- Inks, Coatings, Adhesives & Sealants (ICAS)

- Electrically Conductive Adhesives Market

Electrically Conductive Adhesives Market Size, Share, and Growth Forecast 2026 - 2033

Electrically Conductive Adhesives Market by Product Type (Isotropic Conductive Adhesives, Anisotropic Conductive Adhesives), Resin Type (Epoxy-Based, Silicone-Based, Acrylic-Based, Polyurethane-Based, Others), Form (Paste, Liquid, Film, Tape), Application, End-user, and Regional Analysis, 2026 - 2033

Electrically Conductive Adhesives Market Size and Trend Analysis

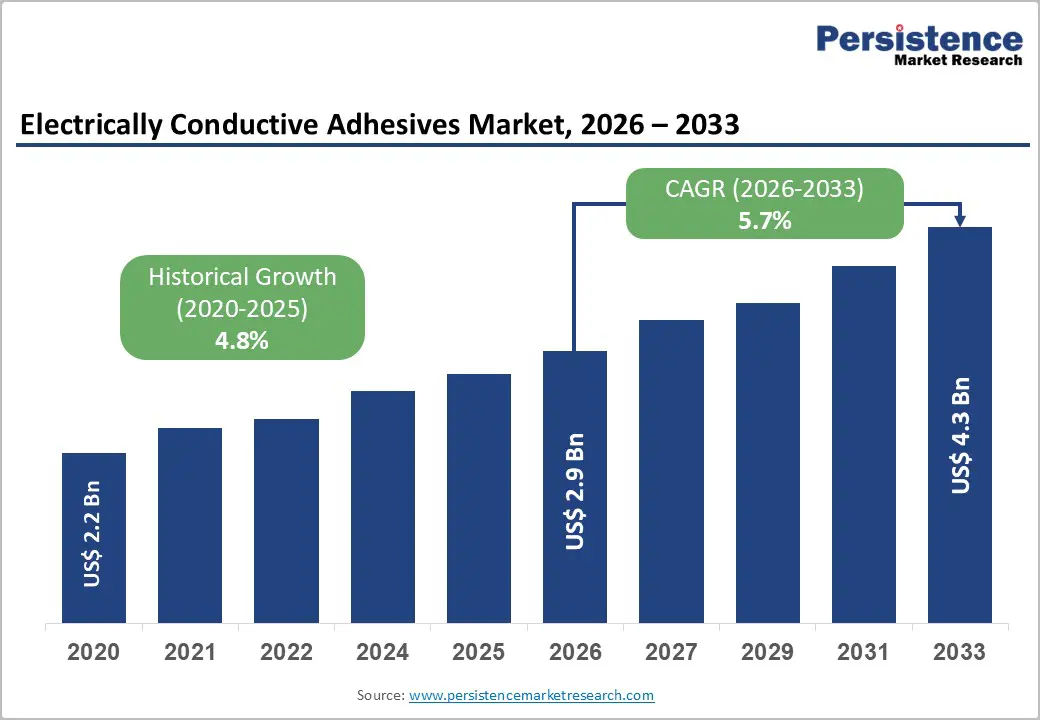

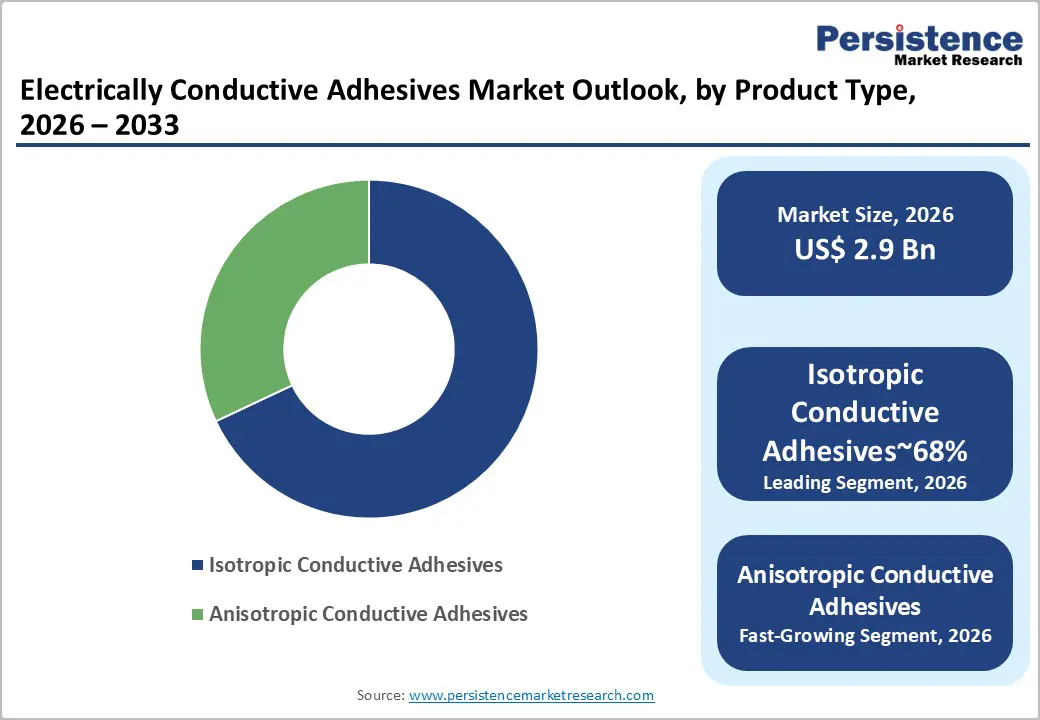

The global electrically conductive adhesives market size is likely to reach US$2.9 billion in 2026 and is expected to reach US$4.3 billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033.

It is driven by the miniaturization of electronic components, the global transition toward lead-free electronics assembly in compliance with the RoHS Directive, and rapidly expanding end-user demand from the electric vehicle, solar energy, advanced semiconductor packaging, and consumer electronics sectors.

Key Industry Highlights:

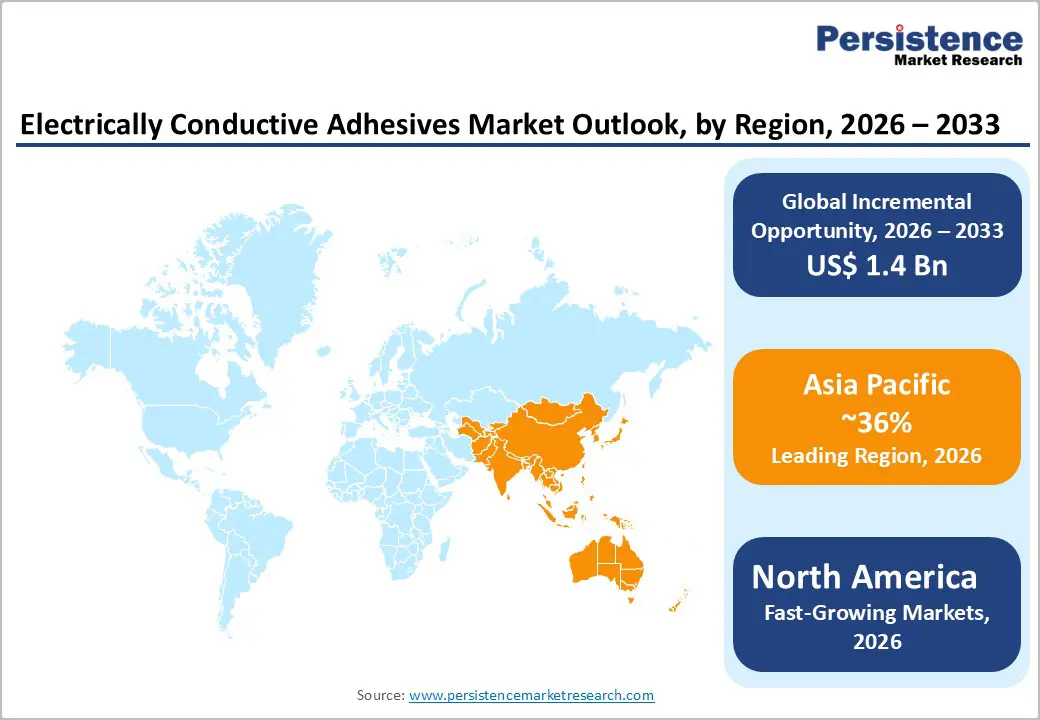

- Leading Region: Asia Pacific leads the electrically conductive adhesives market, holding a 36% share, anchored by China’s world’s largest electronics manufacturing ecosystem, Japan’s premium semiconductor and display industries, and South Korea’s Samsung, SK Hynix, and LG Display, which generate high-specification conductive adhesive procurement demand.

- Fastest-Growing Region: North America is the fastest-growing developed-market region, with a rising CAGR of 7.5%, propelled by the CHIPS Act’s US$ 52.7 billion semiconductor manufacturing investment, expanding EV power-electronics production, and the rise in aerospace and defense advanced electronics

- programs requiring certified conductive adhesive formulations.

- Dominant Segment: Isotropic Conductive Adhesives (ICA) lead the product type category with approximately 68% share, driven by their versatility across die attach, PCB bonding, LED, and solar cell applications and compatibility with standard SMT and dispensing production equipment globally.

- Fastest Growing Segment: Solar Cells / Photovoltaics are the fastest-growing segment, with IRENA reporting record 295 GW annual solar additions and HJT cell adoption requiring low-temperature conductive adhesive interconnection that cannot use conventional tin-lead soldering.

- Key Opportunity: Advanced semiconductor packaging, representing 40%+ of IC packaging revenue and growing, and HJT solar cell interconnection create the highest-value opportunities, where nano-silver sintering pastes and low-temperature ECA formulations command premium pricing with leading semiconductor and photovoltaic manufacturers.

Market Dynamics

Drivers - Global Electronics Miniaturization and RoHS-Driven Lead-Free Assembly Transition

The relentless trend toward miniaturization in consumer electronics, wearables, and advanced semiconductor packaging is creating fundamental demand for electrically conductive adhesives as alternatives to traditional tin-lead solder. As component pitch dimensions shrink below 100 microns in advanced chip packaging applications, the mechanical and thermal stresses of conventional soldering can damage delicate components. Electrically conductive adhesives that cure at significantly lower temperatures offer a critical technical advantage.

The EU RoHS Directive and its recast, combined with similar regulations in China and state-level frameworks in the U.S., have institutionalized the shift away from lead-containing solder. This regulatory tailwind, combined with the semiconductor industry’s projected global capital investment of over US$ 500 billion through 2030, per SEMI estimates, creates a sustained, compliance-driven demand foundation for conductive adhesive formulations.

Electric Vehicle Electronics and Automotive Semiconductor Integration

The accelerating electrification of the global automotive fleet is generating significant new demand for electrically conductive adhesives in automotive electronics, power module assembly, battery management systems, and advanced driver assistance systems (ADAS). Modern electric vehicles contain an estimated 3,000-5,000 semiconductor devices, compared to approximately 1,500 in conventional ICE vehicles, per IHS Markit analysis.

The International Energy Agency (IEA) reported that global EV sales exceeded 14 million units in 2023, and automotive-grade conductive adhesives must meet stringent AEC-Q100 qualification standards for reliability across wide temperature ranges and vibration conditions. Heat-resistant silicone-based and thermally stable epoxy formulations are seeing particularly strong adoption in power electronics and under-hood applications, directly expanding the premium automotive-grade conductive adhesive segment.

Restraints - Higher Cost Compared to Conventional Soldering Materials

Electrically conductive adhesives, particularly silver-filled formulations and anisotropic conductive films, carry significantly higher per-unit material costs compared to conventional tin-lead or SAC (Sn-Ag-Cu) solders.

Silver-filled epoxy conductive adhesives can cost 10-50 times more per unit volume than solder paste, constraining adoption in cost-sensitive, high-volume consumer electronics assembly. The commodity price volatility of silver, a primary filler in the majority of conductive adhesive formulations, introduces additional cost uncertainty for formulators and end-users, limiting expansion in price-competitive market segments.

Technical Performance Limitations vs. Solder in High-Current Applications

Despite their advantages in low-temperature processing and RoHS compliance, electrically conductive adhesives exhibit inherently lower electrical conductivity than metallic solder joints, typically achieving bulk resistivity of 10−4 to 10−3 Ω·cm, compared with 10−5 Ω·cm for solder. In high-current power electronics and RF applications, these conductivity gaps can limit performance.

Some conductive adhesive formulations exhibit contact resistance increases over time under thermal cycling and humidity conditions, raising long-term reliability concerns in mission-critical applications. These technical limitations require ongoing R&D investment, increasing product development costs and moderating rapid market expansion.

Opportunities - Solar Photovoltaic Cell Interconnection and Next-Generation Module Manufacturing

The global solar photovoltaic industry represents one of the most significant and rapidly growing addressable markets for electrically conductive adhesives. The transition from traditional tin-lead tabbing ribbon soldering to conductive adhesive-based cell interconnection, particularly for heterojunction (HJT) and perovskite solar cells that cannot withstand conventional soldering temperatures, is creating substantial new demand.

The International Renewable Energy Agency (IRENA) reports that global solar PV capacity additions reached a record 295 GW in 2022, with even faster growth projected through 2030. HJT solar cell production is growing particularly rapidly, with manufacturers including REC Group, Panasonic, and multiple Chinese tier-1 producers transitioning to HJT at scale. Each GW of HJT solar capacity requires hundreds of tonnes of conductive adhesive, representing a multi-billion-dollar cumulative procurement opportunity for specialized solar ECA formulators through the forecast period.

Advanced Semiconductor Packaging: Fan-Out WLP and 3D IC Integration

The semiconductor packaging industry’s transition toward advanced packaging architectures, including fan-out wafer-level packaging (FO-WLP), 3D IC stacking, chiplet integration, and through-silicon via (TSV) technologies, is creating significant and technically demanding demand for next-generation electrically conductive adhesive formulations. These advanced packaging approaches require conductive adhesives with ultra-fine pitch deposition capability, superior thermal conductivity for heat management, and exceptional reliability under extreme temperature cycling.

According to SEMI, advanced packaging currently represents over 40% of global IC packaging revenue and is growing faster than conventional packaging. Companies developing conductive adhesives specifically engineered for advanced packaging applications, including nano-silver sintering pastes and low-void, void-free epoxy underfills, can target premium-priced, high-specification procurement contracts with leading semiconductor manufacturers and OSAT providers.

Category-wise Analysis

By Product Type Insights

Isotropic Conductive Adhesives (ICA) dominate the product type segment, commanding approximately 68% of total market share. ICAs conduct electricity uniformly in all directions and are the workhorse conductive adhesive type for a broad range of applications including die attach, PCB component bonding, LED assembly, and solar cell interconnection. Their simpler formulation, typically consisting of silver flake or silver-coated particle fillers in an epoxy, silicone, or acrylic resin matrix, supports lower manufacturing costs and wider application versatility compared to anisotropic conductive adhesives (ACAs).

The global proliferation of surface-mount device assembly, LED lighting, and photovoltaic applications, all of which are primary ICA end-users, ensures sustained volume demand. Leading ICA manufacturers, including Henkel AG & Co. KGaA, Heraeus Electronics, and 3M Company, offer extensive ICA portfolios for electronics assembly.

By Resin Type Insights

Epoxy-based conductive adhesives are the leading resin type, accounting for approximately 54% of total market share. Epoxy resins provide the optimal combination of strong adhesion, excellent chemical resistance, a wide cure-temperature range, and compatibility with silver, copper, and carbon filler systems, making them the most versatile and widely adopted base material for electrically conductive adhesive formulations.

One- and two-component epoxy conductive adhesives are the standard die-attach and component-bonding materials across consumer electronics, automotive, and industrial electronic assembly. IPC (Association Connecting Electronics Industries) standards, including IPC-7527, specifically address epoxy-based conductive adhesive dispensing requirements, further institutionalizing their use in professional electronics manufacturing globally.

By Form Insights

Paste is the dominant form segment, accounting for approximately 57% of the total share in 2025. Conductive adhesive pastes are the most versatile and widely deployable form factor, compatible with screen printing, stencil printing, syringe dispensing, and jet dispensing application methods used across PCB assembly, solar cell tabbing, LED manufacturing, and semiconductor packaging.

The paste form’s compatibility with standard SMT (Surface Mount Technology) production equipment, including stencil printers and dispensing robots already installed at electronics manufacturing facilities globally, minimizes process change requirements for manufacturers transitioning from solder to conductive adhesive assembly. Silver-filled conductive paste formulations from companies including Heraeus Electronics, Henkel’s LOCTITE range, and Dow Inc. lead the paste segment across both high-volume electronics and specialty applications.

By Application Insights

Semiconductor Packaging is the leading application segment, representing approximately 28% of total market share. Die attach, the process of bonding semiconductor chips to substrates or lead frames, is one of the most technically critical and highest-value applications for electrically conductive adhesives. As die sizes shrink and power densities increase in advanced semiconductor packages, the thermal and electrical performance requirements of die attach adhesives escalate.

SEMI’s annual semiconductor equipment and materials forecast consistently identifies die attach materials as among the highest-value specialty material categories in semiconductor manufacturing. The transition to advanced packaging architectures, including multi-die modules, 3D stacking, and power semiconductor packages, is further expanding the technical specifications and per-unit material value of conductive adhesive die attach applications.

By End-user Insights

Electronics & Semiconductor is the dominant end-user segment, accounting for approximately 43% of the total market share. This segment encompasses the full spectrum of consumer electronics, professional electronics, and semiconductor manufacturing applications, from smartphone and tablet assembly to server and networking equipment, from LED backlighting to advanced integrated circuit packaging.

The global consumer electronics industry’s sustained demand for thinner, lighter, and higher-performing devices continuously drives the adoption of conductive adhesives in applications where conventional soldering cannot meet miniaturization, thermal, or flexibility requirements. The Consumer Technology Association (CTA) consistently reports that annual global consumer technology product revenues exceed US$ 1 trillion, reflecting the enormous and diverse electronics manufacturing ecosystem that drives consistent demand for conductive adhesives.

Regional Insights

North America Electrically Conductive Adhesives Market Trends

North America is a leading market for electrically conductive adhesives, anchored by the United States’ substantial semiconductor design and manufacturing ecosystem, advanced aerospace and defense electronics sector, and growing EV and renewable energy industries. The CHIPS and Science Act’s US$ 52.7 billion commitment to domestic semiconductor manufacturing is directly stimulating investment in advanced packaging facilities that require sophisticated conductive adhesive materials. U.S.-headquartered conductive adhesive manufacturers, including Dymax Corporation, Master Bond Inc., and Creative Materials Inc., serve both domestic and export markets from technology-advanced formulation capabilities.

The U.S. regulatory environment, including California’s Proposition 65 chemical disclosure requirements and EPA hazardous material standards, alongside federal DoD specifications for aerospace and defense electronics, creates compliance-driven demand for high-performance, certified conductive adhesive formulations. The aerospace and defense sector’s adoption of advanced electronics packaging for radar, satellite, and avionics applications represents a premium demand segment for highly reliable, thermally and electrically characterized conductive adhesive systems manufactured to MIL-STD and AS9100 quality standards.

Europe Electrically Conductive Adhesives Market Trends

Europe is a technically demanding, innovation-driven electrically conductive adhesives, shaped by the EU RoHS Directive, the REACH Regulation, and the EU Chips Act’s ambition to double the EU’s global semiconductor market share to 20% by 2030. Germany is the dominant market, home to major conductive adhesive manufacturers, including Henkel’s electronics adhesives division, DELO Industrie Klebstoffe GmbH & Co. KGaA, and Panacol-Elosol GmbH, as well as world-class automotive electronics OEMs such as Bosch, Continental, and Infineon, which drive premium automotive-grade adhesive demand.

The United Kingdom contributes to demand from its aerospace (Rolls-Royce, BAE Systems) and advanced electronics sectors. France’s defense and space electronics industries (Thales, Airbus Defense & Space) require radiation-hardened and thermally stable conductive adhesive formulations. The EU’s Green Deal Industrial Plan is accelerating solar PV deployment and EV adoption across Europe, expanding the regional addressable market for conductive adhesives in photovoltaic cell interconnection and automotive power electronics, positioning Europe as a high-quality, sustainability-driven demand center through the forecast period.

Asia Pacific Electrically Conductive Adhesives Market Trends

Asia Pacific is the largest and fastest-growing regional market for electrically conductive adhesives, accounting for the dominant share of global demand driven by the region’s concentration of electronics manufacturing, semiconductor fabrication, and photovoltaic production. China is the undisputed volume leader, housing the world’s largest electronics contract manufacturing ecosystem, anchored by companies including Foxconn, Luxshare, and Pegatron, and the world’s largest solar PV manufacturing base. China’s RoHS (GB/T 26572-2011) regulations align with EU RoHS in driving lead-free assembly adoption, directly boosting demand for conductive adhesives.

Japan is a technically sophisticated market for premium conductive adhesive formulations, supported by world-class electronics manufacturers, including Sony, Murata, TDK, and Kyocera, that require high-specification materials. South Korea’s semiconductor and display manufacturing giants, Samsung Electronics, SK Hynix and LG Display, generate significant conductive adhesive procurement for advanced packaging and display panel bonding. India’s rapidly growing electronics manufacturing sector, supported by the Production Linked Incentive (PLI) scheme for electronics, and ASEAN’s expanding semiconductor and electronics assembly industries are creating fast-growing incremental demand for conductive adhesive materials across the broader region.

Competitive Landscape

The global electrically conductive adhesives market is moderately consolidated, led by multinational chemical and specialty materials companies including Henkel, 3M, Dow, and Heraeus Electronics that hold strong market positions through extensive product portfolios, global technical service networks, and close customer co-development relationships with semiconductor and electronics OEMs.

Key competitive differentiators include formulation chemistry expertise, particle size and morphology optimization, specific end-user application qualification (AEC-Q, IPC, MIL-STD), and application process support capabilities. Emerging trends include the development of nano-silver sintering pastes for high-power semiconductor packaging, bio-based and halogen-free formulations for sustainability compliance, and application-specific customization services that command premium pricing from high-specification customers.

Key Developments:

- March 2025: Henkel AG & Co. KGaA launched its LOCTITE ECCOBOND advanced silver sintering paste series for high-power semiconductor die attach applications, targeting SiC and GaN power modules for EV inverters and industrial power electronics requiring superior thermal management.

- October 2024: Heraeus Electronics introduced a new low-temperature curing isotropic conductive adhesive series for heterojunction solar cell (HJT) tabbing applications, enabling cell interconnection at temperatures below 150°C to preserve cell efficiency in next-generation photovoltaic module manufacturing.

- May 2024: DELO Industrie Klebstoffe GmbH & Co. KGaA expanded its anisotropic conductive adhesive portfolio for fine-pitch display panel bonding applications, targeting OLED and micro-LED display manufacturers in China, South Korea, and Japan requiring sub-50 micron pitch interconnection solutions.

Global Electrically Conductive Adhesives Market Report -Key Insights & Scope

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 2.2 Bn |

| Current Market Value (2026) | US$ 2.9 Bn |

| Projected Market Value (2033) | US$ 4.3 Bn |

| CAGR (2026 - 2033) | 5.7% |

| Leading Region | Asia Pacific, 36% share |

| Dominant Equipment Type | Isotropic Conductive Adhesives, 68% share |

| Top-ranking End-userr | Electronics & Semiconductor, 43% |

| Incremental Opportunity | US$ 1.4 Bn |

Companies Covered in Electrically Conductive Adhesives Market

- 3M Company

- Henkel AG & Co. KGaA

- Dow Inc.

- H.B. Fuller Company

- Panacol-Elosol GmbH

- Heraeus Electronics

- Parker-Hannifin Corporation

- Permabond LLC

- Dymax Corporation

- Master Bond Inc.

- MG Chemicals Ltd.

- Nagase ChemteX Corporation

- Creative Materials Inc.

- Aremco Products Inc.

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Sumitomo Bakelite Co., Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Lord Corporation

Frequently Asked Questions

The global Electrically Conductive Adhesives Market is projected to reach US$ 4.3 Billion by 2033, expanding from US$ 2.9 Billion in 2026 at a CAGR of 5.7% during the 2026 - 2033 forecast period. This accelerates from a historical CAGR of 4.8% between 2020 and 2025, driven by electronics miniaturization, RoHS compliance requirements, and expanding solar PV and EV semiconductor demand.

The primary growth drivers are global electronics miniaturization requiring low-temperature assembly below solder’s thermal limits, EU and China RoHS directives mandating lead-free assembly transitions, and the EV sector’s expanding semiconductor content (3,000-5,000 devices per EV versus 1,500 in ICE vehicles), driving demand for automotive-grade thermally stable conductive adhesive formulations.

Isotropic Conductive Adhesives (ICA) lead the product type category with approximately 68% share. Their dominance reflects universal applicability across die attach, PCB assembly, LED bonding, and solar cell interconnection, combined with compatibility with standard SMT stencil printing and dispensing equipment widely deployed in global electronics manufacturing facilities.

Asia Pacific leads the global Electrically Conductive Adhesives Market, driven by China’s world’s largest electronics manufacturing base, Japan’s premium semiconductor and display industries, and South Korea’s Samsung Electronics, SK Hynix, and LG Display, generating high-volume, high-specification conductive adhesive procurement. The region accounts for the majority of global electronics assembly and solar PV manufacturing activity.

The highest-value opportunities are HJT solar cell interconnection, growing with IRENA’s record 295 GW annual solar additions requiring low-temperature conductive adhesive tabbing, and advanced semiconductor packaging representing 40%+ of IC packaging revenue, where nano-silver sintering pastes for SiC/GaN power devices command significant premium pricing from EV and industrial power electronics manufacturers.

The key market participants include 3M Company, Henkel AG & Co. KGaA, Dow Inc., H.B. Fuller Company, Panacol-Elosol GmbH, Heraeus Electronics, Parker-Hannifin Corporation, Permabond LLC, Dymax Corporation, Master Bond Inc., MG Chemicals Ltd., Nagase ChemteX Corporation, Creative Materials Inc., Aremco Products Inc., and DELO Industrie Klebstoffe GmbH & Co. KGaA.