- Pharmaceuticals

- Contrast Media Market

Contrast Media Market Size, Share, and Growth Forecast 2026 - 2033

Contrast Media Market by Product Type (Microbubble, Gadolinium-based), by Modality (Ultrasound, Magnetic Resonance Imaging), by Route of Administration (Intravenous, Oral), by Application, and Regional Analysis, 2026 - 2033

Contrast Media Market Size and Trend Analysis

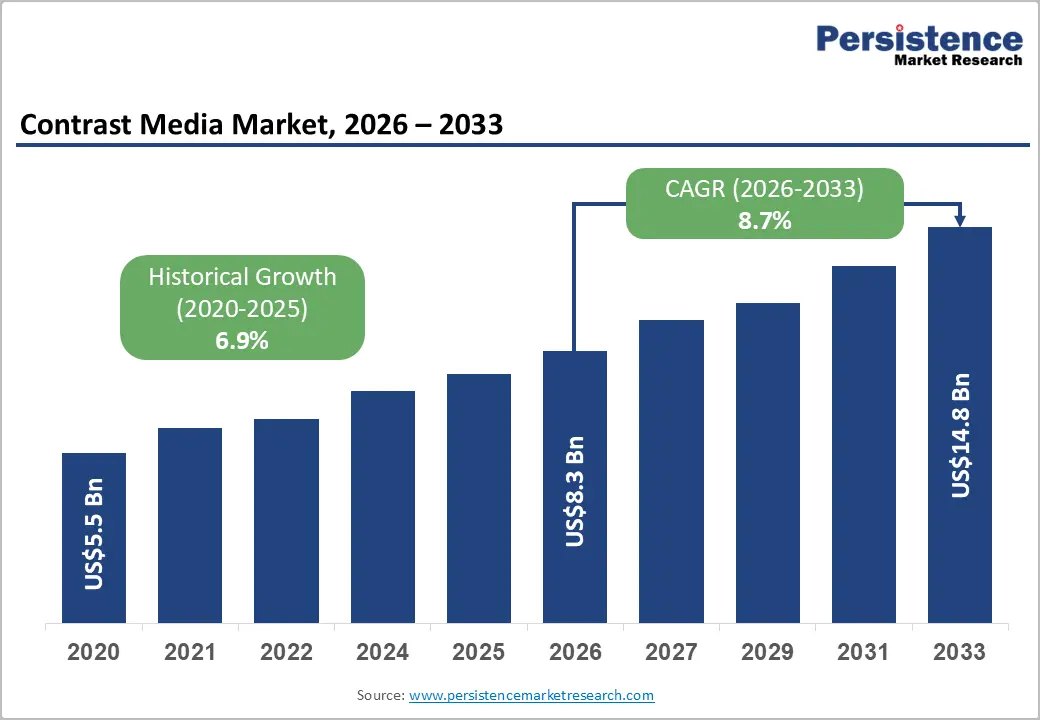

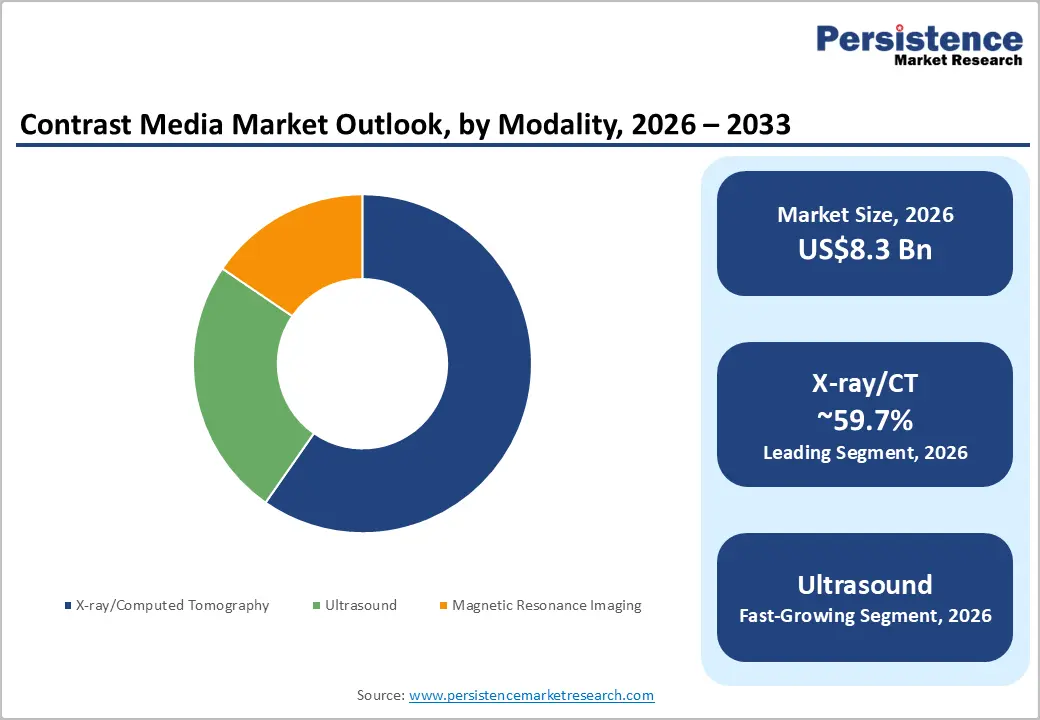

The global contrast media market size is likely to be valued at US$8.3 billion in 2026 and is predicted to reach US$14.8 billion by 2033, growing at a CAGR of 8.7% during the forecast period from 2026 to 2033, driven by the rising volume of diagnostic imaging procedures, where early and accurate detection is becoming a clinical priority. Increasing adoption of advanced imaging modalities, supported by technological upgrades, is also strengthening demand.

Key Industry Highlights:

- New Product: In April 2025, Voyageur Pharmaceuticals launched a new barium contrast product line in Canada and other markets accepting Health Canada standards. The launch followed a clinical performance study at Canada Diagnostic Centers on 24 subjects, where the company's high-density barium suspensions were praised for image quality in gastrointestinal and small bowel exams.

- Leading Product Type: Iodinated contrast media, approximately 70.2% share in 2026, owing to its ability to provide low toxicity and high image clarity for cardiovascular, neurological, and oncology imaging.

- Dominant Modality: X-ray/CT, nearly 59.7% in 2026, backed by developments in photon-counting CT, dual-energy CT, and spectral imaging, which improve diagnostic precision.

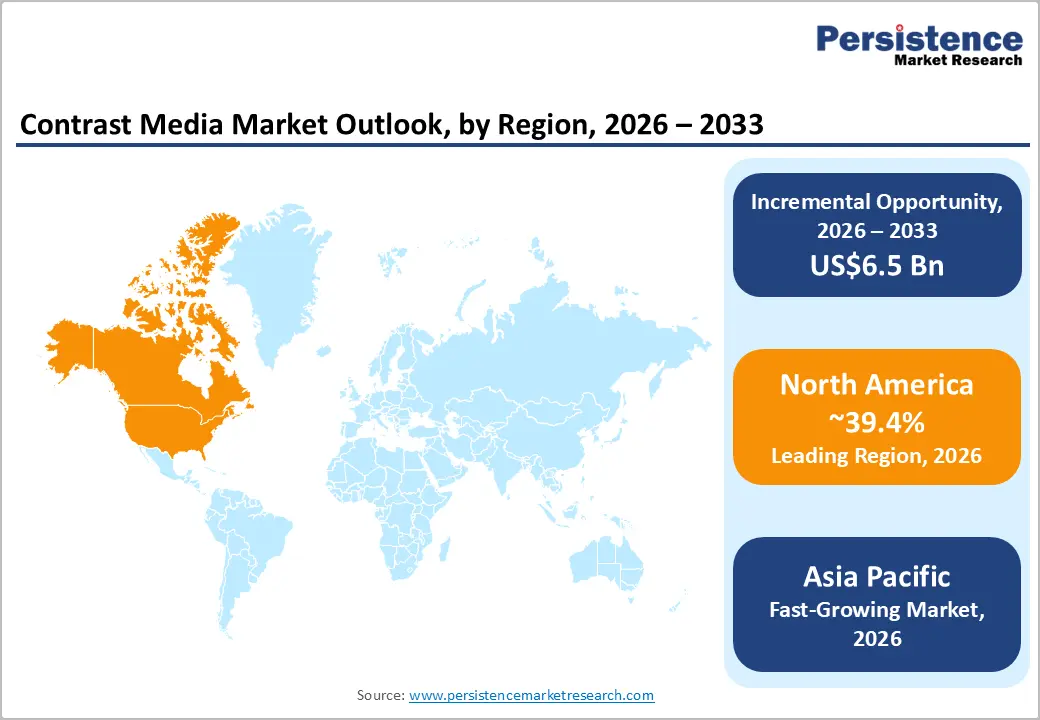

- Leading Region: North America, with about 39.4% share in 2026, owing to high adoption of premium contrast agents and favorable reimbursement policies.

- Fast-growing Region: Asia Pacific, spurred by the expansion of diagnostic imaging infrastructure across India and China.

DRO Analysis

Driver - Increasing Prevalence of Chronic Diseases

Cancer and cardiovascular diseases are among the most prominent demand drivers for contrast media. According to the World Health Organization (WHO), cardiovascular diseases cause 17.9 million deaths annually, while cancer accounts for nearly 10 million deaths globally. Both conditions require repeated imaging for initial diagnosis, staging, treatment planning, and monitoring, making contrast agents a routine part of care pathways.

What makes this more significant is the detection gap. A 2025 study in Clinical Breast Cancer showed that contrast-enhanced mammography detected 80% of cancers, compared to just 41% with traditional 2D mammography. As clinical evidence for contrast-enhanced imaging continues to improve, more guidelines are likely to recommend it as a standard step in disease workup.

Surge in Diagnostic Imaging Volumes Worldwide

The enormous volume of medical imaging procedures performed worldwide continues to drive strong demand for contrast media. Globally, nearly 4.2 billion imaging procedures are conducted annually, including around 450 million CT scans and 150 million MRI scans, with contrast agents used in a substantial proportion of these examinations. In the United States alone, more than 40 million contrast-enhanced CT and MRI procedures are performed each year. This imaging volume continues to rise steadily, fueled by increasing diagnostic needs and expanding healthcare access.

In May 2025, Royal Philips launched the RADIQAL study across six hospitals in Spain, the Czech Republic, Denmark, and the U.S., enrolling 824 patients to test ultra-low-radiation-dose technology for coronary procedures using diluted contrast media. This signals that innovation is actively working to expand the eligible patient population and make contrast imaging more accessible in more clinical settings.

Restraint - Safety Concerns around Gadolinium and Kidney Injury

Safety concerns associated with Gadolinium-Based Contrast Agents (GBCAs) remain a persistent restraint for the market. Research has confirmed that gadolinium accumulates in the brain, bones, and kidneys even in patients with normal kidney function, and the risk grows with repeated exposure. The European Medicines Agency's Pharmacovigilance and Risk Assessment Committee recommended suspending marketing authorizations for four linear gadolinium agents, including Bracco's MultiHance and Bayer's Magnevist, based on evidence of brain accumulation.

The U.S. Food and Drug Administration’s (FDA) Medical Imaging Drugs Advisory Committee in 2017 recommended expanding warning labels across all GBCAs. It also required manufacturers to conduct additional human and animal safety studies to assess potential long-term effects. For patients with compromised kidney function, GBCA exposure can trigger nephrogenic systemic fibrosis, a serious condition. These concerns push clinicians to limit or avoid contrast in vulnerable populations, capping procedure volumes and demand.

Opportunity - Smart Contrast Delivery through AI-Assisted Protocols

Most hospitals today still use a one-size-fits-all approach to contrast dosing. The same volume is utilized for every patient regardless of weight, kidney function, or scanner type. AI-supported systems deliver a solution by selecting the optimal contrast injection protocol for a specific patient, scanner, and clinical indication. It helps in improving both patient outcomes and workflow efficiency.

In December 2025, Bayer received FDA 510(k) clearance to extend the MEDRAD Centargo multi-patient CT injector's compatibility to include single-dose vials across five contrast agents, building toward a more flexible, data-driven injection ecosystem. As more injectors connect to hospital networks and patient data, AI-personalized dosing is poised to reduce contrast waste, lower adverse-event risk, and extend existing contrast supplies.

Development of New Agents by Utilizing Iron Oxide Nanoparticles

Gadolinium safety concerns have opened the door to a new class of contrast agents, iron oxide nanoparticles (IONPs), which are processed differently by the body and do not carry the same kidney-related risks. Ultrasmall superparamagnetic iron oxide nanoparticles with a core diameter of less than 5 nanometers are emerging as next-generation MRI contrast agents, offering superior imaging performance, long blood circulation times, and renal clearance.

A research team at MIT developed iron oxide nanoparticles at just 4.7 nanometers, making them small enough to pass through the kidneys safely after injection. This matters as patients with impaired kidney function are currently excluded from multiple contrast-enhanced scans. IONPs could unlock this underserved patient group, creating a meaningful commercial and clinical opportunity as gadolinium restrictions tighten globally.

Category-wise Analysis

Product Type Insights

The iodinated contrast media segment is projected to lead with nearly 70.2% market share in 2026, driven by CT scanning, where these agents are indispensable, which is the most widely performed imaging modality globally. A research letter published in JAMA Network Open in December 2025 found that iodinated agents accounted for 95.6% of all contrast media volume administered to Medicare beneficiaries between 2011 and 2024, with CT abdomen and pelvis scans alone contributing 4.4 billion milliliters.

The microbubble contrast media segment is expected to be the fastest-growing in the forecast period. They are gas-filled microspheres used exclusively with ultrasound, and they are gaining traction quickly because they offer a radiation-free, kidney-safe alternative to CT and MRI contrast agents. They are the first-line imaging option for several indications and can be used across CT suites, operating rooms, and echo labs. They are also safe for patients who are allergic to iodinated or gadolinium agents.

Modality Insights

The X-ray/Computed Tomography (CT) segment is expected to dominate, with approximately 59.7% share in 2026, as it is fast, widely available, and clinically essential across emergency medicine, oncology, and cardiology. According to the National Institutes of Health (NIH), contrast media is used in 48% of the 91.4 million annual CT scans performed in the U.S., underscoring its key role in improving diagnostic accuracy. The modality also benefits from ongoing technology upgrades, including photon-counting CT.

The ultrasound segment is expected to remain in second place in 2026. Its appeal lies in what it doesn't involve, i.e., no ionizing radiation, no nephrotoxic agents, and no high costs. This makes Contrast-Enhanced Ultrasound (CEUS) particularly valuable for patients with kidney issues, pregnant women, and pediatric cases. China extended reimbursement for contrast-enhanced ultrasound, opening access for 300 million rural residents, demonstrating how policy changes can dramatically expand the patient base for this modality.

Regional Insights

North America Contrast Media Market Trends

North America is expected to dominate with approximately 39.4% of the share in 2026, fostered by high chronic disease burden, dense imaging infrastructure, and superior reimbursement support. The Centers for Disease Control and Prevention (CDC) reports that over 129 million Americans suffer from at least one chronic disease, while imaging procedures exceed 80 million CT scans annually in the U.S. The FDA's fast-track approvals for new contrast agents also give this market a regulatory edge. Key manufacturers such as GE Healthcare, Bracco Diagnostics, Bayer, and Lantheus are headquartered or have their primary operations here, further strengthening supply chain advantages.

U.S. Contrast Media Market Trends

The U.S. is on a strong growth trajectory propelled by aging demographics, expanding cancer screening mandates, and developments in imaging technology. Medicare Advantage plans in the U.S. cover annual lung CT screening for 14 million high-risk smokers, creating a recurring pipeline of contrast media demand. High healthcare spending, innovations in delivery systems, and well-structured reimbursement policies are further supporting market growth. The shift toward outpatient imaging centers, which deliver short wait times and competitive pricing, is also creating new demand channels beyond hospitals.

Asia Pacific Contrast Media Market Trends

Asia Pacific is the standout growth region, as healthcare infrastructure is expanding rapidly across large, underserved populations. Medical tourism across Japan, South Korea, India, Thailand, and Singapore has pushed high demand for premium-quality imaging services. Governments across the region are investing in diagnostics as part of broad universal health coverage initiatives. Multinational players are responding as well.

China Contrast Media Market Trends

China blends a massive patient population with ongoing hospital modernization, making it one of the highest-priority markets for contrast media manufacturers. The country represents a strategic focus for several contrast media manufacturers due to vast patient populations and increasing hospital modernization. The government's healthcare reforms aim to expand insurance coverage and modernize tertiary care centers. The country also has its own growing domestic players. General Electric Pharmaceuticals operates one of the world's largest contrast media manufacturing facilities in Shanghai, giving China both a demand and supply role in the global market.

India Contrast Media Market Trends

India's market is at an inflection point, augmented by a prominent expansion of public diagnostic infrastructure. The country added 15,000 imaging centers through the Ayushman Bharat program by 2025, thereby widening access to diagnostic imaging for low-income populations. Foreign manufacturers are also doubling down. Bracco's new India manufacturing facility, opened in July 2025, signals increasing confidence in the market's expansion. With one of the youngest and fastest-urbanizing populations globally, demand for early disease detection is expected to keep rising.

Europe Contrast Media Market Trends

Europe is a mature but steadily expanding market, supported by aging demographics and stringent regulatory frameworks that push clinicians toward safe and new contrast agents. The European Medicines Agency's strict stance on linear gadolinium agents has also pushed manufacturers to invest in macrocyclic and next-generation alternatives, indirectly spurring research and development and product renewal across the region.

Germany Contrast Media Market Trends

Germany leads Europe both in market share and growth pace, benefiting from a combination of superior clinical research culture, high imaging utilization, and an aging population. Home to Bayer, one of the top four global contrast media players, the country also benefits from proximity to major research and development centers and from early adoption of novel imaging protocols, including spectral CT and contrast-enhanced ultrasound.

U.K. Contrast Media Market Trends

The U.K. market's growth is largely driven by the National Health Service (NHS). Improved investments in NHS modernization have increased the use of contrast media in MRI and CT examinations. NHS data shows that same-day reporting of CT scan results improved from 81% in 2013 to 91% in 2023, reflecting a system that is scanning more and faster. In July 2026, a new Contrast Media and Associated Injectors Framework was launched to streamline NHS procurement, with suppliers including Bayer, Bracco, GE Healthcare, and Guerbet. This was a structural move that is anticipated to make purchasing more efficient and reliable across NHS trusts, underpinning sustained demand.

Competitive Landscape

The global contrast media market is highly consolidated, with GE Healthcare, Bayer AG, Bracco Imaging, and Guerbet collectively holding around 75% of the total share. This is a mature market where dominant players have held their positions for decades, backed by deep hospital relationships, regulatory approvals, and large-scale manufacturing infrastructure. Innovation is becoming the new battleground since generics are commoditizing standard agents.

In October 2024, GE Healthcare announced positive Phase I trial results for a manganese-based MRI contrast agent. It is a potential alternative to gadolinium, which has faced safety scrutiny over retention in the brain. Reducing nephrotoxicity and developing targeted agents for specific imaging modalities are now central competitive priorities. Biotech firms are also working on nanoparticle-based agents that bypass the kidneys entirely.

Key Industry Developments:

- In December 2025, Bayer presented results from the QUANTI Pediatric study at the RSNA annual congress in Chicago. It showed that gadoquatrane met primary and secondary endpoints in children with known or suspected disease. The study confirmed that the pharmacokinetic behavior seen in adults also applies to pediatric patients, at the same 60% reduced gadolinium dose.

- In September 2025, GE Healthcare launched a new line of contrast agents designed specifically for pediatric patients, addressing a gap in the market for age-appropriate imaging solutions. The move complies with the broad industry trend toward personalized medicine.

- In March 2026, Bracco Imaging commercially launched AiMIFY in the European Union at ECR 2026 in Vienna. AiMIFY is an AI-supported software co-developed with Subtle Medical that improves contrast enhancement in brain MRI images.

Companies Covered in Contrast Media Market

- Bracco S.p.A.

- Fresenius Kabi USA, LLC

- Trivitron Healthcare

- Bayer AG

- GE HealthCare

- Beijing Beilu Pharmaceutical Co., Ltd.

- JB Pharma

- Guerbet; iMAX

- Lantheus Holdings, Inc.

- GRUPO JUSTE

- Voyageur Pharmaceuticals Ltd

- Jodas Expoim Pvt. Ltd.

- Livealth

- Blue Jet Healthcare.

- Arco Lifesciences (I) Pvt. Ltd.

- Others

Frequently Asked Questions

The global contrast media market is projected to be valued at US$8.3 billion in 2026.

The contrast media market is expected to reach US$14.8 billion by 2033.

Technological developments in high-resolution CT & MRI scanners and the emergence of renal-safe iron-oxide nanoparticle agents are the key market trends.

X-ray/CT is expected to lead with nearly 59.7% of the share in 2026, as emergency departments and oncology centers rely heavily on contrast-enhanced CT for rapid whole-body imaging.

The contrast media market is expected to grow at a CAGR of 8.7% from 2026 to 2033.

Bracco S.p.A., Fresenius Kabi USA, LLC, Trivitron Healthcare, Bayer AG, and GE HealthCare are a few key market players.