- Pharmaceuticals

- Alzheimer’s Disease Therapeutics Market

Alzheimer’s Disease Therapeutics Market Size, Share, and Growth Forecast 2026 - 2033

Alzheimer’s Disease Therapeutics Market by Drug Type (Cholinesterase Inhibitors, NMDA Receptor Antagonists, Disease-Modifying Therapies (Monoclonal Antibodies), Combination Therapies), by Route of Administration (Oral, Injectable, Transdermal), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Specialty Clinics), by Regional Analysis, 2026 - 2033

Alzheimer’s Disease Therapeutics Market Share and Trend Analysis

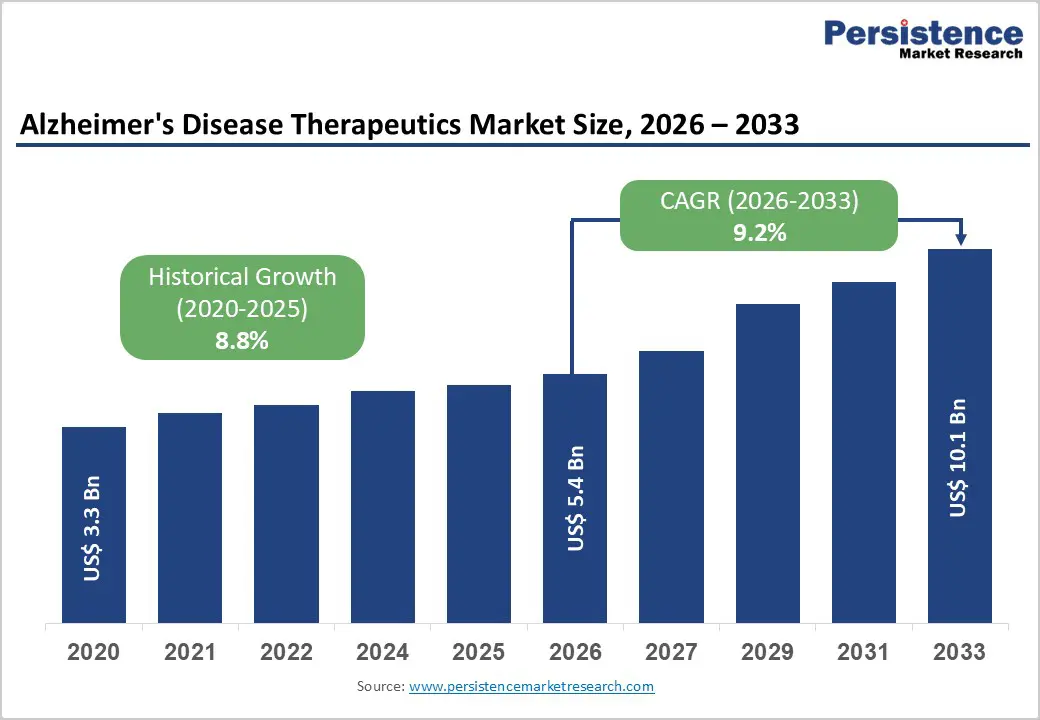

The global Alzheimer’s Disease Therapeutics Market size is expected to be valued at US$ 5.4 billion in 2026 and projected to reach US$ 10.1 billion by 2033, growing at a CAGR of 9.2% between 2026 and 2033. The primary stems from the rise in prevalence of Alzheimer's disease due to an aging population worldwide, coupled with breakthroughs in disease-modifying therapies that promise better patient outcomes.

For instance, recent approvals of monoclonal antibodies have shifted focus from symptomatic relief to slowing disease progression, supported by increased R&D investments from leading pharmaceutical firms. Additionally, rising awareness campaigns by organizations like the Alzheimer's Association and favorable reimbursement policies in key regions are accelerating market expansion by improving access to innovative treatments.

Key Industry Highlights:

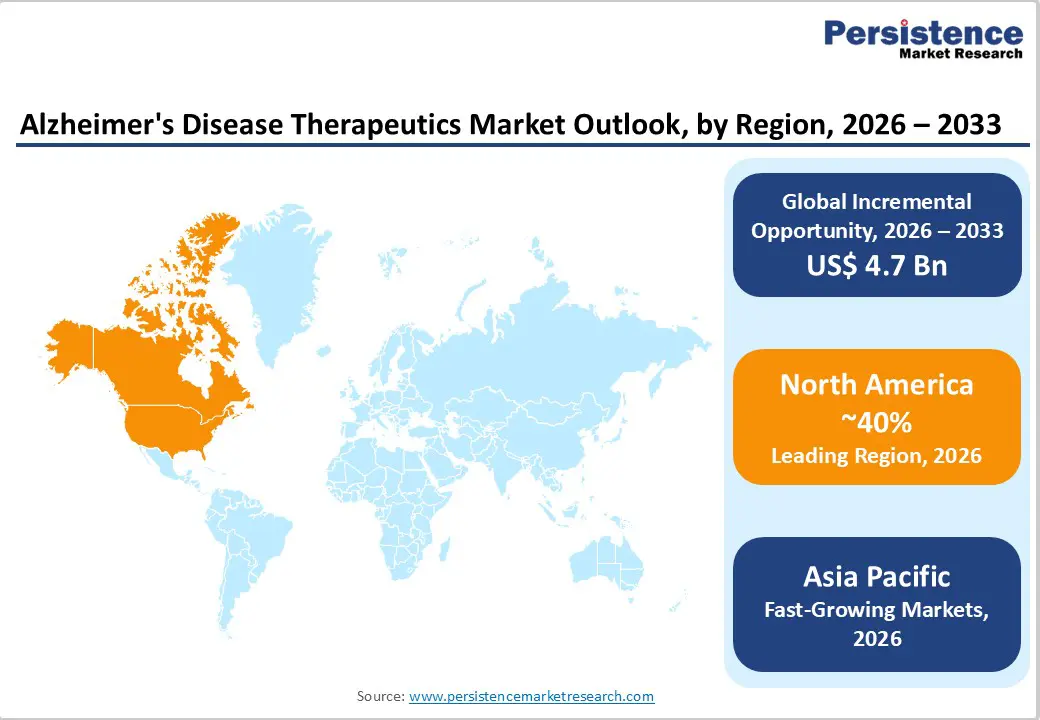

- North America leads with 40% share in 2025, supported by a strong healthcare infrastructure, high diagnosis rates, and rapid adoption of innovative biologics. The United States remains the primary contributor due to advanced research capabilities, favorable reimbursement policies, and an estimated 6.7 million Alzheimer’s patients, driving sustained therapeutic demand.

- Asia Pacific is the fastest-growing region, driven by rapidly aging populations in China and Japan, where Alzheimer’s cases are projected to nearly double by 2030. Improving healthcare access, expanding insurance coverage, and increasing clinical trial activity are accelerating market penetration across emerging economies.

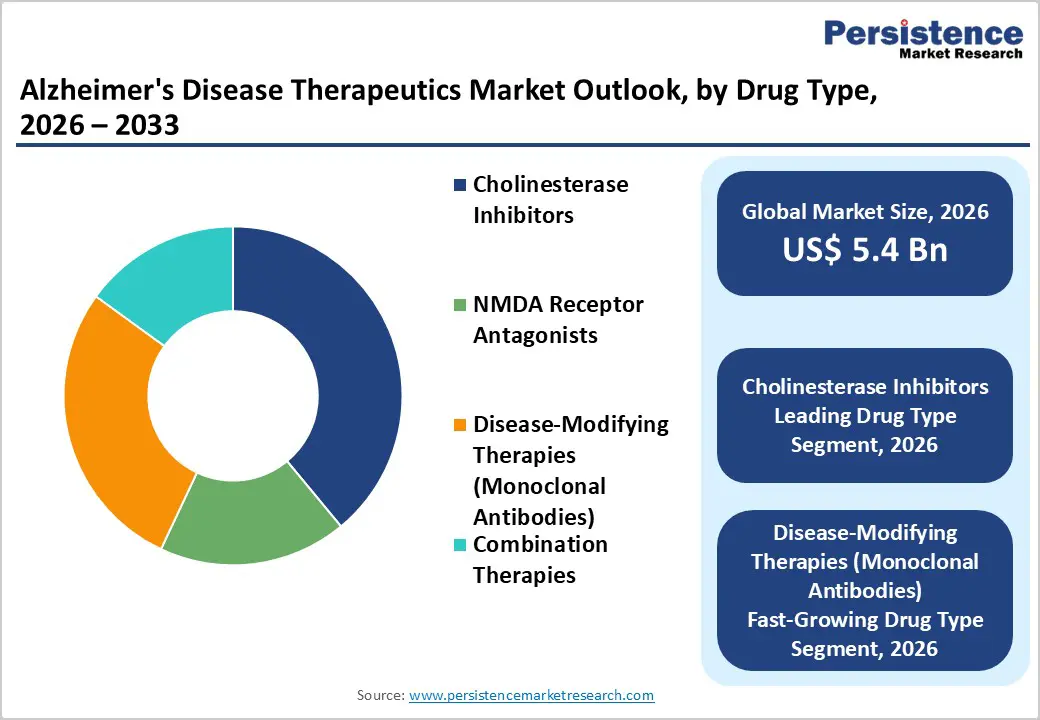

- Cholinesterase Inhibitors dominate drug types with 39% share, as widely prescribed generics such as donepezil remain first-line therapy for mild-to-moderate disease. Their affordability, long-standing safety profile, and strong physician familiarity maintain high prescription volumes globally.

- Disease-Modifying Therapies (Monoclonal Antibodies) are the fastest-growing segment, fueled by recent FDA approvals and strong clinical interest in slowing disease progression. High annual treatment costs and expanded reimbursement support are significantly boosting revenue growth.

| Key Insights | Details |

|---|---|

|

Alzheimer’s Disease Therapeutics Market Size (2026E) |

US$ 5.4 billion |

|

Market Value Forecast (2033F) |

US$ 10.1 billion |

|

Projected Growth CAGR (2026-2033) |

9.2% |

|

Historical Market Growth (2020-2025) |

8.8% |

Market Dynamics

Drivers - Rising Prevalence of Alzheimer's Disease

The surging incidence of Alzheimer's disease, driven by global aging demographics, is a key growth driver for the therapeutics market. According to the World Health Organization (WHO), over 55 million people worldwide live with dementia, with Alzheimer's accounting for 60-70% of cases, and this number is projected to triple by 2050 due to longer life expectancies. This demographic shift increases demand for effective treatments, particularly in regions with expanding geriatric populations like North America and Europe. Pharmaceutical companies are responding with accelerated clinical trials, leading to higher adoption rates of approved therapies. The positive impact is evident in improved patient management and reduced caregiver burden, fostering sustained market momentum.

Advancements in Disease-Modifying Therapies

Breakthroughs in disease-modifying therapies, especially monoclonal antibodies targeting amyloid-beta plaques, are propelling market growth by offering hope beyond symptomatic relief. The U.S. Food and Drug Administration (FDA) has approved drugs like lecanemab and donanemab, demonstrating 27-35% slower cognitive decline in early-stage patients in phase 3 trials published in journals like The New England Journal of Medicine. These innovations validate years of research, encouraging further investment and pipeline development. Consequently, they enhance treatment efficacy, boost physician confidence, and drive prescription volumes, significantly expanding the addressable market for Alzheimer's therapeutics.

Restrains - High Development Costs and Treatment Expenses

High development costs and premium treatment pricing remain major restraints in the Alzheimer’s Disease Therapeutics Market. Alzheimer’s drug development is particularly expensive due to long clinical trial durations, large patient populations, advanced imaging requirements, and complex biomarker assessments. Clinical trials often span 8–12 years, significantly increasing capital investment and risk exposure. Moreover, the disease’s multifactorial nature contributes to exceptionally high failure rates, especially in late-stage trials, leading to substantial financial losses for pharmaceutical companies. As a result, manufacturers price successful therapies at premium levels to recover investments. Newly approved monoclonal antibodies and disease-modifying biologics are often priced at tens of thousands of dollars annually, creating affordability challenges for patients and reimbursement pressures for insurers and public healthcare systems. In low- and middle-income countries, limited healthcare funding and weak insurance penetration further restrict access. These economic barriers reduce patient uptake, slow commercial expansion, and create disparities in treatment availability across regions, ultimately restraining overall market growth despite therapeutic advancements.

Regulatory and Approval Hurdles

Stringent regulatory requirements significantly restrain growth in the Alzheimer’s Disease Therapeutics Market. Due to historical clinical failures and safety concerns, regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) demand robust evidence demonstrating meaningful cognitive and functional benefits. Alzheimer’s trials require long follow-up periods to prove disease progression modification, often extending approval timelines by several years. Additionally, endpoints such as cognitive scales, biomarker validation, and neuroimaging results must meet strict statistical significance thresholds, increasing complexity and uncertainty. Regulatory agencies also mandate post-marketing surveillance and risk management programs, particularly for monoclonal antibodies associated with adverse events like amyloid-related imaging abnormalities (ARIA). These extensive review processes increase development timelines and costs, discouraging smaller biotechnology firms from entering the market independently. Delayed approvals reduce competitive intensity and slow patient access to innovative therapies. While regulatory caution ensures safety and efficacy, it simultaneously limits rapid innovation diffusion and market expansion across global healthcare systems.

Opportunity - Expansion into Disease-Modifying Therapies

Expansion into disease-modifying therapies represents a major growth opportunity in the Alzheimer’s Disease Therapeutics Market. Unlike traditional symptomatic treatments that temporarily manage cognitive decline, disease-modifying therapies (DMTs) aim to slow or alter the underlying pathology of the disease, particularly amyloid beta plaques and tau protein tangles. Growing scientific advancements in biomarker identification, neuroimaging, and early diagnosis are enabling earlier intervention, which improves the commercial potential of these therapies. Recent regulatory approvals of monoclonal antibodies have validated the clinical and commercial feasibility of targeting disease progression, encouraging increased investment from pharmaceutical companies and venture capital firms. Furthermore, aging populations worldwide and rising Alzheimer’s prevalence create a strong demand for long-term solutions rather than short-term symptom management. Governments and healthcare systems are also prioritizing funding for innovative neurological treatments. As pipeline activity intensifies, partnerships, licensing agreements, and biologics manufacturing expansion are expected to accelerate, positioning disease-modifying therapies as the fastest-growing and most transformative segment of the market.

Category-wise Analysis

Drug Type Insights

Cholinesterase inhibitors are projected to lead the drug type segment with around 39% market share in 2025, primarily due to their long-standing clinical use and strong physician familiarity. These agents remain the standard first-line therapy for mild-to-moderate Alzheimer’s disease, supported by decades of clinical data demonstrating modest but meaningful cognitive and functional benefits. Their widespread generic availability significantly lowers treatment costs, improving affordability across both developed and emerging markets. Additionally, multiple dosage forms, including oral tablets and transdermal patches, enhance patient compliance and convenience, particularly among elderly populations who may struggle with complex regimens. While disease-modifying biologics are gaining attention, cholinesterase inhibitors continue to dominate prescription volumes due to their established safety profile, broad reimbursement coverage, and inclusion in major clinical treatment guidelines worldwide.

Route of Administration Insights

Oral administration is expected to account for approximately 60% of the market share in 2025, maintaining its dominance due to convenience, affordability, and patient acceptance. Oral drugs are particularly suited for chronic conditions like Alzheimer’s, where long-term daily treatment is required. Physicians generally prefer prescribing oral medications because they are easy to initiate, require minimal clinical infrastructure, and reduce hospital dependency. High adherence rates observed in real-world settings further strengthen this segment, as patients and caregivers favor non-invasive options over injectable alternatives. Moreover, oral therapies are widely available through retail pharmacies, improving accessibility across urban and rural areas. Although intravenous biologics are expanding rapidly, oral administration remains the backbone of treatment due to cost-effectiveness and strong integration into routine dementia care pathways.

Distribution Channel Insights

Hospital pharmacies are anticipated to hold approximately 45% share in 2025, largely driven by the growing adoption of injectable disease-modifying therapies that require clinical supervision. The introduction of monoclonal antibodies has shifted a portion of treatment administration from outpatient retail settings to hospital-based infusion centers. These therapies require neurologist oversight, imaging monitoring, and management of potential adverse effects such as amyloid-related imaging abnormalities (ARIA). As a result, treatment initiation and follow-up are frequently coordinated within hospital systems. Hospitals also serve as primary diagnostic and referral centers for Alzheimer’s disease, making them key hubs for therapy initiation. While retail pharmacies remain important for oral symptomatic treatments, the increasing role of biologics is strengthening hospital pharmacy dominance in overall market revenue terms.

Regional Insights

North America Alzheimer’s Disease Therapeutics Market Trends and Insights

North America dominates the Alzheimer’s disease therapeutics market due to advanced healthcare infrastructure, strong reimbursement systems, and early adoption of innovative therapies. The United States represents the largest contributor, supported by high disease prevalence among the aging population and substantial healthcare expenditure. The region has been at the forefront of approving and commercializing disease-modifying monoclonal antibodies, accelerating market growth. Strong presence of major pharmaceutical companies, robust clinical trial activity, and continuous investment in neuroscience research further strengthen regional leadership. Favorable regulatory pathways for breakthrough therapies and expanded Medicare coverage for select biologics have improved patient access. Additionally, growing awareness initiatives, early diagnostic adoption using biomarkers and imaging technologies, and expanding specialty infusion centers are reshaping treatment patterns. With increasing focus on early-stage intervention and premium biologics uptake, North America continues to set the pace for innovation and revenue generation in the global market.

Asia Pacific Alzheimer’s Disease Therapeutics Market Trends and Insights

Asia Pacific is emerging as a high-growth region in the alzheimer’s disease therapeutics market, driven by rapid population aging and improving healthcare infrastructure. Countries such as China, Japan, India, and South Korea are witnessing a steady rise in dementia prevalence, increasing demand for both symptomatic and disease-modifying treatments. Expanding government healthcare programs and growing insurance penetration are improving access to diagnosis and therapy. Japan, with one of the world’s oldest populations, leads regional adoption of innovative biologics, while China is strengthening domestic research and fast-tracking regulatory pathways. Rising awareness campaigns, improved diagnostic capabilities, and investment in neurology-focused hospitals are accelerating market expansion. Although affordability challenges remain, increasing clinical trial activity and partnerships between global and regional pharmaceutical companies are positioning Asia Pacific as the fastest-growing emerging market.

Competitive Landscape

The global alzheimer’s disease therapeutics market is moderately consolidated, with a mix of established pharmaceutical players and emerging biotechnology firms competing across symptomatic and disease-modifying segments. Competition is intensifying as innovation shifts from traditional oral therapies toward high-value biologics targeting amyloid and tau pathways. Companies are focusing heavily on clinical pipeline expansion, strategic collaborations, and licensing agreements to strengthen neurological portfolios. Late-stage trial success and regulatory approvals significantly influence competitive positioning due to high development risks and costs. Pricing strategies, reimbursement coverage, and real-world efficacy data also play a critical role in market share dynamics.

Key Developments:

- In October 2025, Eisai Co., Ltd., announced that Health Canada had issued a Notice of Compliance with Conditions (NOC/c) for the humanized anti-soluble aggregated amyloid-beta (Aβ) monoclonal antibody LEQEMBI® (lecanemab). The approval was granted for the treatment of adult patients diagnosed with mild cognitive impairment or mild dementia due to Alzheimer’s disease (early AD) who were apolipoprotein E ε4 (ApoE ε4) non-carriers or heterozygotes and had confirmed amyloid pathology. LEQEMBI became the first therapy in Canada authorized for early Alzheimer’s disease that targeted an underlying cause of the condition rather than only addressing symptoms.

Companies Covered in Alzheimer’s Disease Therapeutics Market

- Biogen Inc.

- Eisai Co., Ltd.

- Eli Lilly and Company

- F. Hoffmann-La Roche Ltd

- Novartis AG

- Pfizer Inc

- Johnson & Johnson

- H. Lundbeck A/S

- AstraZeneca PLC

- AC Immune SA

- Daiichi Sankyo Company

- Limited, Alzheon Inc

- Merck & Co., Inc

- TauRx Pharmaceuticals

Frequently Asked Questions

The alzheimer’s disease therapeutics market is expected to reach US$ 5.4 billion in 2026.

Rising Alzheimer's prevalence from aging populations, affecting 55 million globally per the WHO.

North America with 40% share in 2025, is driven by U.S. FDA approvals.

Cholinesterase Inhibitors at 39% share due to generic availability.

Disease-modifying monoclonal antibodies in Asia Pacific amid rising cases.

Leaders include Biogen Inc., Eisai, and Eli Lilly with approved monoclonals.