- Specialty & Fine Chemicals

- Anionic Polyacrylamide Market

Anionic Polyacrylamide Market Size, Share, and Growth Forecast, 2026 - 2033

Anionic Polyacrylamide Market by Application (Water/Wastewater Treatment, Sludge Dewatering, Others), End-use Industry (Municipal Water & Wastewater Utilities, Mining & Mineral Processing, Others), Product Form, and Regional Analysis for 2026 - 2033

Anionic Polyacrylamide Market Size and Trends Analysis

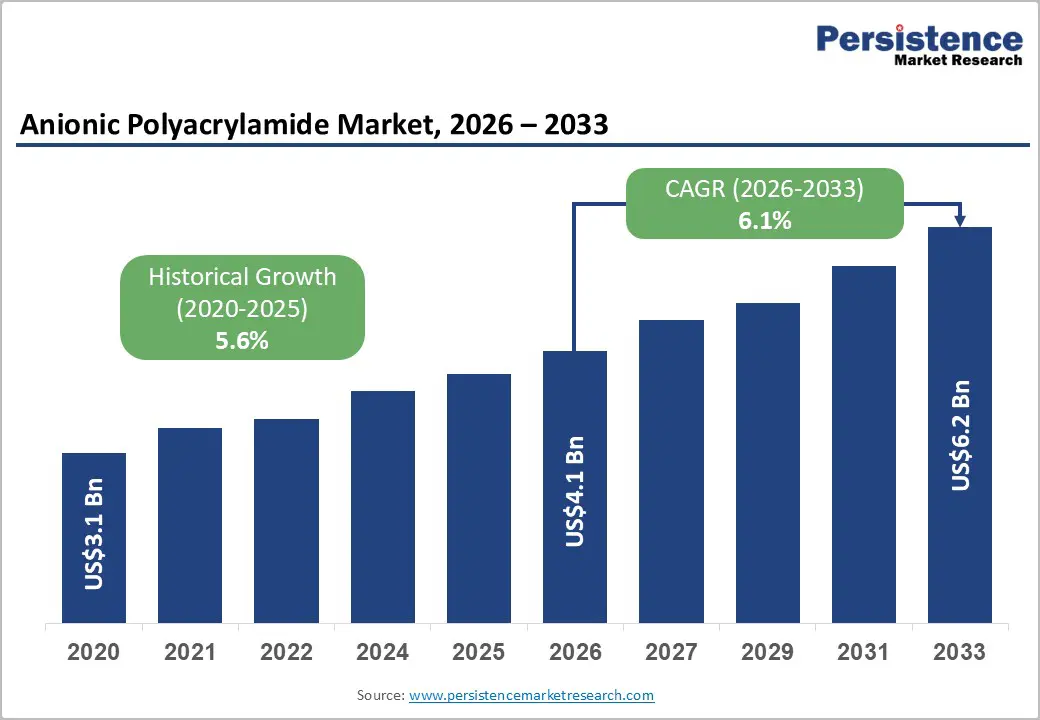

The global anionic polyacrylamide market size is likely to be valued at US$4.1 billion in 2026 and is expected to reach US$6.2 billion by 2033, growing at a CAGR of 6.1% during the forecast period from 2026 to 2033, driven by stricter environmental regulations governing wastewater discharge, rising investment in water treatment infrastructure, and broader adoption of APAM in mining, oil recovery, paper manufacturing, and industrial effluent treatment.

Asia Pacific remains the leading and fastest-growing regional market due to rapid industrialization and infrastructure development, while North America and Europe are emphasizing higher-performance and environmentally compliant polymer technologies. The market outlook remains supported by recurring consumption demand and increasing process optimization requirements across end-use industries.

Key Industry Highlights:

- Leading Region: Asia Pacific is projected to account for approximately 29.4% of the market share in 2026, supported by strong wastewater infrastructure expansion, industrialization, and mining activities across China, India, and Southeast Asia.

- Fastest-growing Region: Asia Pacific is projected to grow during the forecast period, driven by rising investments in industrial water recycling, municipal sewage treatment, and manufacturing capacity expansion.

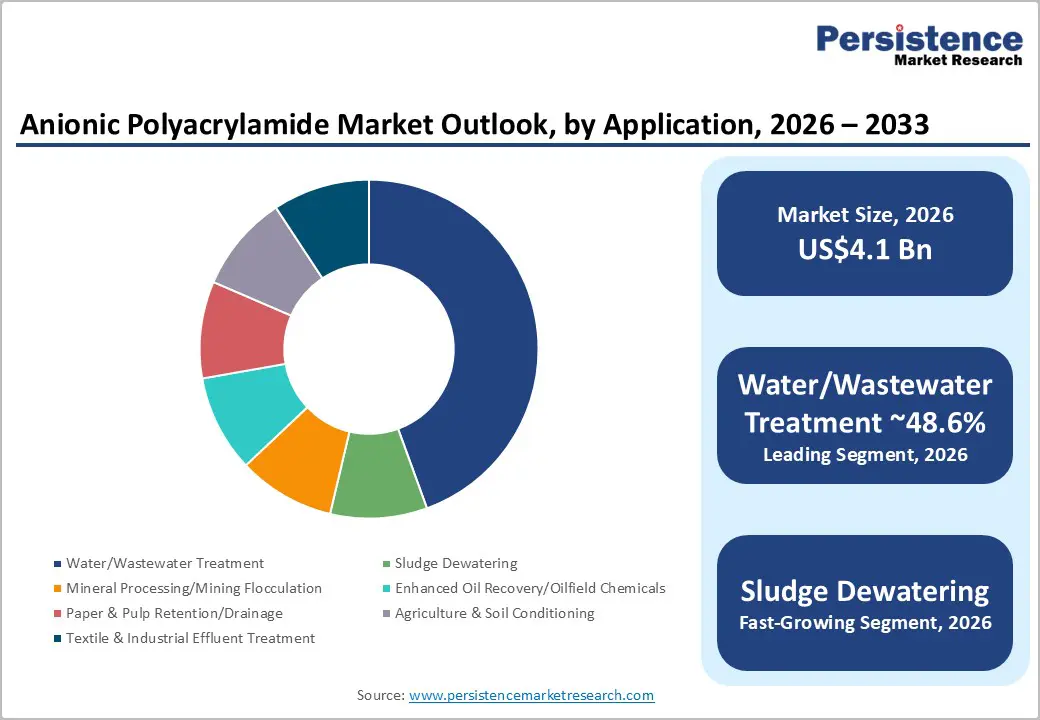

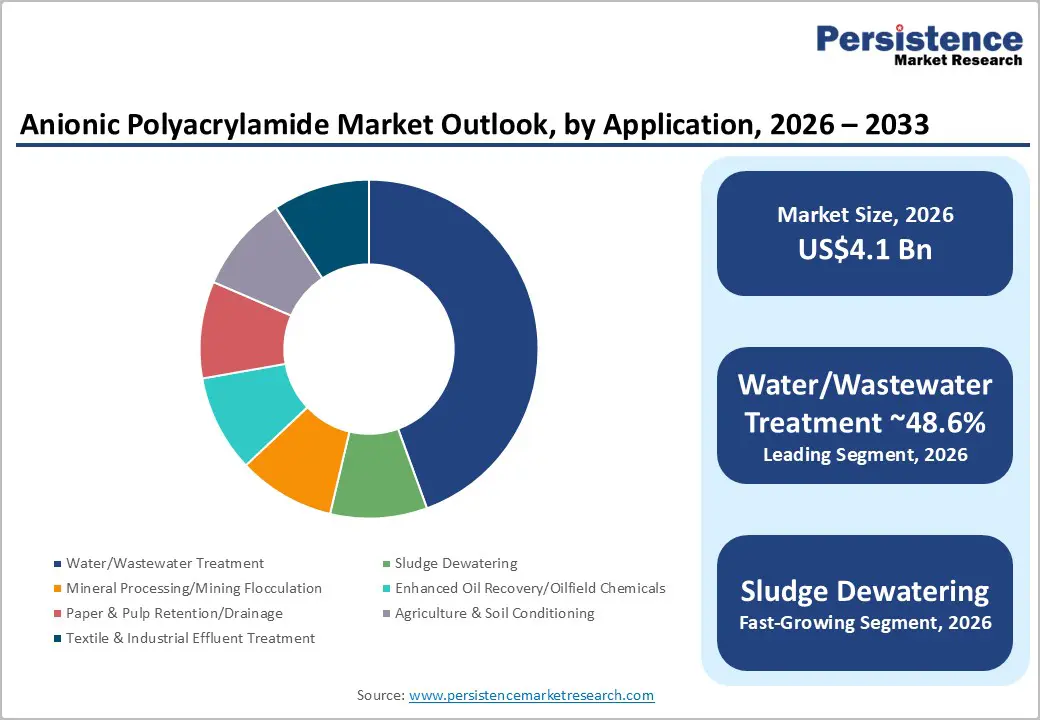

- Dominant Application: Water treatment and wastewater treatment are anticipated to account for approximately 48.6% of market share in 2026, due to recurring consumption across municipal and industrial treatment facilities.

- Leading End-use Industry: Municipal water and wastewater utilities are expected to hold approximately 48.7% of the market share in 2026, supported by long-term infrastructure modernization programs and continuous chemical consumption requirements.

DRO Analysis

Driver - Expansion of Wastewater Treatment Infrastructure and Regulatory Compliance

The increasing global focus on wastewater treatment and water reuse continues to support long-term demand for anionic polyacrylamide. Governments and environmental agencies are implementing stricter wastewater discharge regulations, forcing municipalities and industrial operators to improve treatment efficiency and sludge handling processes. APAM plays a critical role in flocculation, clarification, and sludge dewatering applications because of its ability to improve suspended solids removal and optimize water recovery.

In the U.S., federal infrastructure investments directed toward drinking water and wastewater modernization are increasing the installation and upgrade of treatment systems. European wastewater directives are also tightening standards related to micropollutants, nutrient discharge, and treatment efficiency. These regulatory developments create recurring chemical consumption demand rather than one-time capital expenditure demand. Municipal wastewater plants increasingly rely on APAM to improve operational efficiency, reduce sludge volume, and lower disposal costs. As treatment standards continue to rise globally, APAM demand is expected to remain structurally resilient across both developed and emerging economies.

Growing Demand from Mining, Mineral Processing, and Oilfield Applications

Mining and energy industries are becoming increasingly important growth contributors for the APAM market. In mining operations, APAM is widely used for tailings thickening, water recovery, and solid-liquid separation processes. Rising environmental scrutiny surrounding mine tailings management and water conservation is encouraging operators to adopt advanced flocculation systems that improve water recycling efficiency and reduce waste disposal risks.

The oil and gas sector is also contributing to market expansion through enhanced oil recovery applications. Polymer flooding technologies utilize hydrolyzed polyacrylamide to improve the viscosity of injected water and enhance reservoir sweep efficiency. Mature oilfields in North America, China, and the Middle East continue to utilize polymer flooding to improve extraction economics.

The commercial significance of these applications lies in market diversification. APAM suppliers are no longer dependent solely on municipal water treatment demand. Instead, industrial diversification across mining, oil recovery, paper processing, and manufacturing creates multiple long-term consumption channels that improve market stability and support future revenue growth.

Restraint - Health, Environmental, and Regulatory Concerns Related to Residual Acrylamide

One of the primary restraints affecting the APAM market involves regulatory scrutiny surrounding residual acrylamide monomer content. Although polyacrylamide itself is generally considered stable, residual acrylamide levels must remain tightly controlled because acrylamide exposure is associated with potential toxicological risks. Regulatory agencies across North America and Europe have established strict limits for acrylamide content in water treatment chemicals used in potable water systems.

Compliance requirements increase testing, quality assurance, and formulation costs for manufacturers. Water treatment facilities and industrial users must also maintain precise dosing systems and documentation procedures to comply with environmental and safety standards. These requirements can increase operational complexity and reduce adoption in highly regulated applications such as drinking water treatment, agriculture, and food-adjacent processing industries.

Smaller manufacturers may face challenges meeting increasingly stringent compliance requirements, potentially limiting market entry and intensifying competitive pressure among regional suppliers.

Opportunity - Rising Demand for Advanced Sludge Dewatering Technologies

The modernization of municipal and industrial sludge treatment systems presents a major growth opportunity for APAM suppliers. Wastewater treatment operators are increasingly focused on reducing sludge disposal costs, improving dewatering efficiency, and lowering overall operating expenses. APAM products designed for enhanced sludge conditioning and improved cake dryness are becoming increasingly valuable in this environment.

Utilities are also under pressure to improve sustainability performance and reduce transportation volumes associated with sludge disposal. Even small improvements in dewatering efficiency can significantly reduce hauling and landfill costs for large municipal facilities. This creates strong demand for higher-performance APAM formulations capable of reducing polymer consumption while improving separation efficiency.

Manufacturers that provide technical support, dosing optimization services, and customized treatment programs are expected to gain competitive advantages in this segment. The opportunity extends beyond product sales into long-term operational partnerships with utilities and industrial treatment operators.

Industrial Expansion and Water Recycling Investments across Asia Pacific

Asia Pacific represents the largest long-term growth opportunity for the APAM market due to rapid industrialization, urbanization, and increasing water stress across major economies. China, India, and Southeast Asian countries continue investing heavily in wastewater treatment infrastructure, industrial water recycling systems, and manufacturing capacity expansion.

Industrial sectors including textiles, chemicals, mining, pulp and paper, and food processing are facing increasing pressure to reduce water discharge and improve water reuse rates. APAM is widely used in these industries to improve clarification efficiency, sludge settling, and effluent treatment performance.

The region also benefits from strong local manufacturing capabilities and cost-efficient production infrastructure. Suppliers with localized production, technical support capabilities, and application-specific product portfolios are well positioned to capitalize on rising demand across municipal and industrial treatment markets in Asia Pacific.

Category-wise Analysis

Application Insights

Water treatment and wastewater treatment are anticipated to account for approximately 48.6% of market share during the forecast period, making them the leading application segment. APAM is extensively used in municipal sewage plants, industrial effluent treatment systems, and desalination facilities to improve flocculation, sedimentation, and sludge separation efficiency. For example, large municipal treatment projects in China and India increasingly utilize APAM-based flocculants to improve suspended solids removal and support water reuse targets. The segment maintains stable recurring demand because treatment chemicals are consumed continuously during plant operations.

Rising urbanization, stricter industrial discharge standards, and growing investment in water recycling infrastructure continue supporting long-term demand growth. Municipal wastewater utilities remain the largest consumers due to long-term procurement contracts and large-scale treatment requirements.

Sludge dewatering is anticipated to witness the fastest growth among application segments due to increasing pressure on utilities and industrial operators to reduce sludge disposal costs and improve treatment efficiency. APAM is widely used in belt filter presses, centrifuges, and screw press systems to improve sludge thickening and reduce moisture content. Utilities across Europe and North America are investing in advanced sludge handling technologies to comply with landfill reduction and sustainability targets.

Industrial sectors such as mining, food processing, pulp and paper, and chemicals are also upgrading dewatering systems to improve operational efficiency. For instance, mining operations in Chile and Australia increasingly use APAM-based dewatering systems to improve water recovery from tailings.

End-use Industry Insights

Municipal water and wastewater utilities are anticipated to account for approximately 48.7% of the market share in 2026, making them the dominant end-use industry segment. APAM is widely used in municipal clarifiers, sludge dewatering systems, and wastewater treatment plants to improve solids separation and reduce treatment costs. Large-scale infrastructure modernization projects across the United States, China, and India continue driving polymer consumption within municipal treatment facilities.

The segment benefits from stable recurring demand because utilities require continuous chemical supply for daily operations. Government investments in sewage treatment expansion, water recycling, and urban sanitation infrastructure are further strengthening long-term market demand for APAM products.

Mining and mineral processing are anticipated to be the fastest-growing end-use industries for APAM due to rising demand for water recycling, tailings management, and sustainable mining practices. APAM is extensively used in copper, iron ore, lithium, and gold mining operations to improve sedimentation, accelerate solids separation, and recover process water.

Environmental regulations surrounding tailings disposal and water conservation are encouraging mining companies to adopt advanced flocculation technologies. For example, lithium extraction projects in South America and iron ore operations in Australia increasingly rely on APAM-based water recovery systems to improve sustainability performance and reduce freshwater consumption.

Regional Insights

North America Anionic Polyacrylamide Market Trends

North America represents a technologically advanced and regulation-driven market for anionic polyacrylamide, supported by strong municipal infrastructure investment, industrial wastewater treatment demand, and oilfield chemical applications. The region benefits from strict environmental regulations governing wastewater discharge, sludge management, and industrial effluent treatment, which continue driving consistent APAM consumption across municipal and industrial sectors.

U.S. Anionic Polyacrylamide Market Trends

The U.S. remains the dominant market in North America due to extensive wastewater infrastructure modernization programs and strong industrial demand. Federal investment initiatives supporting drinking water and wastewater treatment upgrades are accelerating the adoption of advanced flocculation and sludge dewatering technologies. Municipal utilities across states such as California, Texas, and Florida are increasingly utilizing APAM in clarifiers, sludge thickening systems, and wastewater recycling projects.

The country also represents a major market for enhanced oil recovery applications, particularly in mature oilfields across Texas and the Permian Basin. Industrial sectors including chemicals, pulp and paper, food processing, and power generation continue contributing to steady APAM demand growth.

Canada Anionic Polyacrylamide Market Trends

Canada is witnessing growing demand for APAM due to increasing investment in municipal wastewater treatment and mining operations. Mining activities involving potash, iron ore, and critical minerals are supporting demand for APAM-based flocculation and water recovery systems. Provinces such as Ontario and British Columbia are also investing in sustainable wastewater management infrastructure to improve water reuse and treatment efficiency.

North America emphasizes specialty polymer formulations, process optimization services, and regulatory compliance support rather than low-cost commodity supply. Suppliers compete primarily through technical expertise, treatment efficiency improvements, and long-term customer service capabilities.

Europe Anionic Polyacrylamide Market Trends

Europe represents a mature but technologically evolving APAM market driven by regulatory harmonization, sustainability initiatives, and wastewater treatment modernization. The region continues prioritizing water recycling, sludge reduction, and industrial discharge compliance, which support long-term demand for advanced flocculation and dewatering chemicals.

Germany Anionic Polyacrylamide Market Trends

Germany is the leading APAM market in Europe due to its highly developed industrial base and advanced municipal wastewater treatment infrastructure. The country’s chemicals, automotive, food processing, and manufacturing industries generate strong demand for industrial water treatment solutions. German municipalities are also investing heavily in energy-efficient sludge management systems and micropollutant removal technologies.

U.K. Anionic Polyacrylamide Market Trends

The U.K. continues expanding investment in wastewater infrastructure modernization and water recycling systems. Water utilities are increasingly adopting advanced sludge dewatering technologies to improve operational efficiency and comply with stricter environmental discharge standards. Industrial demand from food processing, chemicals, and power generation sectors further supports market growth.

France Anionic Polyacrylamide Market Trends

France maintains significant APAM demand through municipal water treatment and industrial wastewater applications. The country’s strong emphasis on sustainable water management and circular economy initiatives is increasing the adoption of environmentally compliant polymer formulations. Wastewater treatment upgrades across urban municipalities continue supporting stable chemical consumption.

Across Europe, regulatory pressure surrounding nutrient removal, micropollutant treatment, and environmental sustainability continues driving demand for high-performance and lower-residual polymer technologies. Suppliers with advanced formulations, sustainability-focused product portfolios, and technical service capabilities maintain competitive advantages across the region.

Asia Pacific Anionic Polyacrylamide Market Trends

Asia Pacific is the leading and fastest-growing regional market for anionic polyacrylamide, accounting for approximately 29.4% of market share and projected to grow at a regional CAGR of 6.7% during the forecast period. Rapid industrialization, urbanization, expanding wastewater infrastructure, and strong manufacturing activity continue driving APAM demand across municipal and industrial applications.

China Anionic Polyacrylamide Market Trends

China represents the largest APAM market in Asia Pacific due to its extensive municipal wastewater treatment infrastructure, mining operations, and manufacturing base. Industrial sectors including chemicals, textiles, paper manufacturing, and mining are major consumers of APAM products for flocculation and sludge management applications.

The country is also investing heavily in water recycling and environmental compliance projects to address industrial pollution and water scarcity concerns. Large-scale wastewater treatment expansion projects across major industrial provinces continue supporting strong market growth.

India Anionic Polyacrylamide Market Trends

India is emerging as one of the fastest-growing APAM markets due to rapid urbanization, industrial expansion, and increasing government investment in sewage treatment infrastructure. Programs focused on river cleaning, smart cities, and urban sanitation are accelerating the installation of wastewater treatment facilities across major cities.

Industrial demand is also rising across textiles, pharmaceuticals, chemicals, food processing, and mining sectors. Domestic manufacturing expansion and growing mining activities are creating additional opportunities for APAM suppliers.

Japan Anionic Polyacrylamide Market Trends

Japan represents a technologically advanced APAM market focused on high-performance water treatment chemicals and industrial process optimization. The country’s mature wastewater treatment infrastructure and advanced manufacturing industries continue generating stable demand for specialty polymer formulations.

Asia Pacific also benefits from strong manufacturing economics, lower production costs, and expanding domestic production capacity. Suppliers are increasingly investing in localized production facilities, regional distribution networks, and technical service centers to strengthen market presence and improve supply chain efficiency across the region.

Competitive Landscape

The global anionic polyacrylamide market is moderately consolidated at the global level, with several multinational manufacturers controlling a significant share of total production capacity. Large companies maintain advantages through integrated manufacturing operations, extensive distribution networks, technical service capabilities, and long-term customer relationships. At the regional level, however, the market remains fragmented due to the presence of numerous local suppliers serving municipal and industrial customers. Competition is influenced by transportation costs, localized technical support, product customization, and regulatory compliance capabilities.

Leading market participants are prioritizing production expansion, regional manufacturing localization, specialty product innovation, and technical service integration. Companies are increasingly differentiating themselves through application optimization, compliance expertise, and long-term customer support programs. Sustainability-focused product development and process efficiency improvements are also becoming important competitive differentiators across municipal and industrial treatment markets.

Key Industry Developments

- In April 2025, Kemira completed the acquisition of Thatcher Group’s iron sulfate coagulant business in the United States, expanding its water treatment chemical portfolio and strengthening its municipal and industrial water treatment presence across North America.

- In March 2025, SNF announced a strategic collaboration with Mitsubishi Chemical Group to commercialize N-vinylformamide (NVF) production technology at SNF’s Dunkirk facility in France, aiming to strengthen its portfolio of specialty water-soluble polymers used in water treatment, papermaking, and oilfield applications.

Companies Covered in Anionic Polyacrylamide Market

- SNF

- Kemira

- Solenis

- BASF

- Solvay

- Kuraray

- Ashland

- Nouryon

- Black Rose Industries

- Anhui Jucheng Fine Chemicals

- Beijing Hengju Chemical Group

- Shandong Polymer Bio-Chemicals

- Xitao Polymer

- PetroChina Daqing Petrochemical

- Anhui Tianrun Chemicals

- Zhejiang Xinhaitian Bio-Technology

Frequently Asked Questions

The global anionic polyacrylamide market is anticipated to be valued at US$4.1 billion in 2026.

The anionic polyacrylamide market is projected to reach approximately US$6.2 billion by 2033.

Key trends include rising investment in wastewater treatment infrastructure, increasing sludge dewatering demand, growing mining water recovery applications, expansion of industrial water recycling systems, and higher adoption of specialty polymer formulations for enhanced treatment efficiency.

Water treatment and wastewater treatment remain the leading application segments, accounting for approximately 48.6% of market demand due to continuous usage across municipal and industrial treatment facilities.

The anionic polyacrylamide market is projected to grow at a CAGR of 6.1% between 2026 and 2033.

Some of the major players include SNF, Kemira, Solenis, BASF and Solvay.