- Food Packaging

- Easy Peel Film Packaging Market

Easy Peel Film Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Easy Peel Film Packaging Market by Material (Polyethylene, Linear Low-Density Polyethylene (LLDPE), Others), Application (Food & Beverage, Medical/Pharmaceutical, Others), and Regional Analysis for 2026 - 2033

Easy Peel Film Packaging Market Size and Trends Analysis

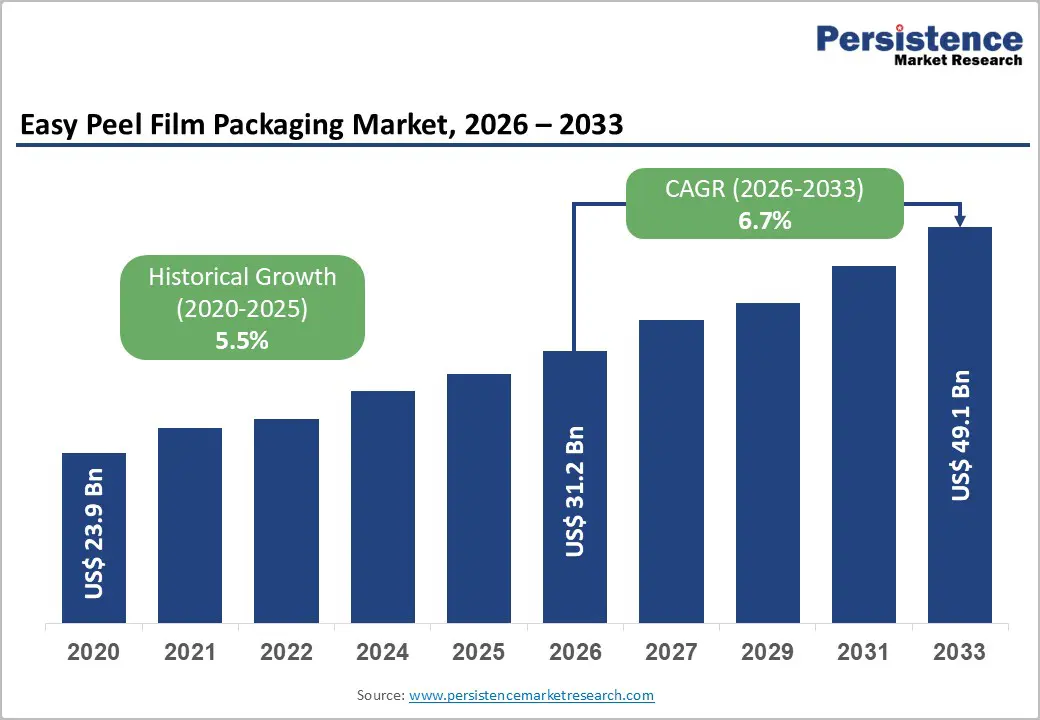

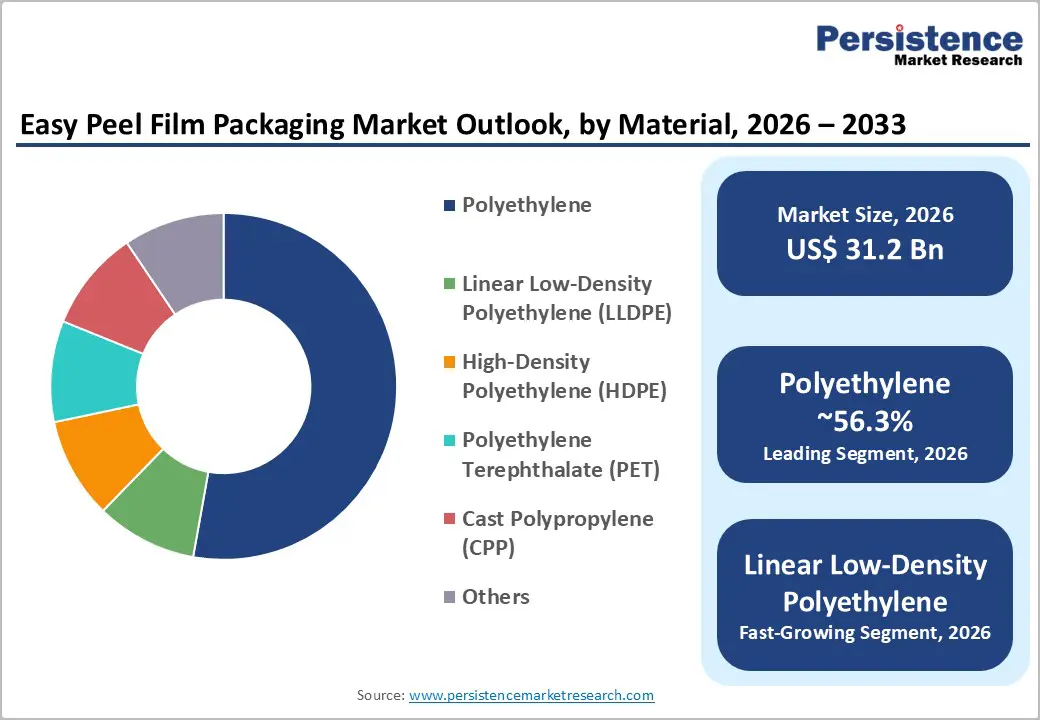

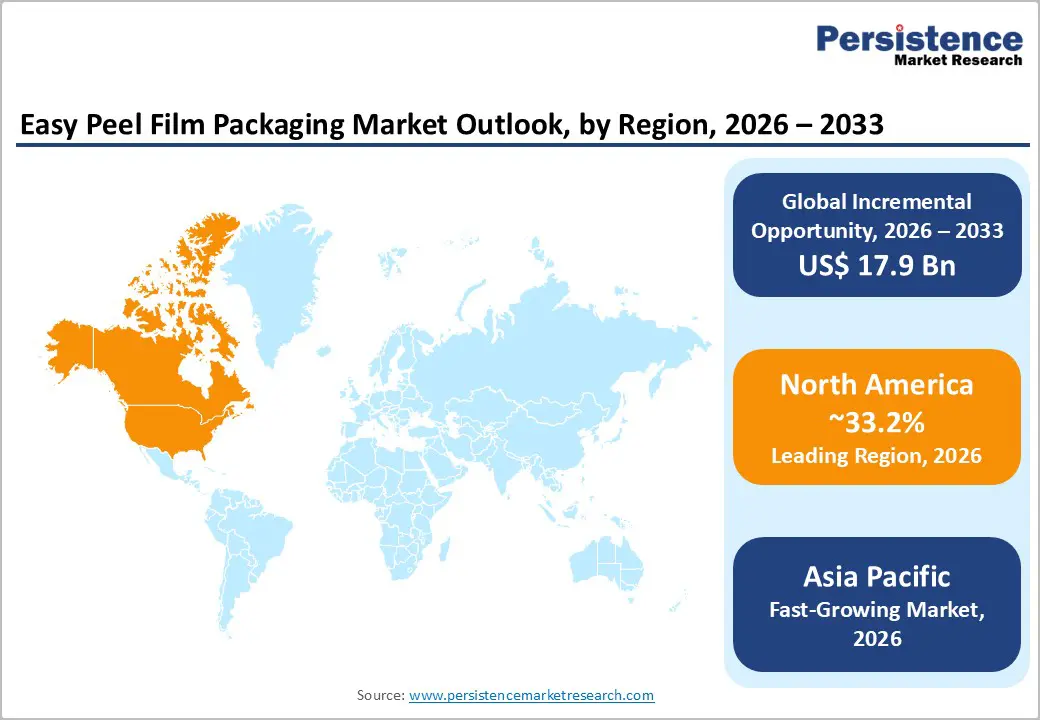

The global easy peel film packaging market size is likely to be valued at US$ 31.2 billion in 2026 and is expected to reach US$ 49.1 billion by 2033, growing at a CAGR of 6.7% between 2026 and 2033, driven by rising packaged and ready-to-eat food consumption, stricter regulatory requirements for tamper-evident medical packaging, and technological advancements in recyclable polymer films.

Manufacturers are prioritizing mono-material structures, operational efficiency, and compliance with global sustainability mandates to secure long-term contracts across multinational supply chains. The market outlook reflects structurally supported demand, anchored in regulatory compliance, convenience-oriented consumption patterns, and expanding cold-chain infrastructure worldwide.

Key Industry Highlights

- Leading Region: North America is projected to hold 33.2% of market share, driven by strong U.S. food processing capacity, pharmaceutical manufacturing leadership, and regulatory emphasis on tamper-evident and recyclable packaging structures.

- Fastest-growing Region: Asia Pacific is projected to grow at the highest regional CAGR, supported by rapid urbanization, cold chain expansion, seafood exports, and polymer production capacity growth in China and India.

- Investment Plans: Significant investments in recyclable mono-material polyethylene film technologies, automated extrusion lines, and healthcare packaging capacity expansion, particularly in the U.S., Germany, China, and India, to meet sustainability mandates and sterile barrier compliance requirements.

- Dominant Material: Polyethylene is anticipated to account for 56.3% share, supported by cost efficiency, heat sealability, and recyclability, aligned with mono-material packaging initiatives.

- Leading Application: Food & beverage is estimated to hold approximately 55.8% share, driven by frozen meals, dairy lids, ready-to-eat products, and growing e-commerce grocery demand.

| Key Insights | Details |

|---|---|

| Easy Peel Film Packaging Market Size (2026E) | US$31.2 Bn |

| Market Value Forecast (2033F) | US$49.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for Convenient and Ready-to-Eat Food Packaging

Global consumption of processed and packaged foods continues to rise, particularly in urban markets across North America and the Asia Pacific. Increased workforce participation and dual-income households are accelerating demand for ready meals, frozen foods, dairy products, and portion-controlled snacks. Easy peel films provide controlled seal strength, extended shelf life, and user-friendly opening without tools, reducing spillage and contamination risks. The food and beverage segment accounts for approximately 55.8% of total market demand, underscoring its structural influence. Easy-peel solutions are widely used for yogurt lids, frozen meal trays, and snack packs, where consistent peel performance and barrier protection are essential. As e-commerce grocery sales expand, packaging durability, combined with consumer convenience, becomes increasingly critical, strengthening long-term demand.

Expansion of Pharmaceutical and Medical Device Packaging Requirements

Global pharmaceutical production and medical device manufacturing have grown steadily, supported by aging populations and increasing healthcare access. Regulatory agencies require tamper-evident and contamination-resistant packaging for sterile products. Easy peel films deliver controlled peel strength, seal validation, and compatibility with sterilization processes, making them suitable for blister packs, diagnostic kits, and surgical device trays. Healthcare packaging compliance has become a mandatory investment area rather than a discretionary cost. Easy peel technology supports adherence to international sterile barrier standards and enhances product safety during transportation and storage. Growth in biologics, injectables, and diagnostic devices further accelerates demand for high-integrity peelable films in regulated healthcare environments.

Shift toward Sustainable and Recyclable Flexible Packaging Materials

Regulatory pressure to reduce plastic waste and improve recyclability is transforming the packaging landscape. Governments across North America and Europe are implementing extended producer responsibility frameworks and recyclability thresholds. Easy-peel films based on polyethylene and linear low-density polyethylene are increasingly being designed as mono-material structures compatible with existing mechanical recycling streams. Manufacturers are investing in downgauging, recyclable film formulations, and improved seal-layer technologies to maintain performance while reducing material usage. Sustainability-driven procurement policies among multinational food and pharmaceutical companies are reinforcing this transition. The shift toward recyclable easy peel films represents a structural transformation that supports medium- to long-term market expansion.

Barrier Analysis - Volatility in Raw Material Prices

Easy peel films rely heavily on petrochemical-derived resins such as polyethylene and polypropylene. Fluctuations in crude oil and natural gas prices directly affect resin costs, which can account for 50-70% of total production expenses. Price volatility reduces margin predictability for converters and increases procurement complexity. Smaller regional manufacturers face greater exposure due to limited hedging capacity and long-term supply contracts. Cost instability can delay capital investments in new extrusion lines and technological upgrades, limiting growth momentum in price-sensitive markets.

Regulatory Pressure on Plastic Waste Management

Plastic packaging remains under scrutiny due to environmental concerns. Governments are implementing stricter waste management policies, including extended producer responsibility programs and recycling mandates. Compliance can increase operational expenses by an estimated 5-10%, depending on jurisdiction. Companies must invest in recyclability certification, redesign packaging formats, and collaborate with recycling infrastructure partners. While sustainability trends create long-term opportunity, short-term compliance costs and regulatory uncertainty may constrain profitability, particularly for small and mid-sized converters.

Opportunity Analysis - Growth in Emerging Consumer Markets

Urbanization and income growth across the Asia Pacific and parts of Africa are expanding demand for packaged foods and consumer goods. Organized retail expansion and improvements in cold storage infrastructure support the adoption of flexible packaging formats. Easy peel films enhance product protection in humid and high-temperature climates, reducing spoilage during transportation. Manufacturers establishing local production facilities in high-growth markets can reduce logistics costs and respond quickly to regional regulatory requirements. Volume-driven growth in the frozen food, dairy, and seafood segments presents scalable opportunities for easy-peel film suppliers.

Technological Integration in High-Barrier and Smart Packaging

Advances in co-extrusion and modified-atmosphere packaging technologies enable the integration of oxygen and moisture barriers into easy-peel structures. Improved polymer blending techniques enhance seal integrity and recyclability compatibility. Functional coatings allow customization of peel force for specific applications, including medical and export-oriented food packaging. Smart packaging features such as traceability codes and digital authentication labels are increasingly incorporated into flexible films. Companies investing in advanced materials science and automation technologies can capture premium segments that require performance differentiation.

Transition toward Mono-Material Recyclable Structures

Global brand owners have announced commitments to achieve 100% recyclable packaging portfolios by 2030. Mono-material polyethylene easy-peel films are compatible with existing recycling systems, positioning them as preferred alternatives to multilayer laminates. Suppliers capable of delivering recyclable structures without compromising barrier performance gain a competitive advantage in procurement processes. Strategic alignment with circular economy principles strengthens long-term customer relationships and supports stable revenue streams.

Category-wise Analysis

Material Insights

Polyethylene is anticipated to account for approximately 56.3% of the market share in 2026, maintaining its position as the leading material segment. Its dominance stems from cost efficiency, strong heat sealability, and reliable moisture barrier performance, which are critical for dairy lids, frozen food trays, portion packs, and snack applications. Polyethylene structures are widely used in yogurt cups, ready-meal containers, and cheese packaging, where consistent peel strength and seal integrity are required. High-Density Polyethylene (HDPE) contributes around 25% share, valued for superior mechanical strength in industrial applications such as rigid-lid sealing and heavy-duty pouches. Polyethylene Terephthalate (PET) continues to gain traction in premium packaging formats requiring clarity, stiffness, and alignment with established PET recycling streams.

Linear Low-Density Polyethylene (LLDPE) is projected to be the fastest-growing material segment. LLDPE offers enhanced flexibility, puncture resistance, and precise peel-force control, making it particularly suitable for high-speed filling operations in frozen food and processed meat packaging. For example, frozen vegetable bags and microwaveable meal trays often incorporate LLDPE sealant layers to optimize openability without compromising barrier performance. Cast Polypropylene (CPP) is used in retort and high-temperature applications, while biodegradable and specialty polymer blends are emerging in sustainability-focused product lines. Ongoing innovation emphasizes downgauging, mono-material design, and improved compatibility with mechanical recycling systems while maintaining compliance with food-contact and healthcare regulations.

Application Insights

The food & beverage segment is expected to account for approximately 55.8% of the market share in 2026, making it the dominant application segment. Demand is driven by frozen meals, yogurt lids, ready-to-eat trays, snack packs, and portion-controlled dairy products. Easy-peel films enhance hygiene, reduce contamination risk, and improve the user experience by enabling tool-free opening. For instance, peelable lidding films used in single-serve yogurt cups and microwave-ready meal trays combine barrier protection with controlled seal strength. The continued growth of online grocery platforms and private-label packaged foods reinforces demand for durable yet consumer-friendly packaging formats.

Medical and pharmaceutical applications are projected to be the fastest-growing segment during the forecast period. Expansion in diagnostic kits, biologics, surgical devices, and sterile medical trays is increasing the need for tamper-evident and contamination-resistant packaging. Easy peel films are widely used in blister packs for tablets, sterile device pouches, and test kit packaging, where controlled peel performance ensures product safety and regulatory compliance. Industrial applications, including toner cartridges and electronic component packaging, provide stable demand due to the need for dust and moisture protection. Consumer goods applications such as wipes, detergents, and personal care products also leverage peelable formats for resealability and controlled dispensing, contributing incremental growth across diversified end markets.

Regional Insights

North America Easy Peel Film Packaging Market Trends - FDA-Regulated Sterile Barrier Demand, Private-Label Food Growth, and Recyclable Mono-Material Innovation

North America is projected to hold the largest share of the market, accounting for 33.2% of the market in 2026. The U.S. dominates regional demand due to its advanced food-processing infrastructure, large-scale retail distribution networks, and a strong pharmaceutical manufacturing base. Strict regulatory oversight by the U.S. Food and Drug Administration (FDA) reinforces demand for tamper-evident and sterile barrier packaging formats, particularly in medical devices and prescription drug applications.

High per capita consumption of packaged foods and frozen meals continues to support stable demand. Major food brands such as Kraft Heinz and General Mills increasingly rely on peelable lidding films for yogurt, ready meals, and snack packs, where controlled peel strength and moisture barrier integrity are critical. Growth in private-label grocery products across retailers such as Walmart and Costco further expands the addressable market for cost-efficient polyethylene-based easy peel films.

On the innovation front, companies such as Amcor and Berry Global have expanded recyclable mono-material polyethylene film portfolios in North America to meet state-level Extended Producer Responsibility (EPR) requirements and evolving recyclability targets. Sealed Air has also strengthened its healthcare packaging capabilities through facility expansions focused on sterile barrier solutions. These developments reinforce the region’s leadership in automation, high-speed extrusion technologies, and sustainable film design. Investments in chemical recycling infrastructure across the U.S. are expected to further support the adoption of recyclable easy peel structures.

Europe Easy Peel Film Packaging Market Trends - PPWR-Driven Material Transition, Recyclability Mandates, and Cross-Border Sustainable Packaging Standardization

Europe represents a mature yet innovation-driven market characterized by regulatory harmonization and sustainability mandates. Germany, the U.K., France, Spain, and Italy collectively account for a substantial portion of regional revenue. The European Union’s Packaging and Packaging Waste Regulation (PPWR) framework emphasizes recyclability thresholds, waste reduction targets, and material traceability requirements, directly influencing the selection of easy-peel film materials.

Germany’s advanced pharmaceutical manufacturing sector supports steady demand for sterile peelable films in blister packs and medical trays. In the U.K., the Plastic Packaging Tax has accelerated the shift toward recyclable polyethylene-based structures with higher recycled content. Companies such as Mondi and Constantia Flexibles have launched recyclable mono-material flexible packaging solutions aimed at replacing multi-layer laminates in food and healthcare applications.

These product introductions are reshaping procurement criteria among European food processors and healthcare suppliers. France and Spain show consistent growth in dairy, seafood, and ready-meal packaging. Retail chains such as Carrefour and Tesco have committed to reducing non-recyclable packaging in their private-label portfolios, increasing demand for compliant easy-peel film formats. Investment in bio-based and downgauged polyethylene structures is rising, particularly in Northern and Western Europe. Although regulatory compliance increases operational costs, harmonized standards across the EU facilitate cross-border trade and promote scalable innovation in recyclable film technologies.

Asia Pacific Easy Peel Film Packaging Market Trends - Polymer Production Scale, Export-Led Food Packaging Expansion, and High-Growth Pharmaceutical Applications

Asia Pacific is expected to be the fastest-growing regional market, driven by urbanization, income growth, and expanding cold-chain logistics. China, Japan, India, South Korea, and ASEAN countries drive the majority of regional demand. China’s large-scale polymer production capacity and integrated manufacturing ecosystem position it as both a major consumer and exporter of easy-peel film packaging. Domestic food brands and seafood exporters increasingly adopt peelable films to meet international hygiene and quality standards.

In Japan, stringent pharmaceutical packaging regulations and high consumer expectations for convenience support demand for high-precision peelable films. Companies such as Toray Industries and regional converters continue to invest in advanced polymer technologies to enhance barrier performance and seal reliability. Japan’s focus on quality assurance strengthens demand in both healthcare and premium food packaging segments. India is emerging as a high-growth market due to expansion in organized retail and increasing consumption of packaged dairy and frozen foods.

Companies such as UFlex and Cosmo Films have expanded specialty film production capacities to serve both domestic and export markets. Growth in seafood exports from India, Vietnam, and Thailand also increases demand for leak-resistant and hygienic peelable packaging formats. Foreign direct investment in flexible packaging facilities across ASEAN markets is improving local production capabilities. Governments across the region are tightening plastic waste management policies, encouraging manufacturers to develop recyclable polyethylene-based structures. This regulatory shift, combined with cost-efficient manufacturing and strong export orientation, positions Asia Pacific as a central hub for volume-driven growth in the market.

Competitive Landscape

The global easy peel film packaging market is moderately fragmented. Leading multinational packaging companies collectively account for approximately 40-50% of total revenue. Large players differentiate through advanced R&D capabilities, global supply networks, and sustainability-focused product portfolios. Regional converters compete on customization, pricing flexibility, and local supply responsiveness. Leading companies prioritize recyclable mono-material innovation, automation to reduce production costs, and geographic expansion in high-growth Asian markets. Long-term supply agreements with food and pharmaceutical manufacturers enhance revenue stability. Investment in regulatory compliance and material science capabilities remains a core competitive differentiator.

Key Industry Developments:

- In June 2025, KM Packaging introduced the K-Peel 4G mono PET easy-peel lidding film, designed for APET and rPET trays with improved peel performance and sustainability features for ambient, chilled, and frozen food applications.

- In February 2026, Amcor announced the expansion of its North American polyethylene (PE) shrink film portfolio through its combined capabilities with Berry Global, positioning it as the largest PE overwrap and shrink film producer in the region to support food, beverage, and industrial applications.

Companies Covered in Easy Peel Film Packaging Market

- Amcor plc

- Berry Global Group, Inc.

- Sealed Air Corporation

- Mondi Group

- Sonoco Products Company

- Constantia Flexibles

- Huhtamaki Oyj

- Coveris Holdings S.A.

- ProAmpac LLC

- Winpak Ltd.

- UFlex Ltd.

- Toray Industries, Inc.

- Cosmo Films Ltd.

- Clondalkin Group

- Schur Flexibles Group

- Transcontinental Inc.

- Wipak Group

- FlexFilms (UFLEX Group)

Frequently Asked Questions

The easy peel film packaging market is estimated to be valued at US$31.2 billion in 2026.

The global easy peel film packaging market is projected to reach US$49.1 billion by 2033.

Key trends include rising adoption of recyclable mono-material polyethylene films, increasing demand for tamper-evident and sterile barrier packaging, growth in convenience and ready-to-eat food packaging, and technological advancements in controlled peel strength and resealable film structures.

The food & beverage segment leads the market, accounting for the largest share due to strong demand from dairy, frozen food, processed meat, and ready-meal packaging applications.

The easy peel film packaging market is expected to grow at a CAGR of 6.7% between 2026 and 2033.

Major players include Amcor plc, Berry Global Group, Inc., Sealed Air Corporation, Mondi Group, and Constantia Flexibles.