- Construction & Engineering

- Africa Construction Chemicals Market

Africa Construction Chemicals Market Size, Share, and Growth Forecast 2026 - 2033

Africa Construction Chemicals Market by Product Type (Concrete Admixture: Plasticizer (Lingo, SNF, PCE), Accelerator, Retarder, Air Entrainer, Others; Adhesives & Sealants: Adhesives, Sealants; Water Proofing Chemicals, Concrete Repair Mortar, Flooring Compounds, Protective Coating, Plaster, Asphalt Additives, Others), Application (Infrastructure, Residential, Commercial, Industrial), and Regional Analysis for 2026 - 2033

Africa Construction Chemicals Market Size and Trend Analysis

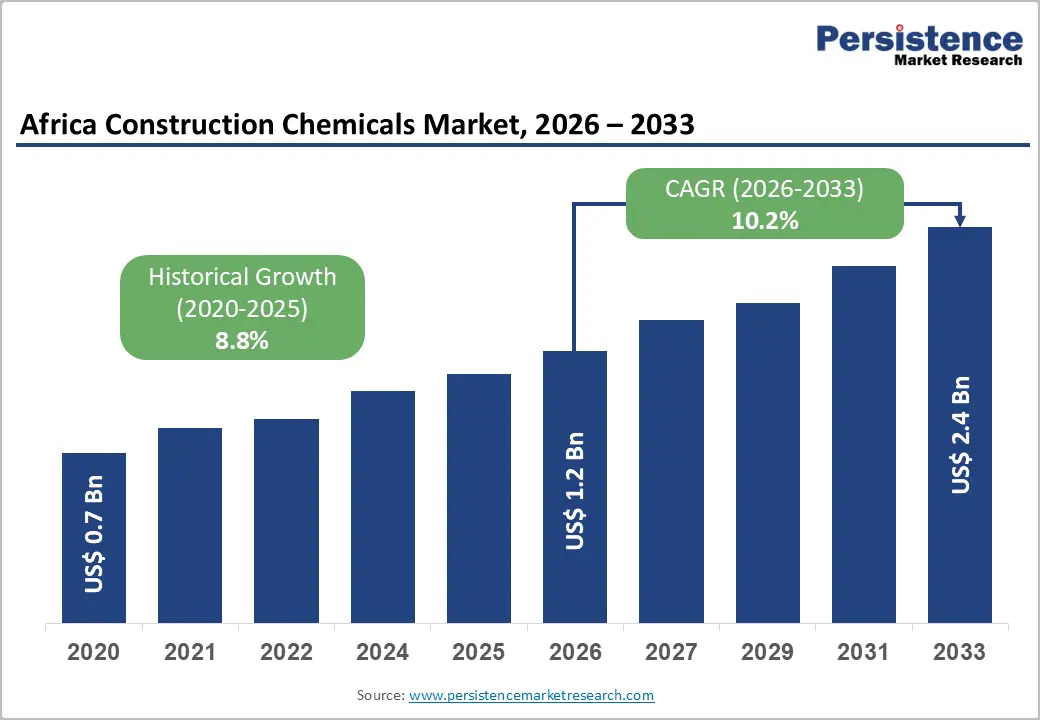

The Africa construction chemicals market size is supposed to be valued at US$ 1.2 Billion in 2026 and is projected to reach US$ 2.4 Billion by 2033, growing at a CAGR of 10.2% between 2026 and 2033.

The Africa Construction Chemicals market is one of the continent's most structurally high-growth specialty chemicals segments, driven by Africa's accelerating urbanization trajectory, large-scale government infrastructure investment programs, and the expanding adoption of performance-enhancing construction chemicals in residential, commercial, and public infrastructure projects across Nigeria, Egypt, South Africa, Ethiopia, Kenya, and other major African construction economies.

Key Market Highlights

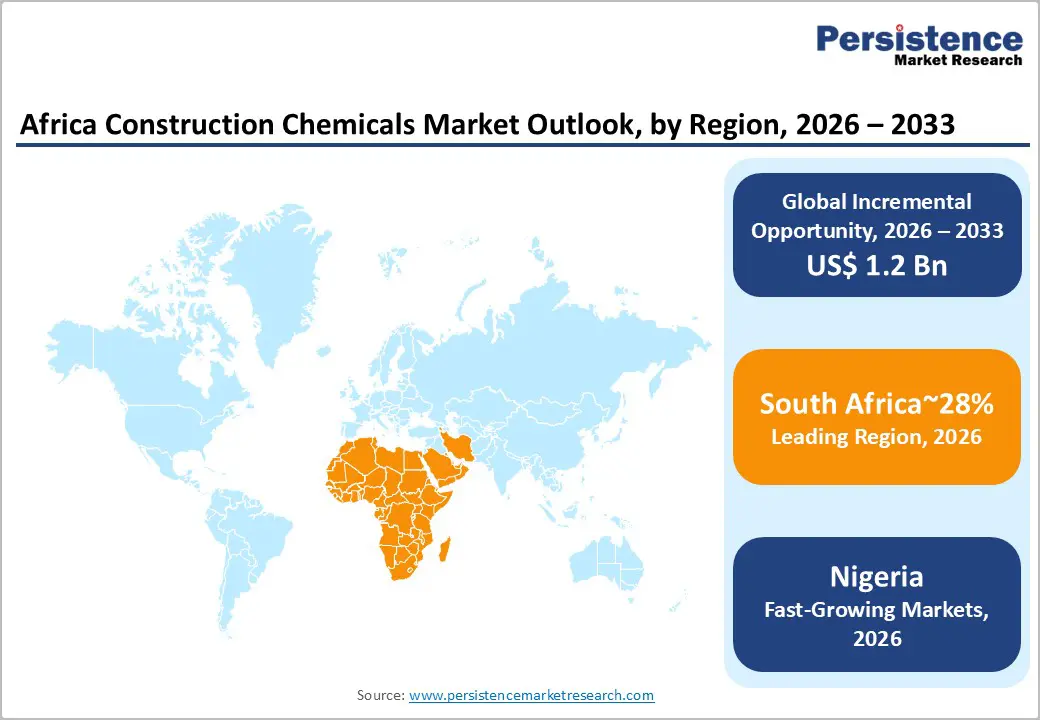

- Leading Country: South Africa leads the Africa Construction Chemicals market in growth momentum and project specification value, anchored by investments in road and bridge programs, New City construction, and the country's construction chemicals demand concentration generating above-CAGR procurement growth through 2033.

- Fastest Growing Country: Nigeria is the fastest-growing Sub-Saharan African Construction Chemicals market, driven by 220 million population-backed residential housing demand, Dangote Industries pan-African construction materials expansion, Federal Government's National Development Plan 2021 - 2025 infrastructure allocation.

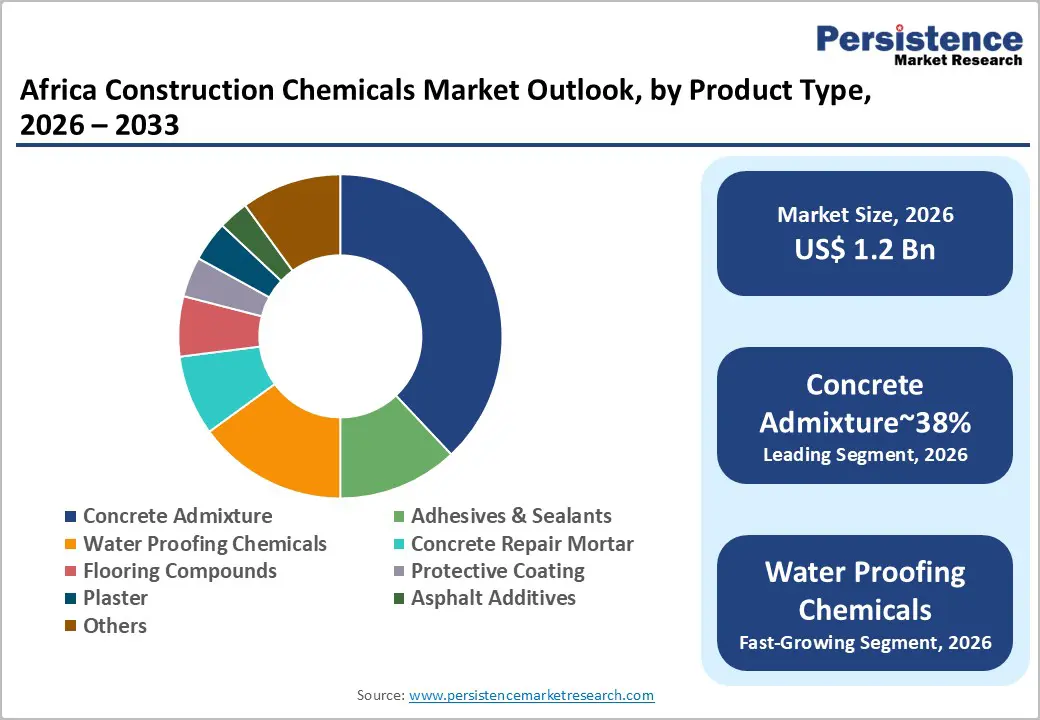

- Dominant Product Type: Concrete Admixture dominates the Product Type segment with approximately 38% revenue share, anchored by AfDB's US$ 68-108 Billion annual infrastructure financing gap driving high-performance concrete specification demand, and residential construction programs sustaining the segment's commercial leadership.

- Dominant Application: Infrastructure Application is the dominant and fastest-growing segment with approximately 42% revenue share, confirmed by AfDB's PIDA portfolio of over 400 priority infrastructure projects, Egypt NAC Phase 1 and 2 construction programs, LAPSSET Corridor multi-country infrastructure development, and AfCFTA implementation.

- Key Opportunity: Green building certified sustainable construction chemicals aligned with AfDB Paris Agreement commitments and GBCSA Green Star specifications represent the key market opportunity, with Egypt Green Building Council (EgGBC) LEED-aligned mandates, AfDB's 100% Paris-aligned sovereign operations commitment.

| Key Insights | Details |

|---|---|

| Africa Construction Chemicals Market Size (2026E) | US$ 1.2 Billion |

| Market Value Forecast (2033F) | US$ 2.4 Billion |

| Projected Growth CAGR (2026 - 2033) | 10.2% |

| Historical Market Growth (2020 - 2025) | 8.8% |

DRO Analysis

Drivers - Africa's Urbanization Megatrend and UN DESA-Documented Population Growth Generating Structural Residential and Infrastructure Construction Demand

Africa is experiencing the world's fastest urbanization growth rate, with the United Nations Department of Economic and Social Affairs (UN DESA) documenting that Africa's urban population is growing at approximately 3.5% annually, adding an estimated 40,000 new urban residents daily across the continent's cities and peri-urban settlements. This urbanization megatrend is creating massive and sustained demand for residential housing, urban road infrastructure, commercial buildings, water supply and sanitation systems, and public facilities, all of which require construction chemicals for concrete workability enhancement, structural durability improvement, waterproofing, and surface protection performance.

The African Development Bank (AfDB)'s annual infrastructure investment tracking confirms sustained multi-billion-dollar public and private capital deployment into urban construction projects across Nigeria, Egypt, Kenya, Ethiopia, Ghana, and Côte d'Ivoire, with the AfDB-financed Urban and Municipal Infrastructure Fund and national government housing programs including Egypt's New Administrative Capital mega-project and Nigeria's National Housing Programme directly sustaining institutional concrete admixture, waterproofing, and construction chemical procurement from BASF, Sika AG, and Fosroc International Ltd. supply networks.

African Government Infrastructure Investment Programs and African Continental Free Trade Area (AfCFTA) Implementation Accelerating Construction Activity

The African Continental Free Trade Area (AfCFTA), operationalized under the African Union (AU) and progressively implemented across 54 African Union member states since 2021, is accelerating cross-border trade infrastructure investment in roads, railways, border facilities, ports, and logistics corridors that collectively represent a sustained institutional demand driver for high-performance concrete admixtures, asphalt additives, protective coatings, and construction repair chemicals.

The AfDB's flagship Programme for Infrastructure Development in Africa (PIDA) has identified over 400 priority infrastructure projects across the continent requiring combined investment exceeding US$ 360 Billion through 2040, with transport infrastructure projects including the Trans-African Highway network rehabilitation and the Lamu Port-South Sudan-Ethiopia Transport (LAPSSET) Corridor representing multi-year construction chemical procurement programs for concrete admixtures, asphalt modifiers, and protective coating systems.

Dangote Industries Limited, through its cement and construction materials divisions, and PPC Ltd (Pretoria Portland Cement) (headquartered in Johannesburg, South Africa) are actively expanding their value-added construction chemicals product portfolios to capture growing institutional infrastructure project procurement demand across Sub-Saharan Africa.

Restraints - Foreign Currency Volatility and Import Dependency for Key Construction Chemical Raw Materials Constraining Market Price Stability

The majority of Africa's construction chemicals market is supplied through imported finished products and raw material intermediates, with key chemical raw materials including polycarboxylate ether (PCE) superplasticizer monomers, epoxy resins, polyurethane precursors, and acrylic polymer dispersions predominantly sourced from European, Asian, and North American chemical manufacturers.

African country currency depreciations, particularly in Nigeria, Egypt, Ghana, and Ethiopia where local currency volatility has been most acute in recent years as documented by International Monetary Fund (IMF) country economic assessments, create significant input cost inflation for construction chemical formulators operating in these markets, directly compressing distributor margins and creating end-user price resistance that slows adoption of premium-performance construction chemical products versus lower-cost conventional alternatives.

Limited Technical Awareness and Skilled Labor Shortage Constraining Proper Construction Chemical Application and Adoption

The optimal performance of construction chemicals, including PCE-based superplasticizers, crystalline waterproofing systems, epoxy injection repair mortars, and cementitious protective coatings, requires technically trained applicators with documented knowledge of mixing ratios, substrate preparation requirements, curing conditions, and application method protocols.

The African Union (AU)'s continental skills development framework and individual country technical and vocational education and training (TVET) program assessments document a significant shortage of trained construction chemical applicators across Sub-Saharan African construction markets, leading to product misapplication, premature performance failures, and contractor reluctance to specify premium-priced chemical solutions over conventional construction methods, directly constraining the market's transition toward higher-value specialty construction chemicals that command the above-average margins driving forecast revenue growth.

Opportunities - Egypt's New Administrative Capital and North African Mega-Project Pipeline Creating Large-Scale Concrete Admixture and Waterproofing Chemical Procurement Opportunity

The Arab Republic of Egypt's unprecedented infrastructure investment program, anchored by the New Administrative Capital (NAC) project covering approximately 170,000 acres east of Cairo and accommodating a planned population of 6.5 million residents across government districts, residential zones, business parks, and cultural facilities, represents one of Africa's largest single construction chemical procurement programs, requiring multi-year high-volume supply of concrete admixtures, waterproofing membranes, protective coatings, flooring compounds, and construction adhesives from global and regional suppliers.

The Egyptian Ministry of Housing, Utilities and Urban Communities has documented investment exceeding US$ 58 Billion in the NAC Phase 1 alone, with the project's demanding structural concrete performance specifications requiring premium PCE-based superplasticizers from BASF SE's MasterGlenium product series, Sika AG's ViscoCrete admixture family, and Chryso S.A.S. (headquartered in Issy-les-Moulineaux, France) CHRYSO®Fluid product portfolio to meet high-rise structural concrete workability, early strength, and durability requirements. Additional Egyptian government megaprojects including the Alamein New City development along the Mediterranean coast and the national road and bridge rehabilitation program documented by the Egyptian Ministry of Transport confirm North Africa's emergence as Africa's highest-value construction chemicals demand concentration geography through the forecast period.

Green Building Standards and AfDB-Supported Sustainable Construction Material Adoption Creating Premium Eco-Label Construction Chemicals Opportunity

The progressive adoption of green building certification standards, including the Green Building Council South Africa (GBCSA)'s Green Star certification, Egypt Green Building Council (EgGBC) LEED-aligned standards, and the World Green Building Council (WorldGBC)'s Africa Regional Network programs, is creating a growing institutional demand channel for low-VOC adhesives and sealants, phthalate-free plasticizers, recycled-content waterproofing membranes, and sustainable protective coating systems that meet green building material specification requirements for certified project procurement.

The African Development Bank (AfDB) has committed to ensuring that 100% of its sovereign public sector operations are aligned with the Paris Agreement climate commitments, with its Sustainable Energy for All (SE4All) and Green Climate Fund (GCF) co-financed construction projects mandating sustainable material specifications that directly favor low-carbon and environmentally certified construction chemical products. Sika AG (headquartered in Baar, Switzerland), whose SikaGard, Sikaflex, and Sika®Monotop sustainable construction chemical product families carry multiple international environmental product declaration (EPD) certifications, and Mapei S.p.A. (headquartered in Milan, Italy) are strategically positioned to capture above-average revenue growth from Africa's emerging green building certified project procurement channels by 2033.

Category-wise Analysis

By Product Type Insights

Concrete Admixture leads the Africa Construction Chemicals market by product type, commanding approximately 38% of total product type segment revenue in 2026, a dominant position reflecting concrete admixtures' foundational role as the most universally specified and volumetrically consumed construction chemical category across all African construction application segments, from large-scale infrastructure concrete placements requiring PCE-based superplasticizers for high-performance workability and reduced water-cement ratio specifications, to mass housing concrete mixes utilizing lignosulfonate (Lingo) and SNF (Sulfonated Naphthalene Formaldehyde) based plasticizers for cost-effective workability improvement.

The Portland Cement Association (PCA) and ASTM International standards for concrete admixture performance classification confirm concrete admixtures as the global construction chemicals standard, with BASF SE's Master Builders Solutions brand and Sika AG's construction chemicals division dominating African institutional project specifications.

Within the concrete admixture sub-segment, pasticizers (PCE, SNF, Lingo) represent the highest-revenue sub-category at approximately 46% of concrete admixture sales, driven by growing infrastructure project concrete performance specifications. Waterproofing Chemicals hold approximately 18% of product type revenue, with strong growth driven by Egypt's mega-project underground construction and South Africa's infrastructure rehabilitation programs. Protective Coatings hold approximately 12%.

By Application Insights

Infrastructure leads the Africa Construction Chemicals market by application, commanding approximately 42% of total application segment revenue in 2026, a dominant position anchored in the African Development Bank (AfDB)'s documented annual continental infrastructure financing gap of US$ 68-108 Billion and the multi-year institutional construction chemical procurement requirements of road, bridge, dam, port, railway, and water infrastructure projects across Africa's major economies that collectively represent the continent's largest and most technically demanding construction chemical application category.

The AfDB's PIDA priority project portfolio, spanning the Trans-African Highway rehabilitation, LAPSSET Corridor, Inga III hydropower dam project, and port expansion programs at Durban, Mombasa, Lagos, and Dakar, generates sustained high-volume procurement of concrete admixtures, asphalt additives, repair mortars, and protective coatings from Fosroc International Ltd., BASF SE, and Sika AG supply networks.

Residential holds approximately 30% of application revenue, driven by Egypt's New Administrative Capital residential districts, Nigeria's National Housing Programme, and South Africa's government-subsidized housing delivery programs. Commercial holds approximately 18%, growing with retail, hospitality, and office development activity. Industrial holds approximately 10%.

Regional Insights

South Africa Construction Chemicals Trends & Insights

South Africa is Africa's most technically mature and commercially established Construction Chemicals market, anchored by the country's developed construction industry ecosystem, Green Building Council South Africa (GBCSA) green building certification framework, and the procurement influence of major South African construction conglomerates including Murray & Roberts, Group Five, and Aveng that specify premium construction chemicals for public and private infrastructure projects.

The South African National Treasury's Infrastructure Fund, a US$ 1 Billion+ blended finance vehicle co-managed with the Development Bank of Southern Africa (DBSA), is channeling capital into water, energy, transport, and human settlements projects that collectively sustain institutional construction chemical procurement. AECI Limited (headquartered in Johannesburg, South Africa) and AfriSam (headquartered in Johannesburg, South Africa) are South Africa's most commercially significant domestic construction chemicals and cementitious products suppliers.

The South African Department of Public Works and Infrastructure (DPWI)'s expanded public works program and the Gauteng Infrastructure Financing Agency (GIFA)'s provincial infrastructure investment pipeline are sustaining construction chemical demand from road rehabilitation, public building refurbishment, and social housing programs. PPC Ltd (Pretoria Portland Cement) (headquartered in Johannesburg, South Africa) has been expanding its value-added construction chemicals and specialty cement products portfolio, targeting domestic infrastructure project specifications for concrete admixtures, repair mortars, and waterproofing systems through its established South African and Sub-Saharan distribution network. BASF SE's South African construction chemicals distribution operations and Sika AG's Johannesburg-based regional manufacturing facility serve the South African premium construction chemical specification market for infrastructure and commercial building projects.

Egypt Construction Chemicals Trends & Insights

Egypt is Africa's fastest-growing Construction Chemicals market, anchored by President Abdel Fattah el-Sisi's administration's unprecedented infrastructure investment drive that has generated one of the world's most active construction pipelines, with the Egyptian Ministry of Housing, Utilities and Urban Communities documenting over US$ 58 Billion invested in the New Administrative Capital (NAC) alone, complemented by the Alamein New City, El-Galala City, and national road, bridge, and metro expansion programs that collectively represent the African continent's largest single-geography construction chemical demand concentration. The NAC's high-rise residential towers, underground parking structures, metro stations, and commercial district construction require premium PCE superplasticizers, crystalline waterproofing systems, epoxy-based protective coatings, and high-performance repair mortars, specifications where BASF SE's MasterGlenium PCE admixtures, Sika AG's ViscoCrete and Sika Watertight Concrete systems, and Chryso S.A.S. CHRYSO®Fluid product families are commercially active.

The Egyptian Ministry of Transport's national road expansion and Suez Canal Zone industrial corridor development programs, supported by Egyptian government capital expenditure budgets documented in the Ministry of Finance's annual economic statements, are sustaining multi-year asphalt additives, concrete admixtures, and protective coating procurement for transportation infrastructure projects. Mapei S.p.A.'s Egyptian manufacturing and distribution operations and Fosroc International Ltd.'s North African technical sales network serve Egypt's growing specification demand for high-performance flooring compounds, tile adhesives, and cementitious repair mortars from the country's rapidly expanding commercial real estate and hospitality construction sector.

Nigeria Construction Chemicals Trends & Insights

Nigeria is Sub-Saharan Africa's largest construction market by economic scale and one of the Africa Construction Chemicals market's most significant growth opportunity geographies, driven by the country's population of over 220 million documented by the National Population Commission of Nigeria, rapid urbanization across Lagos, Abuja, Port Harcourt, Kano, and secondary cities, and the Federal Government of Nigeria's sustained public infrastructure investment under its National Development Plan 2021-2025 allocating trillions of Naira to road, bridge, housing, and port infrastructure projects. The Nigerian Building and Road Research Institute (NBRRI), a government research institution under the Federal Ministry of Science, Technology and Innovation, has been actively promoting adoption of performance-verified construction chemicals for Nigerian infrastructure projects, including concrete admixtures for hot-climate tropical concrete workability management and waterproofing solutions for below-grade construction applications.

Dangote Industries Limited (headquartered in Lagos, Nigeria), through its Dangote Cement affiliate which is the largest cement producer in Africa by capacity with approximately 51.6 million tonnes per annum (MTPA) production capacity across Africa documented in its annual reports, is strategically positioned to integrate value-added construction chemicals including concrete admixtures, waterproofing compounds, and repair mortars into its Nigerian and pan-African construction materials supply chain. Conmix Ltd (headquartered in the UAE with active African market operations) serves Nigerian construction project procurement for concrete admixtures and specialty construction chemicals. The Lagos Metropolitan Area Transport Authority (LAMATA) rail infrastructure expansion and the Nigerian Federal Ministry of Works bridge rehabilitation programs sustain institutional procurement demand for structural concrete admixtures, epoxy repair systems, and protective coatings from international suppliers including Sika AG and BASF SE's West African distribution network.

Competitive Landscape

Africa construction chemicals market is moderately consolidated at the premium technical product level, with BASF SE, Sika AG, Fosroc International Ltd., and Mapei S.p.A. commanding institutional project specification leadership through internationally recognized product quality, technical application support teams, and multi-country African distribution networks. Chryso S.A.S. and Arkema S.A. serve the mid-premium concrete admixture segment. Regional leaders AECI Limited, AfriSam, PPC Ltd, and Dangote Industries leverage local manufacturing cost advantages and established distribution relationships.

Key differentiators include green building product certifications, local technical support capability, hot-climate product formulation adaptation, and AfDB-compliant sustainable material credentials. Emerging business model trends include direct infrastructure project specification partnerships, local manufacturing JVs, and digital technical training platforms for African contractor capacity building.

Key Developments:

- In January 2025, Sika AG expanded its Johannesburg-based South African manufacturing facility, adding dedicated production capacity for SikaGard protective coatings and SikaTop repair mortar product lines, targeting growing South African Infrastructure Fund and DBSA co-financed infrastructure project specification demand across Sub-Saharan Africa.

- In September 2024, BASF SE's Master Builders Solutions division signed a technical partnership agreement with the New Administrative Capital for Urban Development (ACUD) authority in Egypt, supplying MasterGlenium PCE superplasticizers, MasterSeal waterproofing membranes, and MasterEmaco repair mortars for NAC Phase 2 high-rise residential and commercial district construction programs.

- In March 2024, Fosroc International Ltd. strengthened its West African distribution network, establishing new authorized technical distributor partnerships in Ghana, Côte d'Ivoire, and Senegal, targeting growing construction chemicals demand from AfDB-financed road rehabilitation and port infrastructure projects across the ECOWAS region.

Companies Covered in Africa Construction Chemicals Market

- BASF SE

- Sika AG

- Mapei S.p.A.

- Saint-Gobain

- Fosroc International Ltd.

- RPM International Inc.

- Arkema S.A.

- Dow Inc.

- Henkel AG & Co. KGaA

- Chryso S.A.S.

- Dangote Industries Limited

- PPC Ltd (Pretoria Portland Cement)

- AfriSam

- AECI Limited

- Conmix Ltd

Frequently Asked Questions

The Africa Construction Chemicals market is estimated to be valued at US$ 1.2 Billion in 2026 and is projected to reach US$ 2.4 Billion by 2033, registering a forecast CAGR of 10.2% from 2026 to 2033.

The primary drivers are UN DESA's documented 3.5% annual African urbanization growth rate adding 40,000 new urban residents daily that structurally sustains residential and commercial construction chemical demand, and the AfDB's PIDA portfolio of over 400 priority continental infrastructure projects requiring high-performance concrete admixtures, waterproofing systems.

Concrete Admixture leads the Product Type segment with approximately 38% revenue share in 2026, anchored by the AfDB's annual continental infrastructure investment program requiring high-performance concrete specifications, BASF MasterGlenium PCE and Sika ViscoCrete institutional project approvals in Egypt's NAC and South Africa's infrastructure programs, and the universal specification of plasticizers, accelerators, and retarders across all African infrastructure, residential, and commercial construction project concrete placement operations.

Egypt leads the Africa Construction Chemicals market in per-project specification value and growth momentum, anchored by the Egyptian Ministry of Housing's US$ 58 Billion+ New Administrative Capital investment, Alamein New City and Mediterranean coastal development programs, Ministry of Transport national road and bridge infrastructure expansion, and the country's specification of internationally certified premium concrete admixtures, waterproofing systems, and protective coatings from BASF SE, Sika AG, Chryso S.A.S., and Mapei S.p.A. supply networks confirming North Africa's dominant construction chemicals revenue position.

The most significant opportunity is green building certified sustainable construction chemicals aligned with AfDB's 100% Paris Agreement commitment for sovereign operations, GBCSA Green Star and EgGBC LEED-aligned specifications, Sika AG's EPD-certified sustainable product portfolio, and Africa's expanding commercial real estate sector collectively creating a premium pricing market channel, with AfDB Green Climate Fund (GCF) co-financed sustainable construction projects mandating low-VOC, low-carbon certified construction chemical specifications driving above-CAGR margin growth for certified suppliers through 2033.

The leading companies include BASF SE, Sika AG, Fosroc International Ltd., Mapei S.p.A., Chryso S.A.S., Dangote Industries Limited, PPC Ltd (Pretoria Portland Cement), AECI Limited, AfriSam, Henkel AG & Co. KGaA, Arkema S.A., Dow Inc., Saint-Gobain, RPM International Inc., and Conmix Ltd, collectively spanning global premium construction chemicals innovators and Africa-headquartered regional manufacturers serving the full Africa Construction Chemicals value chain.