- Inks, Coatings, Adhesives & Sealants (ICAS)

- Polyurethane Coatings Market

Polyurethane Coatings Market Size, Share, and Growth Forecast, 2026 - 2033

Polyurethane Coatings Market by Technology (Solvent-borne, Water-borne, Others), End-user (Automotive, Construction, Others), Substrate, and Regional Analysis for 2026 - 2033

Polyurethane Coatings Market Size and Trends Analysis

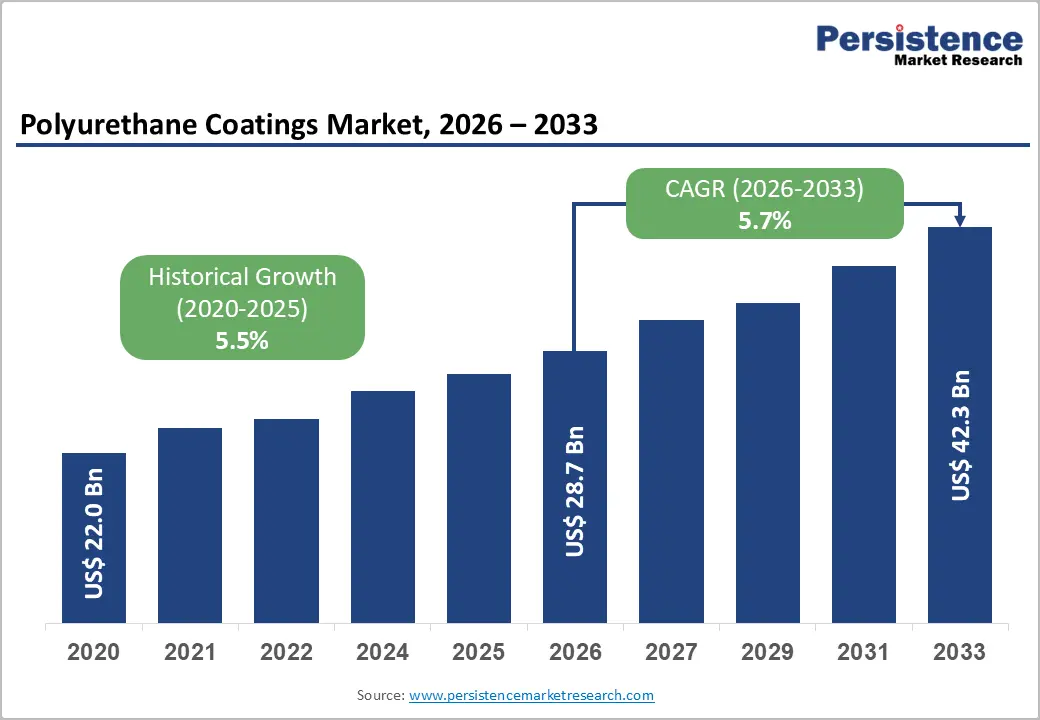

The global polyurethane coatings market size is likely to be valued at US$28.7 billion in 2026 and is expected to reach US$42.3 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033, driven by tightening environmental regulations, increasing adoption of low-emission coating technologies, and rising demand for high-performance protective solutions.

The market outlook remains stable, with growth anchored in performance optimization, regulatory compliance, and lifecycle cost efficiency.

Key Industry Highlights:

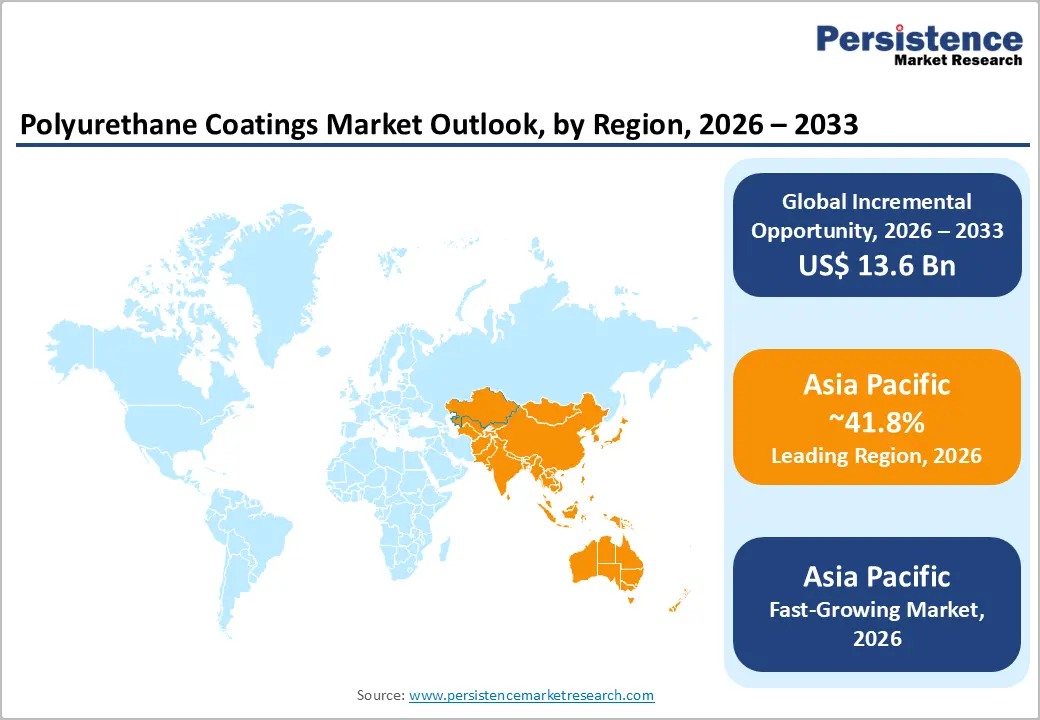

- Leading Region: Asia Pacific is projected to account for approximately 41.8% of the market share, driven by strong industrialization, infrastructure expansion, and high automotive production across China, India, and Southeast Asia.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by rapid urbanization, increasing manufacturing investments, and rising demand for cost-efficient and high-performance coatings.

- Investment Plans: Leading companies are actively investing in low-VOC, water-borne, and high-solids polyurethane technologies, along with expanding production capacities and distribution networks in emerging Asia Pacific markets to strengthen regional presence and meet regulatory requirements.

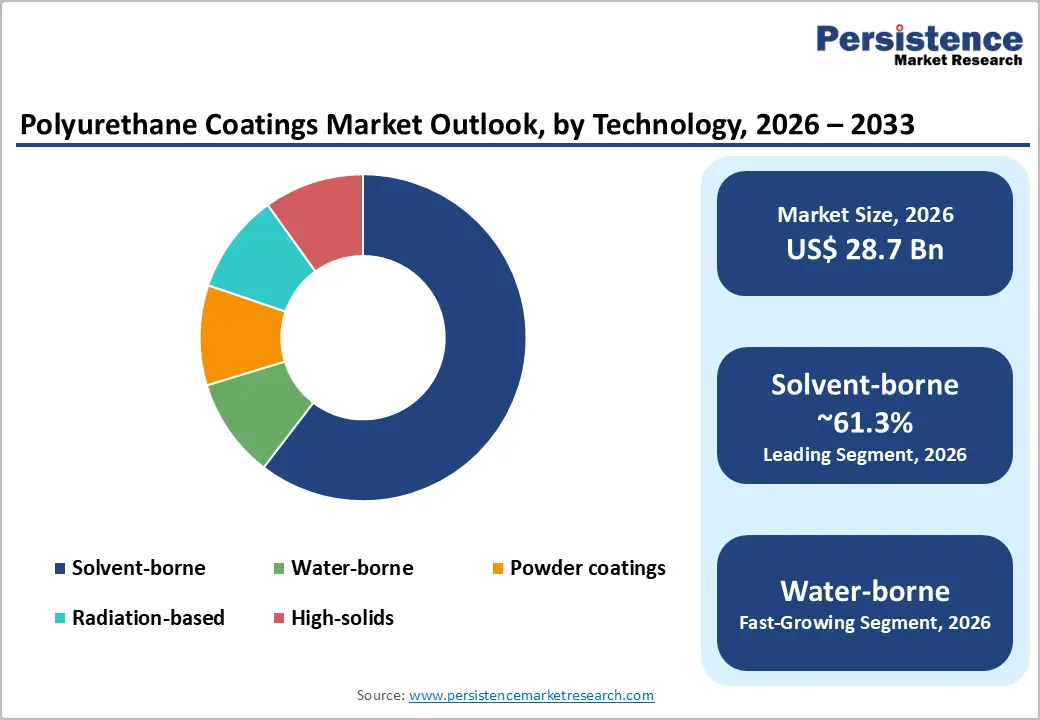

- Dominant Technology: Solvent-borne technology remains the dominant segment, holding an anticipated 61.3% market share, due to its superior performance characteristics and strong presence in industrial and automotive applications.

- Leading End-user: The automotive segment leads with an anticipated 33.7% share, supported by high global vehicle production and the continued demand for durable, high-performance coating systems.

| Key Insights | Details |

|---|---|

| Polyurethane Coatings Market Size (2026E) | US$28.7 Bn |

| Market Value Forecast (2033F) | US$42.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

DRO Analysis

Driver Analysis - Regulatory Pressure Accelerating Transition toward Low-VOC Technologies

Stringent environmental regulations in developed markets are reshaping the polyurethane coatings landscape. Regulatory frameworks targeting volatile organic compound (VOC) emissions have imposed strict limits on solvent-based formulations, particularly in architectural and industrial coatings. These policies are driving the adoption of water-borne, high-solids, and solvent-free polyurethane coatings, which offer compliance without compromising performance. As a result, manufacturers are prioritizing reformulation strategies to meet evolving standards. This regulatory shift is not only influencing product portfolios but also redefining competitive positioning, favoring companies with advanced R&D capabilities and sustainable product offerings.

Expansion of Construction and Infrastructure Activities

Global construction activity continues to provide a strong demand base for polyurethane coatings. Significant investments in residential, commercial, and infrastructure projects are increasing the need for protective and decorative coatings used in flooring, waterproofing, and structural applications. Polyurethane coatings are valued for their abrasion resistance, chemical durability, and long service life, making them essential in high-performance construction environments. The growth of infrastructure modernization programs and urbanization trends is further strengthening demand, particularly in developing economies where large-scale construction projects are ongoing.

Sustained Demand from Automotive and Industrial Manufacturing

The automotive sector remains a key consumption driver, supported by high global vehicle production volumes and increasing demand for durable coatings in OEM and refinish applications. Polyurethane coatings provide excellent gloss retention, weather resistance, and impact protection, making them indispensable in automotive finishing systems. Industrial manufacturing also contributes significantly, as these coatings are widely used in machinery, equipment, and protective applications. Technological advancements, including faster curing systems and energy-efficient coatings, are enhancing productivity and reinforcing demand across these sectors.

Restraint Analysis - High Compliance and Reformulation Costs

Adhering to stringent environmental regulations requires continuous investment in product reformulation, testing, and certification. Developing low-VOC and environmentally compliant coatings often involves higher R&D expenditure and complex manufacturing adjustments. These costs can strain profit margins, particularly for smaller manufacturers with limited resources. The need for ongoing compliance also increases operational complexity, potentially slowing product innovation cycles and market entry timelines.

Volatility in Raw Material Prices

Polyurethane coatings rely on key raw materials such as isocyanates, polyols, and specialty additives, which are subject to price fluctuations driven by global supply-demand dynamics and energy costs. This volatility creates uncertainty in cost structures and can compress margins if price increases cannot be passed on to customers. Supply chain disruptions further exacerbate the challenge, impacting production planning and inventory management. Manufacturers must adopt strategic sourcing and pricing strategies to mitigate these risks.

Opportunity Analysis - Growth of Water-Borne and Solvent-Free Technologies

The transition toward environmentally sustainable coatings presents a significant growth opportunity. Water-borne and solvent-free polyurethane coatings are gaining traction due to their low emissions, improved safety profiles, and regulatory compliance. Advances in formulation technology are enabling these coatings to match or exceed the performance of traditional solvent-based systems. This shift is particularly prominent in construction, industrial maintenance, and automotive refinish applications, where sustainability and efficiency are increasingly prioritized.

Rising Demand in the Asia Pacific Markets

Asia Pacific represents the most dynamic growth region, driven by rapid industrialization, urbanization, and expanding manufacturing capabilities. Strong growth in automotive production, infrastructure development, and industrial activities is creating substantial demand for polyurethane coatings. The region’s cost advantages and large consumer base make it an attractive destination for capacity expansion and market penetration. Companies investing in localized production and distribution networks are well-positioned to capitalize on this opportunity.

Innovation in Performance-Enhanced Coatings

Emerging innovations are shifting the focus from basic functionality to performance optimization and lifecycle efficiency. Developments in fast-curing, energy-efficient, and corrosion-resistant coatings are addressing evolving customer needs. These advanced solutions reduce application time, lower operational costs, and extend asset lifespan, creating value for end-users. The ability to deliver differentiated performance is becoming a key competitive advantage, enabling manufacturers to command premium pricing and strengthen market positioning.

Category-wise Analysis

Technology Insights

Solvent-borne polyurethane coatings are expected to dominate the market, holding 61.3% share in 2026, due to their proven performance characteristics and widespread adoption across demanding industrial and automotive applications. These coatings deliver superior film formation, high gloss retention, strong adhesion, and excellent resistance to chemicals, UV exposure, and abrasion, making them the preferred choice in heavy-duty environments. Their extensive installed base across OEM automotive lines, industrial machinery, and marine coatings reinforces their leadership position. For instance, solvent-borne systems are widely used in automotive OEM clearcoats and industrial protective coatings for steel structures, where consistent performance under extreme conditions is critical. However, increasing regulatory pressure on VOC emissions is gradually limiting their growth potential, particularly in North America and Europe, prompting manufacturers to optimize formulations or transition toward hybrid technologies.

Water-borne polyurethane coatings are anticipated to register the fastest growth, driven by stringent environmental regulations and increasing demand for sustainable coating solutions. These coatings offer low VOC emissions, reduced odor, improved workplace safety, and easier compliance with environmental standards, making them highly attractive across multiple industries. Technological advancements have significantly enhanced their durability, drying time, and resistance properties, enabling them to compete with solvent-borne alternatives. For example, water-borne systems are increasingly used in architectural coatings, wood finishes, and automotive refinish applications, where regulatory compliance and user safety are key considerations. Their adoption is expanding rapidly in construction and industrial maintenance sectors, particularly in indoor applications and urban environments where emission control is critical.

End-use Insights

The automotive sector is anticipated to be the largest end-use segment, anticipated to hold 33.7% share in 2026, supported by high global vehicle production and the critical need for high-performance coatings in both OEM and refinish applications. Polyurethane coatings are extensively used in vehicle body coatings, clearcoats, primers, and protective layers, providing durability, corrosion resistance, and a superior aesthetic finish. Their ability to maintain gloss and color stability under harsh environmental conditions makes them indispensable in automotive manufacturing. For example, polyurethane coatings are commonly applied in passenger vehicles, commercial fleets, and specialty vehicles, where performance and appearance are equally important. Continuous innovation in coating technologies, such as low-energy curing systems and faster drying formulations, is further enhancing efficiency and reducing operational costs for manufacturers and service providers.

The construction sector is anticipated to be the fastest-growing end-use segment, driven by rapid urbanization, infrastructure expansion, and increasing investments in residential and commercial projects. Polyurethane coatings are widely used in flooring systems, waterproofing membranes, bridge coatings, and concrete protection, where durability and long-term performance are essential. Their resistance to abrasion, chemicals, moisture, and temperature fluctuations makes them ideal for high-traffic and harsh environments. For instance, polyurethane coatings are increasingly applied in industrial warehouses, commercial buildings, parking structures, and public infrastructure projects. The growing emphasis on sustainable construction materials and lifecycle cost reduction is further accelerating adoption, creating significant opportunities for manufacturers offering environmentally compliant and high-performance solutions.

Regional Insights

North America Polyurethane Coatings Market Trends - Low-VOC Innovation & Infrastructure-Driven Protective Coatings Demand

North America is a mature yet highly influential market characterized by strong demand from construction, automotive, and industrial sectors. The U.S. leads the region, supported by significant construction spending and a well-established manufacturing base. Regulatory frameworks focusing on VOC emissions are driving the adoption of environmentally compliant coatings, encouraging innovation in low-emission technologies. Major players such as Sherwin-Williams and PPG Industries continue to invest in low-VOC and high-solids polyurethane systems, particularly for infrastructure and industrial maintenance.

For example, Sherwin-Williams has expanded its protective and marine coatings portfolio with solvent-free and corrosion-resistant technologies, targeting oil & gas and energy infrastructure. Similarly, Axalta Coating Systems has introduced fast-curing, low-energy automotive refinish coatings, improving productivity for body shops. These developments reinforce the region’s focus on efficiency, compliance, and lifecycle cost reduction, while ongoing infrastructure modernization programs continue to generate steady demand for advanced polyurethane coatings.

Europe Polyurethane Coatings Market Trends - Sustainability-Driven Shift to Water-Borne & Powder Coatings

Europe represents a technologically advanced market where stringent environmental regulations play a central role in shaping product development. Countries such as Germany, the U.K., France, and Spain remain key contributors due to their strong industrial and construction activities. The region’s regulatory environment is accelerating the transition toward water-borne, powder, and low-emission polyurethane coatings, particularly in architectural and industrial applications.

Companies such as AkzoNobel and BASF are actively investing in sustainable coating technologies and bio-based raw materials to align with European environmental standards. For instance, AkzoNobel has been expanding its powder coatings portfolio, which eliminates VOC emissions entirely and is gaining traction in metal and architectural applications. Meanwhile, Sika continues to strengthen its position in construction-related coatings through acquisitions and product innovation in flooring and protective systems. These developments highlight how Europe’s emphasis on sustainability and regulatory compliance is driving innovation-led growth, even in a relatively mature market.

Asia Pacific Polyurethane Coatings Market Trends - High-Growth, Industrial Expansion & Cost-Driven Production Hub

Asia Pacific is expected to be the leading region in the polyurethane coatings market, commanding approximately 41.8% share in 2026, and is also the fastest-growing region. Rapid industrialization, urbanization, and expanding automotive production are key growth drivers. China, India, Japan, and ASEAN countries are major contributors, each offering distinct demand dynamics. The region’s manufacturing advantages, including cost efficiency and large-scale production capabilities, continue to attract significant investments from both global and regional players. Companies such as Asian Paints and Nippon Paint Holdings are expanding production capacity and distribution networks to meet rising demand in the construction and automotive sectors.

For example, Asian Paints has strengthened its industrial and automotive coatings segment in India through joint ventures and localized manufacturing, supporting infrastructure growth. Similarly, Kansai Paint has expanded its footprint across Southeast Asia, targeting automotive OEM and refinish markets. In China, domestic and international manufacturers are investing in high-performance and eco-friendly coating technologies to comply with tightening environmental norms. These developments collectively reinforce Asia Pacific’s position as a high-growth, investment-driven market, where scale, localization, and cost efficiency define competitive advantage.

Competitive Landscape

The global polyurethane coatings market exhibits a moderately consolidated structure at the top, with fragmentation across regional and niche players. Leading multinational companies dominate high-performance and technologically advanced segments, leveraging strong R&D capabilities and global distribution networks. Smaller and regional players compete in specific applications and local markets, often focusing on cost competitiveness and customization.

The competitive environment is defined by continuous innovation, regulatory compliance, and strategic expansion initiatives. Key players are focusing on innovation, sustainability, and market expansion as core strategies. Emphasis is placed on developing low-emission coatings, enhancing product performance, and expanding presence in high-growth regions. Strategic partnerships, mergers, and R&D investments are critical for maintaining competitive advantage and addressing evolving market demands.

Key Industry Developments:

- In November 2025, AkzoNobel and Axalta Coating Systems announced a definitive agreement to merge in an all-stock deal, creating a global coatings leader with an enterprise value of approximately US$25 billion, aimed at strengthening innovation capabilities, expanding global reach, and achieving significant cost synergies.

- In October 2025, BASF completed the sale of its Brazilian decorative paints business to Sherwin-Williams for approximately US$1.15 billion, as part of its portfolio optimization strategy to focus on higher-value coatings segments and streamline operations.

Companies Covered in Polyurethane Coatings Market

- AkzoNobel

- Sherwin-Williams

- PPG Industries

- Axalta Coating Systems

- BASF

- Nippon Paint Holdings

- Kansai Paint

- Asian Paints

- Jotun

- Hempel

- Sika

- RPM International

- Covestro

- Wacker Chemie

- Allnex

- Berger Paints

Frequently Asked Questions

The global polyurethane coatings market is estimated to be valued at US$28.7 billion in 2026.

The polyurethane coatings market is projected to reach US$42.3 billion by 2033.

Key trends include the shift toward low-VOC and water-borne technologies, increasing adoption of high-performance and corrosion-resistant coatings, and rising focus on sustainable and energy-efficient coating solutions.

The solvent-borne technology segment leads the market, holding an anticipated 61.3% share, supported by its strong performance characteristics and widespread industrial use.

The polyurethane coatings market is expected to grow at a CAGR of 5.7% from 2026 to 2033.

Major players include AkzoNobel, Sherwin-Williams, PPG Industries, Axalta Coating Systems, and BASF.