- Inks, Coatings, Adhesives & Sealants (ICAS)

- Paper Coating Materials Market

Paper Coating Materials Market Size, Share, and Growth Forecast 2026 - 2033

Paper Coating Materials Market by Paper Type (Printing & Writing Paper, Packaging Paper & Paperboard, Label Paper, Specialty Paper), Material (Pigments, Binders, Additives, Others), End-use Industry (Packaging, Food & Beverages, Printing, Pharmaceuticals, Others), and Regional Analysis for 2026 - 2033

Paper Coating Materials Market Size and Trend Analysis

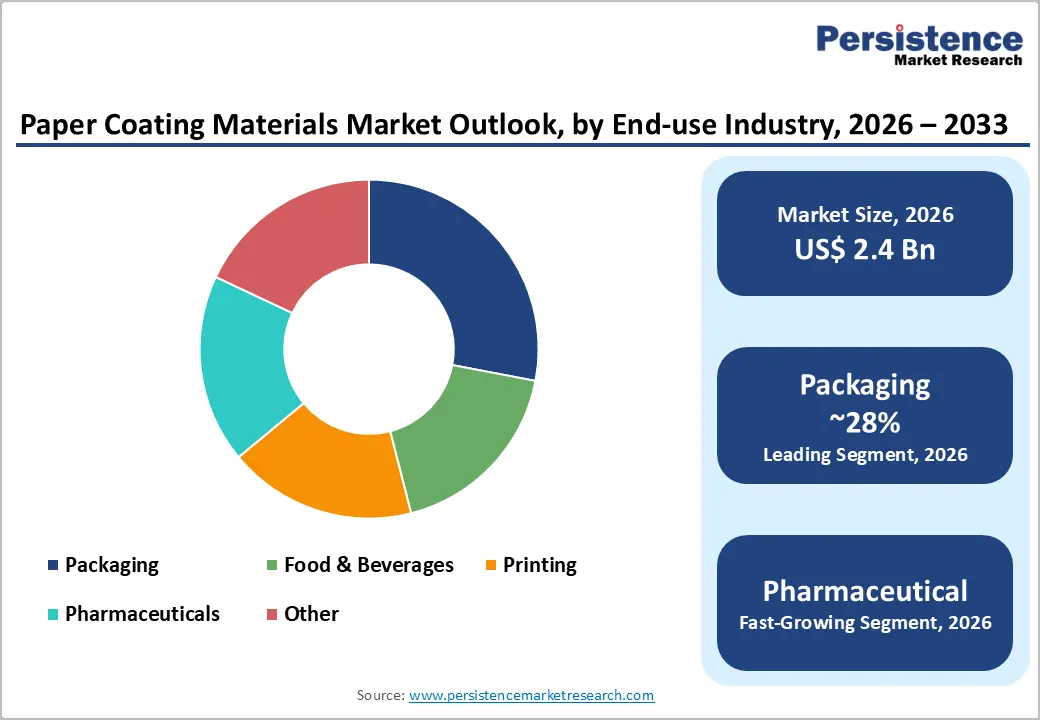

The global paper coating materials market is valued at US$ 2.4 billion in 2026 and is projected to reach US$ 3.4 billion by 2033, growing at a CAGR of 5.0% between 2026 and 2033. The market's expansion is primarily anchored by the accelerating shift away from single-use plastic packaging, rising e-commerce-driven demand for premium corrugated and coated packaging, and mounting regulatory pressure for recyclable, food-safe substrates.

Ground calcium carbonate and kaolin clay continue to be indispensable performance pigments, while bio-based binders and sustainable additives are fast becoming the preferred alternatives to synthetic polymer coatings. Together, these forces create a structurally robust demand trajectory across both developed and emerging markets through the forecast period.

Key Industry Highlights:

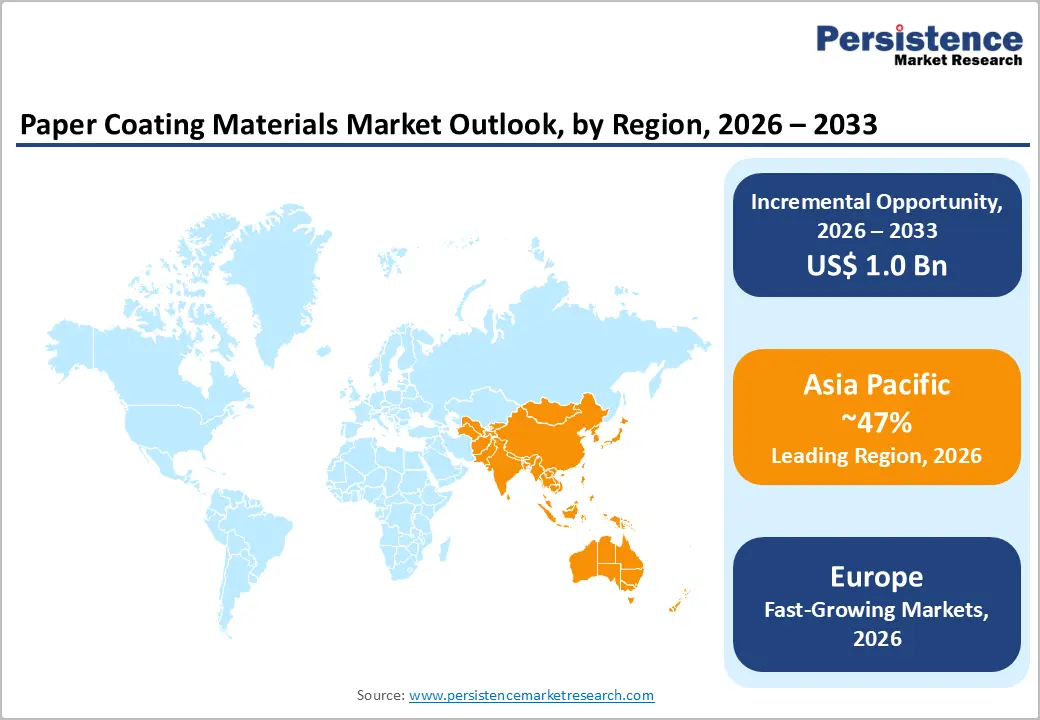

- Leading Region: Asia Pacific dominates the global paper coating materials market with approximately 47% share, driven by China's 7.2% coated-paper production growth in 2024, India's booming packaging sector, and aggressive onsite mineral capacity expansions by leading global suppliers.

- Fastest Growing Region: Europe is the fastest growing region for the global paper coating materials market, supported by advanced paper industries serving export-oriented packaging and premium publishing segments.

- Dominant Segment: Calcium Carbonate holds the largest material-category share at approximately 42%, underpinned by cost leadership, optical performance advantages, and full compatibility with EU PPWR recyclability and PFAS-free compliance mandates now governing food-contact packaging.

- Fastest Growing Segment: Starch-based binders are the fastest growing material sub-segment, benefiting from the regulatory phase-out of PFAS, consumer and brand-owner demand for bio-based coatings, and innovation in modified starch formulations replacing 10-20% of synthetic SB latex in commercial coating trials.

- Key Market Opportunity: Specialty paper coatings for pharmaceutical packaging represent the highest-value growth opportunity, underpinned by 5-6% annual WHO-projected growth in global pharma markets, stringent FDA/EFSA compliance standards, and rising demand for serialization-ready, tamper-evident, high-precision print coating systems.

| Key Insights | Details |

|---|---|

| Paper Coating Materials Market Size (2026E) | US$ 2.4 Bn |

| Market Value Forecast (2033F) | US$ 3.4 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.0% |

| Historical Market Growth (2020 - 2025) | 4.5% |

Market Dynamics

Drivers - E-commerce Boom and Rising Demand for High-Performance Coated Packaging

The rapid expansion of global digital commerce has become a significant structural catalyst for increasing demand for paper coating materials. According to the United Nations Conference on Trade and Development, global e-commerce sales surpassed US$6.3 trillion in 2023, followed by a 12.3 percent rise in shipment volumes in 2024, resulting in substantial growth in corrugated-packaging requirements. Each shipment relies on coated paperboard surfaces that deliver high print clarity, moisture resistance, and mechanical durability, supported by advanced pigments, binders, and functional additives.

Premium and luxury brands are increasingly employing multilayer coating systems to enhance gloss and surface quality. In emerging markets such as India and Southeast Asia, expanding online grocery and electronics retail continues to drive strong demand for food-grade and printable barrier coatings, reinforcing a positive medium-term market outlook.

Regulatory Phase-out of PFAS and Single-Use Plastics Catalysing Paper Substrate Substitution

Stringent environmental regulations are increasingly reshaping material selection across the global packaging value chain, thereby directly supporting growth in the paper coating materials market. The European Union’s Packaging and Packaging Waste Regulation (EU) 2025/40, published in January 2025 and entering into force on 12 August 2026, prohibits the use of per- and polyfluoroalkyl substances (PFAS) above 25 ppb in food-contact packaging, mandates full recyclability of packaging by 2030, and establishes ambitious recycled-content targets.

Parallel regulatory actions, including U.S. state-level PFAS bans in jurisdictions such as Maine and Washington and India’s Extended Producer Responsibility framework, are accelerating the transition away from fluoropolymer-coated films toward mineral-based and bio-based coated paper solutions. This regulatory shift is driving increased demand for calcium carbonate, kaolin clay, and starch-based coating systems that align with recyclability and food-contact safety requirements.

Restraints - Raw Material Price Volatility

Price instability in key coating inputs, kaolin, latex binders, and pulp, poses a persistent margin risk for coating suppliers and paper mills alike. Kaolin prices increased approximately 10% in 2024 following supply-chain disruptions in major mining regions. Styrene-butadiene (SB) latex binder costs fluctuate with petrochemical feedstock cycles, while pulp price swings distort paper mill economics and alter coating application rates. For smaller coating producers lacking long-term supply contracts, these cost headwinds complicate contract negotiations and reduce pricing power, ultimately constraining market growth by pressuring buyer budgets and incentivizing coating weight reductions.

Declining Print Volumes and Digitalization of Media

The structural migration of content consumption to digital platforms continues to erode demand for printing and writing coated papers, one of the historically dominant application segments. According to the International Telecommunication Union (ITU), global internet users surpassed 5.4 billion in 2024, a trend that directly compresses advertising spend on print media and diminishes orders for premium coated fine papers. This secular decline reduces total pigment and binder consumption in the graphical segment, partially offsetting the gains recorded in packaging, label, and specialty paper applications, thereby tempering overall market growth rates.

Opportunities - Bio-based and Sustainable Coating Formulations

The growing global emphasis on circularity and decarbonization is creating significant commercial opportunities for suppliers capable of delivering bio-based and low-carbon paper coating solutions. The gradual phase-out of PFAS and synthetic polymer barriers is accelerating research and development investment in starch-based, nanocellulose, and plant-derived binder technologies. In early 2025, a specialty chemicals manufacturer introduced a starch-based binder formulation that successfully replaced 15% of conventional styrene-butadiene latex in commercial coating trials across Europe, demonstrating technical and economic viability at scale.

Leading suppliers, including Kemira Oyj, have publicly committed to expanding bio-based product portfolios by 2030 and achieving carbon-neutral operations by 2045, signaling a long-term structural shift in supply chains. Brand owners and converters are increasingly prioritizing coating materials that not only meet PPWR recyclability requirements but also support Scope 3 emissions reduction, enabling premium pricing for sustainable formulations.

Expanding Pharmaceutical Packaging Applications for Specialty Paper Coatings

Pharmaceutical packaging has emerged as a strategically important and high-value application within the specialty paper coating materials market. Expansion in global pharmaceutical manufacturing, rising life expectancy, and the growing availability of over-the-counter medicines are collectively driving increased demand for coated folding cartons, blister inserts, and tamper-evident labelling solutions. These packaging formats require coatings that deliver consistent barrier performance, chemical stability, and high-resolution print quality to satisfy stringent regulatory and brand-protection standards.

According to the World Health Organization, the global pharmaceutical market is expected to grow at an annual rate of approximately 5-6% through the latter half of the decade, with particularly strong expansion in Asia Pacific and Latin America. Consequently, demand is rising for titanium dioxide-based opacity systems, advanced latex binders, and specialty functional additives compliant with pharmaceutical migration and sterility requirements.

Category-wise Analysis

Paper Type Insights

Packaging paper and paperboard represent the dominant paper type within the paper coating materials market, accounting for approximately 65% of total demand. This leadership position is underpinned by sustained structural growth in e-commerce, consumer goods distribution, and food packaging applications. Packaging substrates impose stringent functional requirements, including grease resistance, moisture protection, high-definition printability, and compliance with food-contact safety standards, all of which necessitate higher per-unit consumption of pigments, binders, and additives compared with graphical papers.

Coated paperboard is increasingly displacing multilayer plastic packaging in fast-food and ready-meal formats, thereby expanding addressable coating volumes. Although label paper and specialty paper account for smaller shares, they are recording above-average growth driven by pharmaceutical serialization mandates, premium branding requirements, and compatibility with digital printing technologies.

Material Insights

Pigments, encompassing both Ground Calcium Carbonate (GCC) and Precipitated Calcium Carbonate (PCC), is the dominant coating material, holding approximately 58% of total market share. Its leadership reflects a unique combination of cost-effectiveness, optical performance, and mineral abundance. GCC improves paper brightness, opacity, and surface smoothness at substantially lower cost than alternatives like titanium dioxide, while its natural origin makes it compatible with emerging recyclability and bio-content compliance requirements.

Omya AG alone holds approximately 10-12% of global calcium carbonate supply to the paper coating sector. Kaolin clay follows as the second largest material, prized for its superior gloss and printability in premium art and label papers. Titanium dioxide, while commanding a 15% revenue share as of 2022, faces cost and regulatory pressure but remains indispensable for high-opacity coating grades.

Industry Insights

The packaging segment occupies a leading position in the end-use landscape for paper coating materials, accounting for approximately 28% of total market revenue. This dominance reflects sustained demand from consumer goods producers, food and beverage manufacturers, and e-commerce logistics providers, all of which require high-volume coated substrates offering consistent print quality, functional barrier performance, and compliance with sustainability standards.

The food and beverages sub-segment remains structurally integrated with packaging, generating additional demand for food-contact-safe coatings that comply with regulatory frameworks established by the U.S. Food and Drug Administration and the European Food Safety Authority. Pharmaceutical applications represent the fastest-growing end-use segment, while the printing segment continues to decline in relative importance due to ongoing digital substitution of print media.

Regional Insights

North America Paper Coating Materials Trends

North America represents a mature and technologically advanced market for paper coating materials, with demand predominantly driven by the United States. The region benefits from a well-established paper and packaging industry supported by major producers that operate high-precision coating lines for premium packaging and commercial printing applications. Increasing regulatory momentum, particularly state-level restrictions on PFAS, is prompting converters to reformulate coating systems, thereby generating transitional demand for mineral-based and bio-derived alternatives.

Concurrently, geopolitical tensions involving the United States and instability in the Middle East have contributed to petrochemical feedstock volatility, resulting in elevated costs for synthetic binders. These supply-side pressures are accelerating the shift toward bio-based binder systems, while continued investment in innovation and domestic R&D infrastructure is supporting the development of advanced barrier and digital-print-compatible coating technologies aligned with evolving sustainability requirements.

Europe Paper Coating Materials Trends

Europe represents the most proactive regulatory environment globally for paper coating materials and functions as a critical region in shaping demand patterns. Germany, France, the United Kingdom, and the Nordic countries constitute the principal consumption markets, supported by advanced paper industries serving export-oriented packaging and premium publishing segments. The implementation of the EU Packaging and Packaging Waste Regulation from August 2026 is prompting substantial reallocation of research and development resources toward recyclable and PFAS-free coating solutions.

Spain and Italy are emerging as growth centres for coated label and specialty papers, driven by strong food, wine, and pharmaceutical export performance. Concurrently, geopolitical risks arising from U.S.-Iran tensions have increased European energy market volatility, elevating production costs and accelerating investment in energy-efficient coating technologies.

Asia Pacific Paper Coating Materials Trends

Asia Pacific constitutes the largest regional market for paper coating materials, accounting for approximately 47% of global demand. China remains the dominant country market, with coated-paper production expanding by 7.2% in 2024, driven by strong growth in consumer goods packaging and digital printing applications. Strategic investments by major suppliers underscore long-term confidence in the region; notably, Omya AG announced plans in April 2023 to establish seven onsite calcium carbonate plants across China and Indonesia.

Japan continues to serve as a centre for advanced specialty coating innovation, particularly for pharmaceutical and digital printing uses, while ASEAN economies such as Vietnam, Indonesia, and Thailand are attracting sustained foreign direct investment in coated paper and packaging capacity. Geopolitical disruptions affecting global shipping routes have modestly increased freight costs, encouraging localization of raw material supply and further supporting regional capacity expansion.

Competitive Landscape

The global paper coating materials market exhibits a moderately concentrated structure, with the top ten companies collectively accounting for over 60% of total market revenue. BASF SE, Omya AG, and Imerys S.A. function as anchor players, leveraging vertically integrated supply chains, global distribution networks, and extensive R&D infrastructure to maintain competitive differentiation. Bio-based binder development, nanotechnology-enhanced pigment systems, and digital-print-compatible coating architectures represent the three primary vectors of product differentiation. Strategic partnerships, such as the long-standing BASF-Omya Pilot Coating Center collaboration, exemplify the industry's shift toward co-innovation models that reduce time-to-market for next-generation coating solutions.

Key Developments:

- March 2026: BASF SE announced the expansion of its dispersions production capacity in Durban, South Africa, enhancing supply of high-performance coating materials for paper and packaging applications, while strengthening regional supply reliability and technical support capabilities.

- February 2026: BASF SE announced the expansion of its dispersions production capacity at its Mangalore site, India, by adding a new production line to support growing demand in coatings, packaging, and paper applications, strengthening regional supply capabilities.

- November 2025: Michelman Inc. announced the launch of its Michem® Coat 9250, a next-generation water-based coating enabling recyclable paper cups, supporting sustainable paper coating materials by reducing plastic use while maintaining high performance for hot beverage applications.

Top Companies in Paper Coating Materials

- BASF SE (Ludwigshafen, Germany) is one of the two foremost global suppliers of binders and coating additives for paper and board, commanding a leading share of the SB latex and polymer dispersion segments. Through its Pilot Coating Center and sustained R&D investments, BASF delivers a comprehensive range of products including Acronal and Styronal dispersions, catering to packaging, commercial print, and specialty paper applications across global markets.

- Omya AG (Oftringen, Switzerland) is the world's leading producer of calcium carbonate for the paper coating industry, holding 10-12% of global coating pigment supply. Operating from over 175 locations in 50+ countries, Omya provides both ground and precipitated calcium carbonate solutions that enhance brightness, opacity, and surface smoothness. Strategic capacity expansions in China and Indonesia, combined with its Distrupol acquisition in February 2025 to build a global polymers distribution network, signal aggressive portfolio broadening and regional market penetration.

- Imerys S.A. (Paris, France) is the global leader in high-performance kaolin clay and specialty mineral solutions for paper pigments. The company's metakaolin and engineered kaolin grades are widely deployed in art papers, label stocks, and coated folding cartons requiring premium gloss and printability. Imerys's ongoing investment in sustainable pigment systems and its extensive global minerals sourcing infrastructure, spanning Georgia (USA), Brazil, and the U.K., position it as an indispensable partner for paper mills seeking both performance and circular economy compliance.

Companies Covered in Paper Coating Materials Market

- BASF SE

- Omya AG

- Dow Inc.

- Eastman Chemical Company

- Ashland Inc.

- Arkema S.A.

- Michelman, Inc.

- Imerys S.A.

- Solvay S.A.

- Kemira Oyj

- Celanese Corporation

Frequently Asked Questions

The global Paper Coating Materials market is valued at US$ 2.4 Bn in 2026 and is projected to reach US$ 3.4 Bn by 2033, expanding at a CAGR of 5.0% during the forecast period. The growth trajectory is supported by rising demand for high-performance coated packaging, regulatory-driven shift from PFAS-based coatings, and expanding e-commerce logistics globally.

The market is principally driven by the global e-commerce boom, which recorded 12.3% volume growth in 2024, generating unprecedented coated corrugated packaging demand, and tightening environmental regulations, including the EU PPWR (Regulation 2025/40), which mandates PFAS-free, recyclable packaging from August 2026, compelling converters to adopt mineral-based and bio-derived coating alternatives.

Pigments are the dominant material segment, capturing approximately 58% of market share. Both Ground Calcium Carbonate (GCC) and Precipitated Calcium Carbonate (PCC) are widely preferred due to their cost effectiveness, high brightness, opacity enhancement, and compatibility with circular economy and recyclability standards. Omya AG and Imerys S.A. are the leading global suppliers of this material.

Asia Pacific leads the global Paper Coating Materials market, accounting for approximately 47% of total demand. The region's dominance is driven by China's sustained coated-paper production growth, India's expanding packaging sector, and concentrated investment in onsite mineral processing capacity by global suppliers.

The pharmaceutical packaging segment represents the most attractive growth opportunity for paper coating material suppliers. With the WHO projecting global pharmaceutical market growth of 5-6% annually through the late 2020s, particularly across Asia Pacific and Latin America, demand for precision barrier coatings, titanium dioxide-based opacity layers, and FDA/EFSA-compliant specialty binders in pharma folding cartons and blister inserts is expected to generate sustained premium revenue streams.

The leading companies in the global Paper Coating Materials market include BASF SE, Omya AG, Imerys S.A., Dow Inc., Kemira Oyj, Eastman Chemical Company, Ashland Inc., Arkema S.A., Michelman Inc., Solvay S.A., and Celanese Corporation.