- Metalworking & Fabrication

- Deburring Machine Market

Deburring Machine Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Deburring Machine Market by Machine Type (Vibratory Deburring, Barrel Tumbling Deburring, Brush Deburring, Thermal Deburring, Electrochemical Deburring, High-Pressure Water Jet Deburring, Misc.), Deburring Media (Ceramic Media, Steel Media, Plastic Media, Organic Compounds), Operation Mode (Automatic, Semi-Automatic, Manual), Industry (Automotive, Aerospace & Defense, Electronics, Medical Devices, Metal Fabrication, Others), and Region Analysis for 2026 to 2033

Deburring Machine Market Trends & Analysis

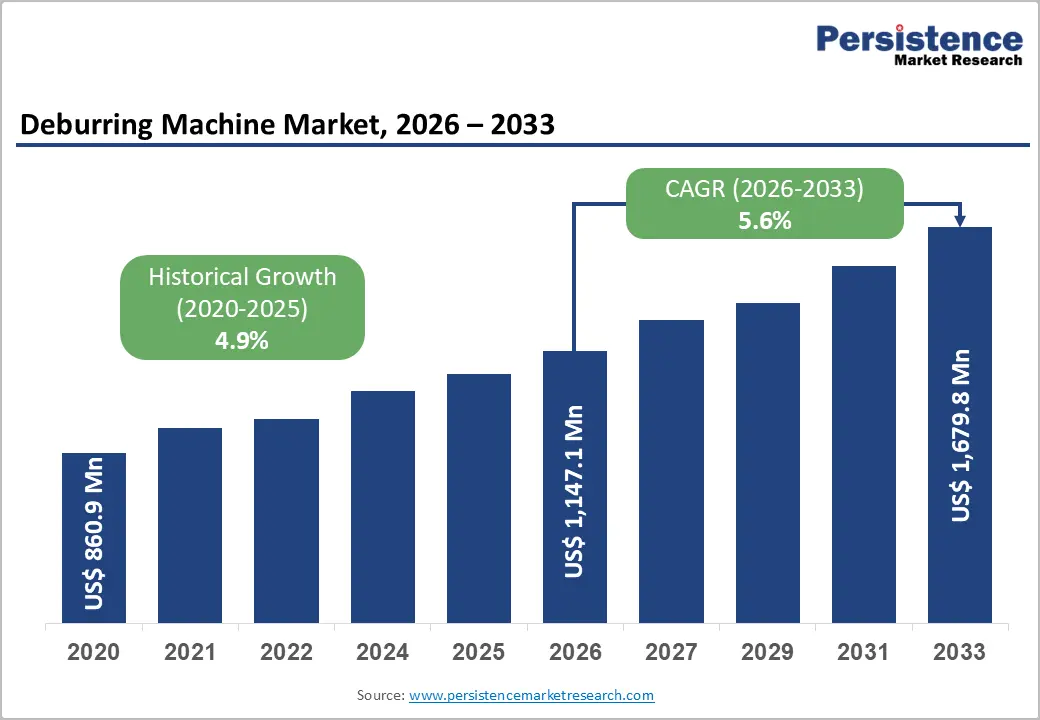

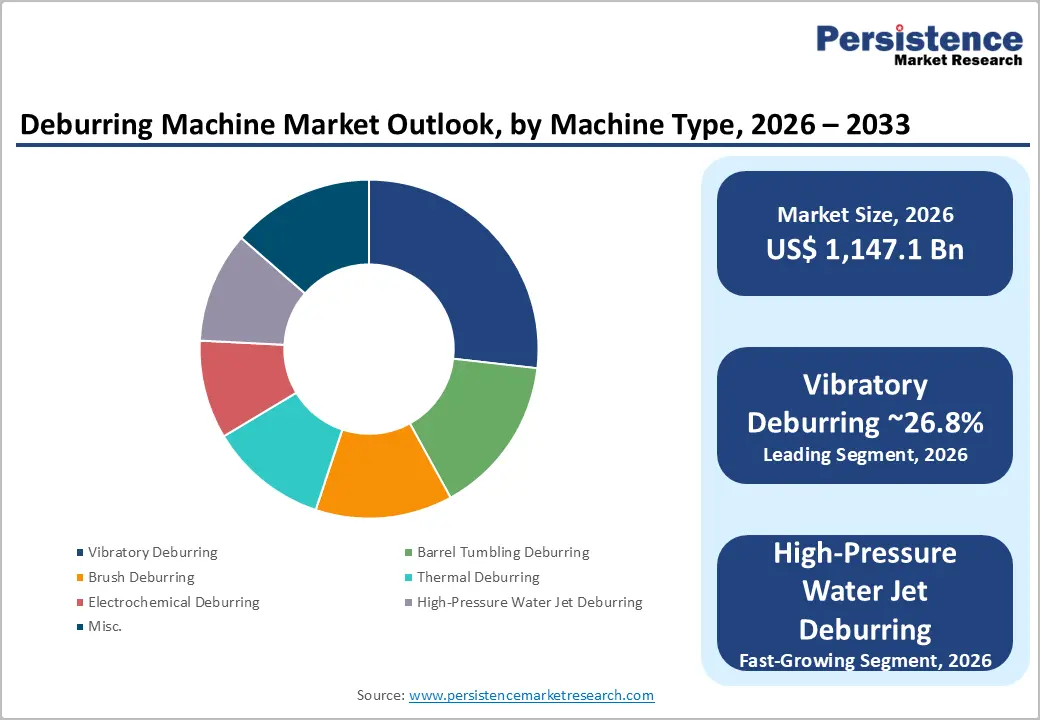

The global deburring machine market size is likely to be US$1,147.1 million in 2026 and is projected to reach US$ 1,679.8 million by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

Need for precision components, quality standards across automotive, aerospace, and medical device sectors mandating burr-free surface specifications, accelerating Industry 4.0, automation adoption driving automated deburring cell integration, and expanding medical device and electronics manufacturing in the Asia Pacific, generating new high-specification deburring demand, are the primary growth drivers.

Key Industry Highlights:

- Leading Machine Type: Vibratory deburring leads at 26.8% share; high-pressure water jJet deburring attains a fast-growth 7.1% CAGR, driven by EV component and semiconductor precision finishing adoption globally.

- Leading Deburring Media: Ceramic media leads at 37.9% share; steel media to have a promising CAGR at 6.3%, driven by hardened automotive and commercial vehicle component tumbling application expansion.

- Leading Operation Mode: Automatic leads at 54.8% share; Semi-automatic to experience fast-growth at 5.5% CAGR, driven by mid-volume precision medical device and aerospace contract manufacturer adoption.

- Leading End-user: Automotive leads at 29.8% share; aerospace & defense to reach 6.1% CAGR driven by NADCAP-certified turbine component deburring and NATO defense manufacturing investment.

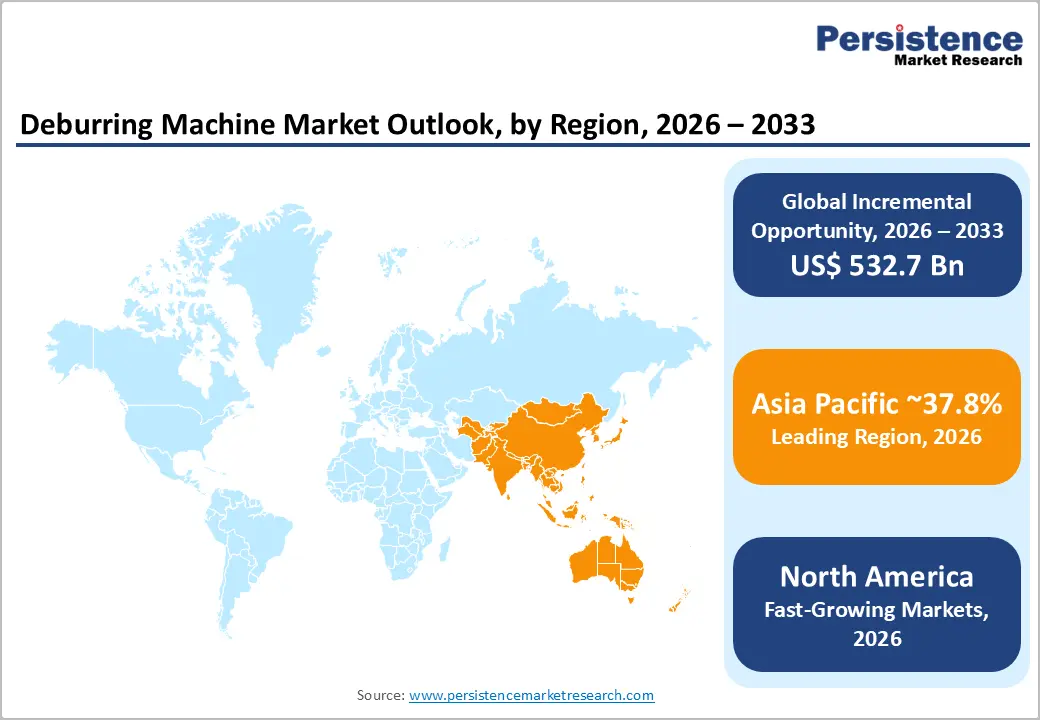

- Regional Performance: North America leads with a 31.6% share, followed by Asia Pacific with a 6.2% CAGR, led by China at US$ 181.2 Mn and India at US$ 40 Mn in 2026.

- Strategic Developments: ATI's Compliant Deburring Blade launch (February 2025) and AXIOME's NADCAP robotic deburring contract with Safran (November 2023) are defining next-generation robotic integration and aerospace precision deburring capability standards globally.

Market Dynamics Analysis

Drivers - Precision Component Quality Mandates Across Automotive and Medical Device Sectors Compelling Deburring Adoption

Global automotive production exceeding 93 million vehicles annually (OICA) drives continuous demand for burr-free metal component surface finishing, with ISO 9001 quality management systems and IATF 16949 automotive quality standards mandating zero-burr component delivery specifications for transmission, engine, braking, and steering system parts that cannot be achieved solely through machining. Each vehicle platform generates 200-500 components that require post-machining deburring, creating a high-frequency, volume-proportional relationship between automotive production scale and deburring machine utilization.

The U.S. FDA's 21 CFR Part 820 Quality System Regulations and the EU Medical Device Regulation (MDR 2017/745) impose surface-finishing standards for implantable medical device components, including orthopedic implants, surgical instruments, and cardiovascular devices, where residual burrs pose direct patient safety risks and require validated deburring process documentation.

The global medical device market is projected to exceed US$ 800 Bn by 2030 (WHO Medical Device Atlas), with precision deburring machine demand scaling proportionally as implant and minimally invasive instrument manufacturing volumes expand across North American, European, and, increasingly, Asia Pacific production facilities, which are demanding ISO 13485-compliant surface finishing validation through 2033.

Industry 4.0 Automation Integration Driving Automated Deburring Cell Adoption Across Manufacturing

The International Federation of Robotics (IFR) World Robotics 2024 Report documented 590,000 industrial robot installations globally in 2023, with robotic deburring, grinding, and finishing applications representing the fifth-largest robot deployment category across automotive and aerospace manufacturing. Automated deburring cells integrating CNC machining centers, six-axis robotic arms with force-torque sensing, and vision-guided burr detection systems are replacing manual and semi-automatic deburring operations across high-volume automotive and aerospace Tier 1 suppliers pursuing labor cost reduction, throughput consistency, and ISO surface quality documentation requirements.

Automated deburring machine configurations command 54.8% of the global market, reflecting OEM and Tier 1 supplier investment in integrated production-line deburring cells that eliminate inter-process material handling, reduce cycle-time variability, and enable real-time process-parameter logging for IATF 16949 and AS9100 aerospace quality compliance.

EMAG GmbH's ECM precision electrochemical deburring systems and BENSELER's industrial deburring automation platforms are directly targeting Tier 1 automotive and aerospace precision component manufacturers investing in next-generation automated finishing cell integration aligned with Industry 4.0 smart factory architectures across Germany, the U.S., Japan, and China.

Restraints - Complexity of Multi-Material and Complex Geometry Deburring Constraining Automation Deployment

Deburring machine automation adoption faces significant technical barriers when applied to complex internal channel burrs, cross-drilled hole intersections, and multi-material assemblies combining metals, polymers, and composites, where standard vibratory, tumbling, and brush deburring systems cannot access internal geometry reliably without risking dimensional tolerance degradation. The American Society for Precision Engineering estimates that 35-40% of precision-machined component geometries in aerospace and medical device applications require manual or semi-automatic deburring operations due to automation accessibility constraints, structurally limiting the addressable market for fully automated deburring solutions and constraining market penetration velocity in complex geometry precision manufacturing segments.

Deburring Process Validation Requirements Constraining Market Entry Speed in Regulated Industries

Deburring machine adoption in aerospace (AS9100D), medical device (ISO 13485), and defense (MIL-SPEC) manufacturing environments requires comprehensive process validation documentation, including Installation Qualification (IQ), Operational Qualification (OQ), and Performance Qualification (PQ) protocols, that extend new machine qualification timelines by 12-24 months per facility.

The European Medicines Agency's and FDA's Part 820 validation requirements for medical device surface finishing processes impose regulatory documentation burdens that constrain the adoption velocity of new deburring machine technology at established regulated-industry facilities, with non-compliant process changes carrying potential product recall exposure quantified at US$ 1-50 Mn per affected device family.

Opportunities - High-Pressure Water Jet Deburring Adoption for EV Component and Semiconductor Precision Finishing

High-pressure water jet deburring, operating at 200-500 bar to remove burrs from precision hydraulic valve bodies, fuel cell bipolar plates, and semiconductor packaging components without abrasive contamination risk, is emerging as the fastest-growing deburring machine technology at 7.1% CAGR, driven by EV powertrain component manufacturing precision requirements and semiconductor fabrication facility adoption. EV battery management system housings, power electronics cooling plates, and hydrogen fuel cell bipolar plate channel deburring represent structurally new application categories that conventional vibratory and tumbling deburring systems cannot serve without contamination risk.

The global high-pressure water jet equipment market is estimated to exceed US$ 2.0 Bn by 2030, with precision deburring applications representing an estimated US$ 300 million addressable sub-segment growing at 7% CAGR.

Sugino Machine Corporation's Aquajet high-pressure deburring systems and PROCECO's industrial water jet cleaning and deburring platforms are commercially pioneering this segment, with EV component manufacturing adoption at Toyota, CATL, and BMW battery system facilities providing reference program traction that is accelerating water jet deburring specification across new EV platform development programs globally through 2033.

Aerospace & Defense MRO Deburring Services and Equipment Expansion

Expanding commercial aircraft MRO activity, driven by record global aircraft fleet utilization rates and aging fleet maintenance requirements across IATA's 25,000+ commercial aircraft in service, is generating growing demand for precision deburring machine investment at licensed MRO facilities performing turbine blade refurbishment, landing gear overhaul, and structural repair operations requiring validated surface finishing to AS9100D and NADCAP standards. The global aerospace MRO market is projected to reach US$ 130 Bn by 2030 (IATA), with deburring and surface finishing equipment representing a structurally essential MRO shop investment category.

Defense sector modernization programs, with NATO member states increasing defense budgets toward 2% of GDP targets, are driving military component manufacturing and overhaul activities, generating demand for deburring machines across armament, vehicle drivetrain, and aircraft engine component refurbishment programs.

Aerospace & defense is the fastest-growing end-user segment at 6.1% CAGR through 2033, with the addressable deburring equipment market in aerospace MRO and defense manufacturing estimated at US$ 250 million by 2030, representing a premium-specification, high-margin opportunity for electrochemical and high-pressure water jet deburring system providers targeting NADCAP-certified facility procurement programs.

Category-wise Analysis

Machine Type Insights

Vibratory deburring machines lead the machine type segment with a 26.8% share in 2026. Vibratory deburring's market leadership reflects its unmatched combination of batch processing versatility, operational simplicity, and broad material compatibility, processing metal castings, stampings, forgings, and plastic components simultaneously in a single mass finishing cycle without requiring individual component fixturing. Its compatibility with all four deburring media categories, ceramic, steel, plastic, and organic, across bowl and through vibratory configurations makes it the most universally applicable deburring technology across automotive, metal fabrication, and general manufacturing end uses.

Barrel tumbling, brush deburring, and thermal deburring serve complementary application niches, but vibratory deburring's versatility and established supply chain position sustain its segment leadership. No dominance shift is expected through 2033.

High-pressure water-jet deburring is the fastest-growing machine type, with a 7.1% CAGR through 2033. EV component precision-finishing requirements, semiconductor packaging deburring without abrasive contamination risk, and aerospace hydraulic-system component precision channel cleaning are driving the adoption of high-pressure water-jet machines across precision manufacturing sectors globally that demand contamination-free, validated deburring processes.

Deburring Media Insights

Ceramic media leads the deburring media segment with a 37.9% share in 2026. Ceramic media's dominance reflects its optimized performance across the broadest range of industrial deburring and surface-finishing applications, delivering precise cutting action, consistent chip geometry, and high durability in vibratory and tumbling mass-finishing processes for metal components in the automotive, aerospace, and metal fabrication sectors.

Alumina and silicon carbide ceramic chip and cone formats provide controlled surface roughness profiles compliant with IATF 16949 and ISO 9001 surface quality documentation requirements across high-volume automotive component finishing programs.

Steel media serves harder workpiece applications, Plastic media addresses softer non-ferrous components, and Organic Compounds serve specialized burnishing applications. Ceramic Media's breadth of applicability ensures sustained leadership.

Steel media is the fastest-growing deburring media, with a 6.3% CAGR through 2033. Expanding adoption of barrel tumbling and vibratory deburring for hardened steel automotive and industrial components that require aggressive burr removal without workpiece marking, combined with steel media's superior durability and lower replacement frequency compared to ceramic alternatives, is driving steel media procurement growth across heavy-duty metal fabrication and commercial vehicle component applications globally.

Operation Mode Insights

Automatic operation mode leads the segment with a 54.8% market share in 2026. Automatic deburring systems command clear segment leadership by aligning with Industry 4.0 manufacturing architecture requirements, enabling continuous production line integration, PLC-controlled process parameter documentation for IATF 16949 quality records, and robotic loading/unloading cell compatibility that eliminates operator-dependent process variability.

Automotive OEM Tier 1 suppliers, aerospace component manufacturers, and medical device producers are systematically specifying automatic deburring machine configurations to achieve consistent, documentable surface quality outcomes at production volumes where manual and semi-automatic processes introduce unacceptable quality variation.

The semi-automatic segment serves mid-volume precision applications, while Manual retains a niche in complex geometry and prototype deburring. Semi-automatic is the fastest-growing operation mode. Growing adoption among mid-size precision engineering and medical device contract manufacturers seeking automation productivity benefits with operator flexibility for complex geometry components, combined with lower capital investment thresholds versus full automation, is sustaining semi-automatic deburring machine adoption growth across Europe and the Asia Pacific precision manufacturing sectors.

Industry Insights

Automotive leads to the Industry segment with a 29.8% share in 2026. Automotive's leadership reflects the industry's unmatched metal component volume and IATF 16949 surface quality standard enforcement intensity, with transmission, engine, brake, and steering components each requiring validated burr-free finishing specifications across OEM and Tier 1 production facilities globally. The EV platform transition is further intensifying deburring requirements, with battery enclosures, aluminum die castings, and power electronics copper bus bars generating new precision-finishing demands.

Aerospace & defense is the fastest-growing industry, with a 6.1% CAGR through 2033. Record Boeing and Airbus delivery backlogs, expanding NADCAP-certified surface treatment requirements for turbine and structural components, and NATO defense manufacturing investment growth are collectively driving the acceleration of aerospace and defense deburring machine procurement across precision MRO and component manufacturing facilities globally.

Regional Market Insights

North America Deburring Machine Market Trends

North America holds the leading 31.6% of the global deburring machine market in 2025, anchored by the U.S.'s deep automotive OEM and Tier 1 supplier deburring machine installed base, NADCAP-certified aerospace component finishing demand, and progressive robotic deburring cell integration investment aligned with IFR-documented automation adoption trends across Michigan, Ohio, Indiana, and California manufacturing corridors. FDA 21 CFR Part 820 and AS9100D validation requirements for medical device and aerospace surface finishing are sustaining premium automatic deburring machine specification across regulated-industry U.S. manufacturers.

U.S. & Canada: Automotive Automation and Aerospace Precision Deburring Leadership

The U.S. market is estimated at US$ 283.1 Mn in 2026, driven by Ford, GM, and Stellantis Tier 1 supplier automated deburring cell investment, Pratt & Whitney and GE Aerospace turbine component electrochemical deburring procurement, and medical device manufacturer vibratory and high-pressure water jet system adoption. Canada contributes Bombardier aerospace component precision finishing and Ontario automotive parts manufacturer deburring capacity investment through 2033.

Europe Deburring Machine Market Trends

Europe is growing at a prominent 5.4% CAGR, driven by EU MDR 2017/745 medical device surface finishing compliance investment, Germany Machine Tool Builders' Association-documented automated deburring system volume growth, and BENSELER and Rösler's European manufacturing innovation leadership, sustaining premium automated deburring system procurement across automotive, aerospace, and medical device end users.

Germany, U.K., France & Spain: Precision Engineering Standards and Medical Device Compliance

Germany's market is estimated at US$ 98 Mn in 2026, anchored by BMW, Volkswagen, and Mercedes-Benz Tier 1 supplier automated deburring investment, EMAG GmbH's Salach-headquartered electrochemical deburring system global product leadership, and BENSELER's precision industrial deburring service and machine programs. The U.K. contributes to the procurement of Rolls-Royce turbine blade precision deburring.

France sustains Safran and Airbus Tier 1 aerospace component water-jet deburring investment, while Spain contributes to automotive sector vibratory and brush deburring capacity expansion through 2033.

Asia Pacific Deburring Machine Market Share

Asia Pacific is the leading and fastest-growing region at 6.2% CAGR through 2033, driven by China's expanding automotive and electronics component precision manufacturing base, India's rapidly growing automotive component supply chain deburring investment, and Japan's precision engineering standards sustaining high-specification electrochemical and high-pressure water jet machine adoption at automotive and electronics Tier 1 manufacturers.

China, India & Japan: Electronics Manufacturing and Automotive Supply Chain Expansion

China's market is estimated at US$ 181.2 Mn in 2026, driven by BYD, SAIC, and Foxconn's automotive and electronics component deburring investments, as well and domestic precision machine tool manufacturer growth. India's market at US$ 40 Mn is growing through Tata Motors, Mahindra, and Bharat Forge's investment in automotive component deburring capacity. Japan sustains the adoption of Toyota, Honda, and Kyocera's precision vibratory and electrochemical deburring equipment through 2033.

Competitive Landscape

The global deburring machine Market is moderately fragmented, with top three players, ATI Industrial Automation, Sugino Corporation, and EMAG Systems GmbH, collectively controlling approximately 20-25% of global production capacity, differentiating through robotic integration expertise, electrochemical precision deburring technology leadership, and validated process documentation platforms targeting regulated aerospace and medical device end users. Aftermarket process media and application engineering service contracts are emerging as recurring revenue differentiators.

Robotic deburring cell integration platform development, high-pressure water jet technology expansion for EV and semiconductor applications, geographic investment in Asia Pacific precision manufacturing markets, and aerospace NADCAP certification program development define the dominant competitive strategic themes across the global deburring machine market through 2033.

Strategic Developments

- In October 2024, BENSELER Group expanded its industrial deburring service and machine manufacturing footprint in Bratislava, Slovakia, establishing a Central European production and application engineering center targeting automotive and aerospace Tier 1 component manufacturers across Poland, Czech Republic, Hungary, and Romania.

- In June 2024, Sugino Machine Ltd. entered a technology partnership with Fanuc Corporation to co-develop a fully integrated robotic high-pressure water jet deburring cell, combining Sugino's Aquajet deburring technology with Fanuc's M-20 robotic arm platform for EV battery housing and power electronics component precision finishing applications.

Companies Covered in Deburring Machine Market

- ATI Industrial Automation

- BENSELER Group

- Sugino Machine Ltd.

- EMAG GmbH & Co. KG

- Rösler Oberflächentechnik GmbH

- Kadia Produktion GmbH

- Dürr Ecoclean GmbH

- PROCECO Ltd.

- Georg Kesel GmbH & Co. KG

- Loeser GmbH

- Abtex Corporation

- AXIOME

- RSA Cutting Technologies Ltd.

- Maschinenbau Silberhorn GmbH

- Bertsche Engineering Corporation

Frequently Asked Questions

The deburring machine market is valued at US$ 1,147.1 Mn in 2026, projected to reach US$ 1,679.8 Mn by 2033.

Precision component quality mandates under IATF 16949, AS9100D, and ISO 13485 standards compelling burr-free surface finishing investment and Industry 4.0 automated deburring cell adoption are the primary growth drivers.

The deburring machine market is projected to grow at a CAGR of 5.6% from 2026 to 2033.

High-pressure water jet deburring adoption for EV and semiconductor precision component finishing and aerospace MRO and defense manufacturing deburring equipment expansion represent the most actionable near-term growth opportunities.

ATI Industrial Automation, BENSELER Group, Sugino Machine Ltd., EMAG GmbH, Rösler Oberflächentechnik, Kadia Produktion, Dürr Ecoclean, PROCECO, AXIOME, Abtex Corporation, and RSA Cutting Technologies are the leading global participants.