- Beverages

- Coffee Concentrate Market

Coffee Concentrate Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Coffee Concentrate Market is segmented by Coffee Source (Arabica, Robusta, Blends), End- Use (Foodservice / HoReCa, Food Manufacturing, Household Retail), and Regional Analysis, 2026 - 2033

Coffee Concentrate Market Share and Trends Analysis

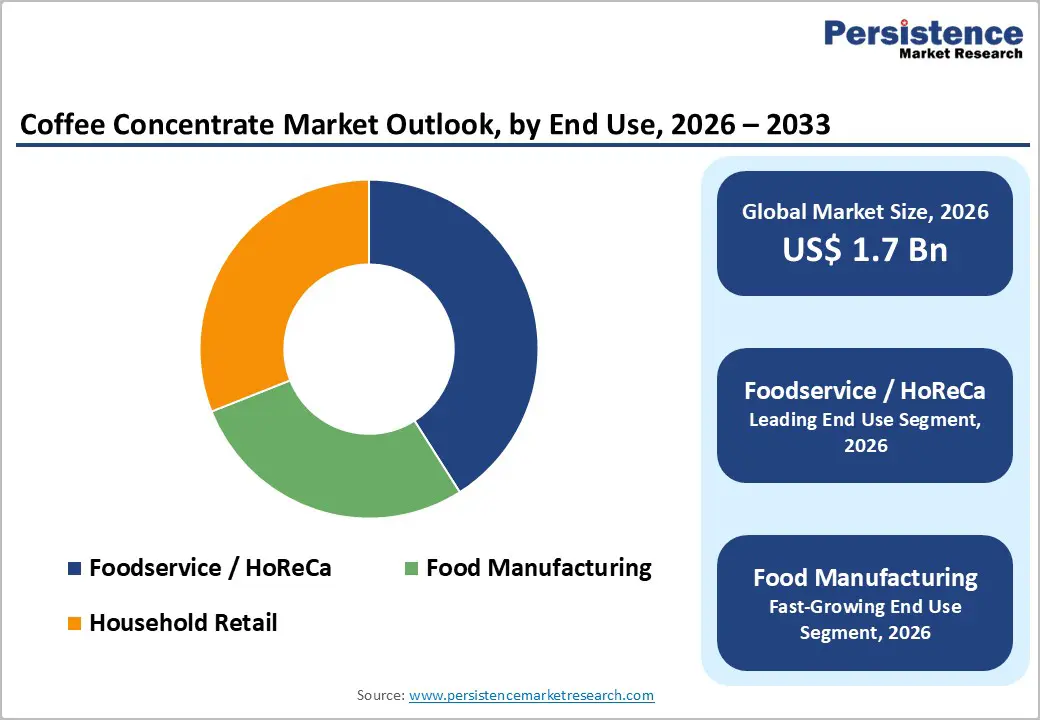

The global Coffee Concentrate market size is expected to be valued at US$ 1.7 billion in 2026 and projected to reach US$ 2.5 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

Market growth is mainly driven by rising demand for convenience-oriented coffee solutions and the rapid worldwide expansion of the cold brew segment. As modern consumers value time-saving options, coffee concentration provides a versatile and high-quality alternative to traditional brewing methods. Additionally, incorporating liquid coffee extracts into industrial food products and the growing popularity of home-based specialty coffee experiences are creating sustainable growth opportunities, especially in urban areas where premiumization of beverages is a prevailing trend.

Key Industry Highlights:

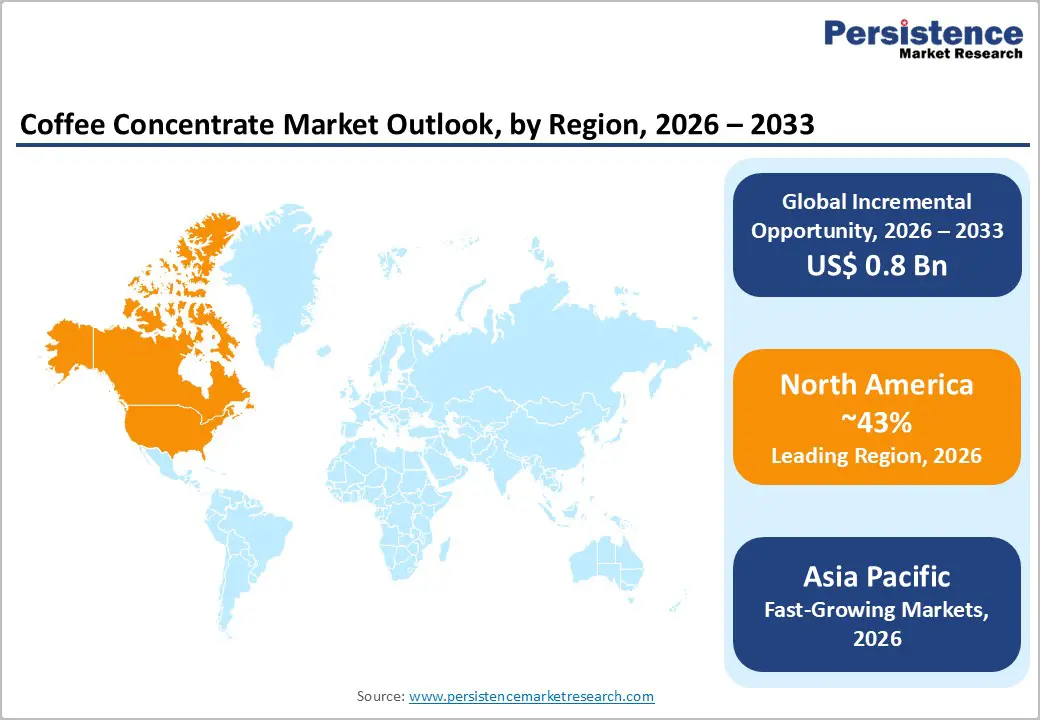

- Leading Region: North America, holding 43% market share, supported by strong cold brew culture, high specialty coffee consumption, and the widespread presence of established beverage players and advanced retail infrastructure.

- Fastest-Growing Region: Asia Pacific, driven by rapid café culture expansion, westernized beverage habits, rising middle-class consumption, and increasing demand for convenient premium coffee formats across China, Japan, and Southeast Asia.

- Leading Coffee Source Segment: Arabica dominates the market due to its superior flavor profile, aromatic complexity, and widespread use in premium coffee concentrate formulations.

- Leading End-use Segment: Foodservice / HoReCa accounts for around 41% market share, as cafés, restaurants, and hotels utilize concentrates for efficient preparation of cold brew, iced coffee, and specialty beverages.

- Growth Indicators: Increasing consumer preference for convenience-oriented beverage solutions and ready-to-mix coffee formats is accelerating the adoption of coffee concentrates in both retail and foodservice channels.

- Opportunities: Sustainable packaging innovations, including recyclable bottles, aluminum cans, and concentrated liquid pouches, are enabling brands to reduce environmental impact while strengthening eco-conscious consumer loyalty.

| Key Insights | Details |

|---|---|

|

Coffee Concentrate Market Size (2026E) |

US$ 1.7 Bn |

|

Market Value Forecast (2033F) |

US$ 2.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

Market Dynamics

Driver - Growing Consumer Preference for Convenience and Ready-to-Drink Formats

A primary driver of the industry is the fundamental shift toward convenience-driven consumption among millennials and Gen Z. According to the National Coffee Association (NCA), coffee consumption remains at record highs, but consumption methods have shifted toward instant-access formats. Coffee concentrates eliminate the need for specialized equipment or long brewing cycles, providing a barista-level experience in seconds. This utility is especially valuable in the Household Retail segment, where consumers use liquid extracts for iced coffees, protein shakes, and baking. The ability to customize strength and flavor while maintaining the nuanced profile of premium beans has positioned concentrates as a superior alternative to traditional soluble powders, driving consistent volume growth across retail channels.

Restraints - High Production Costs and Premium Pricing Barriers

A significant barrier to broader market penetration is the high operational cost associated with advanced extraction and preservation technologies. Producing high-purity concentrates requires sophisticated cold-extraction or thermal-vacuum evaporation processes to retain volatile aromatic compounds. According to industry reports from Persistence Market Research, these technical requirements result in a higher retail price than ground coffee or instant granules. During periods of economic volatility, price-sensitive consumers may pivot toward more affordable traditional formats. Additionally, the premium nature of the raw beans often high-grade Arabica further inflates the cost of goods sold, limiting the addressable market in developing regions where coffee is viewed primarily as a low-cost commodity rather than a lifestyle luxury.

Opportunity - Advancements in Sustainable and Eco-Friendly Packaging Solutions

There is a burgeoning opportunity for market participants to differentiate themselves through sustainable innovation. As consumers become more environmentally conscious, the demand for plastic-free or highly recyclable packaging for coffee liquids is skyrocketing. Opportunities exist for brands to transition to glass bottles, aluminum cans, or concentrated pouches that reduce the overall carbon footprint of shipping. Furthermore, the high concentration levels, where one small bottle replaces multiple bags of ground coffee, allow for a significant reduction in packaging waste per serving. Organizations like the Sustainable Coffee Challenge emphasize that brands prioritizing ethical sourcing and reduced waste are seeing higher consumer loyalty. By highlighting the environmental efficiency of concentrates, companies can attract the eco-conscious demographic while optimizing their own logistics and storage costs.

Category-wise Analysis

Coffee Source Analysis

The Arabica segment is the leading segment in Category-1, accounting for a dominant share of the market in 2025. This leadership is justified by the bean's superior flavor profile, characterized by sweetness, acidity, and aromatic complexity, which are highly prized in the specialty concentrate market. Brands like illycaffè S.p.A. and JDE Peet's N.V. primarily utilize Arabica to ensure the premium quality required for liquid extracts. Conversely, Blends is identified as a significant contributor for the Foodservice sector, as they offer a balanced profile of Arabica’s aroma and Robusta’s body and caffeine content at a more competitive price point. Robusta-heavy concentrates are gaining traction in industrial applications where a strong, bold coffee flavor is needed to stand out against other ingredients.

End Use Analysis

The Foodservice / HoReCa segment was the leading end-user, with a 41% market share in 2025. This dominance is driven by the operational efficiency that concentrates provide to high-volume cafes, hotels, and restaurants. By using liquid extracts, these establishments can serve consistent, high-quality cold brew and specialty drinks with minimal labor. On the other hand, Food Manufacturing is the fastest-growing segment through 2032. The surge in coffee-flavored packaged goods, ranging from protein shakes to artisanal chocolates, is driving industrial-scale demand for concentrates. The Household Retail segment also shows robust growth, fueled by the rise of "at-home barista" trends and the increasing availability of boutique concentrate brands on e-commerce platforms like Amazon and specialized grocery sites.

Region-wise Insights

North America Coffee Concentrate Market Trends and Insights

North America is the leading region in the global market, holding a 43% market share in 2025. The region's leadership is underpinned by a highly developed coffee culture and the massive popularity of cold brew in the United States and Canada. The presence of major industry leaders like Starbucks Corporation and Keurig Dr Pepper Inc. has facilitated the mainstream adoption of coffee concentrates through both retail and foodservice channels.

Innovation in the U.S. is focused on high-concentration formats (e.g., 20x or 30x concentrates) and functional additions such as collagen or vitamins. The FDA's regulatory framework sets high standards for liquid beverage processing, fostering an innovation ecosystem where startups like Jot Coffee and Explorer Cold Brew can thrive. The region's mature e-commerce landscape also plays a vital role, as a significant portion of specialty concentrate sales occurs through direct-to-consumer (DTC) channels, appealing to the tech-savvy urban population seeking premium, customized caffeine solutions.

Asia Pacific Coffee Concentrate Market Trends and Insights

Asia Pacific is identified as the fastest-growing segment for the market through 2033. This rapid expansion is primarily driven by the westernization of diets and the booming coffee shop culture in China, Japan, and South Korea. As the middle class expands, demand for convenient, high-quality coffee solutions among young professionals is surging. China is a major engine of growth, with domestic and international chains rapidly expanding their cold brew and liquid coffee offerings to compete for the morning commute segment.

The region's manufacturing advantages, combined with rising interest in coffee-flavored confectionery and dairy products, are driving industrial demand for concentrates. In countries like Vietnam and Indonesia, major producers of Robusta, there is an emerging trend toward high-caffeine coffee concentrates for the local market. The rapid expansion of modern retail and e-commerce across Southeast Asia is making premium concentrate brands more accessible to a wider demographic. As international players like Starbucks and JDE Peet's increase their regional investments, the Asia Pacific is poised to become a central pillar of the global liquid coffee industry.

Market Competitive Landscape

The coffee concentrate market exhibits a moderately consolidated structure, where a few global beverage giants dominate the high-volume industrial and foodservice channels. Companies like Nestlé S.A., JDE Peet's N.V., and Starbucks Corporation leverage their massive distribution networks and bean-sourcing capabilities to maintain a significant market share. However, the retail landscape remains highly dynamic and fragmented, with a vibrant group of boutique, DTC-focused brands like Jot Coffee, Javvy Coffee Company, and Explorer Cold Brew driving innovation in flavor and concentration levels. Key differentiators employed by market leaders include proprietary cold-extraction technologies and long-term partnerships with estate farmers. Emerging business model trends show a move toward subscription-based services and "miniature" packaging that appeals to the portability needs of travelers and office workers, helping niche players compete against established multinationals.

Key Developments:

- In April 2025, Nescafé introduced Nescafé Espresso Concentrated in the United Kingdom, marking its European debut and targeting the growing demand for convenient at-home iced coffee beverages.

- In November 2025, Nestlé announced plans to invest in production and packaging at its coffee facility in north-west England. In April 2025, Nescafé launched Nescafé Espresso Concentrated in the United Kingdom, marking its European debut and targeting the growing demand for convenient at-home iced coffee beverages.

Companies Covered in Coffee Concentrate Market

- Starbucks Corporation

- Nestlé S.A.

- JDE Peet's N.V.

- Keurig Dr Pepper Inc.

- illycaffè S.p.A.

- Lavazza Group

- Explorer Cold Brew

- Javvy Coffee Company

- The J.M. Smucker Co.

- Jot Coffee

- Others

Frequently Asked Questions

The global Coffee Concentrate market is projected to be valued at US$ 1.7 Bn in 2026.

Growing Consumer Preference for Convenience and Ready-to-Drink Formats is a major factor driving global Coffee Concentrate market.

The Global Coffee Concentrate market is poised to witness a CAGR of 5.5% between 2026 and 2033.

Advancements in Sustainable and Eco-Friendly Packaging Solutions represents a significant opportunity in the Coffee Concentrate market.

Major players in the Global Coffee Concentrate market include Starbucks Corporation, Nestlé S.A., JDE Peet's N.V., Keurig Dr Pepper Inc., Lavazza Group and others