- Inks, Coatings, Adhesives & Sealants (ICAS)

- Asia Pacific Waterproofing Chemicals Market

Asia Pacific Waterproofing Chemicals Market Size, Share, and Growth Forecast 2026 - 2033

Asia Pacific Waterproofing Chemicals Market by Product Type (Bitumen, PVC, EPDM, TPO, PTFE, Silicone, Acrylic Polymer, SBR - Styrene-Butadiene, Others), by Technology (Membrane Systems, Liquid Applied Systems, Cementitious Waterproofing, Injection Grouting Systems, Integral Systems), by Application, by End-Use, and Country Analysis for 2026 - 2033

Asia Pacific Waterproofing Chemicals Market Size and Trend Analysis

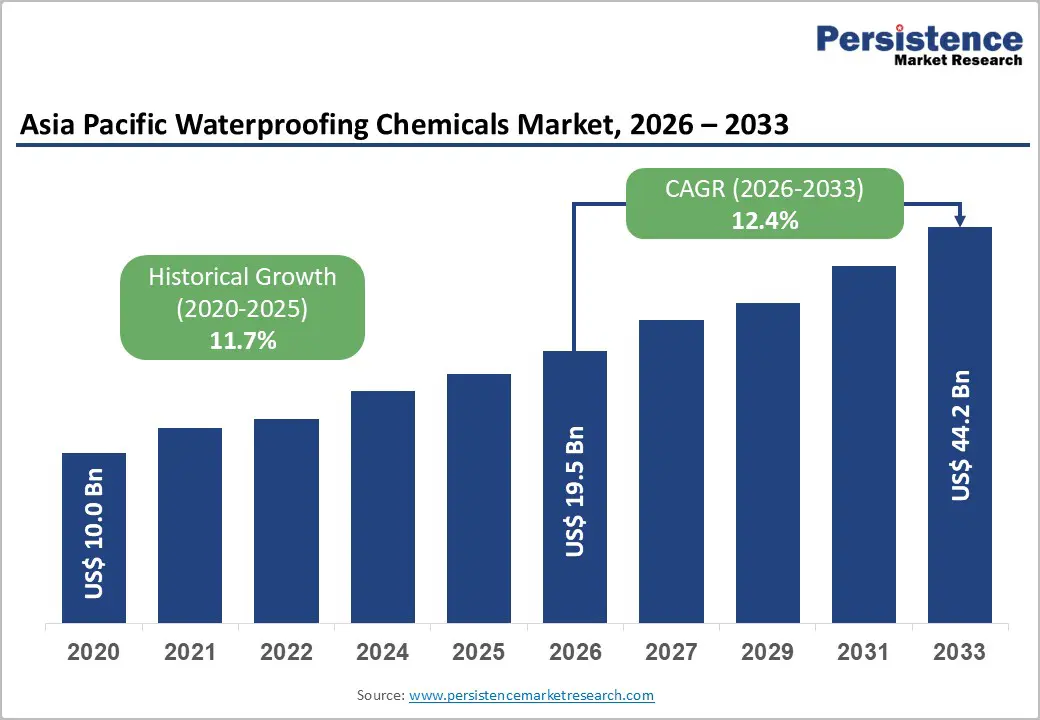

The Asia-Pacific waterproofing chemicals market size is supposed to be valued at US$19.5 billion in 2026 and is projected to reach US$44.2 billion by 2033, growing at a CAGR of 12.4% between 2026 and 2033.

The Asia Pacific waterproofing chemicals market is the world's fastest-growing regional waterproofing chemicals geography, driven by the region's unprecedented urban infrastructure construction scale, escalating climate-resilience investment mandates across flood-prone coastal and riverine cities, and the progressive adoption of high-performance waterproofing systems in mega-infrastructure programs spanning metro rail tunnels, expressway bridges, large-scale housing developments, and water management infrastructure.

Key Market Highlights

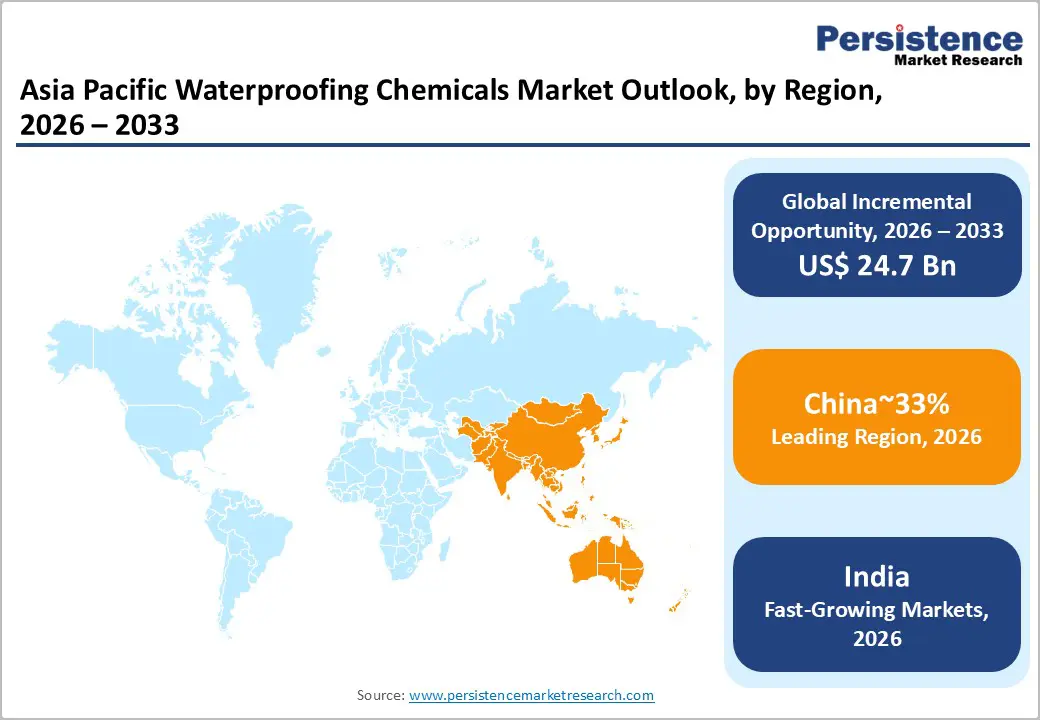

- Leading Country: China leads the Asia Pacific waterproofing chemicals market, anchored by NBS-documented RMB 31.6 trillion annual construction output, CACRTA's metro rail network exceeding 9,000 km requiring tunnel lining waterproofing procurement, CWA's progressive national quality standard upgrading, and the 14th Five-Year Plan urban renewal mandate.

- Fastest Growing Country: India is the fastest-growing Asia Pacific Waterproofing Chemicals market, driven by NIP's US$1.4 trillion infrastructure investment, PMAY's 11.8 million homes sanctioned, MoHUA's metro rail expansion across 27 cities, generating above-12.4% CAGR national waterproofing chemical demand growth.

- Dominant Technology: Membrane Systems dominate the Technology segment with approximately 42% revenue share, anchored by JWIA's documented Japanese membrane specification dominance, Sika AG's Sikaplan®/Sarnafil®/SikaProof® Asia Pacific OEM infrastructure project approvals.

- Dominant End-user: Infrastructure End-Use is the dominant segment with approximately 38% revenue share, confirmed by ADB's US$26 trillion Asia Pacific investment requirement, China's metro rail 9,000 km tunnel procurement, India's US$1.4 trillion NIP waterproofing specification scale, and ASEAN nations' above-average infrastructure construction growth.

- Key Opportunity: China's urban renewal program and India's Smart Cities Mission waterproofing specification upgrade represent dual key opportunities, with China's MOHURD urban renewal targeting 40 billion m² of existing building stock, and India's NIP US$1.4 trillion multi-sector procurement.

| Key Insights | Details |

|---|---|

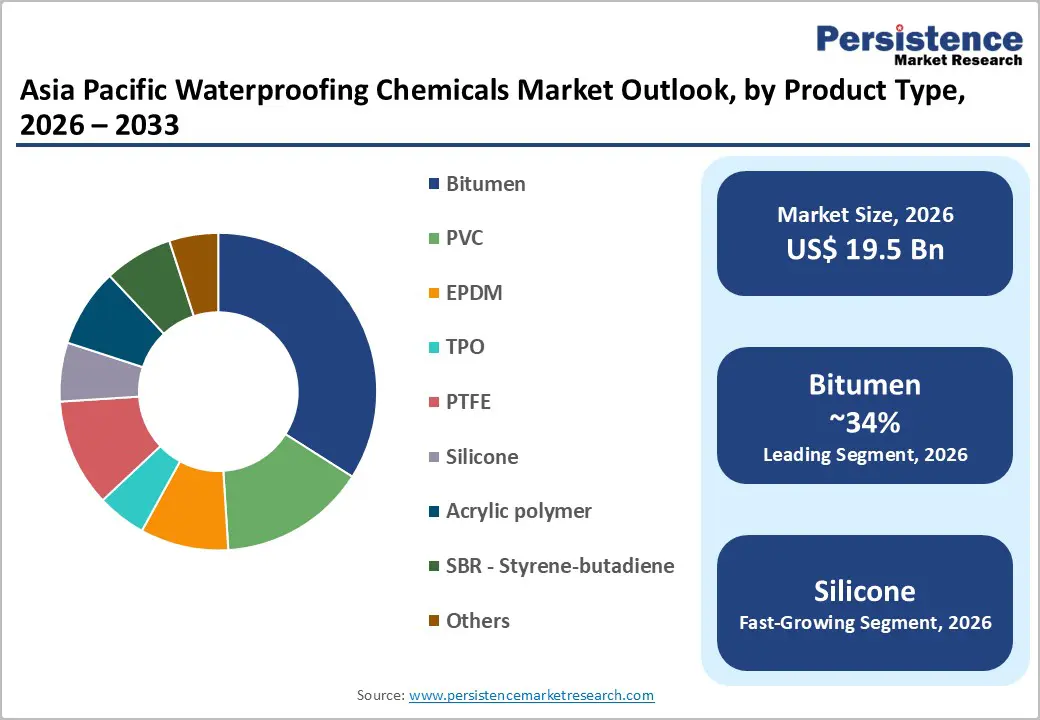

| Asia Pacific Waterproofing Chemicals Market Size (2026E) | US$ 19.5 Billion |

| Market Value Forecast (2033F) | US$ 44.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 12.4% |

| Historical Market Growth (2020 - 2025) | 11.7% |

DRO Analysis

Drivers - Asia Pacific's Urban Infrastructure Construction Scale and ADB-Documented Investment Mandate Sustaining Structural Waterproofing Demand

The Asian Development Bank (ADB)'s infrastructure investment needs assessment, estimating US$ 26 Trillion in regional infrastructure requirements through 2030, represents the foundational driver for the Asia Pacific Waterproofing Chemicals market, as every category of public infrastructure including metro rail tunnels, expressway bridges, water treatment plants, dams, flood control channels, port structures, and underground transit stations requires multi-layer waterproofing systems to ensure structural longevity, operational safety, and lifecycle cost efficiency.

China's Ministry of Housing and Urban-Rural Development (MOHURD) documents that China's urban construction output has consistently exceeded RMB 20 Trillion annually, with the country's rapidly expanding metro rail network, now spanning over 9,000 km across 55 cities per the China Urban Rail Transit Association (CACRTA), representing one of the world's most waterproofing-chemicals-intensive institutional procurement programs for tunnel lining membranes, injection grouting systems, and cementitious waterproofing treatments.

India's Ministry of Housing and Urban Affairs (MoHUA) documents sustained housing construction demand under the Pradhan Mantri Awas Yojana (PMAY) scheme, with over 11.8 million houses sanctioned through 2025, generating consistent residential waterproofing chemical procurement from Pidilite Industries Ltd. (headquartered in Mumbai, Maharashtra, India) through its Dr. Fixit waterproofing brand that commands market-leading specification adoption across Indian residential construction.

Climate Change Resilience Mandates and Flood Risk Management Infrastructure Investment, Accelerating Waterproofing Chemical Specification Upgrades

The Asia Pacific region bears the world's highest exposure to climate-driven flood, typhoon, and extreme rainfall events, with the UNESCAP's disaster risk documentation confirming that Asia accounts for approximately 45% of global economic losses from natural disasters annually. This growing climate risk is driving national government mandates for flood-resilient building standards, upgraded stormwater management infrastructure, coastal protection structures, and climate-adaptive urban design specifications that require above-standard chemical performance for waterproofing across residential, commercial, and infrastructure construction.

Japan's Ministry of Land, Infrastructure, Transport and Tourism (MLIT) has been progressively upgrading national building waterproofing standards, with its Housing Quality Assurance Act mandating waterproofing performance warranties for newly constructed residential buildings and driving specification of certified high-performance EPDM membrane systems, TPO roofing membranes, and liquid-applied polyurethane waterproofing coatings from Sika AG's Japan operations and Wacker Chemie AG's silicone-based waterproofing product portfolio.

Bangladesh's government-supported flood-resilient housing construction program and Vietnam's national coastal protection infrastructure investment, supported by ADB climate adaptation financing, represent additional Asia-Pacific policy-driven drivers of waterproofing chemicals demand, contributing to the region's above-average market growth trajectory through 2033.

Market Restraints

High Raw Material Input Cost Volatility, Particularly Bitumen, Polymer Dispersions, and EPDM, Constraining Manufacturer Margin Stability

Waterproofing chemicals are intensive formulations, with bitumen, modified bitumen, EPDM synthetic rubber, acrylic and polyurethane polymer dispersions, and Portland cement as the primary input cost components, collectively accounting for 50-70% of the manufacturing costs of waterproofing membranes and liquid-applied products. Bitumen prices, directly linked to crude oil refinery output documented by the International Energy Agency (IEA), are subject to significant crude oil price cycles, creating procurement cost volatility for bituminous membrane manufacturers across Asia Pacific.

Polymer dispersion pricing is similarly influenced by movements in ethylene and propylene feedstock prices, with sustained input cost inflation compressing waterproofing product manufacturer margins and creating price resistance in cost-sensitive mass housing segments where project developers prioritize the lowest-cost specification over premium waterproofing chemical performance.

Inconsistent Building Code Enforcement and Low Waterproofing Standard Compliance in Developing Economy Construction Markets Constraining Premium Product Adoption

Despite technically progressive national building waterproofing standards existing across most Asia Pacific construction markets, enforcement quality and contractor technical compliance capacity vary significantly, particularly in Vietnam, Indonesia, the Philippines, Bangladesh, and Pakistan, where construction industry regulatory oversight infrastructure is less mature.

The ASEAN Secretariat's construction standards harmonization working group has documented significant variation in national building code compliance monitoring across ASEAN member states, with inadequate waterproofing specification and substandard application quality in residential construction creating post-occupancy water damage failures that paradoxically slow specification-grade waterproofing chemical market development by eroding contractor and developer confidence in waterproofing chemical system reliability, despite the failures being attributable to poor application rather than product performance limitations.

Opportunity - China's Urban Renewal Program and Underground Infrastructure Expansion Creating Premium Membrane and Injection Grouting Procurement Surge

The Republic Government of China's urban renewal initiative, formalized under the 14th Five-Year Plan (2021 - 2025) with continuation commitments in the 15th Five-Year Plan framework, encompasses the large-scale renovation of aging urban building stock, including roof waterproofing replacement, basement and foundation waterproofing remediation, utility tunnel rehabilitation, and underground parking structure waterproofing remediation across China's tier-1 and tier-2 cities.

China's MOHURD documents that the country's urban renewal investment has been running at multi-trillion-RMB annual scales, with waterproofing chemicals among the highest-value construction chemical procurement categories within renovation programs targeting the approximately 40 billion m² of existing urban building stock requiring periodic waterproofing maintenance and renewal.

The China Waterproofing Association (CWA), the industry body representing Chinese waterproofing material manufacturers, contractors, and specification authorities, documents progressive tightening of national waterproofing material quality standards under GB/T national standards, with the transition from commodity-grade SBS modified bituminous membranes toward higher-performance self-adhesive, thermoplastic polyolefin (TPO), and pre-applied waterproofing membrane systems creating a premium product mix upgrade opportunity for BASF SE's MasterSeal waterproofing product family, Sika AG's Sika® Igolflex and Sika®-Combiflex membrane systems, and GCP Applied Technologies (headquartered in Cambridge, Massachusetts, USA) Preprufe® pre-applied waterproofing technology in China's underground construction market.

India's Smart Cities Mission and National Infrastructure Pipeline Creating Multi-Sector Waterproofing Chemical Demand Acceleration

The Government of India's National Infrastructure Pipeline (NIP), announcing infrastructure investment of INR 111 Lakh Crore (approximately US$ 1.4 Trillion) across 2019 - 2025 with continuation through subsequent investment cycles, encompasses mass housing, metro rail expansion, national highway construction, water supply and sewerage infrastructure, port development, and renewable energy facility construction programs that collectively represent one of Asia Pacific's most commercially significant multi-sector waterproofing chemicals procurement growth platforms.

The Ministry of Housing and Urban Affairs (MoHUA)'s Smart Cities Mission, targeting 100 smart city developments across India, mandates flood-resilient and climate-adaptive building and infrastructure design specifications that are progressively elevating waterproofing chemical quality standards from conventional cement-polymer coating applications toward high-performance liquid-applied polyurethane, cementitious crystalline, and self-adhesive membrane waterproofing systems in urban infrastructure project specifications.

Pidilite Industries Ltd. (headquartered in Mumbai, India), through its industry-dominant Dr. Fixit waterproofing brand with an estimated 40%+ domestic waterproofing market share, is the commercially best-positioned domestic waterproofing chemical company to capture above-average revenue growth from India's infrastructure investment scale-up. Fosroc International Limited (headquartered in Birmingham, UK) and Mapei S.p.A. (headquartered in Milan, Italy) serve the premium institutional infrastructure project waterproofing chemical procurement market in India through their established Indian technical sales and distribution operations.

Category-wise Analysis

By Product Type Insights

Bitumen leads the Asia Pacific waterproofing chemicals market by product type, commanding approximately 34% of total product type segment revenue in 2026, a dominant position reflecting bituminous waterproofing membranes' decades-established commercial standard for roof waterproofing, foundation waterproofing, tunnel lining, and below-grade structural waterproofing applications across the full spectrum of Asian construction sectors, from mass residential housing to institutional infrastructure. Modified bituminous membranes, including APP (Atactic Polypropylene) and SBS (Styrene-Butadiene-Styrene) polymer-modified variants, are the volume backbone of the Asia Pacific roof waterproofing specification, documented by the China Waterproofing Association (CWA) as the most widely installed waterproofing material category in Chinese residential and commercial construction.

The Bureau of Indian Standards (BIS) IS 1322 and IS 1580 standards governing bituminous waterproofing materials confirm bitumen's enduring specification foundation in Indian construction waterproofing applications. Acrylic Polymer waterproofing coatings account for approximately 18% of product type revenue, growing rapidly as liquid-applied systems are adopted for residential roof repair and wet-area waterproofing. EPDM holds approximately 12%, anchored in Japanese industrial roofing and premium residential waterproofing specifications.

By Technology Insights

Membrane systems lead the Asia Pacific waterproofing chemicals market by technology, commanding approximately 42% of total technology segment revenue in 2026, a dominant position anchored in membrane waterproofing's status as the global engineering standard for below-grade structural waterproofing, tunnel lining protection, bridge deck waterproofing, and flat roof waterproofing across the high-value institutional construction project categories where long-term waterproofing system integrity and lifecycle performance are primary specification criteria. The Japan Waterproofing Industry Association (JWIA), representing Japan's specialized waterproofing membrane manufacturers and contractors, documents that sheet-applied and torch-applied membrane systems account for the dominant share of Japanese commercial and infrastructure waterproofing specifications, reflecting Japan's technically advanced construction industry's preference for engineered, certified membrane solutions over liquid-applied alternatives in demanding structural waterproofing applications.

Sika AG's comprehensive membrane waterproofing portfolio, spanning Sikaplan® PVC membranes, Sarnafil® TPO membranes, and SikaProof® pre-applied waterproofing systems, is commercially active across China, India, Japan, and Southeast Asia, in line with premium infrastructure project specifications. Liquid Applied Systems holds approximately 28% of the technology segment revenue, growing as the fastest-rising technology category driven by ease of application, seamless coverage, and cost-competitive roof repair accessibility.

By Application Insights

Roofing & Walls leads the Asia Pacific Waterproofing Chemicals market by application, commanding approximately 35% of total application segment revenue in 2026, a dominant position reflecting roofing's status as the highest-volume waterproofing installation area across all building types in the Asia Pacific region, where the combination of intense monsoon rainfall, typhoon exposure, high humidity, and tropical UV radiation creates severe waterproofing performance demands that mandate high-quality membrane, liquid-applied, and cementitious waterproofing system specification from residential to institutional construction categories. China's MOHURD documents that approximately 2-3 billion m² of new building floor area is constructed annually, with roof waterproofing required on virtually every structure, generating the world's largest single-country roof waterproofing chemical procurement market.

India's Bureau of Indian Standards (BIS) IS 3036 and IS 15491 standards governing roof waterproofing compound specifications shape the Indian residential and commercial roofing waterproofing chemical procurement landscape, where Dr. Fixit by Pidilite Industries commands a dominant market share. Tunnel Linings hold approximately 16% of application revenue, growing rapidly with China's metro rail expansion, India's USBRL mountain tunnel program, and Southeast Asian urban underground transit development programs. Water & Waste Management Structures hold approximately 12%, driven by the Asia Pacific's expanding water infrastructure investment.

By End-user Insights

Infrastructure leads the Asia Pacific Waterproofing Chemicals market by end-use, commanding approximately 38% of total end-use segment revenue in 2026, a dominant position reflecting Asia Pacific's status as the world's most infrastructure-investment-intensive region, with the ADB's US$26 trillion regional investment requirement, China's metro rail network exceeding 9,000 km, India's National Infrastructure Pipeline of US$1.4 trillion, and Southeast Asian nations' above-average GDP growth-linked infrastructure construction collectively sustaining the highest per-annum institutional waterproofing chemical procurement volumes of any regional end-use category.

Infrastructure waterproofing applications, spanning tunnel lining membranes, bridge deck waterproofing, water treatment plant tank lining, dam face waterproofing, and underground station protection, require the highest-performance and highest-value waterproofing chemical systems, driving above-average revenue per square meter compared to residential or commercial applications. GCP Applied Technologies' Preprufe® pre-applied membrane and Fosroc International's Proofex waterproofing membrane systems are among the most institutionally specified products in Asia Pacific infrastructure project waterproofing programs. Residential holds approximately 32%, anchored by China and India's housing construction. Commercial holds approximately 18%, and Industrial holds approximately 12%.

Regional Insights

China Waterproofing Chemicals Trends & Insights

China leads the Asia Pacific waterproofing chemicals market, anchored by the country's position as the world's largest construction economy with China's National Bureau of Statistics (NBS) documenting annual construction output exceeding RMB 31.6 Trillion (~US$ 4.4 Trillion) in 2023, a metro rail network exceeding 9,000 km per the China Urban Rail Transit Association (CACRTA) requiring intensive tunnel lining waterproofing procurement, and the China Waterproofing Association (CWA) documented progressive national waterproofing quality standard upgrading from commodity to performance-grade materials.

The 14th Five-Year Plan urban renewal mandate targeting the renovation of China's existing building stock is simultaneously driving the procurement of roof waterproofing replacements and below-grade remediation, supplementing new construction waterproofing demand. BASF SE's Master Builders Solutions brand and Sika AG's Shanghai-based manufacturing operations serve China's premium infrastructure project waterproofing specification market.

China's domestic waterproofing chemicals manufacturing industry, anchored by companies including Keshun Waterproof Technology Co., Ltd., Oriental Yuhong Waterproof Technology Co., Ltd., and Weifang Hongyuan Waterproof Materials Co., Ltd., dominates the mass-market SBS modified bituminous membrane and cementitious waterproofing compound segments, while international manufacturers BASF, Sika, GCP Applied Technologies, and Fosroc compete on premium technical performance, product certification, and engineering specification support for China's high-value metro rail, expressway, and landmark commercial building waterproofing programs.

The China Waterproofing Association (CWA)'s national quality certification program for waterproofing materials creates an institutional framework that progressively raises the floor for acceptable product performance, benefiting premium international and domestic manufacturers over commodity producers.

India Waterproofing Chemicals Trends & Insights

India is Asia Pacific's fastest-growing Waterproofing Chemicals market, driven by the Government of India's National Infrastructure Pipeline (NIP) investment of approximately US$ 1.4 Trillion, the PMAY housing mission sanctioning over 11.8 million homes, rapid metro rail expansion across 27 cities documented by the Ministry of Housing and Urban Affairs (MoHUA), and India's position as one of the world's fastest-growing construction economies with the Ministry of Statistics and Programme Implementation (MOSPI) documenting India's construction sector growing at over 10% annually in recent fiscal years.

The domestic waterproofing chemicals market is anchored by Pidilite Industries Ltd.'s Dr. Fixit brand, which, through its comprehensive product range of crystalline waterproofing coatings, acrylic-based waterproofing membranes, polyurethane coatings, and cementitious polymer composites, commands an estimated 40%+ domestic market share reinforced by brand recognition, nationwide distribution, and contractor training programs.

International suppliers Sika AG, BASF SE's MasterSeal portfolio, Fosroc International, and Mapei S.p.A. compete in India's premium institutional infrastructure and commercial construction waterproofing segment, with Fosroc's India operations particularly active in metro rail tunnel lining, dam rehabilitation, and industrial waterproofing project specifications.

The Bureau of Indian Standards (BIS) waterproofing material standards, including IS 1322, IS 15491, and IS 16246, provide the regulatory framework shaping Indian waterproofing chemical product certification and specification requirements. India's National Mission for Clean Ganga (NMCG) water infrastructure rehabilitation program, the Jal Jeevan Mission drinking water supply infrastructure expansion, and the Smart Cities Mission's urban drainage and flood resilience investment are driving structural growth in waterproofing chemical procurement across municipal project procurement channels through 2033.

Southeast Asia Waterproofing Chemicals Trends & Insights

Southeast Asia is a structurally high-growth Waterproofing Chemicals sub-region, anchored by Indonesia's status as the region's largest economy with its national capital relocation Nusantara mega-project in East Kalimantan representing a multi-decade new city construction program generating sustained waterproofing chemical procurement from Indonesia's Ministry of Public Works and Housing (PUPR). Vietnam's above-average economic growth, documented by the Asian Development Bank (ADB) at approximately 6-7% annual GDP growth, is sustaining rapid expansion of commercial real estate and infrastructure construction, with Ho Chi Minh City and Hanoi metro rail projects generating institutional waterproofing membrane and injection grouting procurement from international and regional suppliers.

Singapore's Building and Construction Authority (BCA) maintains the region's most technically advanced building waterproofing code framework, with BCA's Code of Practice on Buildability and waterproofing workmanship quality requirements setting the regional premium specification benchmark that influences construction chemical quality standards across neighboring ASEAN construction markets. Mapei S.p.A.'s Singapore and Thailand regional operations and Sika AG's ASEAN manufacturing presence, including production facilities in Thailand, Vietnam, and Indonesia, position these global suppliers to capture above-average revenue growth from Southeast Asia's accelerating premium waterproofing specification adoption.

The ASEAN Sustainable Urbanization Strategy (ASUS), coordinated through the ASEAN Secretariat, is progressively embedding climate-resilient construction standards, including enhanced waterproofing requirements in member state building codes, creating an institutional policy driver for waterproofing chemical quality standard elevation across the region through 2033.

Competitive Landscape

Asia Pacific Waterproofing Chemicals market is moderately fragmented, with BASF SE, Sika AG, and Pidilite Industries Ltd. commanding premium institutional specification leadership through multi-category waterproofing product portfolios, Asia Pacific regional manufacturing operations, and established technical specification relationships with infrastructure project consultants and engineers. Fosroc International and Mapei S.p.A. lead the premium construction repair and waterproofing segment. Chinese domestic manufacturers including Oriental Yuhong and Keshun dominate volume market share through cost-competitive modified bituminous membrane supply.

Key differentiators include certified sustainability profiles, ADB/World Bank project approval status, technical application support capability, and performance-warranty-backed product systems. Emerging business model trends include direct infrastructure project specification partnerships, digital contractor training platforms, and performance-bonded waterproofing system supply agreements.

Key Developments:

- In January 2025, Sika AG expanded its manufacturing capacity at its Pune, India plant, adding dedicated production lines for SikaProof® pre-applied waterproofing membranes and Sika® Monotop repair products, targeting India's accelerating NIP-funded metro rail tunnel and infrastructure project waterproofing procurement programs.

- In August 2024, Pidilite Industries Ltd. launched its next-generation Dr. Fixit Pidicrete URP Plus crystalline waterproofing compound, offering enhanced chloride penetration resistance and self-sealing crack performance, targeting premium institutional infrastructure project specifications across India's Smart Cities Mission urban drainage and water infrastructure programs.

- In March 2024, BASF SE's Master Builders Solutions division announced a strategic technical partnership with the Nusantara Capital Authority (IKN Authority) in Indonesia, supplying MasterSeal waterproofing membranes and MasterEmaco repair mortars for the new Indonesian capital city's underground infrastructure, government district, and water management facility construction programs.

Companies Covered in Asia Pacific Waterproofing Chemicals Market

- BASF SE

- Sika AG

- RPM International Inc.

- Dow Chemical Company

- Pidilite Industries Ltd.

- Wacker Chemie AG

- Fosroc International Limited

- Carlisle Companies Incorporated

- Mapei S.p.A.

- Drizoro S.A.U.

- Saint-Gobain

- Akzo Nobel N.V.

- Evonik Industries AG

- H.B. Fuller Company

- GCP Applied Technologies

Frequently Asked Questions

The Asia Pacific Waterproofing Chemicals market is estimated to be valued at US$ 19.5 Billion in 2026 and is projected to reach US$ 44.2 Billion by 2033, registering a forecast CAGR of 12.4% from 2026 to 2033.

The primary drivers are the ADB's US$ 26 Trillion Asia Pacific infrastructure investment requirement through 2030 sustaining metro rail tunnel lining, bridge deck, and water infrastructure waterproofing procurement, and UNESCAP's documented 50,000 daily new Asia Pacific urban residents generating residential and commercial construction waterproofing demand.

Bitumen leads the Product Type segment with approximately 34% revenue share in 2026, attributed to its cost-effectiveness, strong adhesion properties, and widespread use in roofing, road construction, and large-scale infrastructure projects.

China leads the Asia Pacific Waterproofing Chemicals market, anchored by the NBS-documented RMB 31.6 Trillion annual construction output, CACRTA's metro rail network exceeding 9,000 km requiring intensive tunnel lining waterproofing, and MOHURD's urban renewal program targeting 40 billion m² existing building stock.

The most significant opportunities are China's urban renewal program targeting 40 billion m² existing building stock waterproofing renovation, driven by MOHURD's 14th Five-Year Plan mandate, and India's Smart Cities Mission and NIP US$ 1.4 Trillion infrastructure investment generating premium cementitious crystalline, pre-applied membrane, and injection grouting system procurement.

The leading companies include Sika AG BASF SE, Pidilite Industries Ltd., Fosroc International Limited, Mapei S.p.A., GCP Applied Technologies, RPM International Inc., Wacker Chemie AG, Carlisle Companies Incorporated, Evonik Industries AG, Akzo Nobel N.V., Saint-Gobain, H.B. Fuller Company, Drizoro S.A.U., and Dow Chemical Company, alongside domestic Chinese leaders Oriental Yuhong and Keshun, collectively spanning global premium waterproofing systems innovators and Asia Pacific-focused domestic manufacturers serving the region's full waterproofing chemicals value chain.