- Food Packaging

- Converter Aluminum Foil Market

Converter Aluminum Foil Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Converter Aluminum Foil Market by Product Type (Pouches (Flexible Laminates), Wraps, Laminated Tubes, Foil Lids, Blister Packs / Strip Packs, Others)), Foil Type (Standard Aluminum Foil, Embossed Foil, Coated / Printed Foil, Laminated Foil (multi-layer structures)), Industry (Food Industry, Pharmaceutical & Healthcare Industry, Consumer Goods & Personal Care, Industrial (HVAC, Electronics, Insulation)), and Regional Analysis for 2026 to 2033

Converter Aluminum Foil Market Share and Trends Analysis

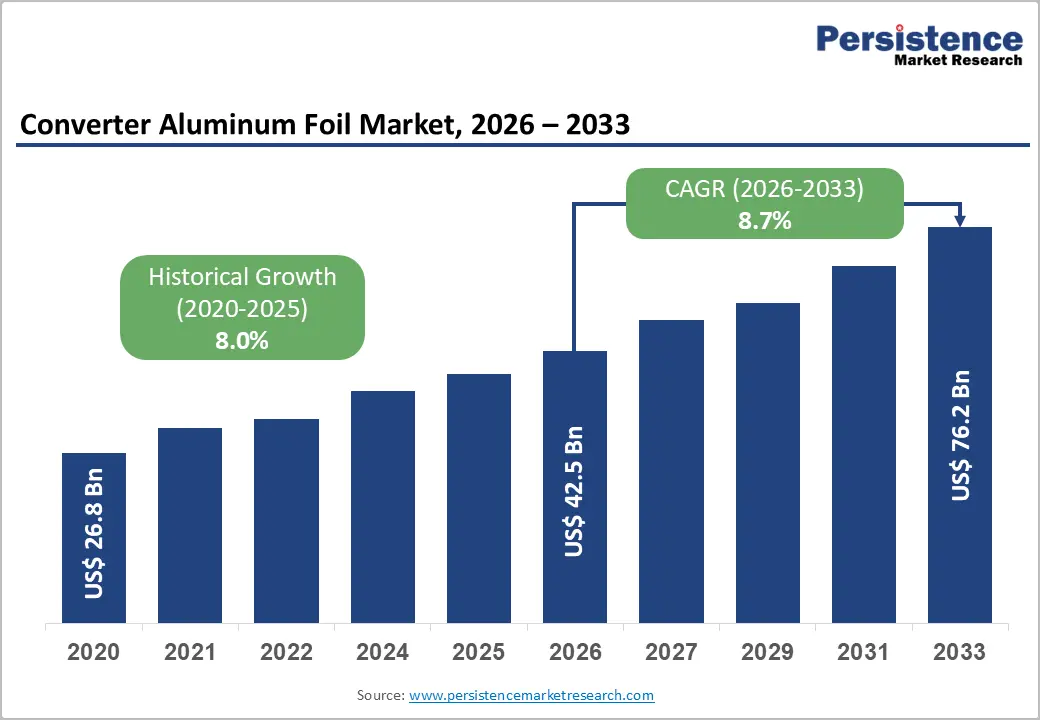

The global converter aluminum foil market size is likely at US$ 42.5 billion in 2026 and is projected to reach US$ 76.2 billion by 2033, growing at a CAGR of 8.7% between 2026 and 2033.

Rising global demand for flexible, high-barrier packaging film across the food and pharmaceutical sectors is the primary market driver. Regulatory mandates restricting single-use plastics are accelerating the substitution of plastic packaging with aluminum foil laminates and pouches. Asia Pacific's expanding packaged food consumption and pharmaceutical production growth, combined with Europe's focus on sustainable converter foil formats, reinforce structural volume expansion through 2033.

Key Industry Highlights

- Leading Product: Pouches (Flexible Laminates) lead product type at 28.6% share; blister packs /strip packs are the fastest-growing product at 9.0% CAGR, driven by pharmaceutical industry expansion.

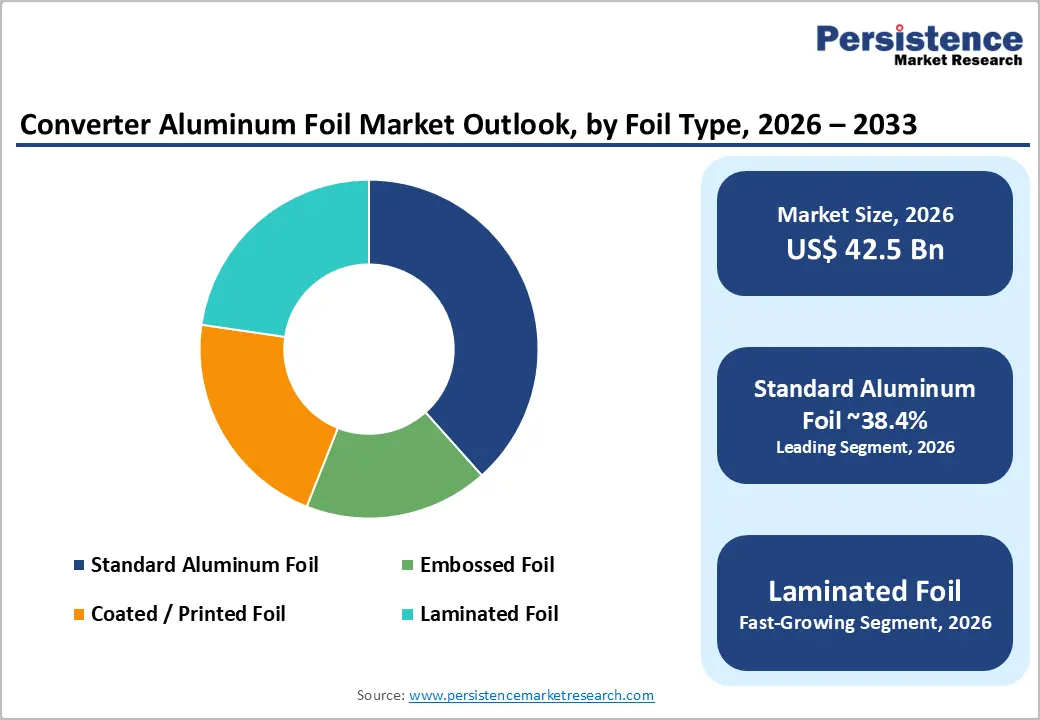

- Leading Foil Type: Standard aluminum foil leads foil type at 38.4% share; laminated foil is expected to reach 10.2% CAGR, driven by high-barrier pharmaceutical and retort food packaging demand.

- Dominant Industry: Food Industry leads end-use with a 36.8% share; the pharmaceutical & healthcare industry is expected to grow at a 9.4% CAGR, backed by global drug expenditure projected at US$ 1.9 Tn by 2027.

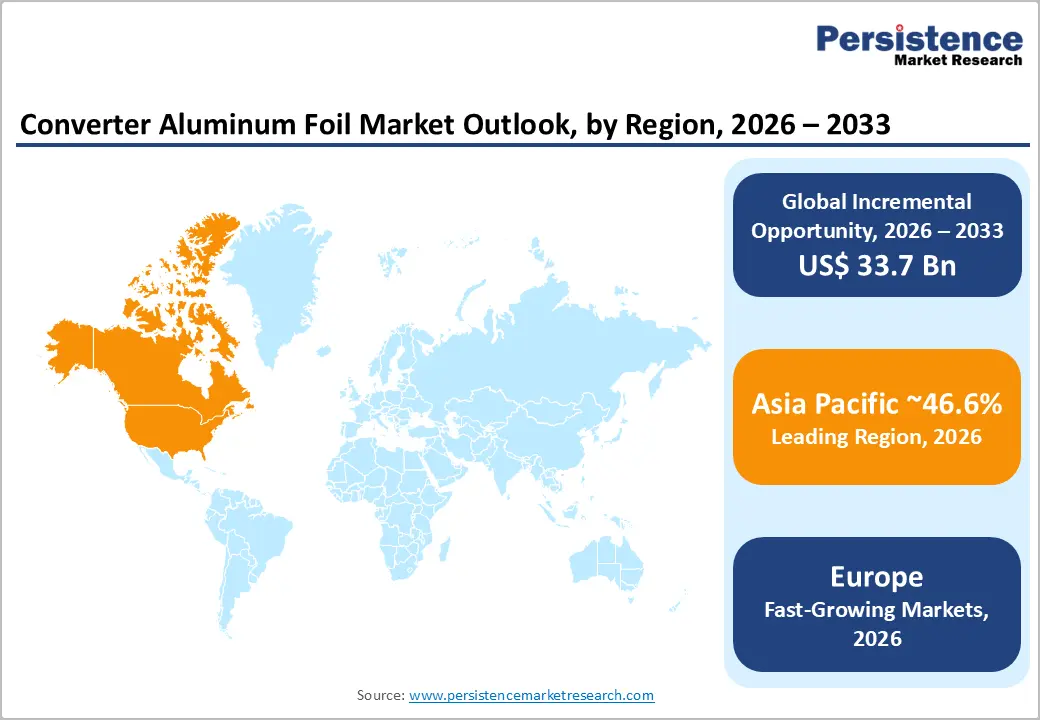

- Regional Leadership: Asia Pacific dominates with 46.6% market share in 2025; Europe is likely to achieve a 7.7% CAGR, driven by 15 newly commissioned high-barrier laminate plants and EU sustainability mandates.

- Opportunities: Amcor, Novelis-Hindalco, and Constantia Flexibles are expanding pharmaceutical-grade lamination capacity and closed-loop recycling programs across Europe and the Asia Pacific post-2024.

Market Dynamics Analysis

Drivers - Surging Global Flexible Packaging Demand and Single-Use Plastic Substitution

The global flexible packaging market, of which converter aluminum foil is a foundational substrate, is experiencing structural expansion driven by urbanization, rising disposable incomes, and the rapid proliferation of convenience and ready-to-eat food formats. According to the World Economic Forum, global aluminum demand is projected to grow approximately 40% by 2030, reinforcing the upstream volume pipeline for converter foil production. European Union directives restricting single-use plastics under the Single-Use Plastics Directive (SUPD) mandate that packaged goods manufacturers transition to aluminum-based flexible laminates that offer superior recyclability and regulatory compliance.

This regulatory transition is creating structural substitution demand in both food and consumer goods packaging categories. In the pharmaceutical sector alone, aluminum foil for blister packaging accounted for approximately 1 million metric tons globally in 2023, according to industry data, underscoring the scale of captive converter foil demand. OEM procurement commitments from major food, confectionery, and pharmaceutical brands are locking in long-term supply agreements with converter foil manufacturers, providing revenue visibility and investment confidence across the value chain.

Pharmaceutical Sector Expansion and Sterile Packaging Requirements

Global pharmaceutical expenditure is projected to reach US$ 1.9 trillion by 2027 (IQVIA Global Use of Medicines Report), and aluminum foil's role as the preferred sterile packaging substrate for blister packs, cold-form foil, and strip packs is intensifying in parallel. The aluminum foil segment within pharmaceutical blister packaging is projected to grow at a CAGR of 8.6% through 2034, driven by demand for superior barrier protection against moisture, oxygen, and light for sensitive pharmaceutical formulations.

International regulatory standards, including U.S. FDA 21 CFR regulations, EU Directive 2011/62/EU on falsified medicines, and WHO's Good Manufacturing Practices, mandate high-integrity, tamper-evident aluminum foil packaging for pharmaceutical distribution, creating non-negotiable specification requirements for converter foil producers. The rapid expansion of biologics, specialty drugs, nutraceuticals, and vaccine packaging, each demanding cold-form or high-barrier aluminum converter foil, further accelerates this demand trajectory and reinforces pharmaceuticals as the fastest-growing end-use application for the global converter foil market.

Restraints - Regulatory Complexity Across Packaging and Food Contact Standards

Converter aluminum foil manufacturers face a fragmented and continuously evolving regulatory landscape governing food contact materials, recyclability declarations, and chemical migration limits across jurisdictions. The EU's Regulation (EC) No. 1935/2004 on food contact materials, the U.S. FDA's Food Contact Notification (FCN) framework, and divergent Asian national standards require separate testing, documentation, and certification cycles. Non-compliance risks include market withdrawal, supply contract termination, and reputational penalties, all of which structurally disadvantage smaller manufacturers without dedicated regulatory affairs capabilities.

Competition from Sustainable Alternative Flexible Packaging Materials

Converter aluminum foil faces competitive displacement pressure from emerging bio-based films, metalized barrier films, and recyclable mono-material flexible packaging formats being developed by materials innovators in response to circular economy mandates. The European Plastics Pact and comparable sustainability commitments by global FMCG brands are driving packaging engineers to evaluate aluminum foil alternatives that achieve recyclable monomaterial structures, particularly for pouches and wraps. While aluminum's barrier performance remains superior, the growing R&D investment in alternative substrates presents a medium-term structural competitive risk requiring converter foil manufacturers to accelerate sustainability and recyclability positioning.

Opportunities - Laminated Foil Innovation for Pharmaceutical and Specialty Applications

The development of next-generation multi-layer laminated aluminum foil, incorporating functional coatings, anti-counterfeiting printing, and intelligent packaging features, represents a high-value growth opportunity that commands significant pricing premiums over standard converter foil. Pharmaceutical companies are increasingly specifying cold-form laminated foil for unit-dose packaging of biologics and high-value specialty drugs, creating a specification-driven demand pipeline that standard foil cannot address.

Beyond pharmaceuticals, multi-layer laminated structures are finding applications in high-barrier food pouches, premium cosmetic packaging, and industrial insulation laminates, broadening the addressable market for laminated foil manufacturers. The global laminated flexible packaging market is estimated at over US$ 200 Bn by 2030, of which aluminum foil-based laminates account for a significant share of the substrate market. Manufacturers investing in precision coating, high-speed printing, and multi-material lamination capabilities are positioned to capture outsized margin expansion from this premium segment.

Asia Pacific Emerging Market Penetration and Localized Manufacturing

South and Southeast Asian markets, particularly India, Vietnam, Indonesia, and Bangladesh, are witnessing rapid expansion in fast-moving consumer goods (FMCG) manufacturing, pharmaceutical export capacity, and modern retail infrastructure, all of which are driving converter aluminum foil demand at scale. India's packaged food market is projected to exceed US$ 100 Bn by 2030 (Ministry of Food Processing Industries data), creating volume-scale demand for pouches, wraps, and foil lids as primary converter foil applications.

ASEAN's pharmaceutical export industry, valued at over US$ 10 Bn annually, is increasingly requiring GMP-compliant aluminum blister and strip packaging to meet export standards for the EU and U.S. markets. Manufacturers establishing localized converter foil production facilities in these markets gain significant supply chain cost advantages, rapid customer responsiveness, and eligibility for government-backed industrial production incentives, making geographic expansion into Southeast and South Asia a strategically compelling investment thesis for established players.

Category-wise Analysis

Product Type Insights

Pouches (Flexible Laminates) lead the product type segment with a 28.6% market share in 2026. Their dominance reflects the global packaged goods industry's preference for lightweight, resealable, and barrier-effective packaging formats across food, pharmaceutical, and consumer goods categories. Pouches offer structural versatility, accommodating liquid, solid, and powder contents, while delivering superior shelf-life extension versus alternative formats.

Stand-up pouches and retort pouches have become the default format for ambient food and infant nutrition packaging across both developed and emerging markets. The Wraps and Foil Lids segments retain meaningful share in confectionery and dairy, but neither approaches Pouches' volume scale or growth momentum. Pouch dominance is expected to intensify with continued e-commerce and convenience food growth.

Blister Packs / Strip Packs is the fastest-growing product type at a CAGR of 9.0% through 2033. Accelerating pharmaceutical production, stringent drug safety packaging regulations, and expanding generic medicine manufacturing in Asia are the primary drivers of this exceptional growth trajectory.

Foil Type Insights

Standard aluminum foil leads the foil type segment with a 38.4% market share in 2026. Its dominance is rooted in broad application compatibility, established supply chains, cost-competitive production, and universal regulatory approval for food contact and pharmaceutical packaging across all major markets. Standard foil serves as the foundational substrate for wraps, basic laminates, and foil lids, high-volume applications that require consistent quality rather than functional differentiation.

Coated/Printed and Embossed Foil serve premium branding applications in confectionery and cosmetics, while Laminated Foil targets high-barrier pharmaceutical and retort packaging. Standard foil's volume scale across commodity applications secures its leadership position, though Laminated Foil is progressively capturing value share.

Laminated Foil (multi-layer structures) is the fastest-growing foil type at a CAGR of 10.2% through 2033. Pharmaceutical blister pack specifications, food retort pouch requirements, and premium cosmetic packaging demands are collectively driving adoption of high-barrier multi-layer laminated foil architectures at accelerating rates.

Industry Insights

The food industry leads the end-use segment with a 36.8% share in 2026, driven by the global processed and packaged food sector's dependence on aluminum foil for moisture barrier, oxygen protection, and shelf-life extension across product categories, including snacks, dairy, bakery, confectionery, and ready meals. Per-capita packaged food consumption growth in developing economies, particularly India, China, and Southeast Asia, is expanding the food segment's addressable converter foil demand base. The Industrial and Consumer Goods segments serve important niche roles, but neither approaches Food's structural volume advantage embedded across global FMCG supply chains. Food's dominance is expected to persist throughout the forecast period.

The pharmaceutical & Healthcare Industry is the fastest-growing end-use segment at a CAGR of 9.4% through 2033. The rise in global pharmaceutical production, the expansion of cold-chain drug distribution, and the growing adoption of unit-dose blister packaging across regulated and emerging markets collectively drive this sector's exceptional growth in converter foil demand.

Regional Insights

North America Converter Aluminum Foil Market Insights

North America holds a considerable 21.8% share of the global market in 2025, anchored by the United States' mature packaged food sector, world-class pharmaceutical manufacturing base, and robust regulatory infrastructure governing food contact materials and drug packaging. The U.S. FDA's requirements for tamper-evident pharmaceutical packaging and the Consolidated Appropriations Act's drug traceability provisions drive consistent demand for high-specification aluminum converter foil in pharmaceutical applications.

Canada contributes meaningful food processing and industrial insulation converter foil demand. U.S.-based converter foil manufacturers benefit from proximity to major FMCG brands' packaging innovation centers, enabling co-development of functional laminate solutions.

North America's growth is driven by pharmaceutical blister-pack adoption, sustainable packaging substitution mandates, and premiumization in food and cosmetic packaging formats that require coated and printed converter foil. The region serves as a critical R&D hub for next-generation functional foil laminate technologies.

Europe Converter Aluminum Foil Market Share

Europe is a technology-leading and regulation-driven market poised to grow at a prominent 7.7% CAGR through 2033, propelled by the EU's Single-Use Plastics Directive, the European Green Deal packaging targets, and the European Food Safety Authority's (EFSA) rigorous food contact materials regulation. Germany and France serve as primary hubs for converter foil manufacturing and innovation, supplying pan-European FMCG and pharmaceutical brands with high-barrier laminated and printed foil formats.

The commissioning of 15 new European plants specializing in high-barrier laminates, reported in 2025, reflects the region's active capacity investment. Spain and the U.K. contribute food and pharmaceutical packaging converter foil demand across their domestic production sectors. Europe's emphasis on circular economy legislation, pharmaceutical packaging innovation agenda, and premiumization of food packaging formats, particularly in organic, nutraceutical, and ready-meal categories, defines the region's key investment and growth themes through 2033.

Asia Pacific Converter Aluminum Foil Market Insights

Asia Pacific commands the dominant 46.6% share of the global market in 2025 and represents the primary volume growth engine through 2033. China drives regional dominance through its mass-market packaged food sector, rapidly expanding pharmaceutical export industry, and large-scale domestic converter foil manufacturing capacity, with manufacturers such as Xiamen Xiashun Aluminium Foil and China Hongqiao Group supplying high-volume global clients.

India's packaged FMCG sector expansion and pharmaceutical manufacturing scale-up are driving dual-channel growth, while Japan is advancing high-value, premium foil laminate innovation. ASEAN markets, particularly Vietnam and Indonesia, are seeing accelerated investment in FMCG and pharma packaging.

The region's manufacturing cost advantages, government industrial incentive programs, and rapidly growing middle-class consumer base make Asia Pacific the most strategically critical production and demand growth region for converter aluminum foil through 2033.

Competitive Landscape

The global Converter Aluminum Foil Market is moderately consolidated at the top tier, with leading players, Amcor plc, Novelis Inc., and UACJ Corporation, collectively accounting for approximately 35% of global market revenue in 2025. Tier-2 players, including Reynolds Group, Hindalco, and China Hongqiao Group, control approximately 30%, while the remaining share is distributed among regional specialists. Market leaders differentiate through proprietary high-barrier lamination technologies, pharmaceutical-grade certifications, closed-loop aluminum recycling capabilities, and global distribution infrastructure.

Sustainability-driven innovation, pharmaceutical-grade capability development, and geographic capacity expansion into Asia Pacific and the Middle East are the dominant strategic themes reshaping competitive positioning. Leading firms are investing in AI-driven process optimization, blockchain traceability for food safety, and ultra-thin high-strength foil development to command pricing premiums and long-term OEM contracts.

Strategic Developments

- In June 2025, Hindalco Industries completed a strategic reinforcement of its Novelis subsidiary, integrating advanced aluminum rolling and recycling capabilities to expand closed-loop converter foil supply for global food and pharmaceutical packaging customers.

- In March 2024, Constantia Flexibles announced the expansion of its pharmaceutical-grade aluminum converter foil lamination capacity in Europe, targeting growing demand for cold-form blister packaging from pharmaceutical OEMs scaling specialty drug production.

- In January 2024, TekniPlex launched a pharmaceutical-grade PET-aluminum hybrid blister material incorporating 30% post-consumer recycled content, compliant with EU and U.S. Pharmacopoeia standards, targeting sustainable pharmaceutical converter foil applications.

- In 2025, European converter foil manufacturers commissioned 15 new high-barrier laminate production plants across Germany and France, targeting regulatory-compliant food and pharmaceutical laminate formats under EU Single-Use Plastics and Packaging Regulation frameworks.

- In September 2024, Amcor plc advanced its closed-loop aluminum foil recycling program in Asia Pacific, partnering with downstream FMCG brands to establish collection and reprocessing infrastructure for post-consumer converter foil laminates, targeting circular economy compliance.

Companies Covered in Converter Aluminum Foil Market

- Amcor plc

- Novelis Inc.

- UACJ Corporation

- Hindalco Industries Ltd.

- Constantia Flexibles

- Reynolds Group Holdings

- China Hongqiao Group Limited

- Symetal S.A.

- Eurofoil Luxembourg S.A.

- Hulamin Limited

- Alibérico Packaging

- Zhejiang Junma Aluminium Industry

- Xiamen Xiashun Aluminium Foil Co., Ltd.

- Ess Dee Aluminium Ltd.

- ACM Carcano Antonio S.p.A.

Frequently Asked Questions

The converter aluminum foil market is valued at US$ 42.5 Bn in 2026 and is projected to reach US$ 76.2 Bn by 2033.

Surging flexible packaging demand, single-use plastic substitution regulations, and pharmaceutical sector growth requiring high-barrier sterile converter foil are the primary growth drivers.

The converter aluminum foil market is projected to grow at a CAGR of 8.7% from 2026 to 2033.

Multi-layer laminated foil innovation for pharmaceutical packaging and localized converter foil manufacturing expansion across South and Southeast Asia represent the most actionable growth opportunities.

Amcor plc, Novelis Inc., UACJ Corporation, Hindalco Industries, Constantia Flexibles, Reynolds Group, China Hongqiao Group, Symetal S.A., and Eurofoil Luxembourg are the leading global participants.