- Semiconductor Materials & Components

- Betavoltaic Device Market

Betavoltaic Device Market Size, Share, and Growth Forecast, 2026 - 2033

Betavoltaic Device Market by Isotope (Tritium, Krypton, Nickel, Others), Application (Medical Implants, Defense & Aerospace, Energy, Consumer Electronics), Form (Planar, Curved, Flexible), and Regional Analysis for 2026-2033

Betavoltaic Device Market Share and Trends Analysis

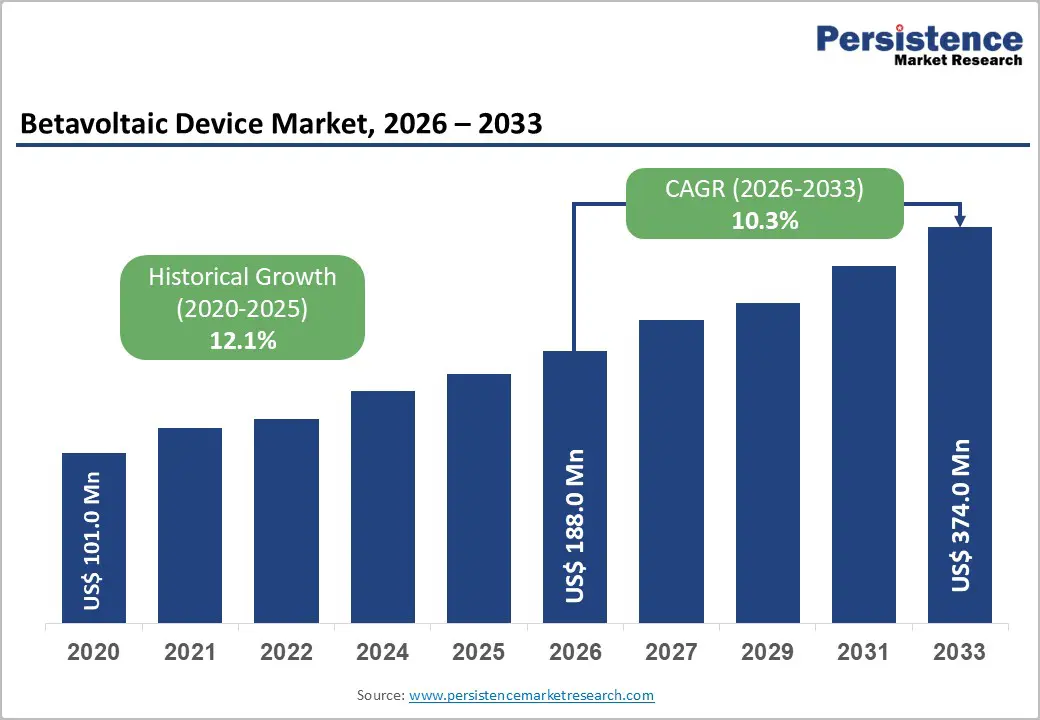

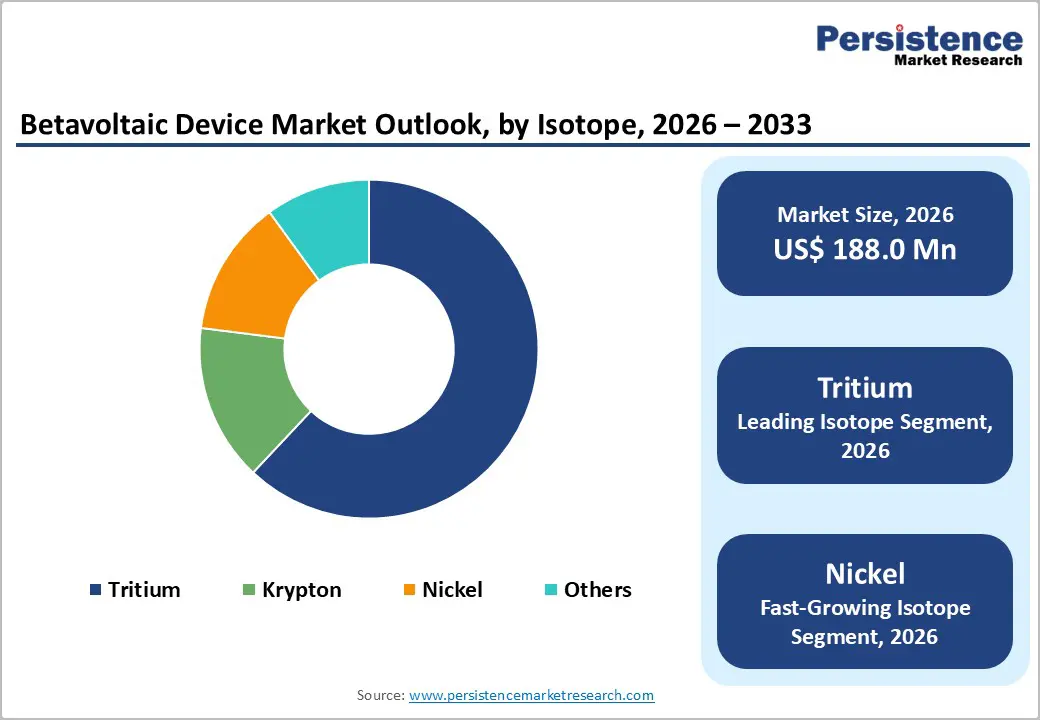

The global betavoltaic device market size is likely to be valued at US$ 188.0 million in 2026, and is projected to reach US$ 374.0 million by 2033, growing at a CAGR of 10.3% during the forecast period 2026−2033.

This growth is primarily driven by the increasing demand for long-lasting, maintenance-free power sources in remote sensing applications, aerospace systems, and medical implants. The market expansion is further supported by technological advancements in radioisotope battery efficiency, growing investments in space exploration programs, and the critical need for reliable power solutions in extreme environmental conditions. Rising adoption across defense and security applications, coupled with miniaturization trends in electronic devices, continues to accelerate market penetration globally.

Key Industry Highlights

- Leading & Fastest-growing Isotope Type: Tritium is slated to lead with an estimated 62% revenue share in 2026, with nickel likely to post the highest 2026-2033 CAGR.

- Leading & Fastest-growing Application: Medical implants are anticipated to capture roughly 45% of the revenue share in 2026, while defense & aerospace applications are set to grow the fastest through 2033.

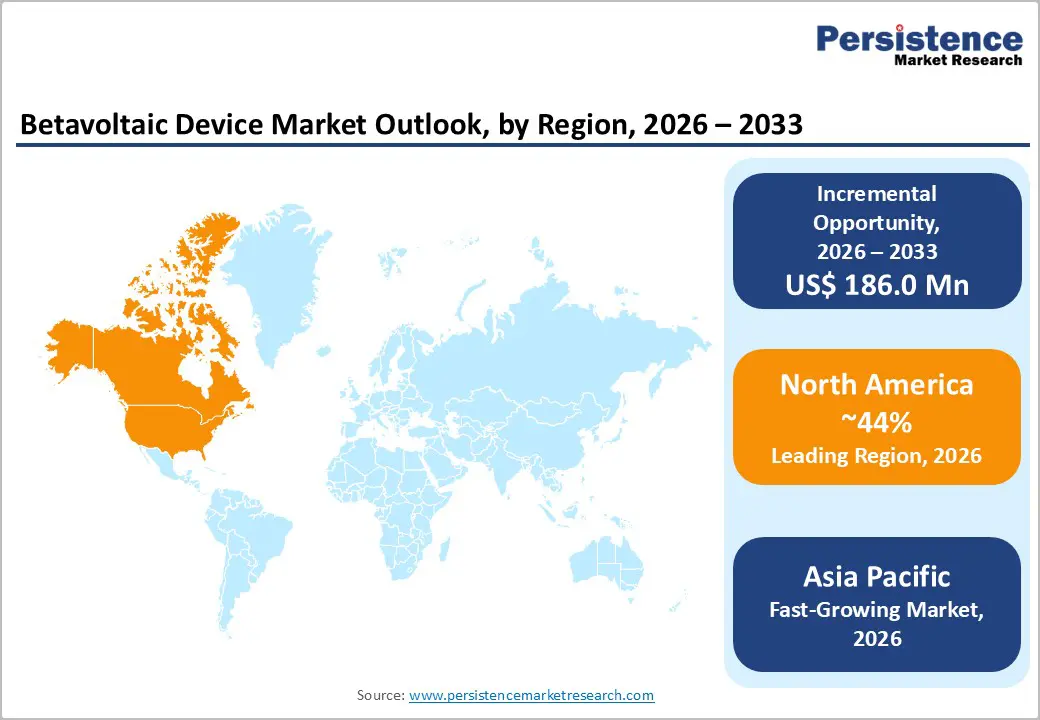

- Dominant Region: North America is slated to command about 44% of the market share in 2026, propelled by enormous investments in defense and aerospace technologies.

- Fastest-growing Market: The Asia Pacific market is likely to be the fastest-growing through 2033, powered by rapid industrial expansion and a soaring appetite for advanced electronics.

- August 2025: The University of Ottawa partnered with Canadian Nuclear Laboratories (CNL) introduced three standardized performance metrics to evaluate betavoltaic batteries, aiming to accelerate commercialization of ultra-long-lasting nuclear micro-power systems.

| Report Attribute | Details |

|---|---|

|

Betavoltaic Device Market Size (2026E) |

US$188.0 Mn |

|

Market Value Forecast (2033F) |

US$ 374.0 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

10.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

12.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expanding Space Exploration and Satellite Deployment Programs

The accelerating pace of space exploration missions and expanding satellite constellations is fueling the demand for advanced, long-lasting power solutions. Government agencies and private companies are investing more in orbital platforms, lunar initiatives, and deep space programs. For example, the National Aeronautics and Space Administration (NASA) is advancing the Artemis program, while commercial operators are developing sustained lunar operations and autonomous surface systems. These missions require compact energy sources that deliver uninterrupted performance in harsh environments. Betavoltaic devices meet this need by generating continuous electricity for decades without significant degradation across extreme temperature ranges. Their durability supports spacecraft subsystems such as remote sensors, navigation modules, communication relays, and scientific payloads operating far from direct sunlight.

The International Space Station (ISS) continues to host long-duration experiments that depend on stable auxiliary power for critical instruments. Deep space probes are traveling farther from the Sun, prompting mission planners to select betavoltaic systems to ensure reliability where solar arrays are less effective. Manufacturers are refining semiconductor materials and improving isotope integration techniques, which increases power density and enhances safety standards. Sustained exploration efforts are expected to accelerate innovation and establish betavoltaic technology as a core energy solution for future space infrastructure.

Rising Defense and Security Infrastructure Investments

Government defense modernization initiatives and critical infrastructure security upgrades are driving sustained demand for betavoltaic technology. National security agencies are strengthening electronic warfare systems, autonomous platforms, and persistent surveillance capabilities. The United States Department of Defense (DOD) is advancing strategic capability plans that prioritize distributed sensor networks with long operational lifespans in remote and denied areas. These programs require compact power sources that operate reliably without regular maintenance. Betavoltaic devices support applications such as unattended ground sensors, subsea monitoring equipment, remote communication nodes, and encrypted tracking systems in harsh terrain. Their ability to deliver continuous energy for decades reduces logistical risks and lowers lifecycle costs.

Governments are reinforcing border protection systems, seismic detection arrays, and environmental surveillance platforms that guard critical assets. Security agencies are deploying long-duration monitoring networks across coastlines, pipelines, and strategic facilities where routine battery replacement is impractical. Betavoltaic solutions ensure uninterrupted operation and strengthen resilience against sabotage and environmental disruption. Procurement authorities are establishing multi-year supply agreements and technical standards to accelerate adoption. As modernization strategies progress, manufacturers are collaborating with defense contractors to improve power density, shielding methods, and integration efficiency. Sustained public sector investment is expected to position betavoltaic technology as a dependable foundation for secure and autonomous monitoring infrastructure worldwide.

Critical Supply Concentration and Geopolitical Risk Exposure

The market is facing structural constraints because radioisotope production is concentrated in a small number of facilities. Commercial nickel sixty-three output is largely controlled by reactor complexes in Russia and Kazakhstan, including the Mayak Production Association and the Research Institute of Atomic Reactors, as well as the Ulba Metallurgical Plant. Tritium manufacturing is also limited to a few qualified sites, mainly operated by state entities such as the U.S. Department of Energy (DOE) at the Savannah River Site, Ontario Power Generation in Canada, and national nuclear organizations in Russia and China. This narrow supplier base is creating supply chain fragility and limiting procurement flexibility. When political tensions or sanctions are emerging, manufacturers are experiencing longer lead times, higher acquisition costs, and project delays. Companies are therefore reassessing sourcing strategies and exploring alternative isotope development pathways to reduce dependence on a restricted production network.

Radioisotopes are classified as dual-use materials under international non-proliferation frameworks, which place strict controls on cross-border transactions. Export licensing, end-use verification, and bilateral nuclear cooperation agreements are shaping commercial access conditions. For instance, the U.S. DOE is restricting certain tritium (hydrogen-3) exports, while the European Union (EU) is enforcing regulations on isotope transport, and China is tightening oversight of strategic materials. These policies are creating uneven market access based on geography and application type. Geopolitical disputes or national security decisions are disrupting established supply relationships and forcing manufacturers to qualify new vendors under complex regulatory review. Persistent uncertainty is encouraging regional production initiatives and greater investment in domestic isotope capabilities.

Stringent Regulatory Requirements and Public Perception Challenges

Radioisotope-based technologies are operating within complex regulatory frameworks across multiple international jurisdictions. Approval processes are extending over long review periods as authorities conduct detailed technical evaluations. The U.S. Nuclear Regulatory Commission (NRC), the International Atomic Energy Agency (IAEA), and national radiation protection bodies are requiring comprehensive safety demonstrations, environmental impact studies, and long-term waste management plans. These obligations are increasing compliance costs and slowing commercialization timelines. Transportation rules classify betavoltaic devices as radioactive materials, which requires certified packaging, trained handlers, and pre-approved shipping routes. These measures are raising logistics expenses and limiting distribution flexibility.

Public perception is also shaping adoption patterns. Although betavoltaic systems emit low-energy beta particles with minimal penetration depth, concerns about radiation exposure are influencing policy debates and procurement decisions. Urban infrastructure planners and consumer product developers are approaching deployment cautiously due to safety sensitivities. Insurers are imposing strict coverage conditions, and operators are planning for long-term liability and decommissioning responsibilities. These factors are increasing total ownership costs and narrowing viable application segments. As regulatory clarity is gradually improving, specialized sectors such as medical devices, industrial monitoring, and defense systems are continuing to adopt the technology where established pathways already exist.

Emerging Applications in Internet of Things and Remote Sensing Networks

The growth of Internet of Things (IoT) devices worldwide opens vast possibilities for betavoltaic power sources. Engineers deploy these devices in hard-to-reach spots, such as remote environmental monitoring stations, structural health sensors on bridges and pipelines, oceanographic data buoys, and agricultural precision farming sensors. These applications demand autonomous performance over extended periods, often 10 to 20 years, where teams find battery replacements too costly. Betavoltaic technology steps in by delivering reliable, long-lasting energy that eliminates frequent maintenance and cuts overall expenses.

Smart city projects in numerous municipalities will integrate maintenance-free power into traffic monitors, air quality detectors, and surveillance systems. Developers prioritize betavoltaic solutions because they lower the total cost of ownership in high-deployment areas. Initial setup expenses run high per sensor site, yet one-time installations outperform ongoing battery services in the long run. This shift will transform IoT reliability, enabling seamless data collection in isolated environments and boosting efficiency across industries. Stakeholders gain deeper insights into operations without interruptions, paving the way for scalable, sustainable networks.

Technological Advancements in Power Density and Efficiency

These materials offer superior radiation tolerance, thermal conductivity, and structural durability, which enhance long-term operational stability. As fabrication methods are becoming more precise, manufacturers are integrating refined junction architectures and optimized isotope layering to capture a greater share of emitted beta energy. These improvements are positioning betavoltaic cells as viable power sources for systems that previously exceeded their output limits. As power capability is increasing, new categories of electronics are becoming technically feasible for integration.

Engineers are evaluating betavoltaic modules for wireless communication units, microelectromechanical systems (MEMS), distributed sensors, and edge computing processors that require persistent micro power. Commercialization efforts are accelerating as public research grants and corporate development programs are supporting pilot-scale production and performance validation. Companies are forming partnerships with telecommunications providers and industrial automation firms to embed long-life energy solutions into next-generation platforms. Over the coming decade, continued materials refinement and manufacturing scale-up will have expanded the addressable market beyond specialized niches. Betavoltaic technology is steadily evolving into a strategic enabler for compact, maintenance-free electronics across advanced digital infrastructure.

North America Betavoltaic Device Market Outlook

North America is anticipated to constitute a highest market share in the Betavoltaic device market over the forecasted period. The North America shows significant growth in Betavoltaic Device market owing to huge investment in R&D of advanced technologies in the space industry by developed economy like US.

The demands for the Betavoltaic device market in North America region is increasing owing to factors such as sudden increasing ubiquity of cardiovascular diseases in region, rising adoption of Betavoltaic device or batteries as an alternatives power supply in hostile conditions in the region.

North America region has massive presence of key Betavoltaic device providers as well as increasing number of startups including Qynergy Corporation, Widetronix, Inc., BetaBatt, Inc., City Labs, Inc., and NDB Inc. Such key vendors adopted various organic/inorganic strategies, to increase customer base at global market.

Presence of such key vendors and emerging startups to provide Betavoltaic device in the region fuels the growth of the Betavoltaic device market in North America region.

Category-wise Analysis

Isotope Insights

Among isotopes, tritium is anticipated to dominate in 2026, capture close to 62% of the betavoltaic device market revenue share, backed by established manufacturing processes, relatively favorable regulatory status, and balanced performance characteristics. Tritium offers a 12.3-year half-life, providing predictable long-term power output, low-energy beta emissions (maximum 18.6 keV), ensuring minimal shielding requirements, and well-established supply chains through nuclear reactor production facilities. Commercial availability from licensed suppliers in the United States, Canada, and Russia, combined with extensive safety data spanning five decades of tritium applications, facilitates regulatory approvals across medical, industrial, and scientific applications.

Nickel is likely to be the fastest-growing isotope during the 2026-2033 forecast period, driven by superior power density characteristics and extended operational lifetime. Nickel-63's 100.1-year half-life provides nearly constant power output over decades, while higher beta particle energy (maximum 67 keV) enables greater current generation per unit volume. Recent manufacturing innovations reducing production costs by 35-40% and increasing commercial isotope availability through reactor irradiation programs in Russia and Kazakhstan support accelerated adoption across space, defense, and long-term monitoring applications where maximum operational longevity justifies premium pricing.

Application Insights

Medical implants are slated to lead by securing approximately 45% of the betavoltaic device market share in 2026. Medical devices such as pacemakers and neurostimulators depend on uninterrupted power to maintain consistent therapeutic performance. Betavoltaic devices are offering a long-lasting and stable energy source, which is reducing the frequency of surgical battery replacements and lowering associated health risks. Their durability is improving device reliability and supporting better long-term patient outcomes. As chronic conditions are becoming more prevalent and the global aging population is expanding, healthcare systems are increasing the adoption of advanced implantable technologies. This trend is strengthening demand for compact, maintenance-free power solutions that can support critical medical functions over extended periods.

Defense & aerospace applications are expected to register highest 2026-2033 growth trajectory. In this industry, betavoltaic devices are gaining attention for delivering reliable power in harsh and remote environments. Military systems, satellites, and unmanned aerial vehicles (UAVs) are operating in high-risk, temperature-sensitive, and maintenance-limited conditions where conventional batteries often fail. Betavoltaic technology is providing a long-life, low-maintenance, and vibration-resistant energy source for mission-critical equipment. Its ability to function continuously without frequent replacement is strengthening operational readiness. Rising investments in defense modernization and space exploration programs are accelerating adoption, positioning betavoltaic solutions as a strategic power option for next-generation, high-reliability applications.

Regional Insights

North America Betavoltaic Device Market Trends

North America is set to command a significant portion of the betavoltaic device market share at approximately 44% in 2026, driven by strategic investments across defense, aerospace, and healthcare sectors. Government agencies and private organizations are increasing funding for advanced energy solutions that support long-duration missions, autonomous systems, and implantable medical devices. Major corporations and innovative startups in the region are focusing on research and development (R&D) to improve energy conversion efficiency, power density, and safety standards for betavoltaic technologies. The presence of well-established manufacturing infrastructure and strong collaboration between academic institutions and industry players is enabling rapid prototyping and accelerated commercialization of next-generation devices.

The adoption of advanced technologies in North America is further strengthening market growth. Aerospace programs, military modernization initiatives, and the rising use of implantable medical devices are increasing demand for compact, reliable, and durable power sources. Companies are integrating betavoltaic modules into satellites, UAVs, edge computing devices, and wireless medical implants to ensure continuous operation under extreme conditions. As government policies and private sector investments are expanding, manufacturers are scaling production capacity, forming strategic partnerships, and boltsering supply chain resilience.

Europe Betavoltaic Device Market Trends

Europe is poised to emerge as a vital hub for betavoltaic devices amid rising commitments to sustainable energy and cutting-edge medical technologies. Germany, France, and the United Kingdom spearhead adoption through dedicated policies and investments. Governments prioritize green power sources, while healthcare sectors seek durable solutions for implants and diagnostics. Researchers collaborate across borders to refine betavoltaic designs, focusing on eco-friendly materials and seamless integration. This momentum positions the region to expand applications in renewable systems and patient care.

Industry players partner with academic centers to accelerate commercialization. They target remote sensors in wind farms, pacemakers, and environmental monitors that operate without maintenance. EU frameworks encourage innovation by streamlining approvals for low-impact nuclear tech. Companies invest in production facilities that meet stringent safety standards, drawing talent from top universities. These efforts will solidify Europe's role in global supply chains, blending sustainability goals with technological prowess. By fostering cross-sector alliances, the region unlocks efficiencies in energy harvesting and biomedical devices, setting benchmarks for long-term reliability worldwide.

Asia Pacific Betavoltaic Device Market Trends

The market for betavoltaic devices in Asia Pacific is anticipated to grow the fastest during the 2026-2033 emerge as the fastest-growing betavoltaic device market, driven by rapid industrial expansion and a strong appetite for advanced electronics. Countries such as China, Japan, and South Korea are prioritizing long-life power sources for sensors, medical implants, and industrial systems. Governments and corporations are investing in research and development to enhance performance, safety, and miniaturization. These efforts are supporting local ecosystems where chipmakers, material suppliers, and device manufacturers are collaborating to tailor betavoltaic solutions for harsh and space-constrained environments. As a result, the region is building strong capabilities across design, prototyping, and volume production.

Technology companies in the Asia Pacific are integrating betavoltaic power into applications that require continuous operation without human intervention. Research institutes are working on new semiconductor structures and radioisotope packaging methods that will have improved efficiency and safety profiles. Policy support for clean and resilient energy solutions is encouraging trials in next-generation IoT platforms, robotics, and autonomous systems. Asia Pacific will have positioned itself as a global innovation leader, with betavoltaic devices becoming a strategic enabler for its broader digital and industrial transformation.

Competitive Landscape

The global betavoltaic device market structure is moderately consolidated, dominated by leading players such as City Labs, Widetronix, JSC LUTCH, BetaBatt, and Qynergy Corporation. The market is defined by a dynamic competitive environment, with major players actively working to strengthen their positions through continuous innovation, strategic collaborations, and sustained R&D efforts. Companies are focusing on creating advanced betavoltaic solutions that deliver higher efficiency, greater reliability, and extended operational lifespans.

Growing demand for durable, maintenance-free power sources across sectors such as aerospace, defense, healthcare, and industrial monitoring is motivating manufacturers to explore novel materials, improved device architectures, and cutting-edge technologies. This focus on innovation and product enhancement is shaping a highly competitive market where technological advancement is a key differentiator.

Key Industry Developments

- In February 2026, Australian company entX, collaborating with the University of Adelaide, developed GenX, a next-generation betavoltaic nuclear battery that uses additive manufacturing to stack ultra-thin layers of metals, oxides, and semiconductors, achieving unprecedented power density in a compact form.

- In September 2025, researchers from the University of Ottawa and Canadian Nuclear Laboratories developed three standardized "figures of merit “capture efficiency, gain, and gain efficiency to benchmark and compare betavoltaic battery performance across technologies.

- In May 2025, researchers at the Daegu Gyeongbuk Institute of Science and Technology (DGIST) developed the world’s first next-generation perovskite betavoltaic cell by directly integrating a radioactive isotope electrode with a perovskite absorber layer, achieving stable long-term power output and improved energy conversion efficiency.

Companies Covered in Betavoltaic Device Market

- City Labs, Inc.

- Widetronix, Inc.

- JSC LUTCH

- BetaBatt, Inc.

- Qynergy Corporation

- Exide Technologies

- II-VI Marlow

- Comsol, Inc.

- Tesla Nanocoatings

- Northrop Grumman Corporation

- Thermo Fisher Scientific

- China General Nuclear Power Corporation (CGN)

- Curtiss-Wright Corporation

- Ultra Electronics Holdings

- Lockheed Martin Corporation

Frequently Asked Questions

The global betavoltaic device market is projected to reach US$ 188.0 million in 2026.

Expanding IoT deployments, demand for maintenance-free power in remote sensors, and advances in semiconductor efficiency are driving the market.

The market is poised to witness a CAGR of 10.3% from 2026 to 2033.

Key market opportunities include long-duration applications in smart cities, medical implants, aerospace, and industrial automation, which offer substantial growth.

City Labs, Inc., Widetronix, Inc., JSC LUTCH, BetaBatt, Inc., and Qynergy Corporation are some of the key players in the market.