- Construction & Engineering

- Concrete Protective Liner Market

Concrete Protective Liner Market Size, Share, and Growth Forecast 2026 - 2033

Concrete Protective Liner Market by Product Type (Geomembranes, Geotextiles, Clay Liners, Composite Liners, Spray-Applied Liners), Material Type (Polyethylene – HDPE/LDPE, Polypropylene, Polyvinyl Chloride – PVC, Polyvinylidene Fluoride – PVDF, Others), Application (Water Management, Waste Management, Mining Operations, Chemical Processing Plants, Infrastructure Protection), Industry and Regional Analysis, 2026 - 2033

Concrete Protective Liner Market Size and Trend Analysis

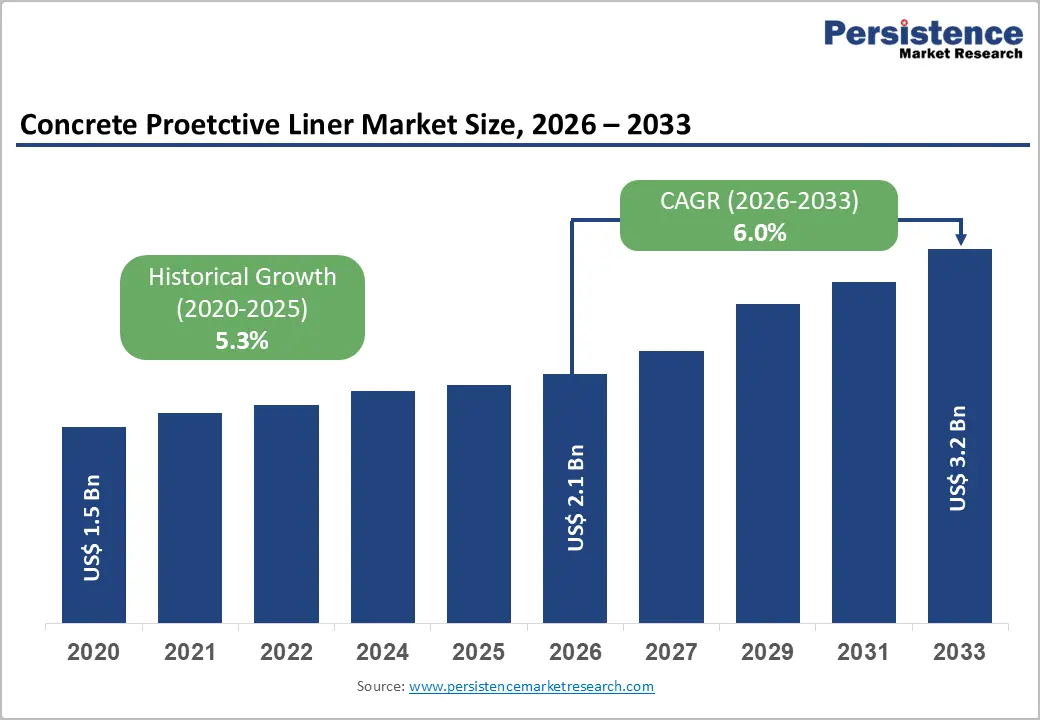

The global concrete protective liner market size is expected to be valued at US$ 2.1 billion in 2026 and is projected to reach US$ 3.2 billion by 2033, growing at a CAGR of 6.0% between 2026 and 2033. The market expansion is underpinned by intensifying global regulatory mandates for environmental containment, accelerating infrastructure rehabilitation investment, and growing industrial demand for durable corrosion-resistant lining systems in water management, mining, and chemical processing facilities.

Governments across North America, Europe, and the Asia Pacific are enforcing increasingly stringent environmental protection standards for groundwater contamination prevention and industrial wastewater containment, creating non-discretionary procurement demand for high-performance concrete protective liner solutions. Simultaneously, aging public water and wastewater infrastructure in developed economies and rapid new industrial construction in emerging markets are driving consistent, multi-cycle demand for geomembrane, spray-applied, and composite liner systems across diverse application verticals.

Key Industry Highlights:

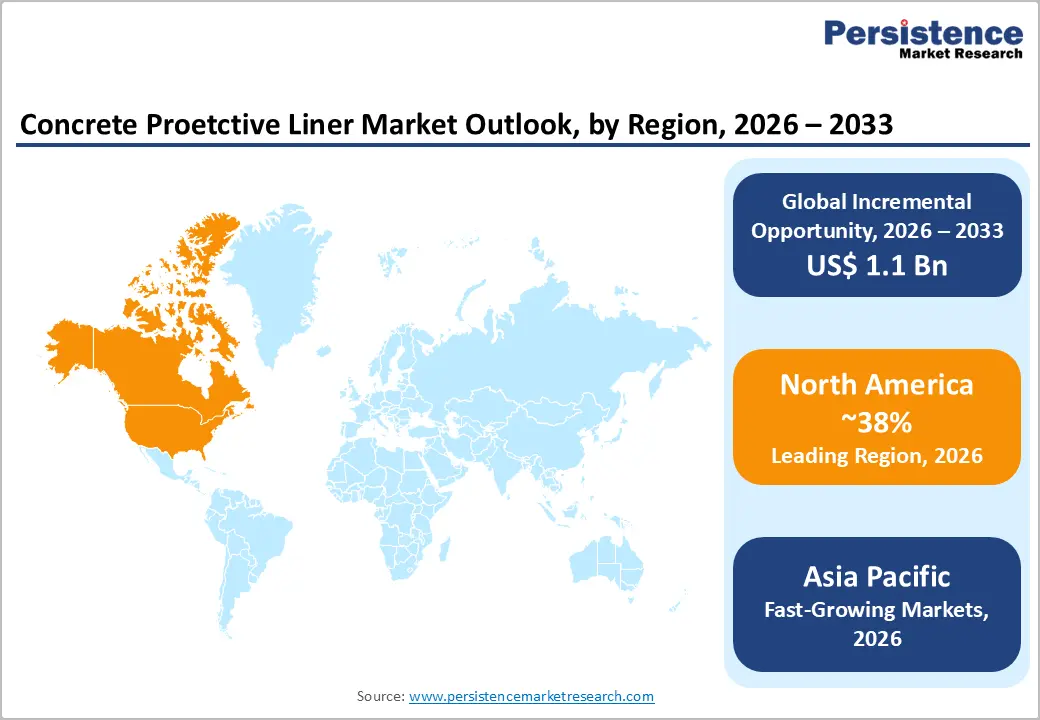

- Leading Region: North America leads the global Concrete Protective Liner market with approximately 38% share in 2025, driven by the EPA’s RCRA regulatory framework, the IIJA’s US$ 55 billion water infrastructure investment, and the United States’ position as the world’s foremost center for liner technology innovation.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market through 2033, fueled by China’s industrial environmental compliance push under the Ministry of Ecology and Environment, India’s Jal Jeevan Mission water infrastructure rollout, and rapidly expanding mining tailings management investment across the region.

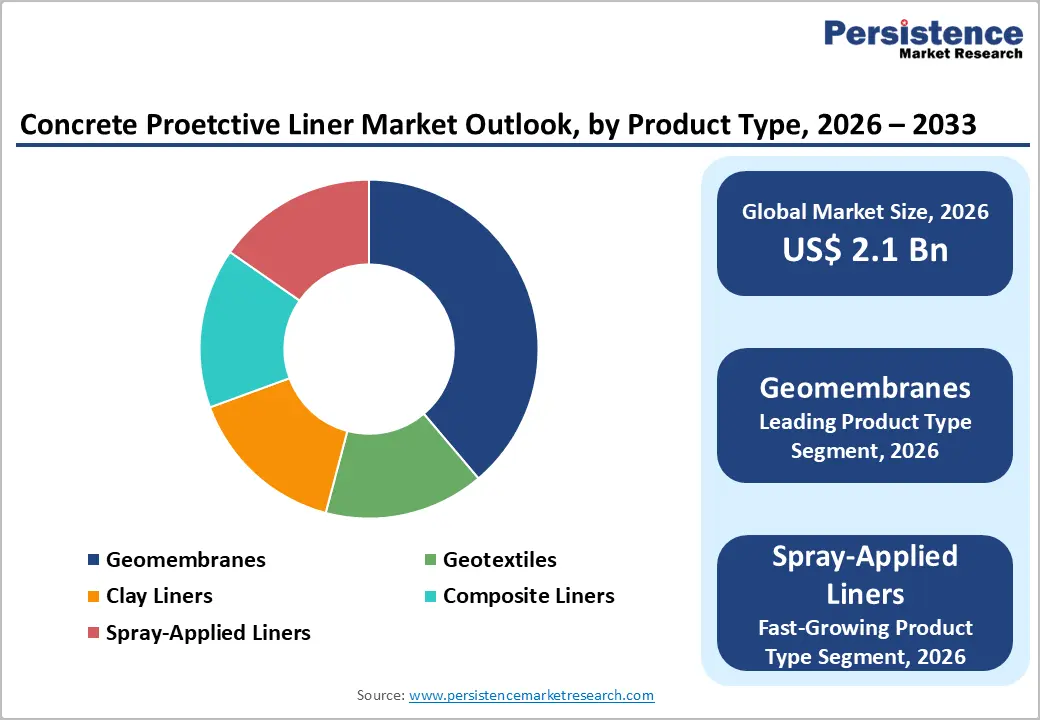

- Dominant Segment: Geomembranes dominate the Product Type category with approximately 35% share in 2025, institutionalized by EPA RCRA mandates, GRI GM13 certification standards, and their proven deployment across the world’s most regulated landfill, mining, and water containment infrastructure environments.

- Fastest Growing Segment: Spray-Applied Liners are the fastest-growing product type segment during 2026–2033, uniquely positioned to capture the rapidly expanding infrastructure rehabilitation market where their application to irregular concrete substrates without structural dismantling delivers decisive cost and operational advantages.

- Key Opportunity: A pivotal market opportunity lies in mining sector tailings management compliance with the Global Industry Standard on Tailings Management (GISTM), driving systematic double-liner composite system upgrades at major mining facilities operated by Rio Tinto, BHP, Anglo American, and other global mining majors through 2033.

| Key Insights | Details |

|---|---|

|

Concrete Protective Liner Market Size (2026E) |

US$ 2.1 Billion |

|

Market Value Forecast (2033F) |

US$ 3.2 Billion |

|

Projected Growth CAGR (2026–2033) |

6.0% |

|

Historical Market Growth (2020–2025) |

5.3% |

DRO Analysis

Drivers - Stringent Environmental Regulations Mandating Industrial Containment Lining Systems

Tightening regulatory frameworks governing industrial waste containment, groundwater protection, and hazardous material management are creating structurally robust, non-discretionary demand for concrete protective liner products. In the United States, the Environmental Protection Agency (EPA) enforces comprehensive liner requirements for municipal solid waste landfills under Subtitle D of the Resource Conservation and Recovery Act (RCRA), mandating composite liner systems comprising a geomembrane over a compacted clay layer. The EPA also prescribes liner system requirements for hazardous waste facilities under Subtitle C, extending obligations to mining tailings impoundments and industrial wastewater lagoons. In the European Union, the Industrial Emissions Directive (IED) and the Landfill Directive (1999/31/EC) impose similarly rigorous containment lining requirements on industrial and municipal waste disposal sites. According to the European Environment Agency (EEA), over 150,000 regulated industrial sites across EU member states are subject to containment infrastructure compliance obligations, generating a sustained, large-scale procurement pipeline for certified concrete protective liner solutions through 2033.

Accelerating Global Investment in Water and Wastewater Infrastructure

Globally escalating investment in water supply, stormwater management, and wastewater treatment infrastructure is serving as a primary and expanding demand driver for concrete protective liner products. The United Nations (UN) estimates that over 2 billion people globally lack access to safely managed drinking water services, driving governments across Asia, Africa, and Latin America to accelerate reservoir construction and water distribution network development, where liner systems are essential for leak prevention and contamination control. In the United States, the Infrastructure Investment and Jobs Act (IIJA) has committed US$ 55 billion specifically to water infrastructure improvements, including treatment plants, reservoirs, and stormwater systems, all major application environments for protective liner deployment. The World Bank reports that developing nations collectively require upward of US$ 114 billion annually in water and sanitation investment, a sustained capital flow that directly translates into long-term demand for geomembrane and spray-applied liner products across potable water, irrigation, and industrial effluent containment applications.

Restraints - High Initial Installation and Material Costs Limiting Adoption in Price-Sensitive Markets

The elevated capital expenditure associated with high-performance concrete protective liner systems, particularly PVDF-based, composite, and spray-applied variants, remains a meaningful adoption barrier in cost-sensitive municipal and industrial project environments. Advanced liner systems can add 15–30% to total project containment infrastructure costs relative to conventional concrete or earthen containment approaches, according to engineering cost benchmarking data from the U.S. Army Corps of Engineers. For smaller municipalities and emerging-market industrial operators with constrained capital budgets, this cost premium frequently delays liner adoption or results in specification downgrading to lower-performance materials, constraining overall market revenue growth and limiting penetration into price-sensitive project tiers.

Technical Complexity and Skilled Installation Workforce Deficits

The performance integrity of concrete protective liner systems is critically dependent on the quality of installation, with seam welding, surface preparation, and application technique directly determining long-term containment effectiveness and service life. However, a persistent and widening shortage of certified geosynthetic installer professionals in several key markets is creating project delivery bottlenecks and increasing total installation costs. The Geosynthetic Institute (GSI) has noted that inconsistent installation quality is among the most prevalent causes of liner system failures in regulated containment sites globally. In rapidly developing markets across Southeast Asia and Sub-Saharan Africa, the absence of a sufficiently trained and certified local installation workforce frequently forces project owners to import specialist contractors, significantly inflating project costs and extending deployment timelines.

Opportunities - Growing Mining Sector Tailings Management Investment Creating High-Value Demand

The global mining industry’s expanding focus on responsible tailings and heap leach pad containment management is emerging as one of the most significant high-value demand opportunities for concrete protective liner manufacturers. Following the catastrophic tailings dam failures at Brumadinho and Mariana in Brazil and growing regulatory scrutiny from bodies including the International Council on Mining & Metals (ICMM), mining operators globally are substantially upgrading their tailings storage facility (TSF) liner specifications. The Global Industry Standard on Tailings Management (GISTM), launched in 2020 and now adopted by major international miners including Rio Tinto, BHP, and Anglo American, mandates significantly enhanced containment integrity requirements for new and existing TSFs. This standard is driving widespread specification of double-liner composite systems incorporating HDPE geomembranes and geotextile cushion layers across new and retrofitted tailings facilities, creating a compelling, durable demand stream for high-specification liner products that is expected to materially expand through 2033 as compliance deadlines approach.

Infrastructure Rehabilitation and Smart Lining Technologies Unlocking Premium Growth

The accelerating rehabilitation of aging concrete infrastructure, including sewer networks, water treatment tanks, tunnels, and stormwater detention basins, represents a significant and underserved growth opportunity for spray-applied and composite liner system providers. According to the American Society of Civil Engineers (ASCE) 2021 Infrastructure Report Card, US$ 81 billion in additional investment is required to address the backlog of deteriorating drinking water and wastewater infrastructure in the United States alone. Spray-applied liners, which can be applied to irregular concrete substrates without major structural dismantling, are particularly well-positioned to capture rehabilitation project demand. Furthermore, emerging technologies such as fiber-reinforced spray liners, smart liner systems with integrated leak detection sensors, and nano-polymer-enhanced membranes are creating differentiated, premium-priced product categories within the concrete protective liner market. Companies investing early in R&D and digital liner monitoring capabilities are positioned to command significant price premiums and long-term service contracts with infrastructure asset managers seeking lifecycle performance guarantees.

Category-wise Insights

Product Type Analysis

Geomembranes dominate the Product Type category, accounting for approximately 35% of the global Concrete Protective Liner market share in 2025. Their market leadership is rooted in their unmatched combination of chemical resistance, hydraulic impermeability, broad material availability, and well-established regulatory acceptance across landfill, mining, and water containment applications globally. Geomembranes fabricated from HDPE are mandated by the U.S. EPA for composite liner systems in Subtitle C and Subtitle D regulated facilities, institutionalizing their procurement in the world’s largest regulated containment market. The Geosynthetic Research Institute (GRI) has developed widely adopted test standards, including GRI GM13 for HDPE geomembranes, that provide project owners and regulators with a reliable performance certification framework, further reinforcing geomembrane specification preference. Spray-Applied Liners are the fastest-growing product type, driven by their unique suitability for infrastructure rehabilitation projects where structural dismantling is impractical or cost-prohibitive.

Material Type Analysis

Polyethylene (HDPE/LDPE) leads the Material Type category, holding an estimated 40% of global Concrete Protective Liner market share in 2025. HDPE’s dominance is driven by its exceptional chemical resistance to acids, alkalis, and hydrocarbons, combined with proven long-term UV stability, weldability, and cost competitiveness relative to fluoropolymer and specialty polymer alternatives. The material is the predominant choice for landfill liner systems, mining tailings impoundments, and industrial wastewater lagoons across all major geographies. ASTM International Standard ASTM D7409 and the GRI GM13 specification, both widely referenced in regulated containment engineering, further institutionalize HDPE as the default material specification in publicly tendered liner projects. Polyvinylidene Fluoride (PVDF) is the fastest-growing material sub-segment, driven by its superior resistance to concentrated acids and aggressive chemical environments in specialty industrial and chemical processing plant applications where conventional polyolefin liners are inadequate.

Application Insights

Water management is the leading application segment, capturing approximately 30% of the global concrete protective liner market share in 2025. The segment’s dominance reflects the universal and non-discretionary nature of water containment infrastructure requirements, spanning potable water reservoirs, irrigation canal lining, stormwater detention ponds, and wastewater treatment lagoons across both developed and developing economies. According to the World Health Organization (WHO), more than 2 billion people consume water from contaminated sources, driving multilateral development bank and government investment in lined water storage and conveyance infrastructure globally. The U.S. Bureau of Reclamation, one of the largest water infrastructure agencies in the world, specifies geomembrane liner systems extensively in its reservoir and canal rehabilitation programs, providing institutional validation for high-performance liner adoption. Mining Operations represents the fastest-growing application segment, driven by escalating tailings management compliance requirements under the GISTM standard.

Industry Insights

Environmental protection is the dominant segment, accounting for approximately 35% of global Concrete Protective Liner demand in 2025. This leadership reflects the regulatory and compliance-driven nature of liner procurement in landfill containment, hazardous waste impoundment, groundwater protection, and contaminated site remediation, domains where liner deployment is legally mandated rather than value-engineered. The EPA’s RCRA program alone regulates thousands of active hazardous and municipal waste facilities in the United States, each requiring certified liner system installation, inspection, and long-term maintenance.

Across Europe, the EU Landfill Directive has mandated the progressive upgrading of existing landfill liner systems in member states, creating a large-scale, government-driven retrofit procurement market. The Industrial end-use segment is the fastest-growing, driven by expanding chemical plant construction, mining sector tailings management investment, and oil & gas produced water containment requirements in emerging economies.

Regional Insights

North America Concrete Protective Liner Market Trends and Insights

North America holds the leading position in the global Concrete Protective Liner market, commanding approximately 38% of global market share in 2025. The United States represents the regional demand core, underpinned by a mature and extensively enforced regulatory framework that mandates liner deployment across landfill, mining, and industrial waste containment applications. The EPA’s RCRA regulations, combined with state-level environmental agency requirements, create a large and structurally stable procurement base for geomembrane, composite, and spray-applied liner systems. The IIJA’s US$ 55 billion water infrastructure commitment is further expanding the addressable liner market within municipal water and wastewater applications.

Canada contributes meaningfully to regional demand, particularly through its large mining sector in Alberta, Ontario, and British Columbia, where heap leach pad and tailings storage facility liner upgrades are accelerating under tightened provincial environmental regulations. The Mining Association of Canada (MAC) has reinforced tailings management standards aligned with the GISTM framework, driving systematic adoption of high-specification double-liner composite systems. The U.S. also leads in technology innovation, with companies such as GSE Environmental LLC and Solmax International Inc. investing in next-generation leak detection-integrated liner systems and fiber-reinforced spray coatings, reinforcing the region’s dual position as both the world’s largest demand market and its foremost product innovation center.

Europe Concrete Protective Liner Market Trends and Insights

Europe is the second-largest regional market for Concrete Protective Liner products, driven by a comprehensive harmonized regulatory environment and significant investment in environmental infrastructure upgrades across Germany, the United Kingdom, France, and the Netherlands. The EU Landfill Directive (1999/31/EC) and the Industrial Emissions Directive collectively mandate liner system compliance across tens of thousands of regulated waste management and industrial sites, creating a large and structurally stable demand base. Germany hosts globally recognized liner manufacturers including Naue GmbH & Co. KG and AGRU Kunststofftechnik GmbH, reinforcing the country’s position as Europe’s primary production and innovation hub.

The United Kingdom’s post-Brexit infrastructure investment programs and France’s long-term energy transition plan, incorporating significant investment in water treatment and industrial waste management, are creating new demand vectors for high-performance liner solutions. Across Southern Europe, Spain and Italy are deploying liner systems in expanding irrigation canal rehabilitation projects, supported by the EU Common Agricultural Policy (CAP) water efficiency mandates. The European Geosynthetics Society (EGS) continues to promote standardized liner testing and application guidelines across member states, facilitating specification consistency and supporting market growth in emerging Central and Eastern European infrastructure programs.

Asia Pacific Concrete Protective Liner Market Trends and Insights

Asia Pacific is the fastest-growing regional market for concrete protective liner products, projected to register the highest regional CAGR during the forecast period. The region’s accelerating demand trajectory is anchored in massive infrastructure investment programs in China, India, Australia, and Southeast Asia, combined with rapidly tightening environmental regulations. China’s 14th Five-Year Plan has directed substantial investment into industrial wastewater treatment, solid waste management facilities, and mining sector environmental compliance, all requiring certified liner system deployment. China’s Ministry of Ecology and Environment (MEE) has significantly strengthened industrial effluent containment regulations, creating regulatory pull for high-specification HDPE and composite liner systems across the country’s vast industrial base.

India is emerging as a particularly dynamic growth market, driven by the Jal Jeevan Mission’s potable water infrastructure investment, the Smart Cities Mission incorporating advanced stormwater management infrastructure, and the rapid expansion of industrial and mining activities under the National Mineral Policy. The Bureau of Indian Standards (BIS) is progressively formalizing geomembrane and liner system standards, supporting specification-based procurement in government infrastructure programs. Australia’s world-class mining sector, a major global consumer of tailings containment liner systems, continues to drive high-value demand for double-liner HDPE composite systems, with Geofabrics Australasia Pty Ltd serving as a leading regional supplier. Asia Pacific’s expanding local manufacturing base in India and China is progressively reducing import dependence and supporting regional price competitiveness.

Competitive Landscape

The global concrete protective liner market exhibits a moderately fragmented structure, with a combination of large multinational manufacturers and regionally focused specialists catering to diverse end-use requirements. While global players benefit from scale, integrated supply chains, and broad product portfolios, regional participants compete through niche application expertise and localized project execution capabilities, particularly in infrastructure and environmental containment segments.

Competition is primarily driven by material innovation, regulatory compliance, and engineering support capabilities. Key business strategies include targeted acquisitions to expand geographic reach, continuous R&D investment in advanced and smart liner systems, and development of sustainable material offerings. Companies are increasingly adopting service-oriented models, offering lifecycle performance assurances and integrated maintenance solutions, especially in highly regulated municipal, mining, and wastewater infrastructure projects where long-term durability and compliance are critical.

Key Developments:

- January 2025: GSE Environmental LLC secured multiple containment infrastructure contracts across North America, supplying advanced liner systems for wastewater and industrial facilities to enhance leakage prevention and extend concrete asset lifespan.

- May 2024: Solmax International Inc. completed a significant capacity expansion at its North American geomembrane production facility, enhancing supply chain resilience and reducing lead times for large-scale mining and municipal water containment liner projects.

- September 2022: Concrete Canvas introduced CCX geotextile, a next-generation geosynthetic cementitious composite mat designed for canal and water infrastructure lining, offering faster installation, reduced seepage, and improved durability compared to conventional concrete solutions.

Companies Covered in Concrete Protective Liner Market

- Carlisle SynTec Systems

- Sika AG

- DuPont de Nemours

- BASF SE

- Poly-Flex, Inc.

- Layfield Group Ltd.

- Juta a.s.

- Plastika Kritis S.A.

- Naue GmbH & Co. KG

- Atarfil S.L.

- Geofabrics Australasia Pty Ltd

- AGRU Kunststofftechnik GmbH

- GSE Environmental LLC

- Solmax International Inc.

- Raven Industries Inc.

- Firestone Building Products

- Sotrafa S.A.

- RENOLIT SE

- TDM Geosynthetics

Frequently Asked Questions

The concrete protective liner market is projected to reach US$ 2.1 billion by 2026, supported by steady historical growth and demand from waste containment, water infrastructure, and industrial construction.

Growth is driven by stringent environmental regulations and rising investments in global water and wastewater infrastructure.

North America is leading supported by strong regulatory frameworks, infrastructure investments, and advanced liner technologies.

Key opportunities lie in mining tailings containment upgrades and rehabilitation of aging water infrastructure using advanced liner systems.

Major players include Sika AG, BASF SE, Solmax International, GSE Environmental, AGRU Kunststofftechnik, Naue, Carlisle SynTec Systems, Geofabrics Australasia, Layfield Group, and Raven Industries.