- Advanced Materials

- Balsa Wood Market

Balsa Wood Market Size, Share, and Growth Forecast 2026 - 2033

Balsa Wood Market by Grade Type (Grade A, Grade B, Grade C), Product Form (Raw Blocks & Sheets, Processed), Application (Wind Energy, Aerospace & Defense, Marine, Industrial Construction, Transportation, Other), and Regional Analysis for 2026 - 2033

Balsa Wood Market Size and Trend Analysis

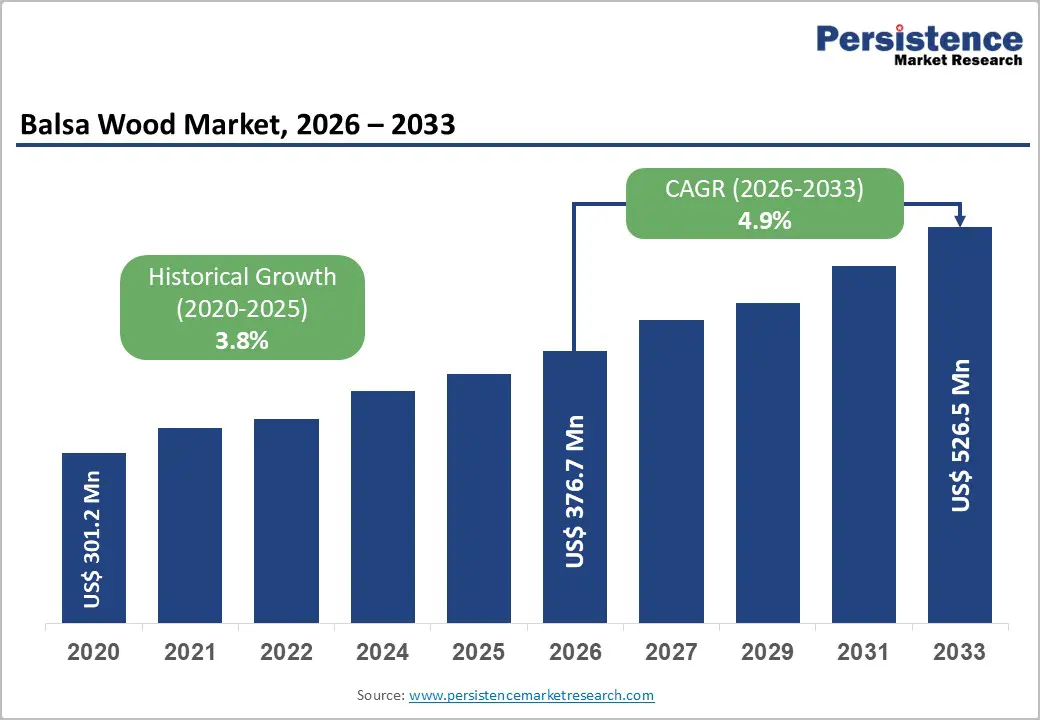

The global Balsa Wood market size is valued at US$ 376.7 million in 2026 and is projected to reach US$ 526.5 million by 2033, growing at a CAGR of 4.9% between 2026 and 2033. It is primarily driven by the sustained global expansion of wind energy capacity, growing aerospace composite demand, and the increasing adoption of sustainable lightweight materials across marine and industrial construction sectors.

Balsa wood's distinct honeycomb cellular structure, compressive strength of 3.6–5.0 MPa, and low density of 150–250 kg/m³ make it structurally irreplaceable in turbine blade cores, aircraft sandwich panels, and marine hull composites. According to the International Energy Agency (IEA), global wind energy capacity additions reached a record 117 GW in 2023, directly reinforcing demand for balsa wood core materials. Rising ecological awareness and Forest Stewardship Council (FSC) certification mandates further favor plantation-sourced balsa over synthetic foam substitutes in premium procurement segments, supporting the market's steady upward growth trajectory through the forecast period.

Key Industry Highlights:

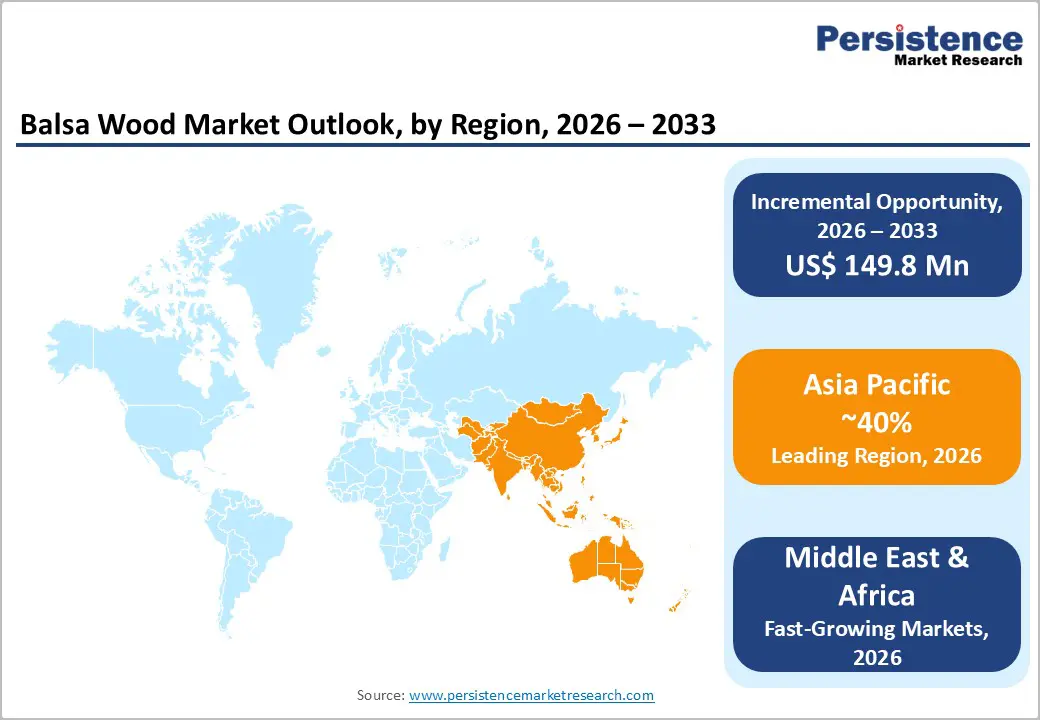

- Leading Region: Asia Pacific dominates the global Balsa Wood market, accounting for approximately 40% of total consumption in 2025, anchored by China's massive wind turbine manufacturing base and India's rapidly expanding renewable energy sector.

- Fastest Growing Region: The Middle East is projected to be the fastest-growing regional market for balsa wood, supported by increasing investment in renewable energy infrastructure and construction applications under national development plans in Saudi Arabia and the UAE.

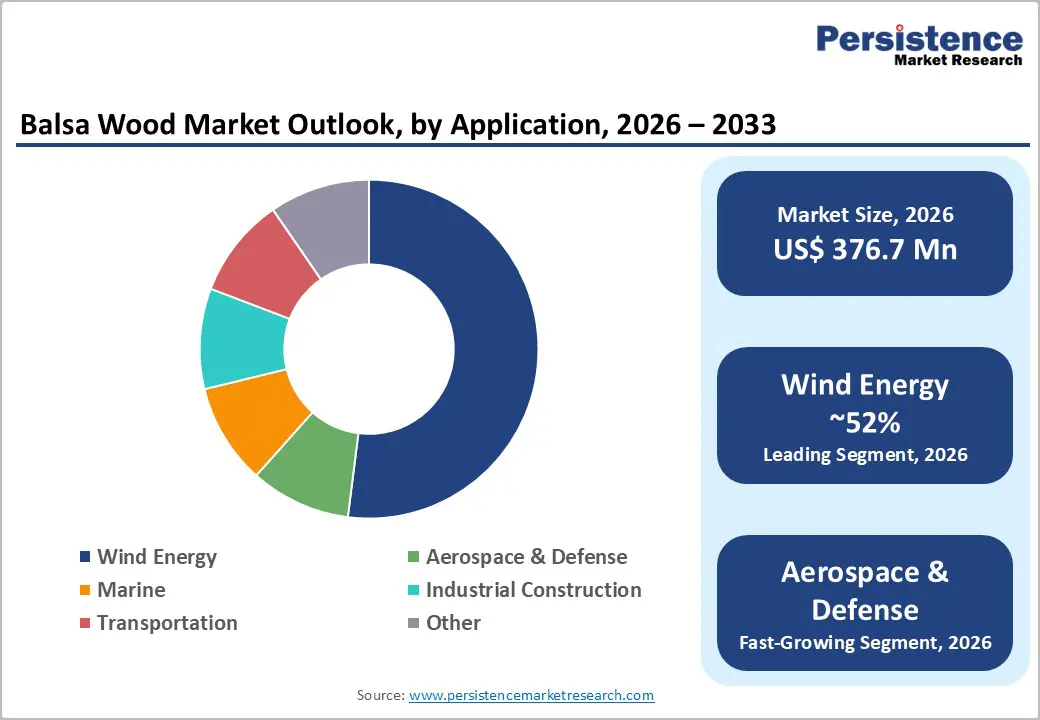

- Dominant Segment: The Wind Energy application segment leads the global market with approximately 52% share in 2025, driven by the non-substitutable role of balsa end-grain cores in structural blade root sections of turbines exceeding 5 MW in capacity.

- Fastest Growing Segment: Aerospace & Defense is projected to record the highest application-level CAGR through 2033, driven by eVTOL aircraft commercialization, rising defense composite adoption, and growing demand for ultra-lightweight balsa core inserts in satellite payload platforms.

- Key Opportunity: Offshore wind energy presents the largest single growth opportunity for balsa wood suppliers, with the Global Wind Energy Council (GWEC) projecting offshore capacity to exceed 380 GW by 2032, requiring increasingly material-intensive large-format turbine blades.

| Key Insights | Details |

|---|---|

|

Balsa Wood Market Size (2026E) |

US$ 376.7 Mn |

|

Market Value Forecast (2033F) |

US$ 526.5 Mn |

|

Projected Growth CAGR (2026–2033) |

4.9% |

|

Historical Market Growth (2020–2025) |

3.8% |

Market Dynamics

Drivers - Expanding Global Wind Energy Capacity Fuelling Demand for Lightweight Core Materials

The exponential growth in onshore and offshore wind energy installations globally remains the most powerful demand driver for the balsa wood market. According to the International Energy Agency (IEA), global wind energy capacity additions reached a record 117 GW in 2023, and cumulative installed wind capacity surpassed 1,000 GW globally that same year. Engineers at the National Renewable Energy Laboratory (NREL), United States, have calculated that a single 100-metre wind turbine blade requires approximately 150 cubic metres of balsa wood core material.

Balsa's end-grain panel structure delivers superior shear strength and fatigue resistance, properties that polymer foam alternatives struggle to replicate in blades exceeding 15 MW capacity, particularly in offshore deployments. With turbine blade lengths continuing to increase and offshore wind project pipelines expanding globally, per-unit balsa consumption is set to rise considerably, sustaining robust demand through 2033.

Growing Use of Balsa Wood in Aerospace, Defense, and Marine Composite Structures

Aerospace and defense applications represent the second-most significant demand driver, leveraging balsa wood's superior strength-to-weight ratio for structural panels, aircraft interior linings, drone airframes, and satellite payload platforms. According to the International Air Transport Association (IATA), global commercial aviation activity in 2024 surpassed 2019 pre-pandemic levels, prompting aircraft manufacturers to accelerate lightweight composite adoption for fuel efficiency.

Grade A balsa, with densities between 100–150 kg/m³, is increasingly specified in aerospace sandwich panels. In the marine sector, balsa core panels are used in yacht hulls, bulkheads, and naval vessel superstructures. The European Maritime Safety Agency (EMSA) has noted a sustained rise in composite-hulled vessel registrations across European Union member states, creating a stable and growing demand base for high-quality balsa sandwich core materials in marine composite applications.

Restraints - Supply Concentration and Illegal Logging Risks in Ecuador

The balsa wood market faces a critical supply vulnerability given that Ecuador produces over 90% of the world's commercial balsa, with annual exports averaging 56,000 tons from 2013 to 2022, according to the Environmental Investigation Agency (EIA). This geographic concentration creates exposure to weather-related disruptions, political instability, and unsustainable harvesting pressures.

A sharp demand surge in 2019–2020, driven by Chinese wind energy expansion, triggered documented illegal logging in protected Amazon territories. The Ecuador Ministry of Environment reported a 180% increase in illegally sourced balsa seizures, from 700 cubic metres in 2019 to 1,973 cubic metres in 2020, underscoring the supply chain fragility that threatens market participants' procurement reliability and ESG compliance posture.

Competition from Synthetic Core Substitutes Constraining Balsa Market Penetration

Balsa wood faces intensifying competition from synthetic alternatives, including PVC foam, PET foam, SAN foam, and aluminum honeycomb core materials. Industry composite manufacturing analyses note that in 2019, balsa commanded 38% of wind blade core material volume, compared to 31% for PVC and 25% for PET.

By the mid-2020s, PET foam had captured a significant share in non-critical blade sections, offering superior moisture resistance, dimensional consistency, and logistics cost advantages over a single-origin supply material. For manufacturers focused on total cost of ownership, synthetic foam panels present a compelling alternative, particularly in market segments where blade specifications do not demand peak compressive performance levels uniquely offered by balsa's end-grain structure.

Opportunities - Offshore Wind Expansion Creating Premium Demand for High-Grade Balsa Cores

The rapid global expansion of offshore wind energy represents a high-value growth opportunity for balsa wood market participants. The Global Wind Energy Council (GWEC) projects that offshore wind installations will surpass 380 GW by 2032, up from approximately 75 GW in 2023. Offshore turbines require blades frequently exceeding 100 metres in length, subject to far harsher fatigue loading and marine environments than onshore equivalents.

Grade A end-grain balsa, with compressive strength of 4.5–5.0 MPa, is technically preferred for these demanding applications because PET foam demonstrates reduced rigidity under dynamic marine loading at scale. Manufacturers capable of delivering FSC-certified, traceable, plantation-grown Grade A balsa through reliable and transparent supply chains are well-positioned to capture the pricing premium and long-term offtake agreements associated with offshore blade procurement programs.

eVTOL Aircraft and Next-Generation Aerospace Composite Applications

The nascent but fast-growing electric vertical take-off and landing (eVTOL) aircraft sector presents a significant emerging demand opportunity for balsa wood in ultra-lightweight structural panels. Both the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA) are actively developing airworthiness certification frameworks foreVTOL aircraft , validating the commercial scale-up trajectory of this segment.

The Vertical Flight Society reported that over 700 eVTOL designs were in active development globally as of 2024. Balsa wood cores are increasingly being specified for structural bulkheads, floor panels, and interior sandwiches in eVTOL prototype designs owing to their natural vibration damping, electromagnetic transparency, and low areal weight. Companies investing in precision-machined, tightly density-controlled Grade A balsa core components for advanced aerospace composites can capture high-value early-stage demand, particularly in North America and Europe.

Category-wise Analysis

Grade Type Insights

The Grade B segment accounted for approximately 42% of the global balsa wood market in 2024, making it the dominant grade type across the market. Grade B balsa is widely classified as an all-purpose material, offering a balanced combination of density, machinability, and structural integrity that makes it suitable for wind turbine blade core panels, trailing edges, marine deck structures, transportation floor panels, and model construction. Unlike Grade A, which requires more stringent density control for premium aerospace uses, Grade B provides flexibility for procurement teams managing cross-sectoral supply chains.

The grade's versatility has made it the material of choice for large-volume blade manufacturers in China and India, which collectively account for a dominant share of global wind capacity additions. Growing demand from industrial construction for lightweight, thermally efficient sandwich panels is expected to sustain Grade B's segment leadership through 2033.

Product Form Insights

Raw blocks and sheets constitute the dominant product form in the global balsa wood market, accounting for approximately 65% of total market volume in 2025. This leadership is primarily attributed to the superior structural flexibility offered by unprocessed forms, which allow downstream composite manufacturers to cut, shape, kerf, and score the material with high precision to meet specific curvature and panel geometry requirements. Wind turbine blade manufacturers, marine composite fabricators, and aerospace panel producers continue to rely heavily on raw blocks and sheets as their preferred procurement format.

The intrinsic cellular honeycomb structure of balsa wood, which enables accurate density grading during fabrication, is most effectively utilized through processing from raw forms. Although processed and pre-shaped core kits are gaining traction, particularly in Chinese blade manufacturing facilities due to labor cost efficiencies, raw blocks and sheets remain the foundational supply format globally.

Application Insights

The Wind Energy segment dominates the global balsa wood market by application, accounting for an estimated 52% of total market demand in 2025. Balsa wood's honeycomb end-grain structure is particularly suited to wind turbine blade sandwich construction; it delivers the highest shear strength per unit weight of any natural core material, a critical specification in blade root sections of turbines exceeding 5 MW. The Global Wind Energy Council (GWEC) reported that global wind power installations reached a record 117 GW in 2023, with China alone accounting for over 65 GW of that total.

Offshore wind blade programs, which require blades of 100 metres and above, are further intensifying per-unit balsa consumption. The wind energy segment is forecast to sustain its leading position through the forecast period, as global decarbonization commitments under the Paris Agreement continue to drive utility-scale wind procurement and blade manufacturing activity.

Regional Insights

North America Balsa Wood Market Trends

North America represents a mature and strategically important market for balsa wood, supported primarily by the United States’ advanced aerospace, marine, and renewable energy industries. The U.S. Department of Energy’s commitment to deploy 30 GW of offshore wind capacity by 2030 is expected to significantly increase demand for high-quality blade core materials, including Grade-A balsa. Major industry participants, such as GE-Vernova, are actively involved in wind blade manufacturing and balsa supply chain management.

However, supply chain traceability remains a compliance challenge, as highlighted by the Environmental Investigation Agency. The United States relies heavily on balsa imports from Ecuador and the Asia Pacific region, and accounted for approximately 20 percent of global import shipments in 2023–2024. Stringent regulations under the U.S. Lacey Act, combined with geopolitical shipping uncertainties, have modestly increased procurement costs.

Europe Balsa Wood Market Trends

Europe represents one of the most dynamic regional markets for balsa wood, underpinned by the continent’s rapid offshore wind expansion and its well-established aviation and marine manufacturing sectors. Germany, the United Kingdom, Denmark, Spain, and France are the principal consuming countries. The European Commission’s REPowerEU plan, which targets 600 GW of installed renewable energy capacity by 2030, positions offshore wind as a core growth pillar and significantly strengthens demand for large turbine blades and balsa wood core materials.

The United Kingdom’s Crown Estate Round-4 offshore wind leasing program, offering up to 32 GW of capacity, further reinforces this demand outlook. Germany’s industrial composite cluster, particularly around Airbus and marine shipbuilders, supports consistent consumption of Grade-A and Grade-B balsa. At the same time, the EU Deforestation Regulation is reshaping procurement practices by favoring FSC-certified, fully traceable suppliers, accelerating consolidation among established processors such as 3A-Composites and Gurit.

Asia Pacific Balsa Wood Trends

Asia Pacific represents the largest regional market for balsa wood, accounting for approximately 40% of global consumption in 2025. China is the principal demand driver, responsible for more than 50 percent of global balsa imports by volume during the 2024–2025 period. The country’s extensive wind energy expansion, including 65 GW of new installations in 2023, has positioned China as the world’s single largest consumer of balsa wood.

Long-term demand visibility is further supported by China’s 14th Five-Year Plan, which targets 1,200 GW of combined solar and wind capacity by 2030. India is emerging as a key secondary growth engine, supported by ambitious renewable energy targets and rising import volumes. Meanwhile, Vietnam and Indonesia are expanding balsa processing capabilities to serve regional composite manufacturers. Although geopolitical tensions have had a limited direct impact, elevated shipping insurance costs have moderately increased regional logistics expenses.

Competitive Landscape

The global balsa wood market exhibits moderate concentration at the processing and distribution level, with the top three players, Schweiter Technologies AG (3A Composites), Gurit Services AG, and DIAB International AB, collectively holding approximately 46% of global market revenue. Market leaders differentiate through vertical integration (plantation ownership to finished core panel), Forest Stewardship Council (FSC) certification, and advanced CNC kerfing and pre-shaping capabilities. Strategic activity includes joint ventures in Asia, acquisitions of engineering kitting firms, and expansion into processed blade core kitting services. Mid-tier players such as CoreLite Inc. and The Gill Corporation focus on cost-competitive solutions for marine and industrial segments, while regional manufacturers in China and Southeast Asia compete on pricing and geographic proximity to blade plants.

Key Developments:

- November 2026: 3A Composites Core Materials is pleased to announce that its BALTEK® balsa wood core materials are now fully EUDR ready, in advance of the EU Deforestation Regulation (EUDR) enforcement date of December 30, 2025.

- October 2024: The Environmental Investigation Agency (EIA US) released its 'Ill Wind' report, directly linking major wind turbine manufacturers including GE Vernova, Goldwind, and Mingyang to illegal balsa logging in Ecuador's Amazon, intensifying industry-wide pressure for FSC-compliant and fully traceable balsa supply chains.

- July 2024: Bougainville, Papua New Guinea, under the oversight of the Autonomous Bougainville Government (ABG), completed its first commercial balsa wood shipment, marking a meaningful step toward geographic supply diversification and reducing global market dependence on Ecuadorian supply.

Top Companies in the Balsa Wood Market

Schweiter Technologies AG / 3A Composites (Steinhausen, Switzerland), through its Baltek® and Airex® brands, holds over 25% of the global core-panel market share with installed processing capacity of approximately 100,000 m³/year. The company's fully integrated value chain, from plantation-owned Ecuadorian seed stock to precision-shaped end-grain panels delivered to global blade plants, underpins its market leadership.

Gurit Services AG (Zürich, Switzerland) holds the second-largest balsa wood market position with approximately 18% share of the global core material market. The company's balsa panel portfolio serves major European turbine OEMs, naval shipbuilders, and high-performance yacht manufacturers globally. In February 2025, Gurit announced a strategic portfolio diversification aimed at reducing its historical wind energy revenue concentration of 63% and expanding into marine and industrial composite material segments.

DIAB International AB (Laholm, Sweden) is a globally recognized structural core material manufacturer serving aerospace, marine, wind energy, and transportation sectors across 100 countries. Its balsa wood portfolio is complemented by PVC, PET, and SAN foam solutions. A joint venture established in Indonesia in 2024 aims to shorten supply lead times to Chinese blade manufacturing facilities, strengthening DIAB's competitive positioning across the Asia Pacific.

Companies Covered in Balsa Wood Market

- Schweiter Technologies AG (3A Composites)

- Gurit Services AG

- DIAB International AB

- CoreLite Inc.

- The PNG Balsa Company Ltd.

- Auszac Pty Ltd.

- Carbon-Core Corp.

- The Gill Corporation

- Guangzhou Sinokiko Balsa Co., Ltd.

- GM BALSA COMPOSITE S.A.

Frequently Asked Questions

The global Balsa Wood market was valued at US$ 301.2 Mn in 2020 and is estimated to reach US$ 376.7 Mn in 2026, projected to further expand to US$ 526.5 Mn by 2033, reflecting a forecast CAGR of 4.9% from 2026 to 2033.

The primary demand driver is the global expansion of wind energy capacity. According to the International Energy Agency (IEA), global wind capacity additions reached a record 117 GW in 2023. Engineers at the National Renewable Energy Laboratory (NREL) confirm that a single 100-metre wind turbine blade requires approximately 150 cubic metres of balsa wood core material, making wind energy the anchor end-use driving balsa demand.

The Wind Energy application segment leads the global balsa wood market, holding approximately 52% of total demand in 2025. Balsa's superior shear strength and compressive performance of 3.6–5.0 MPa make it the preferred core material for high-capacity turbine blades, particularly in offshore installations exceeding 5 MW.

Asia Pacific is the dominant regional market, accounting for approximately 40% of global balsa wood consumption in 2024. China's wind energy sector, with 65 GW of new capacity added in 2023 per the National Energy Administration (NEA), makes it the world's largest single importer of balsa wood by volume.

The most significant market opportunity lies in the offshore wind energy sector. The Global Wind Energy Council (GWEC) projects global offshore wind capacity to surpass 380 GW by 2032, requiring increasingly large turbine blades that demand premium Grade A balsa end-grain cores with FSC certification and fully traceable sustainable supply chains.

The leading companies in the global balsa wood market include Schweiter Technologies AG (3A Composites), Gurit Services AG, and DIAB International AB, which together hold approximately 46% of global market revenue. Other notable participants include CoreLite Inc., The Gill Corporation, Guangzhou Sinokiko Balsa Co., Ltd., The PNG Balsa Company Ltd., and Carbon-Core Corp.