- Metalworking & Fabrication

- Laser Welding Machine Market

Laser Welding Machine Market Size, Share, and Growth Forecast, 2026 - 2033

Laser Welding Machine Market by Technology (Fiber Laser, CO2 Laser, Others), Product Form (Automated/Robotic Laser Welding Systems, Stationary Bench/Fixed Systems, Others), End‑use Industry, Power Scale, and Regional Analysis for 2026 - 2033

Laser Welding Machine Market Size and Trends Analysis

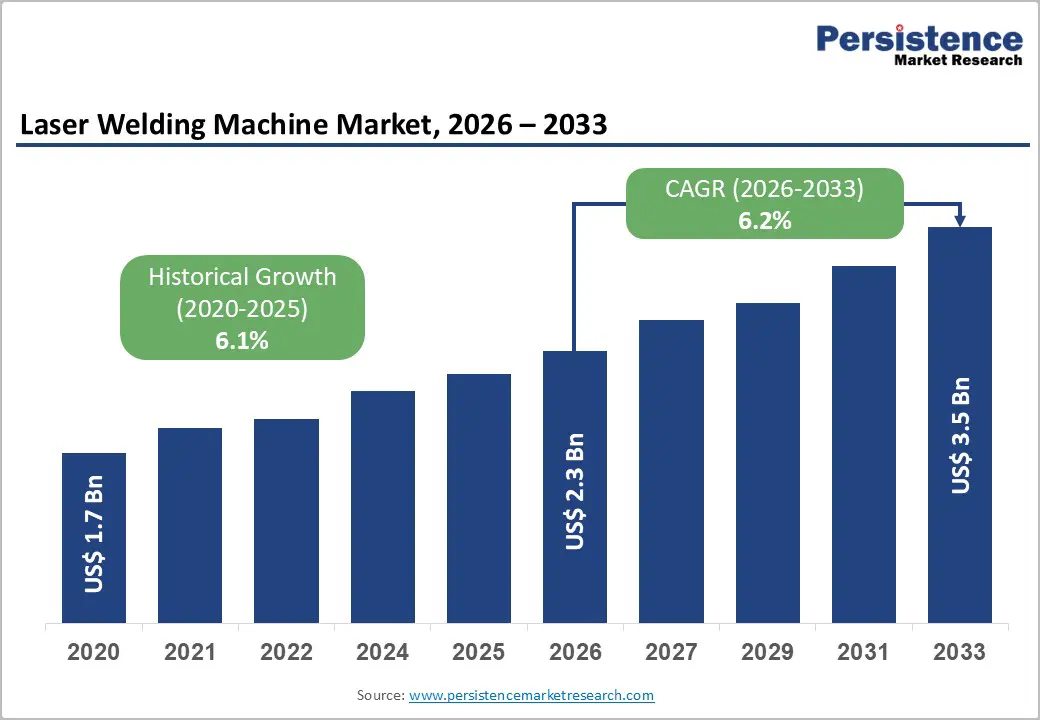

The global laser welding machine market size is likely to be valued at US$2.3 billion in 2026 and is expected to reach US$3.5 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033, driven by rising investments in EV battery manufacturing, semiconductor packaging, electronics miniaturization, and smart factory deployment.

Manufacturers are increasingly adopting laser welding systems because they offer high precision, low thermal distortion, repeatable weld quality, and compatibility with robotic automation. Market expansion is also supported by industrial modernization initiatives across the Asia Pacific, North America, and Europe, particularly in automotive, aerospace, and medical device manufacturing.

Key Industry Highlights:

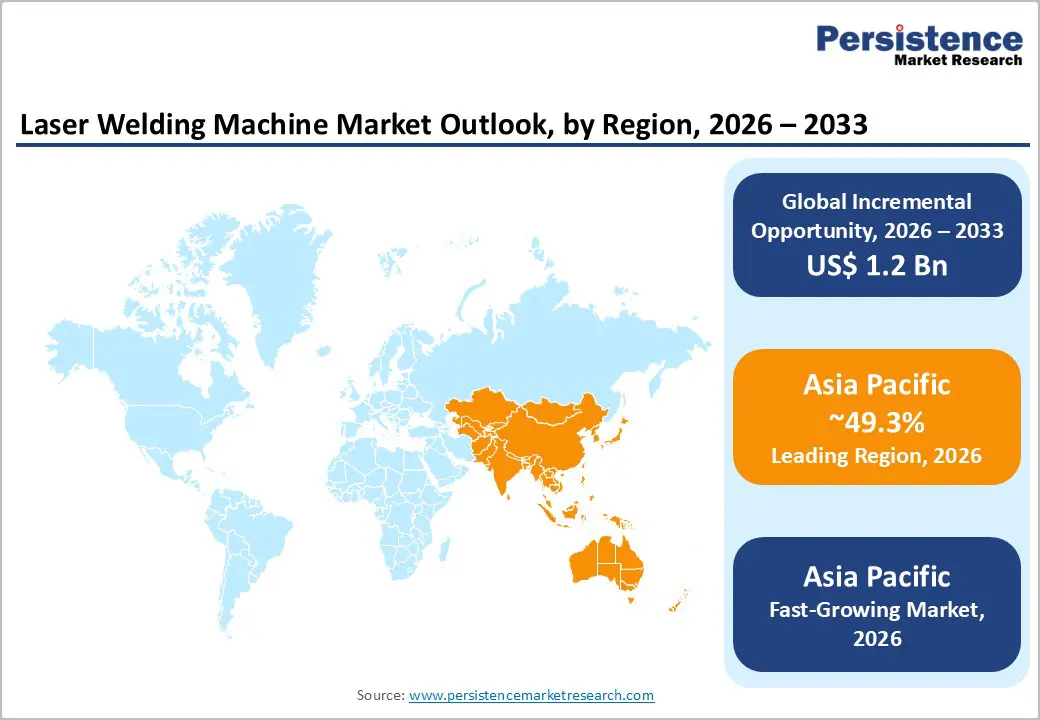

- Leading Region: Asia Pacific is projected to lead with an anticipated market share of over 49.3% in 2026, supported by strong automotive, EV battery, electronics, and semiconductor manufacturing capacity across China, Japan, South Korea, and India.

- Fastest-growing Region: Asia Pacific is also anticipated to remain the fastest-growing regional market, driven by industrial automation expansion, battery gigafactory investments, and electronics localization initiatives.

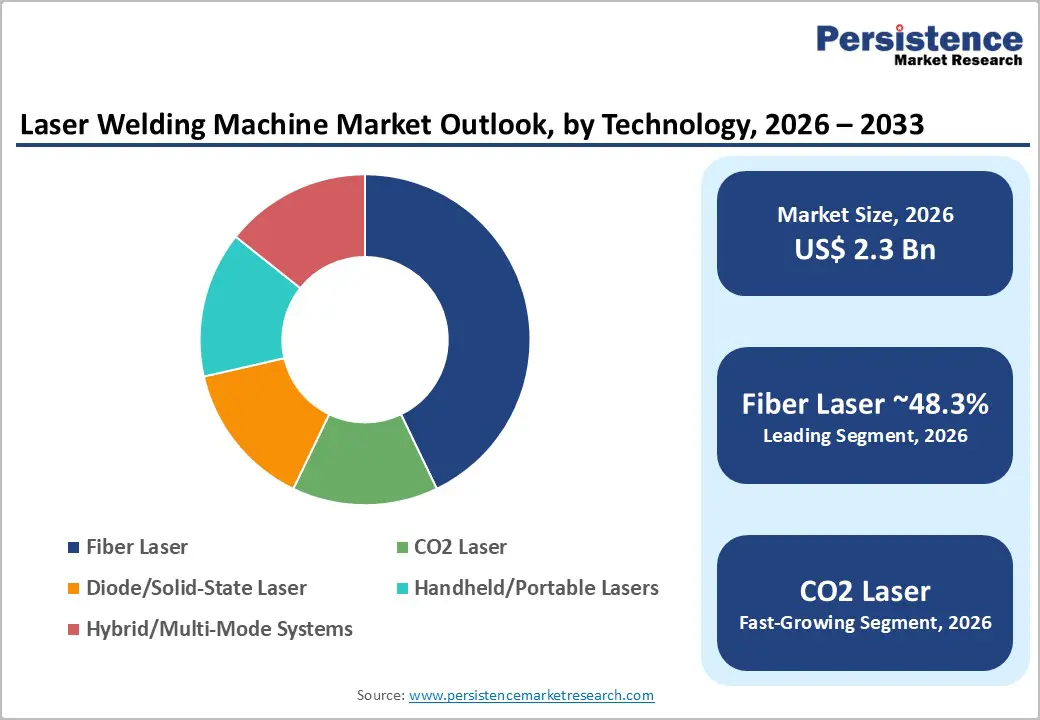

- Dominant Technology: Fiber laser technology is anticipated to account for approximately 48.3% of the market share due to its high precision, energy efficiency, low maintenance requirements, and strong compatibility with robotic welding systems.

- Leading Product Form: Automated and robotic laser welding systems are the leading product form, with an anticipated market share of nearly 41.5%, supported by growing adoption across the automotive, electronics, and metal fabrication industries.

DRO Analysis

Drivers - EV Battery Manufacturing and High-Precision Joining Are Expanding Laser Welding Adoption

Electric vehicle manufacturing has become one of the strongest growth drivers for the laser welding machine market. Battery modules, busbars, thin foils, tabs, and cooling systems require highly precise welding with minimal heat-affected zones and low defect rates. Global EV production growth has therefore created sustained demand for advanced welding systems capable of maintaining consistency at high production volumes.

Large-scale battery manufacturing facilities across China, Europe, and North America are increasing investments in automated welding lines to improve throughput and reduce scrap generation. Public funding programs supporting battery manufacturing expansion in Europe and Asia are also accelerating investments in industrial equipment. Laser welding systems are increasingly preferred because they provide cleaner weld seams, higher process stability, and improved repeatability compared to conventional welding methods. Commercial EVs, energy storage systems, and mobility electronics are driving increased demand for compact laser-welding solutions integrated with robotics and machine vision systems.

Automation, Robotics, and Semiconductor Manufacturing Are Increasing Factory-Level Demand

The rapid adoption of industrial automation is strengthening long-term demand for laser welding machines across manufacturing sectors. Industrial robots are increasingly deployed in automotive, electronics, semiconductor, and precision engineering facilities where manufacturers require consistent weld quality, low downtime, and traceable production processes. Electronics and semiconductor manufacturing represent particularly strong growth areas because advanced packaging, AI hardware infrastructure, and miniaturized components require high-precision joining technologies. Laser welding integrates effectively with robotic systems, closed-loop quality control, and machine vision technologies, making it suitable for automated production environments.

Manufacturers are also prioritizing labor efficiency and process standardization amid rising wage pressures and tightening quality requirements. Automated laser welding systems support these objectives by reducing human error, minimizing material waste, and improving production repeatability.

Restraint - High Capital Costs and Integration Complexity Limit SME Adoption

Despite strong industrial demand, the market continues to face adoption challenges related to high initial investment requirements. Laser welding systems require specialized optics, shielding systems, motion controls, cooling infrastructure, safety enclosures, and process engineering support, significantly increasing implementation costs. Small and mid-sized manufacturers often struggle to justify capital expenditures, particularly when production volumes are inconsistent or product changeovers are frequent. Integration challenges also remain substantial because welding parameters must be validated for each material type and application. Companies must invest in workforce training, process qualification, and quality testing before full-scale deployment.

Maintenance costs and technical expertise requirements further increase operational barriers. In facilities lacking a strong automation infrastructure, the payback period for laser welding systems can extend considerably. As a result, adoption remains concentrated among large OEMs, high-volume manufacturers, and technologically advanced production facilities with sufficient automation maturity.

Opportunities - EV Batteries, Power Electronics, and Lightweight Structures Create Demand for Adaptive Welding Systems

One of the strongest growth opportunities lies in battery manufacturing, lightweight mobility platforms, and power electronics production. These applications require precise thermal management, narrow weld seams, and minimal structural distortion, creating favorable conditions for advanced laser welding technologies. Manufacturers are increasingly investing in adaptive laser systems capable of foil-to-tab welding, thin busbar welding, and precision assembly. Compact fiber lasers with software-controlled operation are gaining traction because they support flexible production lines and reduce downtime during manufacturing transitions.

The opportunity extends into medical devices, aerospace electronics, and consumer electronics, where miniaturization continues to increase the need for highly controlled welding processes. As component complexity increases, manufacturers are expected to prioritize laser systems with integrated monitoring, real-time quality feedback, and programmable automation.

Portable and Modular Welding Solutions Can Expand Adoption across Emerging Manufacturing Hubs

The market is also witnessing growing demand for modular automation systems and portable laser welding machines. Manufacturers are increasingly developing integrated cells, handheld systems, and cobot-compatible welding solutions to reduce implementation complexity and improve operational flexibility.

Portable systems are particularly attractive for smaller factories, maintenance operations, repair applications, and low-volume production environments where large robotic installations may not be economically viable. These systems reduce floor space requirements while providing higher weld quality than conventional arc-welding methods. Emerging manufacturing regions such as India, Southeast Asia, and Mexico, as well as secondary industrial hubs in North America and Europe, are expected to benefit significantly from this trend. Industrial operators in these regions are seeking cost-efficient automation solutions that improve productivity without requiring large-scale factory redesigns.

Category-wise Analysis

Technology Insights

Fiber laser technology is anticipated to account for approximately 48.3% of the market share in 2026, making it the dominant technology segment. Fiber lasers are widely adopted because they offer high beam quality, superior electrical efficiency, lower maintenance requirements, and strong compatibility with robotic automation systems. These systems are extensively used in automotive manufacturing, EV battery assembly, consumer electronics, and precision engineering applications where manufacturers require consistent weld quality and rapid processing speeds.

For example, EV battery manufacturers increasingly use fiber lasers for busbar and battery tab welding due to their low thermal distortion and precision control. Companies such as TRUMPF, IPG Photonics, and Coherent continue to expand their fiber-laser portfolios for semiconductor packaging, battery modules, and advanced electronics assembly. Fiber lasers also offer greater flexibility for thin materials and high-volume production environments than conventional welding technologies.

CO2 laser systems and hybrid welding technologies are anticipated to grow the fastest over the forecast period due to rising demand from the heavy industrial manufacturing, structural fabrication, and shipbuilding sectors. These technologies are gaining traction because they support deep-penetration welding, long-seam applications, and processing of thick materials.

For instance, hybrid laser-arc welding is increasingly used in shipbuilding and rail manufacturing to improve welding speed and reduce structural distortion. Hybrid systems combine conventional arc welding with laser technology to improve productivity, weld strength, and process efficiency in heavy-duty industrial applications. Large fabricated structures such as ship hulls, heavy machinery, and industrial steel frameworks increasingly rely on hybrid welding methods to enhance throughput and reduce rework.

Product Form Insights

Automated and robotic laser welding systems are anticipated to account for approximately 41.5% of the global market share in 2026, driven by their alignment with industrial automation trends. These systems provide consistent weld quality, reduced defect rates, and high production throughput, making them highly suitable for automotive, electronics, and metalworking industries.

Automotive OEMs increasingly deploy robotic laser-welding cells for EV body structures and battery-pack assembly to improve process consistency and reduce material waste. Manufacturers prefer robotic laser welding systems because they support closed-loop quality monitoring, process traceability, and reduced labor dependency. Integration with machine vision systems, AI-driven quality inspection, and industrial software platforms further strengthens the segment’s position in smart manufacturing environments.

Handheld and portable laser welding systems are anticipated to register the fastest growth during the forecast period due to rising demand for flexible and cost-efficient automation solutions. These systems are increasingly used in maintenance operations, low-volume manufacturing, repair services, jewelry fabrication, and smaller industrial workshops where large robotic systems may not be practical.

Portable laser welders offer advantages such as reduced setup complexity, greater mobility, and lower investment costs than fully automated robotic cells. For example, small fabrication shops and HVAC equipment manufacturers are increasingly adopting handheld laser welders for stainless steel and aluminum joining applications.

Regional Insights

North America Laser Welding Machine Market Trends

North America remains a major technology-driven market for laser welding machines, supported by strong demand from aerospace, defense, medical devices, automotive electrification, and semiconductor manufacturing industries.

U.S. Laser Welding Machine Market Trends

The U.S. dominates the North American market due to its advanced manufacturing ecosystem, strong adoption of industrial automation, and rising investments in EV battery production and semiconductor fabrication facilities. Automotive manufacturers increasingly deploy robotic laser welding systems for EV body structures, battery packs, and lightweight aluminum components. The aerospace and defense industries also represent major demand centers because laser welding supports high-strength and precision-critical applications.

The U.S. market benefits from strong R&D capabilities and collaboration between automation providers, industrial equipment manufacturers, and semiconductor companies. Government support for domestic semiconductor manufacturing and advanced industrial modernization is expected to sustain long-term demand for automated laser welding systems integrated with robotics and digital monitoring technologies.

Canada Laser Welding Machine Market Trends

Canada is witnessing steady growth in the adoption of laser welding across automotive components, aerospace manufacturing, and industrial machinery production. The country benefits from its integration with North American automotive supply chains and increasing investments in EV battery materials and clean technology manufacturing.

Manufacturers are gradually upgrading production facilities with automated welding technologies to improve quality consistency and operational efficiency. Aerospace manufacturing clusters in Quebec and Ontario continue to support demand for high-precision welding systems used in lightweight structural components and aircraft assemblies.

Europe Laser Welding Machine Market Trends

Europe represents a technologically advanced market characterized by strong automation adoption, industrial quality standards, and supportive manufacturing policies. The region continues to benefit from advanced engineering capabilities, strong automotive production infrastructure, and industrial modernization programs.

Germany Laser Welding Machine Market Trends

Germany remains the largest laser welding machine market in Europe due to its leadership in automotive manufacturing, industrial engineering, and factory automation. German automotive OEMs and industrial machinery manufacturers extensively utilize robotic laser welding systems to improve productivity, precision, and manufacturing consistency.

The country also benefits from high robotics density and strong adoption of Industry 4.0 technologies. Investments in EV battery manufacturing and semiconductor production are expected to further strengthen demand for advanced welding systems across automotive and electronics applications.

U.K. Laser Welding Machine Market Trends

The U.K. is a significant market for laser welding systems across the aerospace, defense, medical devices, and precision engineering industries. Aerospace manufacturing facilities increasingly use laser welding technologies for lightweight structures and high-performance components that require stringent quality standards.

Medical device manufacturing is also contributing to market growth because laser welding supports contamination-free and highly precise joining applications. Industrial automation upgrades across manufacturing facilities are expected to create additional opportunities for advanced welding technologies.

Asia Pacific Laser Welding Machine Market Trends

Asia Pacific is expected to lead the global laser welding machine market, accounting for more than 49.3% of the market share during the forecast period. The region is also the fastest-growing market globally, driven by its strong manufacturing base across automotive, electronics, semiconductors, and industrial equipment sectors.

China Laser Welding Machine Market Trends

China dominates the Asia Pacific market due to its massive automotive production capacity, extensive EV battery manufacturing ecosystem, and large-scale electronics assembly operations. The country is also the world’s largest industrial robotics market, supporting widespread adoption of automated laser welding systems.

Chinese manufacturers are increasingly investing in smart factory infrastructure, battery gigafactories, and semiconductor fabrication facilities, driving strong demand for high-precision welding technologies. Domestic equipment manufacturers are also expanding capabilities in compact fiber lasers and automated welding platforms.

Japan Laser Welding Machine Market Trends

Japan remains a highly influential market because of its expertise in precision engineering, industrial robotics, semiconductor manufacturing, and automotive production. Japanese manufacturers prioritize highly accurate, low-defect welding technologies for electronics, sensors, medical devices, and advanced automotive components.

The country’s strong focus on manufacturing quality and automation efficiency continues to support demand for compact, high-performance laser welding systems integrated with robotics and machine vision technologies.

Competitive Landscape

The global laser welding machine market is moderately fragmented, with a combination of global industrial technology companies and regional equipment manufacturers competing across application segments. Leading players collectively account for approximately 25%–30% of the total market share, while the top five companies hold nearly 30% combined.

Leading manufacturers are prioritizing innovation, automation integration, localized manufacturing expansion, and software-enabled welding systems. Companies are increasingly shifting from standalone machine sales toward application-focused production ecosystems combining lasers, robotics, machine vision, monitoring software, and predictive maintenance services.

Key Industry Developments:

- In September 2025, TRUMPF introduced BrightLine Scan technology for its TruLaser Weld 5000 platform at FABTECH North America 2025. The technology improves welding robustness, seam quality, and tolerance control by enabling synchronized laser beam movement through both robotic guidance and laser scanning systems.

Companies Covered in Laser Welding Machine Market

- TRUMPF

- Coherent Corp.

- IPG Photonics

- AMADA WELD TECH

- Han's Laser Technology Industry Group

- FANUC

- ABB

- KUKA

- Jenoptik

- Bystronic

- Prima Industrie

- Panasonic Connect

- Lincoln Electric

- Mitsubishi Electric

- Nidec Laser Rotech

- LaserStar Technologies

Frequently Asked Questions

The global laser welding machine market is anticipated to be valued at approximately US$2.3 billion in 2026.

The laser welding machine market is projected to reach approximately US$3.5 billion by 2033.

Key market trends include rising adoption of fiber laser welding systems, expansion of EV battery and semiconductor manufacturing, and increasing deployment of robotic and automated welding cells.

Fiber laser technology is the leading segment and is anticipated to account for approximately 48.3% of the market share in 2026 due to its high precision, energy efficiency, and compatibility with automated manufacturing systems.

The laser welding machine market is projected to grow at a CAGR of 6.2% between 2026 and 2033.

Major companies include TRUMPF, Coherent Corp., IPG Photonics, ABB, and FANUC.