- Inks, Coatings, Adhesives & Sealants (ICAS)

- Zero Friction Coatings Market

Zero Friction Coatings Market Size, Share, and Growth Forecast 2026 - 2033

Zero Friction Coatings Market by Coatings Type (PTFE-Based Coatings, MoS₂-Based Coatings, Graphite-Based Coatings, WS₂-Based Coatings, Boron Nitride-Based Coatings, Fluoropolymer Coatings, Ceramic Coatings, Composite Coatings), Formulation, Application Method, Substrate Type, End-user, and Regional Analysis, 2026 - 2033

Zero Friction Coatings Market Size and Trend Analysis

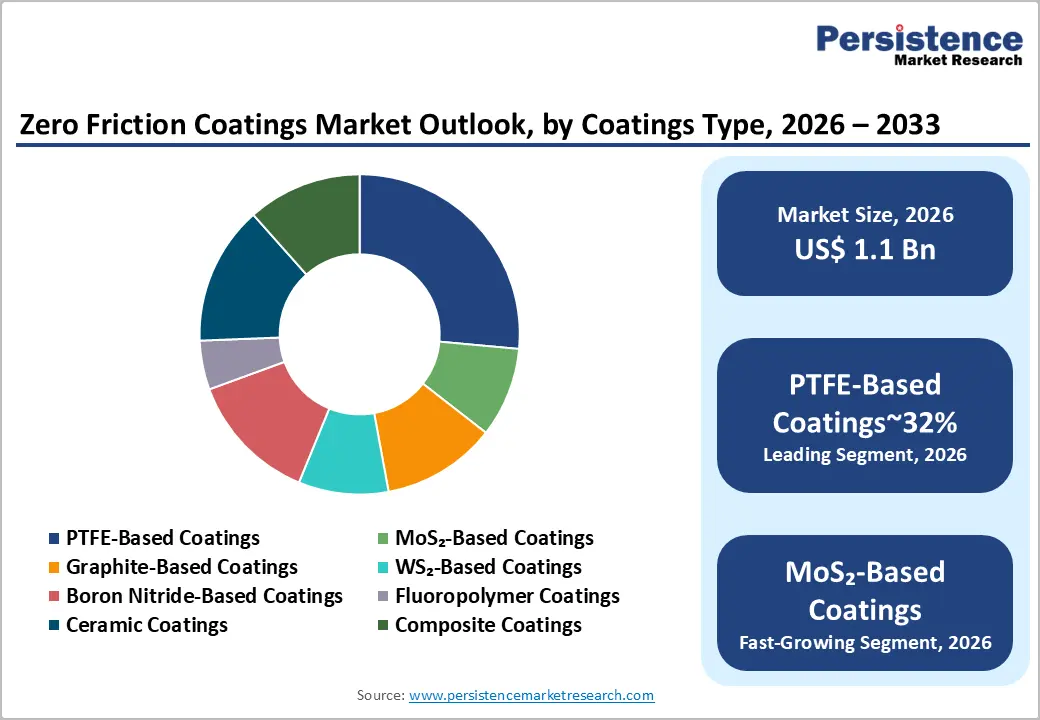

The global Zero Friction Coatings Market size is likely to be valued at US$ 1.1 billion in 2026 and is expected to reach US$ 1.6 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033. The market is advancing steadily driven by intensifying demand for wear-resistant and friction-reducing surface treatments across automotive, aerospace, industrial machinery, and energy sectors, where component longevity and energy efficiency are paramount operational objectives.

Key Industry Highlights:

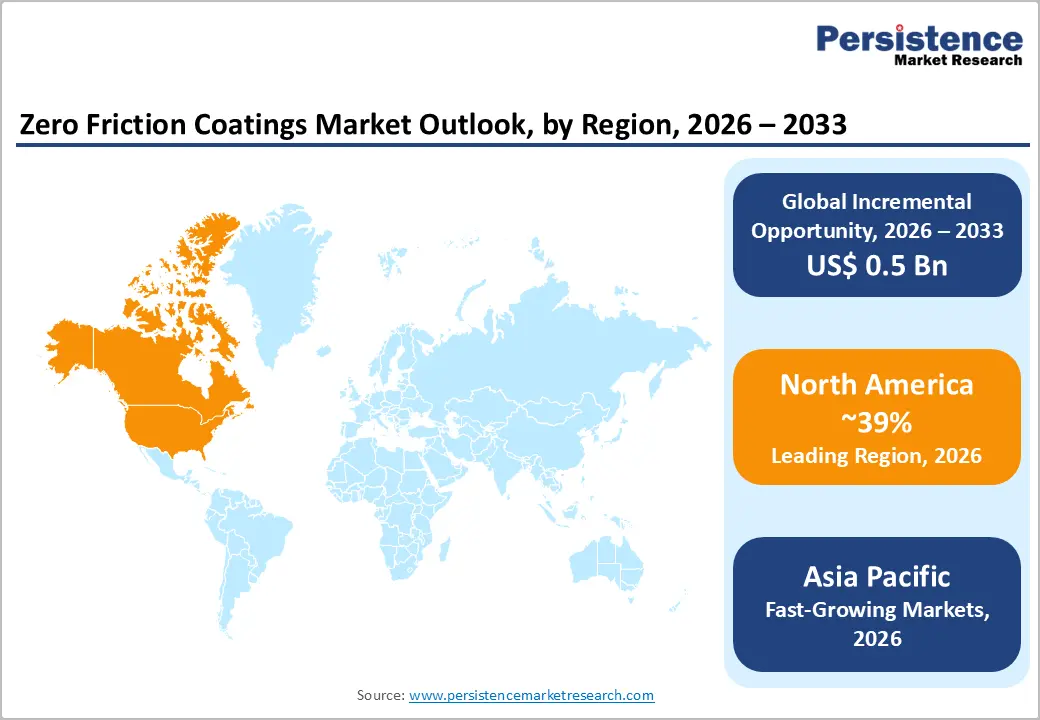

- Leading Region: North America, led by the United States, dominates the global zero friction coatings market and accounted for 39% share in 2025. The world's largest aerospace and defense industrial base is located here that generates approximately US$ 900 billion in annual economic impact.

- Fastest Growing Region: Asia Pacific is the fastest-growing followed with a CAGR of 6.8%, driven by China's position as the world's largest automotive and EV manufacturer, with over 30 million vehicle sales in 2023and expanding semiconductor, robotics, and renewable energy manufacturing across Japan, India, and South Korea.

- Dominant Segment: PTFE-based coatings lead the coatings type category with approximately 32% share, driven by the lowest commercially available coefficient of friction (~0.04), exceptional chemical inertness, broad thermal stability up to 260°C, and decades of validated industrial application data across automotive, food processing, and medical device sectors.

- Key Opportunity: Wind energy expansion, with global installations reaching a record 117 GW in 2023 per the Global Wind Energy Council (GWEC) and the IEA projecting tripled capacity by 2030, creates a durable, large-scale demand pipeline for zero friction coatings in turbine pitch bearings, gearboxes, and generator components requiring maintenance-free tribological protection.

| Key Insights | Details |

|---|---|

|

Zero Friction Coatings Market Size (2026E) |

US$ 1.1 Billion |

|

Market Value Forecast (2033F) |

US$ 1.6 Billion |

|

Projected Growth CAGR (2026–2033) |

5.3% |

|

Historical Market Growth (2020–2025) |

4.8% |

Market Dynamics

Drivers - Growing Demand for Energy-Efficient Tribological Solutions Across Industrial Sectors

The imperative to reduce industrial energy consumption and extend equipment service life is creating structural and growing demand for zero friction coating technologies. According to a landmark study published by VTT Technical Research Centre of Finland and supported by data from the International Energy Agency (IEA), implementing advanced tribological solutions globally could reduce total energy consumption by approximately 8.7% and CO2 emissions by 1,460 Million tonnes over a 15-year horizon.

Zero friction coatings, including PTFE, MoS2, tungsten disulfide (WS2), and diamond-like carbon (DLC) systems, are increasingly specified in precision machinery, compressors, hydraulic systems, and automotive powertrains to reduce sliding friction, minimize lubricant use, and extend component replacement intervals. This energy efficiency imperative, reinforced by government industrial decarbonization targets in the EU, U.S., and China, is creating a durable and policy-supported demand cycle for zero friction coating solutions.

Electrification of Automotive and Aerospace Applications Driving Advanced Coating Adoption

The global transition toward electric vehicles (EVs) and next-generation aircraft is creating specialized demand for zero friction coatings tailored to the unique tribological requirements of electrified drivetrain components. Unlike conventional internal combustion engines, EV motors, gearboxes, and battery thermal management systems require coatings compatible with electric fields, low-viscosity lubricants, and elevated temperature cycling.

According to the International Energy Agency (IEA), global EV sales exceeded 14 Million units in 2023, representing approximately 18% of total new car sales, with over 240 Million EVs projected on roads by 2030. The European Aviation Safety Agency (EASA) and NASA have published research validating dry film lubricant coatings for space and aerospace applications operating in vacuum and extreme temperature environments where liquid lubricants are impractical. These sectoral transitions are expanding the performance envelope and application addressable market for zero friction coating technologies.

Restraints - High Application and Processing Costs for Advanced PVD/CVD Coating Technologies

Physical vapor deposition (PVD) and chemical vapor deposition (CVD) coating processes, while delivering superior zero friction performance for aerospace and precision engineering applications, involve substantial capital investment in vacuum deposition equipment, cleanroom-grade application facilities, and highly trained technical personnel.

According to the Society of Vacuum Coaters (SVC), industrial PVD coating systems can cost between US$ 500,000 and US$ 5 Million per installation, creating a prohibitively high entry barrier for smaller manufacturers and limiting adoption to large-scale industrial and defense applications where the performance premium justifies the investment. This cost constraint disproportionately restrains market penetration among small and mid-sized enterprise end-users.

Environmental and Regulatory Restrictions on PTFE and Fluoropolymer Coatings

Regulatory pressure on per- and polyfluoroalkyl substances (PFAS), the chemical family encompassing PTFE and related fluoropolymer coatings, is emerging as a significant headwind for a major segment of the Zero Friction Coatings Market.

The U.S. Environmental Protection Agency (EPA) finalized the first-ever PFAS national drinking water standards in 2024, and the European Chemicals Agency (ECHA) has proposed broad restrictions on non-essential PFAS uses under the EU REACH regulation. These regulatory developments are compelling zero friction coating manufacturers to invest in PTFE-free alternatives, including MoS2, boron nitride, and ceramic-based systems, creating formulation transition costs and market uncertainty for both suppliers and end-users reliant on established fluoropolymer coating specifications.

Opportunities - Rapid Adoption of Zero Friction Coatings in Semiconductor and Electronics Manufacturing

The semiconductor and electronics manufacturing sector represents an emerging and high-growth end-use opportunity for advanced zero friction coatings, driven by the extreme precision requirements of wafer handling equipment, photolithography systems, and microelectronic packaging lines. Zero friction coatings, particularly PTFE alternatives, boron nitride, and tungsten disulfide (WS2) systems, are specified for robotic handling components, precision linear guides, and vacuum system components where particle generation from conventional lubricants is prohibited.

According to the Semiconductor Industry Association (SIA), global semiconductor sales exceeded US$ 526 Billion in 2023, with capital equipment investment remaining at historically elevated levels driven by the U.S. CHIPS and Science Act authorizing US$ 52.7 Billion in domestic semiconductor manufacturing investment. This capacity buildout is directly expanding the installed base of precision semiconductor equipment requiring zero friction coatings for cleanroom-compatible lubrication.

Growing Demand in Wind Energy and Renewable Power Generation Applications

The global wind energy sector's accelerating expansion is creating a significant and structurally durable demand opportunity for zero friction coatings in turbine pitch and yaw bearing systems, gearboxes, and generator components. Wind turbine drivetrain components operate under highly variable load conditions, extreme temperature cycling, and limited maintenance access, conditions that make solid film and zero friction coatings preferable to conventional grease lubrication for reducing wear-induced downtime and extending maintenance intervals.

According to the Global Wind Energy Council (GWEC), global wind power installations reached a record 117 GW in 2023, bringing total installed capacity to over 1,000 GW worldwide, with the IEA projecting installed wind capacity to triple by 2030. Major turbine manufacturers including Vestas, Siemens Gamesa, and GE Vernova are specifying advanced dry film lubricant and zero friction coating systems in turbine design guidelines to extend service life in offshore and remote onshore installations.

Category-wise Analysis

Coatings Type Insights

PTFE-Based Coatings dominate the Zero Friction Coatings Market by coating type, accounting for approximately 32% of total market revenue. Polytetrafluoroethylene (PTFE), commercially known as Teflon (a registered trademark of The Chemours Company), offers the lowest coefficient of friction among commercially available solid lubricant coatings, with static friction coefficients as low as 0.04, combined with exceptional chemical inertness, thermal stability up to 260°C, and broad compatibility with diverse substrate materials.

According to the American Chemical Society (ACS), PTFE coatings are specified across thousands of industrial applications including automotive fuel system components, food processing equipment, medical devices, and precision instrumentation. Despite growing regulatory scrutiny under PFAS frameworks, PTFE coatings currently maintain dominant market share due to their unparalleled performance and decades of established application validation data.

Formulation Insights

Solvent-Based formulations constitute the leading segment in the Formulation category, accounting for approximately 36% of total market revenue. Solvent-based zero friction coatings offer superior film-forming properties, excellent substrate adhesion on metals and engineering plastics, and broad application temperature tolerance, making them the preferred formulation for industrial machinery, automotive, and aerospace applications requiring high-performance tribological coatings on complex geometries.

According to the American Coatings Association (ACA), solvent-based coatings remain a substantial share of the global industrial coatings market due to their well-understood application characteristics and superior performance in demanding environmental conditions. However, water-based formulations are the fastest-growing segment, driven by tightening VOC emission regulations under the U.S. EPA and the EU's Industrial Emissions Directive (IED), compelling manufacturers to develop high-performance water-based alternatives.

Application Method Insights

Spray coating is the dominant application method in the zero friction coatings market, accounting for approximately 41% of total market revenue. Spray application, encompassing both air-atomized and airless spray technologies, offers unmatched versatility for coating complex three-dimensional geometries, large surface areas, and high-throughput production line environments across automotive, industrial machinery, and consumer goods manufacturing.

According to the Spray Systems Company and industry technical literature, spray coating enables precise film thickness control, uniform coating distribution, and rapid application speeds compatible with automated production environments. The widespread availability of spray coating infrastructure in existing industrial facilities further reinforces the method's market dominance. PVD and CVD processes are growing fastest within the application method category, driven by adoption in aerospace, semiconductor, and high-precision engineering applications.

Substrate Type Insights

Metals represent the dominant substrate type, accounting for approximately 58% of total zero friction coatings market revenue. Metal substrates, including steel, aluminum, titanium, cast iron, and copper alloys, are the primary surfaces requiring tribological coating treatment across the market's largest end-use sectors: automotive drivetrain components, industrial machinery bearing surfaces, aerospace structural interfaces, and energy sector rotating equipment.

The superior adhesion of PTFE, MoS2, and ceramic zero friction coating systems to metal substrates, facilitated by established surface pre-treatment protocols including grit blasting, phosphating, and chemical etching, has created a well-validated and extensive product application library. According to the World Steel Association (WSA), global steel production totaled approximately 1.89 Billion tonnes in 2023, reflecting the scale of the metal substrate base across which zero friction coatings are applied.

End-user Insights

Automotive & Transportation represents the dominant end-use segment, accounting for approximately 28% of total Zero Friction Coatings Market revenue. Vehicle powertrain components, including pistons, piston rings, camshafts, valve stems, fuel injectors, and transmission gears, are extensively coated with zero friction materials to reduce sliding friction losses, minimize wear, and improve fuel economy.

According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production totaled approximately 93 million units in 2023, each incorporating multiple friction-critical components requiring tribological coating treatment. The global automotive lightweighting trend, driven by EU CO2 fleet emission regulations and U.S. CAFE standards, is expanding the use of aluminum and composite components, which require specialized zero friction coating systems compatible with non-ferrous and polymer substrate materials.

Regional Insights

North America Zero Friction Coatings Market Trends

The United States leads the North American Zero Friction Coatings Market, supported by its advanced automotive manufacturing cluster, world-class aerospace and defense industrial base, and a dense network of precision industrial machinery producers. Major automotive manufacturing hubs in Michigan, Ohio, and Kentucky generate sustained demand for zero friction piston, bearing, and drivetrain coatings. According to the Aerospace Industries Association (AIA), the U.S. aerospace industry generates approximately US$ 900 Billion in economic impact annually, sustaining high-value demand for advanced PVD and dry film lubricant coatings in jet engine, actuation, and structural joint applications. The U.S. CHIPS and Science Act is further driving semiconductor equipment demand for precision zero friction coatings.

The U.S. EPA's evolving PFAS regulatory framework is compelling coating formulators to accelerate development of PTFE-free zero friction alternatives, driving R&D investment among leading suppliers including 3M Company, The Chemours Company, and DuPont de Nemours Inc. Canada's mining and oil sands industries represent a significant demand source for industrial machinery zero friction coatings applied to heavy equipment operating under extreme abrasion and load conditions. North America's innovation ecosystem, encompassing national laboratories, university tribology research programs, and corporate R&D centers, sustains the region's position as a global leader in zero friction coating technology development.

Europe Zero Friction Coatings Market Trends

Europe is a technologically advanced and innovation-rich market for zero friction coatings, anchored by Germany's world-leading automotive and mechanical engineering industries. According to the German Association of the Automotive Industry (VDA), Germany produced approximately 4.1 Million vehicles in 2023, generating substantial demand for precision tribological coatings in powertrain, transmission, and braking systems. Germany also hosts major zero friction coating suppliers including Carl Bechem GmbH and Henkel AG & Co. KGaA, which develop lubricant and coating solutions for global automotive and industrial machinery markets. The European Commission's Fit for 55 climate package and fleet CO2 reduction targets are incentivizing automotive manufacturers to specify friction-reducing coatings that improve powertrain efficiency.

The European Chemicals Agency (ECHA)'s proposed PFAS restrictions under REACH are reshaping the European zero friction coatings landscape, compelling accelerated transition toward fluoropolymer-free alternatives including MoS2, boron nitride, and ceramic-based coating systems. France's aerospace manufacturing sector, anchored by Safran and Airbus, drives demand for high-performance dry film lubricants in aircraft actuator and engine component applications. The United Kingdom's National Aerospace Technology Programme (NATP) supports R&D investment in advanced tribological coatings for next-generation aircraft. Spain's growing wind energy manufacturing base is creating incremental demand for zero friction coatings in turbine drivetrain and pitch bearing components.

Asia Pacific Zero Friction Coatings Market Trends

Asia Pacific is the fastest-growing regional market for zero friction coatings, driven by massive automotive, electronics, and industrial machinery manufacturing scale across China, Japan, South Korea, and India. China is both the world's largest automotive market, with the China Association of Automobile Manufacturers (CAAM) reporting over 30 Million vehicle sales in 2023, and the global leader in EV production, with NEV sales exceeding 9 Million units. Chinese manufacturers are increasingly specifying zero friction coatings for EV drivetrain components, industrial automation equipment, and renewable energy installations. Local suppliers and global players including Nippon Paint Holdings Co. Ltd. are expanding their tribological coating product portfolios to capture this high-growth demand.

Japan's precision engineering industry, encompassing robotics, machine tools, and semiconductor equipment, drives sustained demand for ultra-precision PVD and dry film lubricant coatings from companies including Akzo Nobel N.V. and specialty Japanese coating houses. According to the Japan Machine Tool Builders' Association (JMTBA), Japan remains among the world's top three machine tool producers, with precision coating demand directly correlated with production output. India's rapidly expanding automotive and aerospace manufacturing sectors, supported by Make in India and Production Linked Incentive (PLI) schemes, are creating incremental demand for zero friction coating solutions as domestic manufacturers upgrade component quality standards to meet export market specifications.

Competitive Landscape

The global Zero Friction Coatings Market is moderately fragmented, featuring a mix of diversified specialty chemical and coatings conglomerates, including PPG Industries Inc., Akzo Nobel N.V., Axalta Coating Systems Ltd., The Sherwin-Williams Company, and Henkel AG & Co. KGaA, alongside focused tribological coating specialists such as Carl Bechem GmbH, IKV Tribology Ltd., and Poeton Industries Ltd.

Key differentiators include proprietary coating chemistry, PFAS-free formulation capabilities, application process engineering support, and industry-specific qualification packages. Emerging business model trends include application-as-a-service offerings for precision component manufacturers and digital coating specification platforms. R&D investment is concentrated on water-based and PFAS-free zero friction alternatives, DLC coatings for EV drivetrains, and nano-composite coating systems.

Key Developments:

- March 2025: The Chemours Company launched its next-generation Teflon® industrial coating series with enhanced PFAS-reduced formulations, targeting automotive and industrial machinery customers seeking regulatory-compliant zero friction solutions while maintaining performance benchmarks of conventional PTFE systems.

- November 2024: Henkel AG & Co. KGaA expanded its Bonderite dry film lubricant portfolio with new water-based zero friction coating grades for EV motor and gearbox applications, targeting the rapidly growing electric vehicle drivetrain component coating market across Europe and Asia Pacific.

- June 2024: PPG Industries Inc. introduced a next-generation PTFE-free fluoropolymer-alternative coating system under its industrial coatings range, developed in response to EPA PFAS regulations, targeting automotive fuel systems, food processing, and medical device component applications in North America.

Companies Covered in Zero Friction Coatings Market

- 3M Company

- Akzo Nobel N.V.

- Axalta Coating Systems Ltd.

- Carl Bechem GmbH

- DuPont de Nemours Inc.

- Endura Coatings

- Henkel AG & Co. KGaA

- IKV Tribology Ltd.

- Nippon Paint Holdings Co. Ltd.

- Poeton Industries Ltd.

- PPG Industries Inc.

- RPM International Inc.

- The Chemours Company

- The Sherwin-Williams Company

- VITRACOAT

- Whitford Corporation

- Impreglon UK Ltd.

- OKS Spezialschmierstoffe GmbH

Frequently Asked Questions

The global Zero Friction Coatings Market is projected to reach US$ 1.6 Billion by 2033, growing at a CAGR of 5.3% during the forecast period 2026–2033, from an estimated US$ 1.1 Billion in 2026. The market recorded a historical CAGR of 4.8% between 2020 and 2025, driven by growing demand for wear-resistant, energy-efficient tribological coatings across automotive, aerospace, industrial machinery, and renewable energy sectors.

The primary drivers are the global imperative to reduce industrial friction losses, with the U.S. Department of Energy (DOE) and IEA research indicating friction accounts for approximately 23% of world energy consumption, and the electrification of automotive drivetrains, with global EV sales exceeding 14 Million units in 2023 per the IEA, creating specialized demand for dry film and zero friction coating systems compatible with EV motor and gearbox components.

PTFE-Based Coatings dominate with approximately 32% market share, driven by the lowest commercially available static friction coefficient (~0.04), exceptional chemical inertness, thermal stability up to 260°C, and decades of validated application data across automotive, food processing, medical, and industrial sectors. Despite growing PFAS regulatory pressure, PTFE coatings maintain market leadership due to unparalleled and well-documented performance credentials.

North America, led by the United States, is the dominant regional market, supported by the world's largest aerospace and defense coating demand base, with the Aerospace Industries Association (AIA) reporting approximately US$ 900 Billion in U.S. aerospace economic impact annually, combined with a mature automotive tribological coating ecosystem, active PFAS-alternative R&D investment, and a strong semiconductor manufacturing growth trajectory under the U.S. CHIPS and Science Act.

The accelerating expansion of global wind energy represents the most structurally durable growth opportunity, with the Global Wind Energy Council (GWEC) reporting record installations of 117 GW in 2023 and total global capacity surpassing 1,000 GW. Wind turbine gearbox, pitch bearing, and generator components operating under high-load, limited-access conditions create sustained demand for maintenance-minimizing zero friction coating systems specified by major turbine OEMs including Vestas, Siemens Gamesa, and GE Vernova.

Leading market participants include 3M Company, Akzo Nobel N.V., Axalta Coating Systems Ltd., Carl Bechem GmbH, DuPont de Nemours Inc., Endura Coatings, Henkel AG & Co. KGaA, IKV Tribology Ltd., Nippon Paint Holdings Co. Ltd., Poeton Industries Ltd., PPG Industries Inc., RPM International Inc., The Chemours Company, The Sherwin-Williams Company, and VITRACOAT, among specialty tribological coating suppliers including Whitford Corporation and OKS Spezialschmierstoffe GmbH.