1%, driven by record defense budgets in India and China, indigenous fighter programs such as HAL Tejas Mk. 2 and KF-21 Boramae, and Japan's GCAP participation, which is stimulating advanced avionics procurement.

- Dominant Aircraft Type: Fighter aircraft is dominant, commanding approximately 35% market share, backed by global fleets of F-35, Rafale, and Eurofighter Typhoon, and sustained modernization spending by NATO and Asia Pacific air forces.

- Fastest-Growing Display Segment: OLED display technology is the fastest-growing segment, gaining rapid traction in next-generation HMDs and HUDs for sixth-generation fighter programs, owing to superior contrast, weight efficiency, and refresh rates versus AMLCD.

- Key Opportunity: The advancement of UAV and optionally manned aircraft programs, including MQ-9B and GCAP UCAV variants, presents a significant opportunity for digital cockpit system suppliers to develop hybrid manned/unmanned cockpit architectures for the future air combat environment.

| Key Insights | Details |

|---|---|

| Digital Glass Military Aircraft Cockpit Systems Market Size (2026E) | US$ 1.7 Billion |

| Market Value Forecast (2033F) | US$ 2.5 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.7% |

| Historical Market Growth (2020 - 2025) | 4.8% CAGR |

Market Dynamics Analysis

Drivers - Accelerating Military Aircraft Modernization Programs

Governments across the globe are channeling substantial budgets into fleet modernization, directly benefiting the digital glass cockpit systems market. The U.S. Department of Defense (DoD) allocated over US$ 858 billion in defense spending for FY2024, with a significant portion earmarked for avionics upgrades across platforms such as the F-35, F/A-18, and KC-46.

The NATO alliance nations have committed to achieving the 2% GDP defense spending target, spurring procurement of advanced aircraft fitted with integrated digital cockpit systems. Similarly, India's Ministry of Defence has approved procurement of 114 Multi-Role Fighter Aircraft (MRFA), each requiring modern glass cockpit avionics. Such programs collectively sustain robust demand for Multi-Function Displays, Sensor Fusion Systems, and Flight Management Systems, establishing a strong long-term procurement pipeline.

Rising Adoption of Sensor Fusion and Integrated Avionics Architectures

Modern aerial warfare demands real-time integration of radar, electro-optical, and electronic warfare data on a unified pilot interface. The growing shift toward Open Systems Architecture (OSA) and Modular Open Systems Approach (MOSA), mandated by the U.S. DoD through its Better Buying Power 3.0 initiative, enables seamless upgrades and interoperability of avionics sub-systems.

Programs such as Northrop Grumman's AN/APG-83 AESA radar and Collins Aerospace's Pro Line Fusion avionics suite demonstrate the market's pivot toward fully networked cockpit environments. According to the Congressional Budget Office (CBO), the U.S. Air Force plans to spend over US$ 14 Billion on avionics and electronic systems during FY2024-FY2028, underscoring the scale of investment supporting integrated cockpit adoption.

Restraints - Exceptionally High Development and Certification Costs

One of the most significant barriers in the digital glass cockpit systems market is the steep cost associated with design, development, testing, and regulatory certification. Military avionics must comply with stringent standards such as DO-178C (software) and DO-254 (hardware), published by RTCA.

Achieving certification for safety-critical display systems can cost between US$ 50 Million and US$ 200 Million per platform, according to estimates from the Aerospace Industries Association (AIA). These costs restrict market entry to a small number of established prime contractors, while simultaneously straining defense budgets, potentially delaying procurement timelines and limiting adoption in smaller national air forces with constrained fiscal capacity.

Cybersecurity Vulnerabilities and Electronic Warfare Threats

The increasing digital connectivity of modern cockpit systems introduces significant cybersecurity risks. As mission computers, data buses, and communication systems become more networked, they also become more susceptible to adversarial electronic warfare and cyberattacks.

The U.S. Government Accountability Office (GAO) has repeatedly flagged cybersecurity weaknesses in weapon system software, noting in its 2023 Annual Threat Report that adversaries are developing tools specifically targeting avionics networks. Securing military cockpit systems against such threats demands continuous software updates and dedicated cybersecurity protocols, adding layers of operational complexity and cost that can slow procurement decisions and system upgrades.

Opportunities - Next-Generation Fighter Programs and NGAD/GCAP Initiatives

The development of sixth-generation fighter aircraft presents a transformational opportunity for advanced cockpit system manufacturers. The U.S. Air Force's Next Generation Air Dominance (NGAD) program and the Global Combat Air Programme (GCAP) jointly developed by the U.K., Italy, and Japan, are designed from the ground up with fully digital, AI-assisted cockpit architectures.

These programs mandate Helmet-Mounted Displays (HMDs), advanced Head-Up Displays (HUDs), and real-time sensor fusion systems. The GCAP program alone is expected to generate procurement requirements across three nations over the 2035-2050 timeframe. For companies like BAE Systems, Leonardo, and Thales, early-stage involvement in these programs provides multi-decade revenue visibility and positions them as critical technology suppliers in the evolving military aerospace ecosystem.

UAV and Unmanned Combat Aerial Vehicle (UCAV) Cockpit Integration

The rapid proliferation of Unmanned Aerial Vehicles (UAVs) and Unmanned Combat Aerial Vehicles (UCAVs) in modern military arsenals represents a substantial emerging opportunity. While UAVs operate without onboard pilots, they require sophisticated ground control station (GCS) displays, mission management software, and data link interfaces that draw heavily on digital cockpit technologies.

The Global UAV defense market has seen consistent budget increases, with the U.S. Air Force requesting over US$ 2.7 billion for unmanned systems in FY2024. Programs such as General Atomics' MQ-9B SkyGuardian and Northrop Grumman's MQ-4C Triton incorporate advanced GCS cockpit systems. As optionally manned aircraft gain traction, hybrid cockpit architectures that can function both in manned and unmanned modes represent a critical technology frontier and a compelling market opportunity for system integrators.

Category-wise Analysis

By System Type Insights

The Multi-Function Display (MFD) segment dominates the By System Type category, commanding approximately 28% of the overall market share. MFDs serve as the central interface for presenting flight data, tactical imagery, navigation charts, and weapons management information on a single reconfigurable screen, making them indispensable across virtually all military aircraft platforms. Their versatility enables pilots to consolidate information from multiple sub-systems, radar, FLIR, moving maps, into a unified display, significantly reducing workload and improving decision-making speed.

Leading programs such as Lockheed Martin's F-35 Lightning II, which features an 8-inch x 20-inch panoramic MFD developed by BAE Systems, exemplify the growing screen real estate and processing power being built into modern MFDs. The segment's dominance is further reinforced by ongoing retrofit programs for F-16 and F/A-18 fleets, driving sustained aftermarket demand globally.

By Component Insights

Among cockpit components, display units hold the leading position, accounting for roughly 32% of the component segment. Display units form the most visible and mission-critical hardware layer of any digital cockpit, encompassing MFDs, PFDs, HUDs, and standby instrument displays. Their centrality to pilot interfaces means they attract the largest share of both new-build and upgrade procurement spending.

Advanced AMLCD and OLED display units are witnessing strong demand in programs such as Boeing's T-7A Red Hawk trainer and Airbus Defence & Space's A400M Atlas transport aircraft. The proliferation of touchscreen-enabled display units, driven by standards from ARINC 661 for cockpit display systems, further cements this segment's lead, as military customers increasingly seek rugged, high-brightness displays for sunlight-readable cockpit environments.

By Display Technology Insights

The AMLCD (Active Matrix Liquid Crystal Display) technology segment leads the display technology category, holding an estimated 38% market share. AMLCD panels have become the preferred technology in military cockpits owing to their proven reliability, superior sunlight readability, critical in airborne environments, wide operating temperature range, and availability in ruggedized form factors meeting MIL-STD-810G specifications.

Key suppliers including Barco, Elbit Systems, and Astronautics Corporation of America widely AMLCD-based displays across F-15, F-16, Eurofighter Typhoon, and helicopter platforms. However, OLED technology is the fastest-growing segment, gaining traction for its superior contrast ratio, faster refresh rates, and thinner form factor, attributes critical for next-generation HMDs and Head-Up Displays in programs like NGAD and GCAP.

By Aircraft Type Insights

The fighter aircraft segment holds the dominant position within the By Aircraft Type category, representing approximately 35% of total market demand. Fighter aircraft demand the most sophisticated digital cockpit systems due to the complexity of their missions, which require seamless integration of weapons management, radar, electronic warfare, and navigation data on a single platform.

Globally, approximately 10,000+ fighter aircraft are currently in active service according to IISS Military Balance 2024, with a significant portion undergoing avionics upgrades. Programs such as the F-35 Joint Strike Fighter (over 900 aircraft delivered as of 2024), the Dassault Rafale, and the Eurofighter Typhoon collectively represent major demand anchors. Emerging markets such as India, Poland, and Greece are procuring advanced fighters, creating new adoption waves for state-of-the-art cockpit systems.

By End-user Insights

The Air Force segment commands the largest share among end-users, accounting for approximately 47% of total market revenue. Air forces globally operate the largest and most technologically advanced military aircraft fleets, necessitating continuous investment in digital cockpit modernization.

The U.S. Air Force, the world's largest, operates over 5,000 aircraft according to IISS Military Balance 2024, with major modernization programs underway including the F-35A procurement, the B-21 Raider stealth bomber, and the F-16V Viper upgrade program. Simultaneously, China's People's Liberation Army Air Force (PLAAF) and India's Indian Air Force (IAF) are among the fastest-growing end-user segments, driven by indigenous fighter development programs such as the HAL Tejas Mk. 2 and the Chengdu J-20, both of which integrate advanced glass cockpit avionics.

Regional Insights

North America Digital Glass Military Aircraft Cockpit Systems Trends

North America, led by the United States, holds the largest share of the global digital glass military aircraft cockpit systems market. The region benefits from a dense ecosystem of prime defense contractors, including Honeywell International, Collins Aerospace, L3Harris Technologies, and Northrop Grumman, that supply both domestic and international military customers. The U.S. DoD's FY2024 budget allocated over US$ 37 Billion for aircraft procurement and modification, ensuring a steady pipeline for cockpit system integrations. Additionally, Canada's Strategic Fighter Capability program, which selected the F-35A for its 88-aircraft requirement in 2023, will drive significant cockpit technology adoption through the 2030s.

The U.S. Federal Aviation Administration (FAA) and DoD jointly maintain robust regulatory and certification frameworks, anchored by MIL-SPEC and DO-178C/DO-254 standards, that set the global benchmark for avionics development. The MOSA mandate embedded in the National Defense Authorization Act (NDAA) compels program offices to adopt open architecture cockpit systems, stimulating competition and innovation among Tier-2 suppliers and fostering a healthy innovation ecosystem.

Europe Digital Glass Military Aircraft Cockpit Systems Trends

Europe represents the second-largest regional market, underpinned by robust defense spending commitments following Russia's invasion of Ukraine in 2022. Germany announced a €100 Billion special defense fund (Sondervermögen) and has committed to purchasing 20 Eurofighter Typhoon Tranche 4 aircraft and 20 F/A-18E/F Super Hornets. France continues investment under Loi de Programmation Militaire (LPM) 2024-2030, allocating €413 Billion for defense, including Dassault Rafale F4 standard upgrades with enhanced avionics. The U.K. is a key participant in the GCAP sixth-generation fighter program, which will integrate the most advanced digital cockpit systems developed in the region.

Regulatory harmonization under the European Defence Agency (EDA) and NATO STANAG standards is streamlining cross-border avionics certification, reducing time-to-deployment for digital cockpit system upgrades across member states. Spain's F-18 Hornet modernization program and Italy's participation in both the F-35 program and GCAP position these markets as significant growth contributors within the European cockpit systems landscape.

Asia Pacific Digital Glass Military Aircraft Cockpit Systems Trends

Asia Pacific is the fastest-growing market for digital glass military aircraft cockpit systems, driven by heightened geopolitical tensions, rapidly increasing defense budgets, and ambitious indigenous defense manufacturing programs. China's People's Liberation Army Air Force continues to expand its fleet of J-20 stealth fighters and J-16 multirole jets, all equipped with advanced indigenous glass cockpit systems developed by entities such as AVIC. India's defence budget for FY2024-25 reached a record INR 6.21 Trillion (approximately US$ 74 Billion), with HAL Tejas Mk.1A and Mk.2 programs prominently featuring modern digital avionics.

Japan's F-X program, co-developed under GCAP with the U.K. and Italy, signals a strategic pivot toward domestically developed advanced cockpit systems. South Korea's KF-21 Boramae and ASEAN nations such as Indonesia and Philippines are actively modernizing their air forces. Competitive manufacturing costs and expanding domestic supply chains in India under the Atmanirbhar Bharat (Self-Reliant India) initiative present significant opportunities for global OEMs to establish local partnerships and joint ventures, driving both technology transfer and long-term market penetration.

Competitive Landscape

The digital glass military aircraft cockpit systems market exhibits a moderately consolidated structure, dominated by a handful of global prime contractors and specialized avionics OEMs. Tier-1 players such as Collins Aerospace, Honeywell International, Thales Group, BAE Systems, and Elbit Systems collectively account for the majority of market revenue. Competition is driven by R&D investment in OLED display technologies, AI-assisted pilot interfaces, and open systems architecture.

Companies are pursuing growth through strategic acquisitions, long-term program partnerships, and co-development agreements with national defense agencies. Emerging players from India and South Korea are beginning to contest market share in their domestic procurement programs, gradually introducing competitive pressure in the Asia Pacific segment.

Key Developments:

- February 2025: Collins Aerospace was awarded a US$ 174 Million contract by the U.S. Air Force for the development and integration of advanced digital cockpit systems for the F-15EX Eagle II modernization program, covering next-generation MFDs and integrated avionics.

- October 2024: Elbit Systems announced a contract with an undisclosed NATO nation to supply Helmet-Mounted Display (HMD) systems integrated with night-vision-compatible displays for its tactical fighter fleet, valued at approximately US$ 35 Million.

- March 2024: Thales Group unveiled the TopDeck digital cockpit suite at Eurosatory 2024, featuring an AI-augmented Sensor Fusion System and advanced Head-Up Display designed for integration into next-generation European fighter and rotary-wing platforms.

Companies Covered in Digital Glass Military Aircraft Cockpit Systems Market

- Honeywell International Inc.

- Thales Group

- Collins Aerospace

- BAE Systems plc

- Northrop Grumman Corporation

- Elbit Systems Ltd.

- L3Harris Technologies Inc.

- General Dynamics Corporation

- Safran S.A.

- Leonardo S.p.A.

- Lockheed Martin Corporation

- Garmin Ltd.

- Astronautics Corporation of America

- Moog Inc.

- Meggitt PLC

- Rockwell Collins (now part of Collins Aerospace)

- ASELSAN A.Ş.

- Hindustan Aeronautics Limited (HAL)

- Barco N.V.

- Universal Avionics Systems Corporation

Frequently Asked Questions

The global Digital Glass Military Aircraft Cockpit Systems Market is projected to reach US$ 2.5 Billion by 2033, growing from US$ 1.7 Billion in 2026 at a CAGR of 5.7% during the forecast period.

The market is primarily driven by increasing military modernization budgets globally, rising procurement of next-generation fighter jets such as the F-35 and Rafale, the adoption of Open Systems Architecture (OSA) and MOSA mandates, and growing integration of AI-assisted sensor fusion and advanced HMD systems in modern military aircraft.

The Multi-Function Display (MFD) segment holds the dominant position in the By System Type category, accounting for approximately 28% market share, driven by its critical role in consolidating flight, tactical, navigation, and weapons management data into a single reconfigurable interface across virtually all military aircraft platforms.

North America is the leading regional market, supported by the substantial U.S. defense budget, a highly developed OEM ecosystem featuring companies such as Collins Aerospace and Honeywell, and sustained demand from flagship programs including the F-35A, B-21 Raider, and various legacy aircraft upgrade initiatives.

The most compelling near-to-medium term opportunity lies in the development and supply of advanced cockpit systems for sixth-generation fighter programs such as NGAD and GCAP, as well as hybrid manned/unmanned cockpit architectures for UCAV platforms. These programs demand cutting-edge OLED HMDs, AI-augmented sensor fusion systems, and integrated mission management suites, creating multi-billion-dollar procurement pipelines stretching through the 2040s.

The leading companies operating in this market include Honeywell International Inc., Collins Aerospace, Thales Group, BAE Systems plc, Northrop Grumman Corporation, Elbit Systems Ltd., L3Harris Technologies Inc., Safran S.A., Leonardo S.p.A., and Lockheed Martin Corporation, among others.