- Metalworking & Fabrication

- Broaching Machines Market

Broaching Machines Market Size, Share, and Growth Forecast, 2026 - 2033

Broaching Machines Market by Product Type (Horizontal Broaching Machine, Vertical Broaching Machine, Surface Broaching Machine, and Others), End-user (Automotive, Aerospace & Defense, Industrial Machinery, Metalworking & Fabrication, Others), and Regional Analysis for 2026 - 2033

Broaching Machines Market Size and Trends Analysis

The global broaching machines market size is likely to be valued at approximately US$ 539.2 million in 2026 and is projected to reach US$ 747.3 million by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033.

This growth trajectory reflects robust demand for precision machining across automotive, aerospace, and defense sectors, driven by increasing adoption of advanced manufacturing technologies, including CNC integration and Industry 4.0 digitalization.

The market's expansion is underpinned by rising requirements for sub-micron tolerances in electric vehicle powertrains, continuous emphasis on production efficiency improvements, and strategic capital investments in automated broaching systems across developed and emerging markets. These factors collectively position the broaching machines market for sustained mid-single-digit growth despite inflationary pressures on raw materials and labor costs.

Key Industry Highlights:

- Market Challenges: High capital costs, volatile raw material prices, and skilled labor shortages restrict broaching adoption, especially among small and mid-sized manufacturers globally.

- Opportunity: Electrified retrofits of hydraulic broaching machines are a strong opportunity, improving energy efficiency, precision control, reliability, and long-term sustainability compliance.

- Product Type Analysis: Horizontal broaching maintains over 45% revenue share, while vertical broaching accelerates the fastest, driven by rising deployment in aerospace, defense, and gear machining.

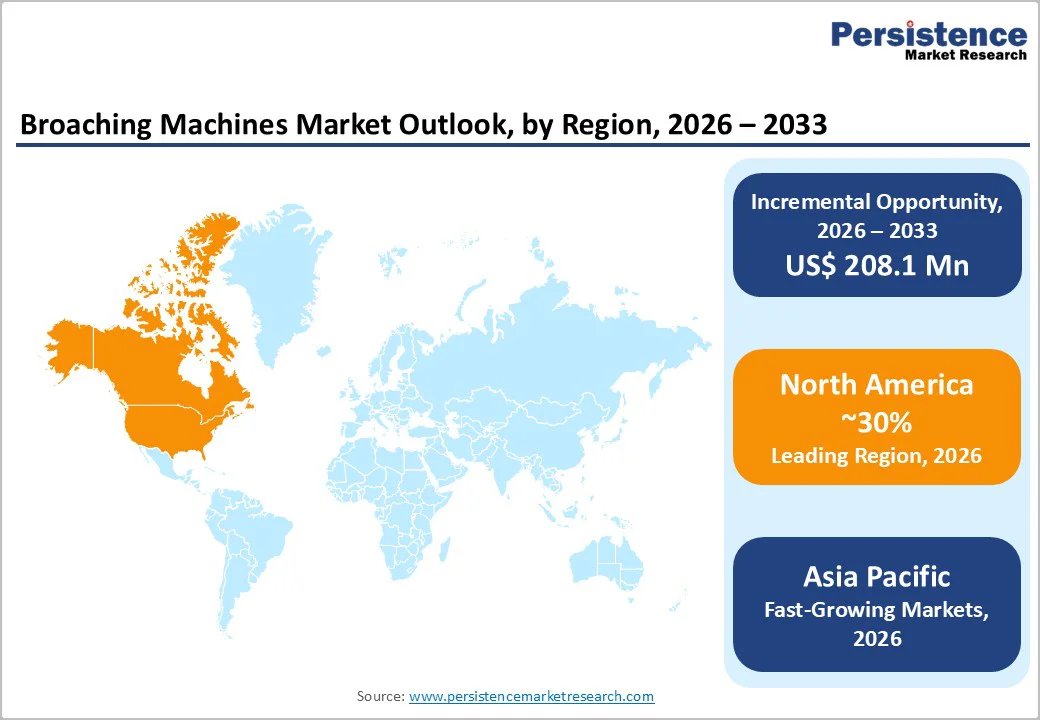

- Regional Market Performance: North America and Asia Pacific drive global demand, supported by EV manufacturing expansion, aerospace modernization, automation upgrades, and growing precision engineering requirements. Overall, North America is likely to dominate with an exceeding 30% revenue share in the forecast period.

| Key Insights | Details |

|---|---|

| Broaching Machines Market Size (2026E) | US$ 539.2 Mn |

| Market Value Forecast (2033F) | US$ 747.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.6% |

Market Dynamics

Drivers - Rising Demand for Precision Engineering in Electric Vehicle Manufacturing

The electric vehicle (EV) sector has emerged as a primary growth catalyst for the broaching machines market, reinforced by the rapid global acceleration in EV adoption. According to the IEA, global electric car sales continue to set new benchmarks despite broader economic pressures on the automotive industry.

As EV models become more cost-competitive, sales surpassed 17 million units in 2024, accounting for more than 20% of total car sales.

Notably, the additional 3.5 million EVs sold in 2024 compared with 2023 alone exceed the entire global EV sales volume recorded in 2020. Looking ahead, electric car sales are projected to exceed 20 million units in 2025, pushing their share to over one-quarter of all cars sold worldwide. Momentum remained strong in early 2025, with global EV sales rising 35% year-on-year in Q1 2025.

This explosive rise in EV production directly intensifies demand for precision machining technologies. Modern EV powertrains require unprecedented dimensional accuracy, particularly tooth accuracy of ±0.0005 inches for transmission components, making broaching the preferred machining method at scale.

Integrated e-axle architectures increasingly consolidate multiple gears, splines, and keyways into a single compact housing, further amplifying the requirement for adaptable broaching systems capable of executing internal and surface cuts in a single line.

Chinese manufacturers, supported by policy loans and targeted tax incentives, are already deploying advanced horizontal broach cells equipped with fully enclosed servo drives that maintain dimensional drift below 2 microns across 20-hour production cycles.

These high-precision, high-throughput systems are setting new global productivity benchmarks that competing regional and international manufacturers must now match to remain competitive in the rapidly evolving EV machining landscape.

Industry 4.0 Digitalization and Smart Manufacturing Integration

Manufacturers are systematically retrofitting production environments with IoT-enabled broaching machines integrated with advanced control systems, creating significant opportunities for replacement and upgrades. Real-time monitoring capabilities, predictive maintenance modules, and remote diagnostics enhance operational efficiency while reducing unplanned downtime, and are critical advantages in high-volume, cost-sensitive manufacturing environments.

North American and European manufacturers increasingly prioritize machines with fully enclosed servo drives, high-speed capabilities, and modular broach heads offering quick-change guides that reduce setup times by approximately 40%.

These technological advancements support the broader Industry 4.0 ecosystem, enabling manufacturers to achieve tighter production tolerances, compress manufacturing cycle times, and optimize asset utilization rates while generating valuable operational datasets for continuous improvement initiatives.

Restraint - Cost Pressures, Capital Barriers, and Limited Adoption Capacity in Broaching Machines

Broaching machine manufacturers continue to face persistent challenges driven by fluctuating prices for tungsten carbide, alloy steels, and other specialty metals, which directly elevate production costs and compress profit margins. These pressures are amplified by skilled labor shortages in developed markets, which limit operational flexibility and hinder the ability to absorb raw material volatility.

At the same time, competition from cost-competitive Asian manufacturers intensifies pricing pressure across the global supply chain, squeezing the profitability of regional players and restricting their ability to invest in technological upgrades. Small and mid-sized manufacturers are particularly vulnerable due to limited supply chain diversification, weaker procurement leverage, and the absence of integrated production capabilities.

Compounding these cost pressures are high capital requirements and long payback periods associated with broaching machinery procurement. The complex specifications, customization needs, and precision engineering involved in broaching systems extend purchasing cycles and deter investment, especially for organizations with limited upfront capital.

Economic uncertainties and stricter credit conditions in certain regions further reduce willingness to commit to large capital expenditures, constraining adoption among small and mid-sized enterprises despite clear productivity advantages.

Although emerging models such as Equipment-as-a-Service (EaaS), remote diagnostics, and predictive maintenance offer more accessible pathways for modernization, their adoption remains at an early stage. It is insufficient to offset the traditional capital barriers that continue to limit market expansion in the near term.

Opportunity - Retrofitting Existing Hydraulic Systems with Electric Drives and Servo Technologies

A substantial market opportunity exists in retrofitting traditional hydraulic broaching machines with electrified drives and servo systems to enhance energy efficiency, precision, and operational reliability. Electrification reduces hydraulic leaks, lowers maintenance requirements, enables real-time digital control, and extends machine lifespan without requiring complete replacement, presenting compelling value propositions for cost-sensitive manufacturing environments.

As regulatory frameworks tighten around energy consumption and sustainability requirements, particularly within Europe following the implementation of Regulation (EU) 2023/1230, electrified retrofits align seamlessly with mandated modernization initiatives and cleaner production requirements. This retrofit market segment can potentially represent 15-20% of annual equipment spending across mature industrial regions.

Category-wise Analysis

Product Type Insights

Horizontal broaching machines continue to dominate the global market, accounting for over 45% of revenue and more than 60% of total installations worldwide.

Their ability to handle complex, large-scale components with high precision makes them essential for automotive transmission systems, aerospace structural parts, and heavy industrial machinery. These machines integrate seamlessly into automated production lines, delivering consistent quality and high throughput while reducing labor dependency, key factors that reinforce their long-term leadership through 2033.

Alongside this dominance, vertical broaching machines are emerging as the fastest-growing segment, projected to expand at a 4.9% CAGR by 2034. Their compact footprint and superior ability to handle heavier workpieces make them ideal for manufacturers operating in space-constrained facilities.

Enhanced performance in deep, intricate cutting, combined with strong compatibility with automation and lean manufacturing workflows, is driving rising adoption across aerospace precision parts, gear assemblies, and defense components. Surface and specialized broaching systems serve niche but critical applications, contributing around 15% of market revenue by supporting precision external profiling in aerospace, heavy machinery, and industrial equipment manufacturing.

End-user Insights

Three major end-use sectors shape the broaching machine market, led prominently by automotive, which consistently accounts for more than 40% of global revenue. This dominance stems from the sector’s deep reliance on precision machining for transmission components, engine structures, steering assemblies, and drivetrain systems.

The rapid shift toward electric mobility further strengthens this demand, as EV powertrains require extremely tight tolerances and refined geometries for compact e-axle and motor components. In North America alone, 55-60% of broaching machine consumption originates from automotive applications, with Europe and Asia exhibiting similar concentration patterns.

Parallel to this, the aerospace & defense sector is emerging as the fastest-growing segment, expanding at a 4.9% CAGR. Fleet modernization programs, defense manufacturing localization, and rising adoption of lightweight, high-strength materials continue to drive investment in high-precision broaching capabilities.

Applications such as landing gear parts, aerospace housings, and defense ordnance components require premium equipment with advanced controls and full traceability, supporting higher pricing and strong adoption, especially in North America, which will represent about 43% of the market by 2034.

Regional Insights and Trends

North America Strengthens Broaching Market Leadership Through Automation, Aerospace Growth, and EV Manufacturing Expansion

North America accounts for nearly 30% of the global broaching machine market revenue in 2026, maintaining its leadership through strong technological innovation, advanced automation adoption, and a well-established aerospace and defense manufacturing base.

The United States remains the core growth engine, supported by the resurgence of domestic automotive production, especially electric vehicle platforms, and sustained capital spending across defense programs.

The rapid adoption of automation, CNC-controlled systems, and Industry 4.0-aligned manufacturing practices drive growth in the region. Demand is reinforced by the region’s strong ecosystem of aerospace, automotive, and industrial machinery manufacturers, all of which require high-precision, reliable broaching solutions.

American OEMs increasingly deploy servo-driven broaching systems with predictive maintenance features to boost efficiency and quality. Regulatory incentives supporting digital transformation and factory modernization further strengthen equipment spending.

A notable example includes American Broach & Machine Company supplying high-speed internal broaching systems for Ford’s EV transmission program. Ongoing investments in smart factories, aerospace modernization, and EV drivetrain capacity, combined with retrofit opportunities for hydraulic-to-electric system upgrades, position North America as a sustained high-value market through 2027 and beyond.

Asia Pacific Accelerates as Global Hub for Advanced Broaching Machinery Growth and Investment

Asia Pacific stands out as the fastest-growing region, expanding at a 4.9% CAGR, driven by rapid industrialization, rising automotive production, and accelerating aerospace manufacturing capabilities. Within the region, India leads with a 6.6% CAGR, the highest among all country markets, while China remains the dominant contributor supported by strong government investment programs, EV manufacturing leadership, and defense modernization initiatives.

China’s machine-tool investment roadmap targets 25% real growth by 2027, emphasizing advanced precision broaching systems for EV drivetrains, gearboxes, and defense components. Policy-backed incentives, including tax credits, subsidized loans, and procurement prioritization, enable the deployment of servo-driven broaching cells that achieve sub-2-micron tolerances.

Japan, with its mature automotive and precision engineering ecosystem, continues to generate stable demand for high-accuracy broaching machines and is projected to grow at 4.4% CAGR through 2034. India’s expanding automotive production base, Smart Factory initiatives, and strong push for industrial automation attract global broaching machine OEMs to set up localized manufacturing and technical support operations.

The region’s competitive advantages, including lower production costs, skilled labor availability, and supportive industrial policies, continue to draw large-scale capital investments. Post-pandemic supply chain diversification is accelerating manufacturing relocation into Asia, strengthening demand for capital equipment.

Additionally, expanding aerospace capabilities in India and China broadens broaching applications beyond traditional sectors, reducing market concentration risk and elevating Asia Pacific’s long-term growth potential.

Competitive Landscape

The global broaching machines market exhibits a fragmented competitive structure, with no single manufacturer commanding a dominant share exceeding 15% of total market value. Market fragmentation reflects specialized application requirements, regional manufacturing preferences, and customer relationships favoring localized suppliers offering customized solutions and responsive service.

Leading companies, including Nachi-Fujikoshi Corp., Mitsubishi Heavy Industries Machine Tool Co. Ltd., American Broach and Machine Company, The Ohio Broach & Machine Co., and Danish Broach Company, collectively represent approximately 35-40% of global market revenue.

The remaining 60-65% is distributed across specialized regional manufacturers, boutique equipment providers, and emerging suppliers establishing market presence through technology differentiation or cost leadership positioning.

Market concentration reflects technological barriers to entry, established customer relationships spanning decades, and specialized expertise requirements limiting competitive pressures. However, emerging Chinese manufacturers increasingly penetrate developed markets through cost-advantaged offerings and aggressive pricing strategies, creating competitive intensity particularly in standardized horizontal broaching machine segments.

Equipment-as-a-Service subscription models and remote diagnostics are fragmenting traditional market structures, enabling smaller manufacturers to compete with established leaders by reducing capital barriers and enhancing service accessibility.

Key Industry Developments:

- In December 2022, NIDEC CORPORATION launched the Robot Camera SPEED for hobbing tools and MAX for broaching tools. Using high-resolution digital imaging, these systems inspect tool edges for defects such as chipping, coating wear, and missing parts. By automating inspection and data storage, they enhance Nidec’s tool production and regrinding processes, cutting inspection time by up to 90%.

- In September 2022, CNC Broach Tool LLC introduced indexable carbide spline-cutting inserts compatible with its existing holders. Featuring TiN coating and dual cutting edges, the inserts enable internal and external spline broaching directly on mills and CNC lathes. This eliminates costly pull-broach machines, reduces subcontracting, lowers lead times, and supports automated blind-hole broaching.

Companies Covered in Broaching Machines Market

- MITSUBISHI HEAVY INDUSTRIES, LTD.

- Accu-Cut

- Apex Broaching Systems

- Broaching Machine Specialties

- Colonial tool group Inc.

- The Ohio Broach & Machine Co.

- Pioneer Broach

- The Ohio Broach & Machine Co.

- AXISCO PRECISION MACHINERY CO., LTD.

- YAO SHENG MACHINERY CO., LTD.

- Power Broach

- YEOSHE HYDRAULICS TECHNOLOGY CO.,LTD

- Taizhou Chengchun Automation Co., Ltd.

- Other Market Players

Frequently Asked Questions

The Broaching Machines market is estimated to be valued at US$ 539.2 Mn in 2026.

The key demand driver for the Broaching Machines market is the rising production of precision-engineered automotive, aerospace, and industrial components that require high-accuracy internal and external profiling.

In 2026, the North America region will dominate the market with an exceeding 30% revenue share in the global Broaching Machines market.

Among end-users, automotive has the highest preference, capturing beyond 30% of the market revenue share in 2026, surpassing other end-users.

MITSUBISHI HEAVY INDUSTRIES, LTD., Accu-Cut, Apex Broaching Systems, Broaching Machine Specialties, Colonial Tool Group Inc., and The Ohio Broach & Machine Co. are a few leading players in the Broaching Machines market.