- Food Ingredients & Additives

- Cane Sugar Market

Cane Sugar Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Cane Sugar Market by Product Type (Organic, Conventional), Form (Crystallized Sugar, Non-crystallized sugar), Distribution Channel (Food & Beverage Industry, Pharmaceutical Industry, Personal Care & Cosmetics, Biofuel & Industrial Applications), and Regional Analysis from 2026 to 2033

Cane Sugar Market Share and Trends Analysis

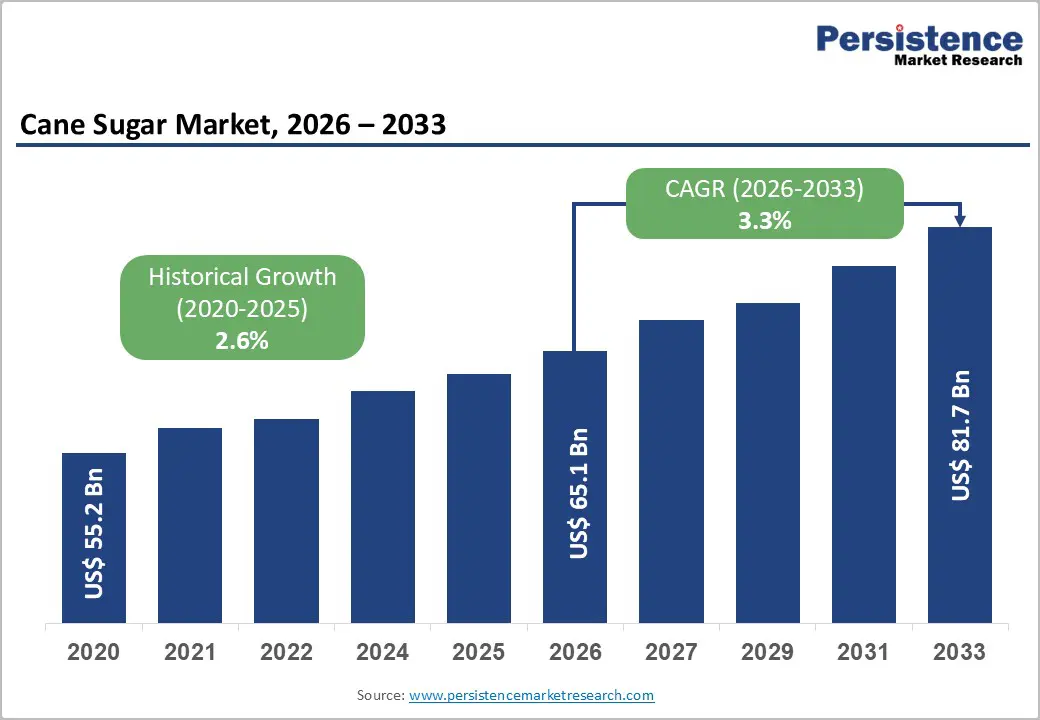

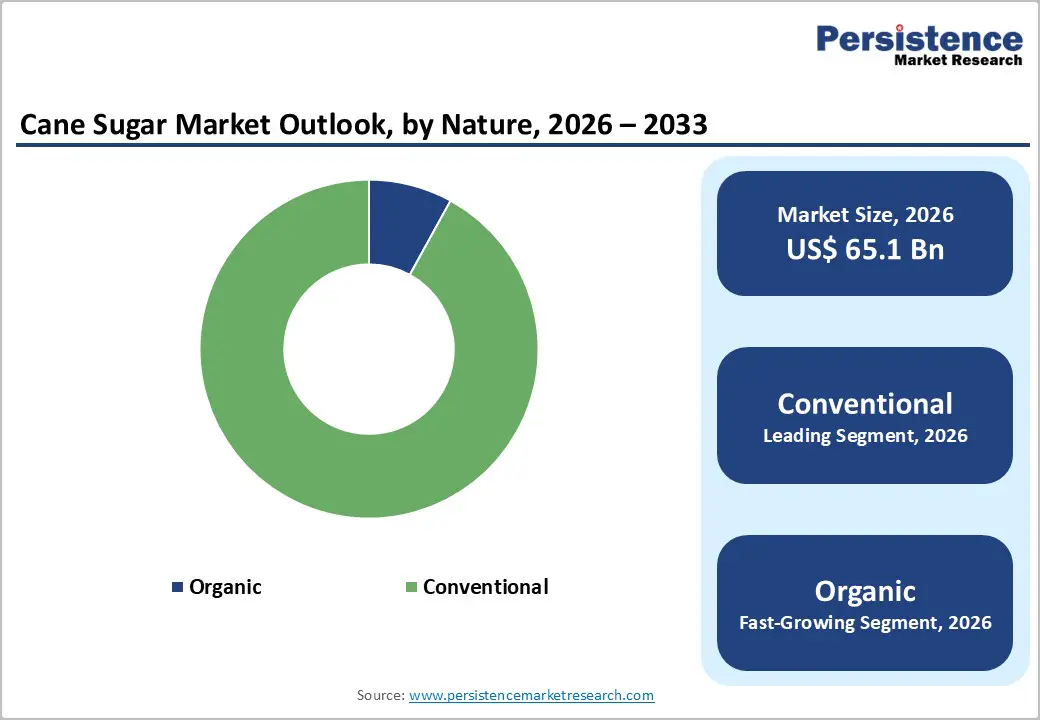

The global cane sugar market is estimated to grow from US$ 65.1 billion in 2026 to US$ 81.7 billion by 2033. The market is projected to record a CAGR of 3.3% during the forecast period from 2026 to 2033.

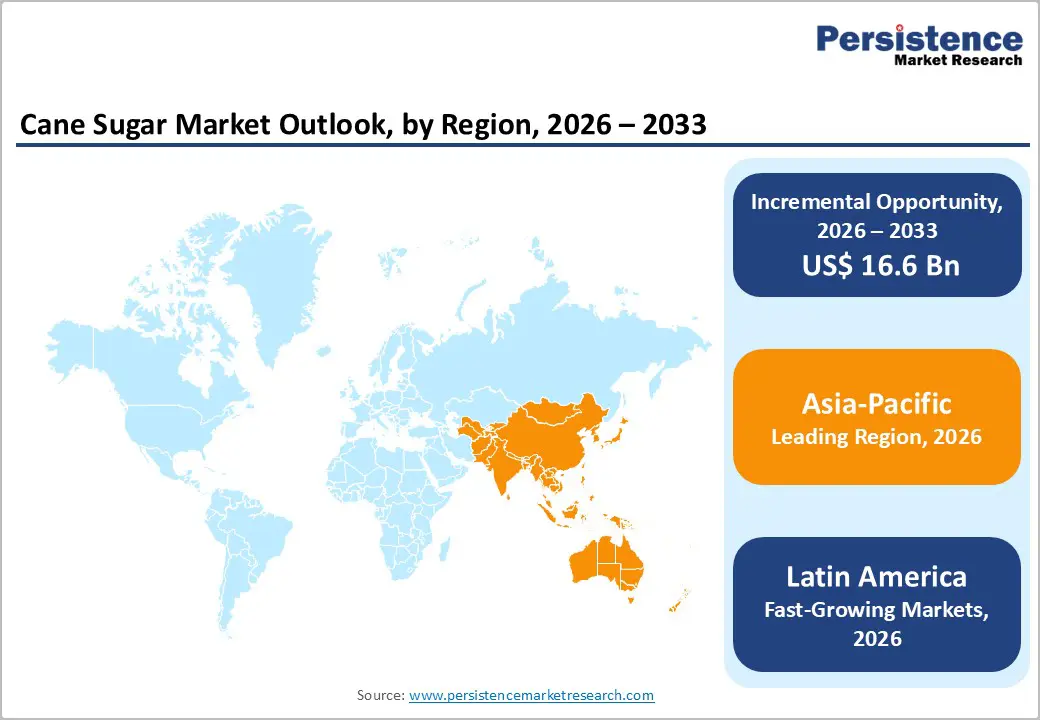

The global market is expanding steadily, driven by rising demand for natural sweeteners and growth in food and beverage processing. North America leads due to strong refining infrastructure and established consumption patterns, while Asia-Pacific is the fastest-growing region, supported by large sugarcane production, increasing population, and expanding food manufacturing industries.

Key Industry Highlights:

- Dominant Product Segment: Conventional cane sugar held 92.0% share in 2025, driven by its large-scale production, affordability, and extensive use in food processing, beverages, confectionery, and bakery products worldwide.

- Dominant Region: Asia Pacific is the leading region in the cane sugar market with 46.5% share in 2025, driven by large sugarcane production in countries like India, Thailand, and China, high population-driven consumption, and expanding food and beverage industries. Strong agricultural support and export activities further strengthen the region’s dominance.

- Growth Indicators: Growth is driven by rising demand for sweeteners in processed foods and beverages, expanding food manufacturing industries, increasing population, and growing use of sugarcane for ethanol and biofuel production.

- Opportunity: Opportunities include expansion of organic and specialty cane sugar products, development of sustainable sugar production, increasing ethanol production from sugarcane, and growing demand from emerging markets and food processing industries.

| Key Insights | Details |

|---|---|

| Global Cane Sugar Market Size (2026E) | US$ 65.1 Bn |

| Market Value Forecast (2033F) | US$ 81.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.6% |

Market Dynamics

Driver: Rising Demand from Food & Beverage Processing Industry

The food and beverage industry is the largest consumer of cane sugar, as sugar is a key ingredient used in bakery products, confectionery, beverages, dairy desserts, and processed foods. According to the Food and Agriculture Organization (FAO), global sugar consumption reached about 187.6 million metric tons in 2022, reflecting strong demand from packaged food and beverage manufacturing worldwide. Sugar remains one of the most widely used caloric sweeteners because it enhances flavor, texture, and shelf life in processed foods. Rapid urbanization and the growing consumption of convenience foods have further increased the demand for sugar as a fundamental ingredient in large-scale food production.

In addition, global demand for sugar is projected to continue expanding due to rising population and increasing food processing activities. The OECD-FAO Agricultural Outlook estimates that worldwide sugar consumption could reach around 202 million metric tons by 2034, growing at approximately 1.2% annually. Much of this growth is expected in emerging economies where processed food consumption is increasing, and beverage markets are expanding rapidly. Since more than 85% of the world’s sugar is derived from sugarcane, the expansion of food manufacturing and beverage industries directly drives demand in the cane sugar market.

Restraint: Growing Health Concerns Related to Excess Sugar Consumption

Despite strong demand, rising health concerns related to excessive sugar intake are restraining the cane sugar market. Medical research and public health agencies have increasingly linked high sugar consumption with conditions such as obesity, diabetes, cardiovascular disease, and dental problems. The World Health Organization (WHO) recommends limiting free sugar intake to less than 10% of total daily energy intake, and ideally below 5% for additional health benefits. These recommendations have encouraged governments and health organizations to promote sugar reduction strategies and encourage consumers to choose low-sugar diets.

Growing health awareness has also led to policy interventions aimed at reducing sugar consumption. For example, several countries have introduced taxes on sugar-sweetened beverages and high-sugar products to discourage excessive intake. Public health data also show the scale of the issue: over 2.5 billion people worldwide suffer from dental caries, one of the most common diseases associated with high sugar consumption. Such health concerns are pushing consumers toward reduced-sugar foods and alternative sweeteners, which may limit the growth potential of the traditional cane sugar market over time.

Opportunity: Rising Demand for Organic and Specialty Cane Sugar

The growing preference for natural and sustainably produced foods has created opportunities for organic and specialty cane sugar products. Consumers are increasingly seeking food ingredients that are minimally processed and produced using environmentally responsible farming practices. This trend is particularly strong in developed markets where demand for clean-label and organic products is rising. As a result, food manufacturers are incorporating organic cane sugar in premium beverages, bakery products, and natural sweetener blends to meet changing consumer preferences for healthier and traceable ingredients.

Agricultural trends also support this opportunity. Global sugarcane production exceeded 1.9 billion tonnes in 2022, with countries such as Brazil and India producing around 38% and 23% of global output, respectively, according to FAO data. Large-scale cultivation creates strong supply potential for differentiated sugar products such as organic, raw, and minimally refined cane sugars. As consumers increasingly prioritize sustainability, fair-trade sourcing, and natural ingredients, producers and food companies are expanding their portfolios with premium cane sugar products, creating significant growth opportunities in the global cane sugar market.

Category-wise Insights

By Nature

Conventional cane sugar dominates the market with 92.0% share in 2025, because it is produced on a much larger scale and at lower cost compared with organic sugar. Most sugarcane cultivation globally follows conventional farming methods using fertilizers and crop protection inputs to maintain high yields and stable supply. According to the Food and Agriculture Organization (FAO), global sugarcane production exceeded 1.9 billion tonnes in 2022, making it one of the largest agricultural crops worldwide. Countries such as Brazil, India, and Thailand account for a significant share of this production, and the majority is cultivated using conventional practices. Large food and beverage manufacturers require consistent and affordable sugar supplies, which conventional production systems provide. In contrast, organic sugar requires certification, strict cultivation standards, and typically produces lower yields, limiting its share in the global market.

By Form

Crystallized sugar dominates the cane sugar market because it is the most practical and widely used form of sugar for both industrial and household consumption. During processing, sugarcane juice is crystallized to produce solid sucrose crystals, such as granulated and refined sugar, which are easy to transport, store, and measure during manufacturing. According to the OECD-FAO Agricultural Outlook, global sugar production is estimated at around 186-187 million tonnes annually, with most of this output distributed in crystalline form for commercial use. Crystallized sugar is extensively used in bakery, confectionery, dairy products, beverages, and packaged foods because it provides consistent sweetness, texture, and stability. Its long shelf life and compatibility with large-scale food processing make crystallized sugar the dominant form in the global cane sugar market.

Regional Insights

Asia Pacific Cane Sugar Market Trends

Asia Pacific dominates the cane sugar market mainly due to its large-scale sugarcane production and high consumption levels. Countries such as India, China, and Thailand are among the world’s largest producers and consumers of sugar. According to the Food and Agriculture Organization (FAO), India produced about 490 million tonnes of sugarcane in 2022, making it one of the top global producers, while Thailand and China also contribute significantly to the regional supply. The region’s large population and growing food and beverage industry drive substantial sugar demand. In addition, government support programs for sugarcane cultivation and ethanol blending initiatives in countries like India further strengthen the production and consumption of cane sugar, reinforcing Asia Pacific’s leading position in the global market.

Europe Cane Sugar Market Trends

Europe remains an important region in the cane sugar market because of its strong sugar refining industry and high demand from the food processing sector. Although much of Europe’s domestic sugar production comes from sugar beet, the region imports significant quantities of raw cane sugar for refining. According to the European Commission, the European Union imported about 1.7 million tonnes of raw sugar in 2023, mainly from developing countries under trade agreements. These imports are processed in large refining facilities across countries such as the United Kingdom, Portugal, and Italy. Europe also has a well-established confectionery, bakery, and beverage industry that requires stable sugar supplies, making cane sugar imports an important component of the region’s overall sugar market.

North America Cane Sugar Market Trends

North America is emerging as one of the fastest-growing regions in the cane sugar market due to increasing demand from the food and beverage sector and rising consumer preference for natural sweeteners. The United States remains one of the world’s largest sugar consumers. According to the United States Department of Agriculture (USDA), total sugar consumption in the U.S. reached approximately 11.5 million short tons in 2023. The region also produces sugarcane in states such as Florida, Louisiana, and Texas, supporting domestic supply. Additionally, the expansion of processed food production, growing demand for organic and minimally refined sugars, and rising imports from major producing countries are contributing to the steady growth of the cane sugar market in North America.

Competitive Landscape

The cane sugar market is highly competitive, led by major producers and agribusiness companies such as Wilmar International, Raízen, and ASR Group. Companies focus on expanding sugarcane processing capacity, improving refining efficiency, and diversifying into ethanol and bioenergy while strengthening global export networks and supply chains to maintain market share.

Key Industry Developments:

- In September 2025, BASF announced that it completed the sale of its Food and Health Performance Ingredients business to Louis Dreyfus Company. The transaction marked BASF’s strategic move to streamline its portfolio and focus on its core chemical and industrial businesses.

- In June 2025, ASR Group announced that it optimized its U.S. operational network to improve efficiency and strengthen its supply chain across the country. The company implemented strategic adjustments in its production and distribution operations to better align with market demand and enhance overall operational performance.

Companies Covered in Cane Sugar Market

- Louis Dreyfus Company B.V.

- Wilmar Sugar Australia Limited

- ASR Group International, Inc.

- Biosev S.A.

- Nanning Sugar Industry

- Bunge Limited

- Raizen

- Shree Renuka Sugars Limited

- Bajaj Hindusthan Sugar Limited

- Balrampur Chini Mills Limited

- Florida Crystals Corporation

- Others

Frequently Asked Questions

The global cane sugar market is projected to be valued at US$ 65.1 Bn in 2026.

Rising demand from food and beverage industry, population growth, expanding processed foods, and increasing sugar consumption globally.

The global cane sugar market is poised to witness a CAGR of 3.3% between 2026 and 2033.

Expansion of organic cane sugar, ethanol production, emerging market demand, sustainable farming, and value-added sugar products.

Louis Dreyfus Company B.V., Wilmar Sugar Australia Limited, ASR Group International, Inc., Biosev S.A., Nanning Sugar Industry, Bunge Limited.