- Pharmaceuticals

- Antiseptic and Disinfectant Market

Antiseptic and Disinfectant Market Size, Share, and Growth Forecast 2026 - 2033

Antiseptic and Disinfectant Market Product Type (Quaternary Ammonium Compounds, Chlorine Compounds), Application (Enzymatic Cleaners, Medical Device Disinfectants), Sales Channel, End-user, and Regional Analysis, 2026 - 2033

Antiseptic and Disinfectant Market Size and Trends Analysis

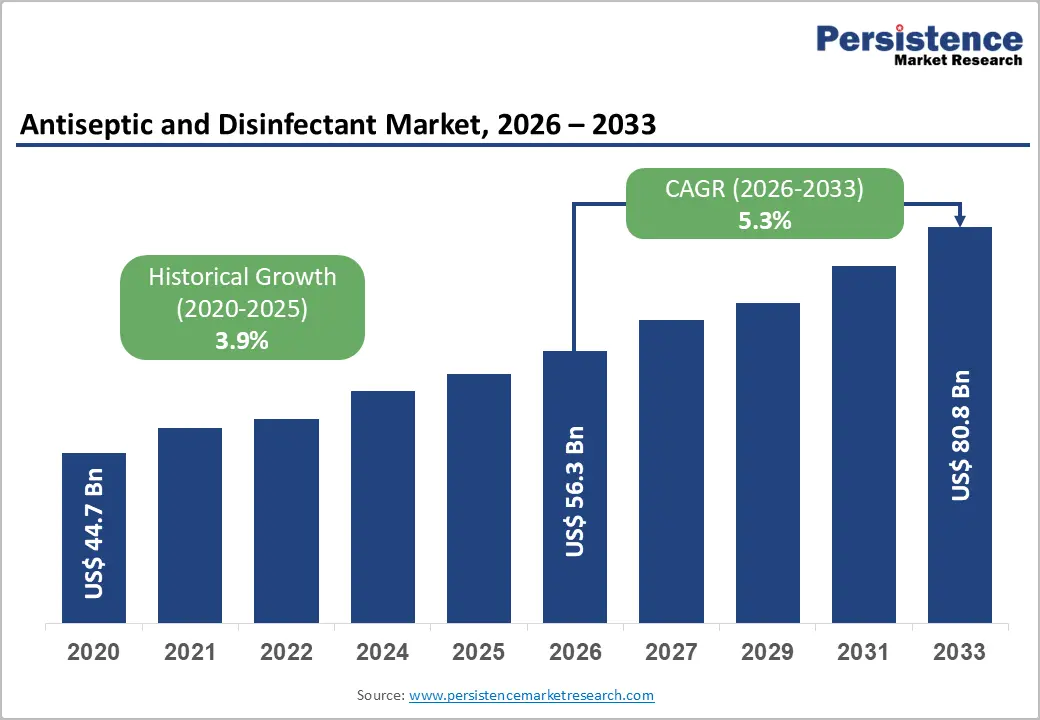

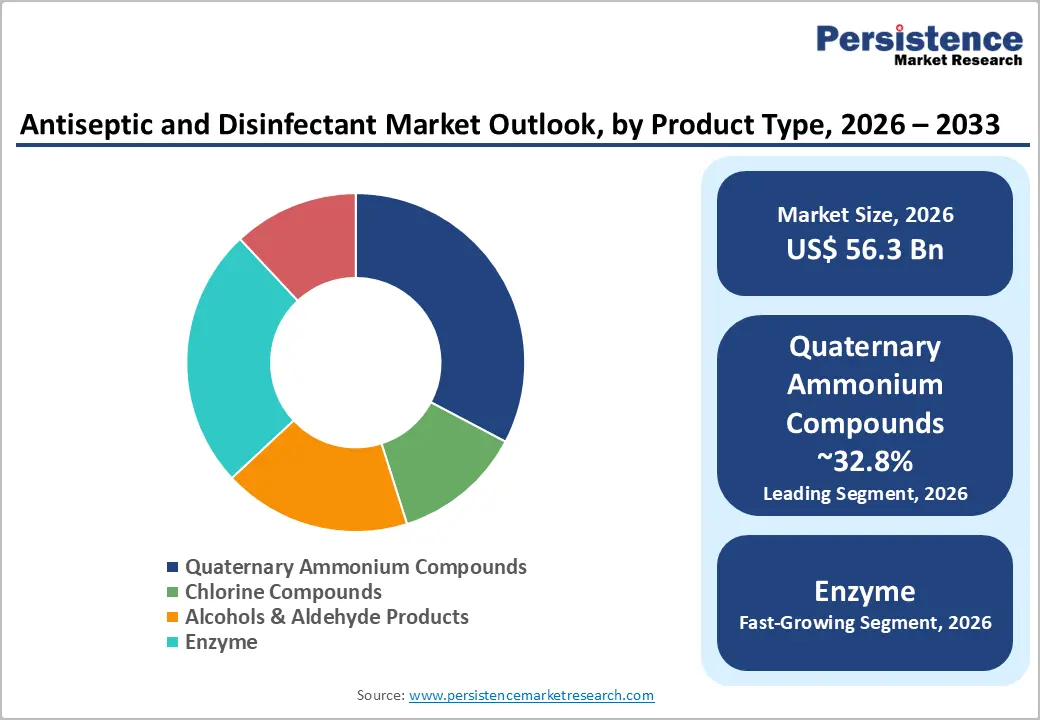

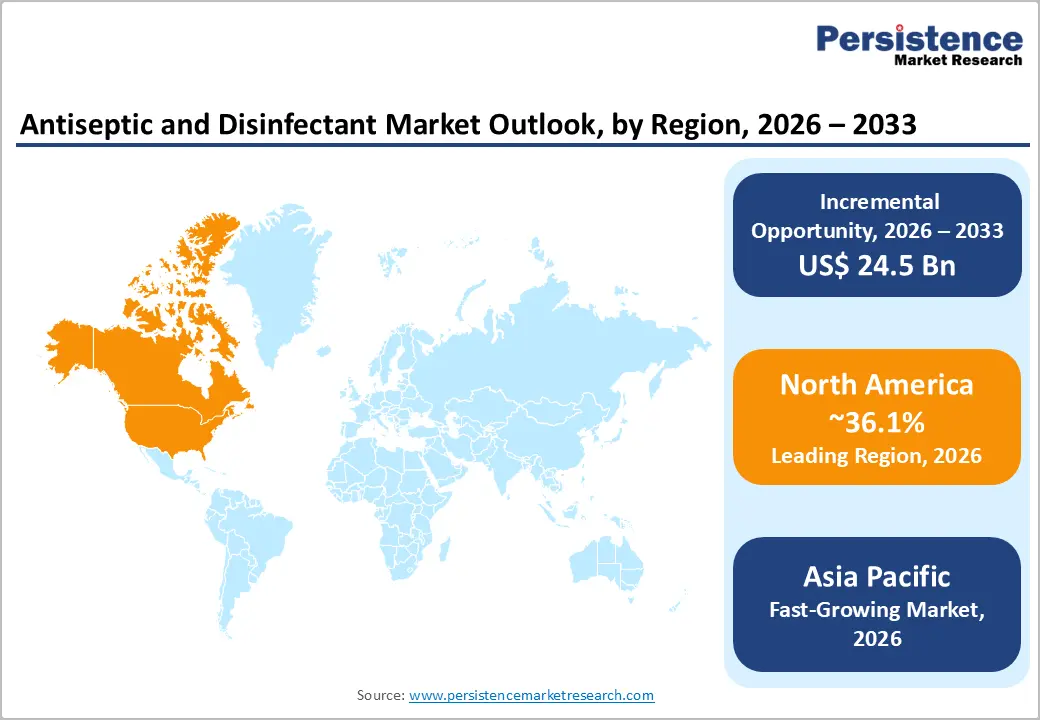

The global antiseptic and disinfectant market size is likely to be valued at US$56.3 billion in 2026 and is expected to reach US$80.8 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033, driven by the persistent burden of infections and the rising emphasis on prevention across healthcare systems.

Healthcare-associated infections remain a daily risk, affecting about 1 in 31 hospital patients at any given time in the U.S., underscoring the severity of the problem.

Key Industry Highlights:

- Leading Region: North America, with around 36.1% of share in 2026, owing to strict infection control regulations, high surgical volumes, and widespread adoption of novel disinfection technologies across healthcare facilities.

- Fast-growing Region: Asia Pacific, due to ongoing hospital expansion, rising surgical procedures, and improving hygiene awareness following COVID-19.

- Funding Round: In April 2025, CARB-X funded ArrePath with US$3.7 million to accelerate treatments targeting multidrug-resistant infections. This reflects broad investment momentum in infection prevention and control technologies.

- Leading Product Type: Quaternary Ammonium Compounds (QACs), approximately 32.8% of the market share in 2026, as these provide broad-spectrum efficacy with low corrosion, making them suitable for frequent use across multiple surfaces.

- Dominant Application: Medical device disinfectants, with nearly 46.2% of share in 2026, as reusable instruments require mandatory high-level disinfection to prevent cross-contamination and infection outbreaks.

DRO Analysis

Driver - Rising Emphasis on Infection Control in Healthcare Settings

Healthcare facilities are intensifying hygiene protocols to limit hospital-acquired infections (HAIs), which remain a persistent burden. According to the World Health Organization (WHO), out of every 100 hospitalized patients, 7 in developed and 10 in developing countries acquire at least one HAI.

Pathogens such as MRSA and Clostridioides difficile have pushed hospitals to adopt routine surface disinfection, hand antisepsis, and instrument sterilization practices. Recent guidelines from the Centers for Disease Control and Prevention (CDC) and WHO have further strengthened compliance requirements, making disinfectant use non-negotiable in critical care areas. This has also pushed demand beyond hospitals to diagnostic labs, dialysis centers, and long-term care facilities, where infection risks are equally high.

Increasing Surgical Volumes to Propel Demand for High-Level Disinfection Practices

The steady rise in surgical procedures, including minimally invasive and same-day surgeries, is creating consistent demand for antiseptics and high-level disinfectants. Data from the Organization for Economic Co-operation and Development (OECD) shows that procedures such as cataract surgeries and cesarean sections have increased significantly over the past decade across prominent healthcare systems.

Each procedure requires strict pre-operative skin antisepsis and post-operative instrument sterilization to avoid complications. The surging use of reusable medical devices, including endoscopes, has also heightened demand for specialized disinfection solutions. This is because improper reprocessing has been linked to outbreaks of infection in recent years.

Restraint - Toxicity Concerns and Material Compatibility Issues

Several commonly used disinfectant chemistries raise safety and usability concerns, particularly in high-frequency or enclosed environments. Compounds such as formaldehyde and phenolics are associated with respiratory irritation and potential long-term health risks, requiring controlled handling, proper ventilation, and protective equipment.

Even widely used agents such as sodium hypochlorite (bleach) can corrode metals, degrade plastics, and damage sensitive medical equipment over time, increasing maintenance costs for healthcare facilities. The U.S. CDC has also highlighted cases where improper disinfectant use led to chemical exposure incidents among hospital staff. These drawbacks are pushing end users to reconsider their product choices, often slowing adoption or compelling a shift toward safer but sometimes less cost-effective alternatives.

Opportunity - Adoption of Automated Systems and New Disinfectant Formats

Healthcare and commercial facilities are increasingly integrating automated disinfection technologies to reduce human error and improve consistency. Systems such as UV-C robots and hydrogen peroxide vapor units are being deployed in hospitals to disinfect patient rooms within minutes, especially after infectious cases.

For instance, studies published in 2023 showed UV-C devices can reduce surface pathogens by over 90% when used alongside manual cleaning. Demand for ready-to-use formats, including pre-saturated wipes, is also rising, mainly in high-turnover settings such as outpatient clinics and diagnostic labs. The shift toward plastic-free or biodegradable wipes is also gaining traction as hospitals adjust their procurement practices to meet sustainability targets.

Shift toward Environmentally Responsible Formulations Opening New Avenues

There is a gradual transition toward disinfectants that balance efficacy with environmental and user safety. Regulatory pressure, especially in Europe under the Biocidal Products Regulation (BPR), is encouraging the use of biodegradable and low-toxicity ingredients. Companies are introducing plant-based or hydrogen peroxide-based formulations that decompose into non-harmful byproducts such as water and oxygen.

Accelerated hydrogen peroxide solutions, for instance, are being widely adopted in healthcare settings as they provide short contact times with reduced residue. This trend is further supported by institutional buyers, including hospitals and hospitality chains. They are incorporating sustainability criteria into vendor selection, creating new opportunities for green product development.

Category-wise Analysis

Product Type Insights

Quaternary Ammonium Compounds (QACs) are estimated to lead with approximately 32.8% of the share in 2026. These are widely used as they strike a balance between efficacy, safety, and material compatibility. Unlike harsher agents such as chlorine, QACs are non-corrosive and can be safely used on floors, walls, and medical surfaces without damaging equipment. They are effective against a wide range of bacteria and enveloped viruses, which makes them ideal for routine disinfection in hospitals, offices, and public spaces. Their low odor and residual antimicrobial effect further increase their practicality for frequent use. This versatility has made QAC-based formulations a standard choice in both healthcare and commercial cleaning protocols.

The enzyme segment is anticipated to follow by registering a decent CAGR over the forecast period, as these products help overcome the limitations of traditional disinfectants, particularly in eliminating organic residues such as blood, mucus, and biofilms. Instead of just killing microbes, enzymes break down proteins, fats, and carbohydrates at the source. This is important in reprocessing complex medical devices, such as endoscopes, where biofilm formation has been linked to outbreaks of infection. Recent healthcare guidelines increasingly recommend enzymatic pre-cleaning before high-level disinfection. These products are also generally less toxic and more environmentally friendly, meeting strict safety and sustainability requirements in healthcare facilities.

Application Insights

Medical device disinfectants are projected to dominate with nearly 46.2% of the market share in 2026, as these represent one of the most important infection transmission pathways in healthcare settings. Hence, they require rigorous and repeated disinfection. Reusable devices such as surgical instruments, catheters, and endoscopes must be high-level disinfected or sterilized after each use to prevent cross-contamination.

Reports from the US Food and Drug Administration (FDA) and the CDC have shown infection clusters linked to improperly disinfected endoscopes, underscoring the need for validated disinfection protocols. As the use of minimally invasive devices increases, the demand for specialized disinfectants that are both effective and compatible with delicate equipment continues to rise.

Enzymatic cleaners are anticipated to be the fastest-growing segment in 2026, as disinfection alone is ineffective if organic debris is not removed first. Blood, tissue, and other residues can shield microorganisms from chemical disinfectants, reducing their effectiveness. Enzymes break down these residues, ensuring that subsequent disinfection steps can reach and eliminate pathogens.

This is particularly relevant for devices with narrow channels or complex designs, such as endoscopes and dental instruments. Clinical studies have shown that inadequate pre-cleaning is a leading cause of sterilization failure. This has pushed hospitals to standardize enzymatic cleaning as a mandatory first step in instrument reprocessing workflows.

Regional Insights

North America Antiseptic and Disinfectant Market Trends

In 2026, North America is predicted to lead and account for about 36.1% of the share as disinfection is embedded into routine healthcare workflows rather than being reactive. Over 95% of hospitals follow standardized hand hygiene and disinfection protocols, and nearly half of healthcare facilities use high-grade disinfectants daily.

The region also consumes massive volumes of ready-to-use formats such as wipes, estimated at over a billion units monthly, reflecting preference for speed and compliance. Automation is gaining traction, with over a quarter of public facilities adopting automated sanitization systems, showing a shift toward technology-led infection control.

U.S. Antiseptic and Disinfectant Market Trends

The U.S. stands out for strong regulatory oversight by bodies such as the CDC, EPA, and FDA, which standardizes product approval and use. Infection risks remain a key trigger. During the 2023 to 2024 flu season alone, there were about 40 million cases, underscoring the importance of routine disinfection across healthcare and community settings.

The country also sees high surgical volumes and device usage, which directly increases demand for medical-grade disinfectants. Incidents such as infection exposure risks in hospitals due to poor sterilization practices have further tightened compliance and auditing requirements.

Asia Pacific Antiseptic and Disinfectant Market Trends

Asia Pacific will likely be the fastest-growing market in 2026, backed by rising hospital admissions and surgical volumes. More than 400 million hospitalizations and 50 million surgeries take place annually across the region. Growth is being boosted by expanding private healthcare infrastructure and increasing awareness of infection risks after COVID-19.

Unlike mature markets, there is still variability in hygiene practices, which creates both demand and inconsistency. Governments are now pushing strict infection control norms, especially in large economies, which is accelerating the adoption of hospital-grade disinfectants.

Japan Antiseptic and Disinfectant Market Trends

Japan’s market is defined by precision, consistency, and high regulatory compliance. With nearly 30% of its population aged 65 and above, the country faces high vulnerability to infections, especially in hospitals and long-term care facilities. This has led to strict adherence to disinfection protocols, including frequent use of alcohol-based antiseptics and unique surface disinfectants.

Japan also has a superior culture of hygiene, which extends beyond healthcare into public and commercial spaces. Hospitals prefer low-residue, fast-acting formulations to ensure patient safety and equipment compatibility. Automation in disinfection, including UV-based systems, is also gradually being adopted in healthcare settings to improve efficiency and reduce manual dependency.

China Antiseptic and Disinfectant Market Trends

China’s market is mainly pushed by expansion. Public hospitals handle extremely high patient loads, often exceeding capacity, which increases the frequency of surface disinfection and hand hygiene practices. Following COVID-19, the government strengthened infection control guidelines, making routine disinfection mandatory across hospitals, schools, and public transport systems.

Reports from the National Health Commission have showcased gaps in hospital hygiene compliance, compelling facilities to upgrade disinfection protocols and adopt high-grade products. At the same time, domestic manufacturers dominate the market with cost-effective formulations. There is also a rising demand for novel products in Tier-1 cities where private hospitals and premium care facilities are expanding.

Europe Antiseptic and Disinfectant Market Trends

Europe operates under one of the most stringent regulatory frameworks, specifically the Biocidal Products Regulation (BPR). It ensures safety and efficacy standards for disinfectants. This has led to consistent use of approved formulations across hospitals, food processing, and public infrastructure.

Healthcare systems in the region perform tens of millions of surgeries annually and maintain frequent surface cleaning cycles, often multiple times a day, driving steady consumption. There is also a gradual shift toward eco-friendly and low-toxicity formulations, especially compared to North America.

U.K. Antiseptic and Disinfectant Market Trends

The U.K. stands out due to centralized healthcare governance through the National Health Service (NHS), which enforces strict infection control standards across hospitals and clinics. High-profile reports on hospital-acquired infections have led to routine audits and mandatory disinfection practices, especially for high-touch surfaces and reusable devices.

Hospitals in the U.K. follow frequent cleaning cycles and standardized disinfectant use, contributing to consistent demand. The country has also been an early adopter of disinfectant wipes and ready-to-use formats, particularly in clinical and community healthcare settings.

France Antiseptic and Disinfectant Market Trends

France’s market is bolstered by public healthcare infrastructure and strict hygiene compliance in hospitals and eldercare facilities. The country has been actively promoting infection prevention measures, primarily in response to concerns about antimicrobial resistance.

Hospitals are constantly adopting oxidizing disinfectants and hydrogen peroxide-based solutions to reduce chemical exposure. Sustainability is also becoming a procurement factor. This is because public institutions are prioritizing biodegradable formulations and reduced chemical residues in cleaning protocols.

Competitive Landscape

The global antiseptic and disinfectant market is moderately fragmented, but with dominance of a few global and multi-segment players. Large companies such as 3M, Ecolab, Reckitt, STERIS, and Procter & Gamble operate across both healthcare-grade disinfection and consumer hygiene, giving them expansion advantages in distribution, research, and regulatory compliance. The presence of regional manufacturers and private-label brands keeps pricing competitive, especially in developing markets.

What makes this market different from typical FMCG categories is that competition is split into two parallel tracks. In the institutional segment, firms compete on efficacy certifications, spectrum coverage, and compatibility with medical devices. For example, players, including STERIS and Getinge, focus on sterilization systems and high-level disinfectants used in surgical settings. In the retail or FMCG segment, on the other hand, brands such as Reckitt (Dettol) and P&G compete on brand trust, convenience formats, and pricing.

Key Industry Developments:

- In January 2026, The Clorox Company announced the acquisition of GOJO Industries for US$2.25 billion. This acquisition helped the former bring the Purell brand under its portfolio to strengthen its position across both surface disinfectants and hand hygiene solutions.

- In December 2025, Punjab Agricultural University (PAU) introduced a bioenzyme-based disinfectant and cleaning product range under EcoSol. It used fermented citrus waste to create biodegradable and low-toxicity formulations to address rising concerns over chemical exposure from conventional disinfectants.

- In June 2025, ArrePath secured a new financing round led by the Boehringer Ingelheim Venture Fund. It aimed to expand its anti-infective research platform, indirectly supporting development in antimicrobial and hygiene-related solutions.

Companies Covered in Antiseptic and Disinfectant Market

- Steris Plc

- Kimberly-Clark Corporation

- 3M

- Reckitt Benckiser

- Bio-Cide International, Inc.

- Johnson & Johnson

- Cardinal Health

- BD

- Others

Frequently Asked Questions

The global antiseptic and disinfectant market is projected to be valued at US$ 56.3 billion in 2026.

The antiseptic and disinfectant market is expected to reach US$ 80.8 billion by 2033.

Shift toward eco-friendly formulations and surging use of automated disinfection systems are the key market trends.

Medical device disinfectants are expected to lead with nearly 46.2% of the share in 2026, as reusable instruments require high-level disinfection to prevent infection transmission.

The market is expected to grow at a CAGR of 5.3% from 2026 to 2033.

Steris Plc, Kimberly-Clark Corporation, 3M, and Reckitt Benckiser are a few key market players.