- Metalworking & Fabrication

- Material Removal Tools Market

Material Removal Tools Market Size, Share, and Growth Forecast, 2026 - 2033

Material Removal Tools Market by Tool Types (Grinders, Circular Cutters, Others), Material Types (High-Speed Steel, Diamond, Others), End-user Industry, Power Sources, and Regional Analysis for 2026 - 2033

Material Removal Tools Market Size and Trends Analysis

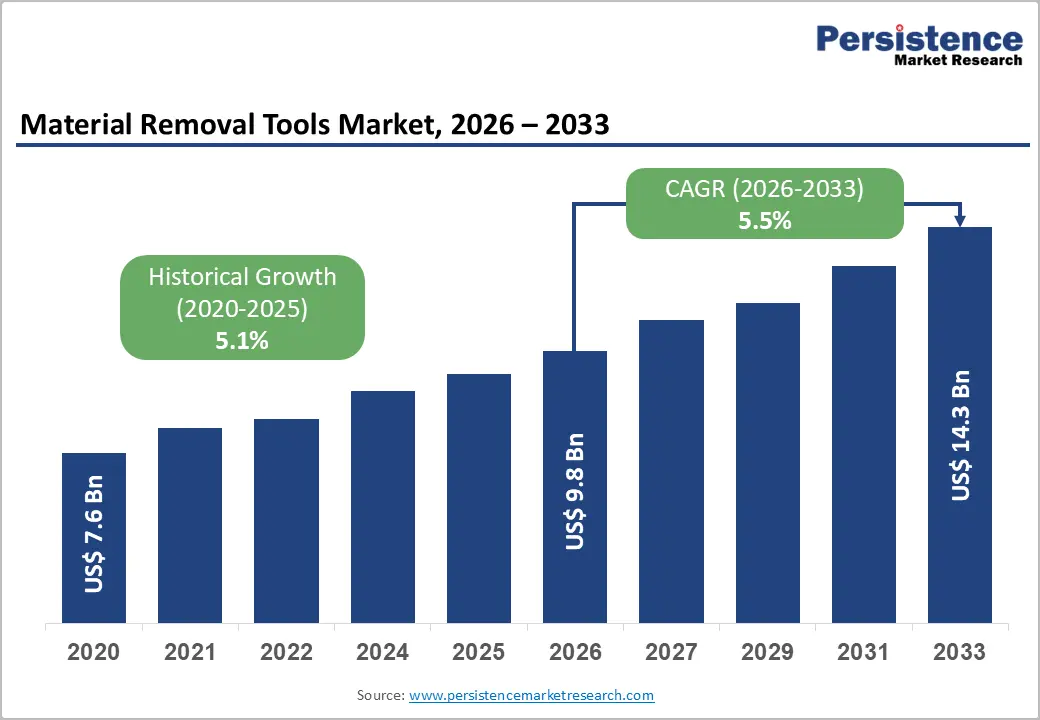

The global material removal tools market size is likely to be valued at US$ 9.8 billion in 2026 and is expected to reach US$14.3 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033, driven by sustained manufacturing expansion, aerospace production pipelines, and the increasing adoption of precision-led and digitally integrated machining systems.

The market is transitioning from volume-driven consumption to efficiency-driven procurement, in which tool performance, lifecycle cost, and machining precision determine purchasing decisions. Leading manufacturers such as Sandvik and Kennametal are integrating advanced grades, digital machining ecosystems, and traceability solutions, improving productivity while reducing scrap and downtime.

Key Industry Highlights:

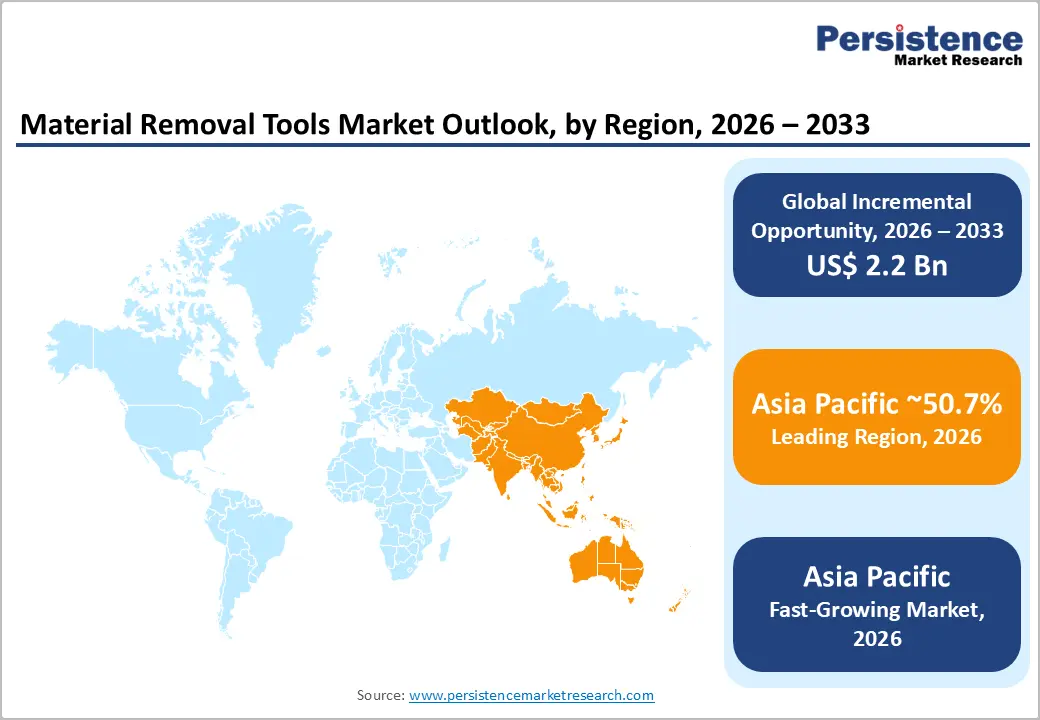

- Leading Region: Asia Pacific is projected to account for approximately 50.7% of the market share, driven by strong manufacturing hubs in China, India, and Japan.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by expanding industrialization, infrastructure investments, and rising demand from the automotive and aerospace sectors.

- Investment Plans: Leading companies such as Sandvik Coromant and Kennametal are actively investing in digital machining technologies, AI-driven CAM systems, and localized production facilities, particularly across the Asia Pacific, to enhance productivity and strengthen regional presence.

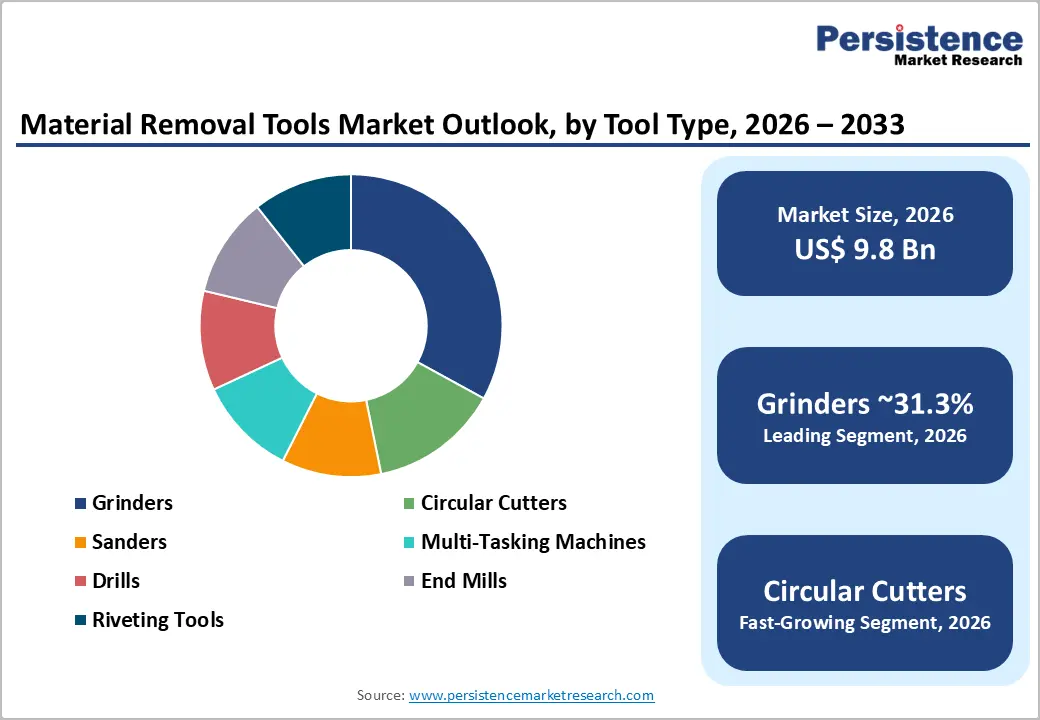

- Dominant Product Types: Grinders dominate the market with an anticipated 31.3% share, owing to their critical role in precision finishing and dimensional accuracy across key industries.

- Leading End-user Industry: The automotive segment leads with an anticipated 30.5% share, supported by high-volume production and continuous demand for machining in both conventional and electric vehicle manufacturing.

DRO Analysis

Driver - Rising Manufacturing Output and High-Tech Production Mix

Global manufacturing activity is steadily improving, particularly in high-value segments. According to the United Nations Industrial Development Organization, output expanded 0.7% in Q3 2025, following 1.0% growth in Q2, while high-technology industries grew 1.4%. Key economies, including China, India, and Japan, reported positive growth, reinforcing demand for material removal tools across continuous production environments.

Material removal tools are inherently linked to machining intensity, meaning increased production volumes directly translate into higher tool consumption. High-frequency operations such as drilling, milling, and finishing require consistent tool replacement, particularly in automated production lines.

Demand is shifting toward high-performance tooling solutions, where durability, cutting efficiency, and process stability justify premium pricing. Companies like Sandvik Coromant are benefiting from this transition by offering integrated tooling and digital machining solutions.

Aerospace Expansion and Electrification Driving Precision Machining

The aerospace and EV sectors are significantly increasing demand for advanced machining tools. Airbus projects 3.6% annual growth in air traffic, supported by a 1.5 billion increase in the global middle class, driving long-term aircraft demand. Simultaneously, the International Energy Agency estimates EV battery demand will surpass 3 TWh by 2030, up from 1 TWh in 2024.

These sectors rely heavily on lightweight and difficult-to-machine materials, including titanium, aluminum alloys, and composites. Such materials require advanced tooling solutions such as diamond-coated tools, CBN inserts, and precision cutters. This trend structurally supports the adoption of premium-grade tooling, increasing the value share of specialized products over standard tools while strengthening supplier differentiation.

Restraint - Cyclical Industrial Demand and Pricing Pressure

The market remains sensitive to macroeconomic cycles, particularly in steel-intensive industries. The World Steel Association forecasts global steel demand at 1,749 million tonnes in 2025, indicating stagnation compared to 2024. In parallel, the United Nations Industrial Development Organization reported minimal growth in Europe (0.09%), with declines in Germany and the U.K. Lower industrial activity reduces machine utilization rates, directly impacting tooling consumption and replacement cycles. Slower capital expenditure cycles increase pricing pressure and competition, particularly in commoditized tool categories, while delaying large-scale tooling upgrades.

Opportunity - Digital Machining and AI-Driven Tool Optimization

The integration of software and tooling is emerging as a key growth area. In May 2025, Kennametal invested in Toolpath Labs to enhance AI-driven CAM capabilities. Meanwhile, Seco Tools has implemented Data Matrix traceability across 90% of its tools, enabling lifecycle tracking and sustainability metrics. These technologies allow manufacturers to optimize machining parameters, reduce tool wear, and improve overall efficiency. Digital tooling ecosystems create recurring revenue streams, enhance customer retention, and provide measurable productivity gains.

Asia Pacific Manufacturing Expansion and Localization

Asia Pacific remains the dominant and fastest-growing region, accounting for 50.7% of global demand. Countries such as China, India, and Japan continue to expand manufacturing capacity, supported by infrastructure investment and industrial policy. The International Energy Agency highlights that emerging markets will increase their share of EV battery demand to 10% by 2030, further boosting machining demand. Tool manufacturers are increasingly investing in localized production, distribution networks, and application engineering centers to capture regional growth.

Category-wise Analysis

Tool Types Insights

Grinders are expected to account for an anticipated 31.3% of the market share in 2026, driven by their essential role in surface finishing, dimensional accuracy, and precision engineering. These tools are critical in applications where micron-level tolerances and repeatability are required, particularly in automotive, aerospace, and heavy machinery manufacturing. Their ability to deliver superior surface integrity and consistent output makes them indispensable in high-precision production lines. Companies such as Sandvik Coromant integrate grinding solutions within broader machining ecosystems, combining tooling with digital optimization platforms to improve productivity and reduce rework.

Circular cutters are projected to be the fastest-growing segment, supported by increasing demand for precision machining and high-efficiency material removal. These tools offer enhanced edge stability, improved cutting speeds, and reduced cycle times, making them highly suitable for aerospace structures and EV components. Their modular design and adaptability to automated machining environments further enhance their adoption. Innovations from Walter AG demonstrate a clear shift toward high-performance, modular cutting systems, aligning with the industry's focus on productivity and process reliability.

Material Types Insights

High-speed steel (HSS) is expected to hold an anticipated 34.8% of the market share in 2026, supported by its cost-efficiency, versatility, and ease of regrinding. HSS tools remain widely used in general engineering, maintenance operations, and mid-precision machining, where cost-performance balance is critical. Their adaptability across multiple materials and machining conditions ensures continued relevance despite the rise of advanced materials. Companies such as Dormer Pramet maintain extensive HSS product portfolios, supporting broad industrial applications and reinforcing steady demand.

Diamond tools are projected to be the fastest-growing segment due to their superior performance in abrasive, high-precision, and high-speed machining applications. These tools are increasingly used in aerospace, electronics, and advanced manufacturing environments where surface finish, tool life, and dimensional accuracy are critical. The shift toward composite materials and lightweight alloys further accelerates adoption. ISCAR has expanded its advanced-grade tooling portfolio to address this demand, reflecting a broader industry trend toward premium, application-specific solutions.

End-user Industry Insights

The automotive industry is projected to hold an anticipated 30.5% market share in 2026, maintaining its position as the largest end-user due to high-volume production and repetitive machining processes. Components such as engines, transmissions, chassis systems, and EV powertrain parts require extensive material removal, resulting in continuous tool wear. The transition toward electric vehicles is also increasing demand for precision machining of lightweight materials and battery components. MAPAL identifies automotive and e-mobility as core growth drivers, reflecting the sector’s ongoing importance in shaping tooling demand.

The aerospace segment is expected to be the fastest-growing segment, driven by rising aircraft production and increasing demand for lightweight, high-strength components. Materials such as titanium and advanced composites require specialized tooling that can maintain precision under challenging conditions. Long-term projections from Airbus reinforce sustained production growth, while tooling providers like KYOCERA SGS Precision Tools are expanding aerospace-focused product portfolios. This segment is characterized by high tooling intensity per component, supporting above-average growth rates.

Regional Insights

North America Material Removal Tools Market Trends

North America represents a stable, innovation-driven market led by the U.S. Manufacturing output grew 0.31% QoQ in Q3 2025, according to the United Nations Industrial Development Organization. The region benefits from strong aerospace, defense, and advanced manufacturing sectors, along with increasing adoption of digital machining technologies.

U.S. Material Removal Tools Market Trends

The U.S. remains the dominant contributor, supported by aerospace demand and reshoring initiatives. Kennametal’s May 2025 investment in Toolpath Labs (AI-driven CAM software) highlights the region’s shift toward digital machining ecosystems, where tooling is integrated with software for process optimization. This directly improves tool utilization rates and reduces cycle times, increasing demand for high-performance tooling rather than commodity tools.

In parallel, KYOCERA SGS Precision Tools has expanded its solid carbide tooling lines for aerospace and medical applications, reflecting growing demand for precision machining in high-spec industries. This aligns with Airbus and the broader OEM supply chain expansion in North America.

North America is transitioning toward value-driven tooling consumption, where software integration, automation compatibility, and aerospace-grade precision tools are driving growth rather than volume alone.

Europe Material Removal Tools Market Trends

Europe remains a global hub for precision tooling innovation, despite slower industrial growth. Manufacturing output stagnated at 0.09% QoQ, with Germany and the U.K. facing contractions, according to the United Nations Industrial Development Organization. However, the region continues to lead in high-performance tooling, sustainability integration, and advanced machining technologies.

Germany Material Removal Tools Market Trends

Germany anchors Europe’s tooling ecosystem, supported by companies such as Walter AG and MAPAL. In August 2025, Walter launched an upgraded ConeFit milling cutter platform, emphasizing modularity and high-precision machining. This development reflects a broader industry trend toward flexible tooling systems that reduce setup time and improve machining efficiency, critical in high-mix, low-volume production environments.

Sweden & Luxembourg Material Removal Tools Market Trends

The Nordic and Western European players are driving sustainability and digital innovation. Sandvik Coromant continues to expand its CoroPlus digital machining platform, integrating tool data, process optimization, and lifecycle management. Meanwhile, CERATIZIT achieved Science Based Targets initiative (SBTi) validation in 2025, reinforcing its commitment to carbon reduction.

These developments align with stricter EU regulations on traceability, emissions, and resource efficiency, pushing tooling manufacturers to embed sustainability into product design and lifecycle management.

U.K. Material Removal Tools Market Trends

Although manufacturing growth is weaker, companies such as Seco Tools (with a strong European presence) are advancing tool traceability systems, including Data Matrix codes across a majority of their portfolio. This enables real-time tracking, lifecycle monitoring, and compliance reporting, which are increasingly required by European OEMs.

Europe’s market is shifting toward premium, sustainable, and digitally traceable tooling solutions, where compliance and engineering excellence outweigh volume growth.

Asia Pacific Material Removal Tools Market Trends

Asia Pacific is expected to dominate the market with a 50.7% share in 2026, and remains the fastest-growing region, with an estimated CAGR of 6.3%.

China Material Removal Tools Market Trends

China is expected to lead with a 19.7% regional share, supported by strong manufacturing output, infrastructure investments, and expanding industrial ecosystems. China remains the largest contributor due to its scale in automotive, electronics, and heavy manufacturing. Domestic demand for high-precision tooling is rising as manufacturers upgrade toward advanced and automated production systems. Global players, such as ISCAR, are expanding their presence in China through localized production and distribution networks, enabling faster delivery and cost competitiveness.

India Material Removal Tools Market Trends

India is emerging as a high-growth market due to infrastructure expansion and “Make in India” manufacturing initiatives. Sandvik Coromant has strengthened its footprint through its Pune manufacturing facility and application center, focusing on training, digital machining, and localized production. Similarly, Mitsubishi Materials continues to expand its tooling distribution and service capabilities in India.

These investments are directly supporting localized tooling ecosystems, reducing dependency on imports and improving responsiveness to industrial demand.

Japan Material Removal Tools Market Trends

Japan remains a leader in high-precision tooling and advanced materials. Companies such as Mitsubishi Materials and OSG Corporation are driving innovation in carbide tooling and precision cutting technologies, particularly for automotive and electronics applications.

Asia Pacific is evolving into a high-volume, high-growth, and increasingly high-precision market, where localization, cost efficiency, and manufacturing scale combine with rising demand for advanced tooling solutions.

Asia Pacific will remain the primary revenue driver and investment destination, while North America and Europe will lead in innovation, digital integration, and premium tooling development. The global competitive landscape is therefore becoming regionally specialized, with production scale concentrated in Asia and technological leadership anchored in Western markets.

Competitive Landscape

The global material removal tools market is moderately fragmented, with a mix of global leaders and regional specialists. Major players, such as Sandvik, Kennametal, and Mitsubishi Materials, dominate high-value segments, while smaller firms compete in cost-sensitive markets.

Key players are focusing on innovation, digital ecosystems, and regional expansion. Competitive advantage is increasingly defined by application expertise, software integration, and lifecycle services, rather than standalone tooling products.

Key Industry Developments:

- In March 2025, Sandvik Coromant announced the launch of its CoroDrill® Dura 462 drilling family, featuring over 2,000 tool variants designed for multi-material applications, aimed at improving productivity, extending tool life, and reducing tooling inventory across manufacturing operations.

- In March 2025, Sandvik Coromant introduced its CoroPak 25.1 product release, including solutions such as CoroMill® MS40, CoroCut® 2, and CoroMill® Plura Barrel, focusing on enhancing machining efficiency, improving chip control, and reducing cycle times for industrial manufacturers.

Companies Covered in Material Removal Tools Market

- Sandvik Coromant

- Kennametal

- Mitsubishi Materials

- ISCAR

- Walter AG

- Seco Tools

- CERATIZIT

- MAPAL

- OSG Corporation

- Dormer Pramet

- KYOCERA SGS Precision Tools

- NACHI-FUJIKOSHI Corp.

- Sumitomo Electric Industries

- Tungaloy Corporation

- Guhring KG

- Yamawa Co., Ltd.

Frequently Asked Questions

The global material removal tools market is valued at US$9.8 billion in 2026.

The material removal tools market is projected to reach US$14.3 billion by 2033.

Key trends include increasing adoption of CNC machining and automation, rising demand for precision engineering in aerospace and automotive sectors, growing use of advanced cutting materials such as carbide and ceramics, and integration of digital monitoring for tool performance optimization.

The grinders segment leads the market, accounting for an anticipated 31.3% share, due to its critical role in surface finishing and precision engineering applications.

The material removal tools market is expected to grow at a CAGR of 5.5% between 2026 and 2033.

Major companies include Sandvik AB, Kennametal Inc., Iscar Ltd., Mitsubishi Materials Corporation, and Seco Tools AB.