- Pharmaceuticals

- Diabetic Ketoacidosis Treatment Market

Diabetic Ketoacidosis Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Diabetic Ketoacidosis Treatment Market by Treatment Type (Fluid Replacement Therapy, Electrolyte Replacement Therapy), Route of Administration (Parenteral/IV, Oral/Enteral), End-user (Hospitals), and Regional Analysis, 2026 - 2033

Diabetic Ketoacidosis Treatment Market Size and Trends Analysis

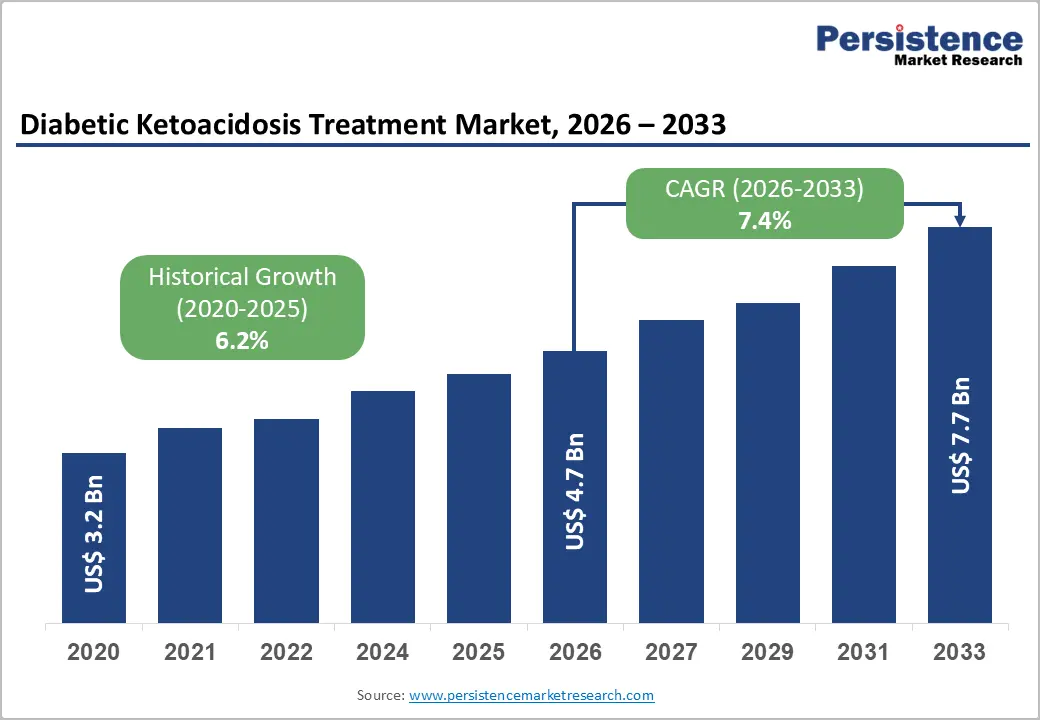

The global diabetic ketoacidosis treatment market size is likely to be valued at US$4.7 billion in 2026 and is expected to reach US$7.7 billion by 2033, growing at a CAGR of 7.4% between 2026 and 2033, driven by the rising global diabetes burden, with the IDF Diabetes Atlas 2023 reporting over 537 million adults currently living with diabetes, each carrying measurable diabetic ketoacidosis risk.

Key Industry Highlights:

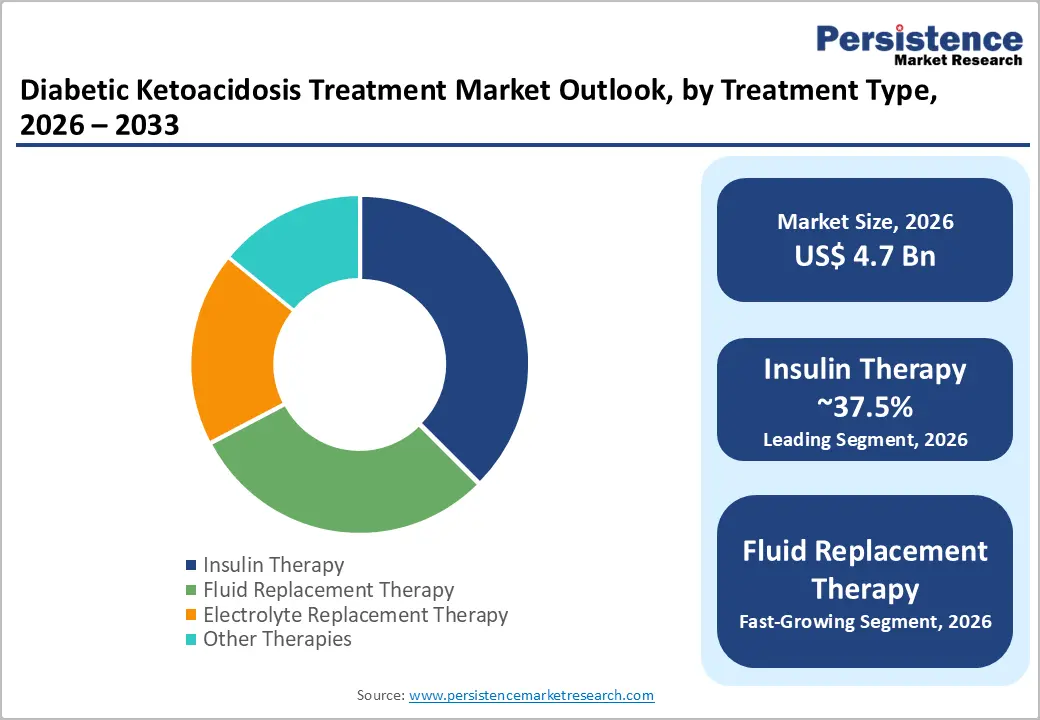

- Leading Treatment Type: Insulin therapy, with nearly 29.5% share in 2026, as insulin is the only therapy that directly halts ketogenesis at its source.

- Dominant End-user: Hospitals, approximately 76.4% of share in 2026, as DKA management requires continuous venous blood gas monitoring, real-time electrolyte correction, and cardiac surveillance for potassium-driven arrhythmias.

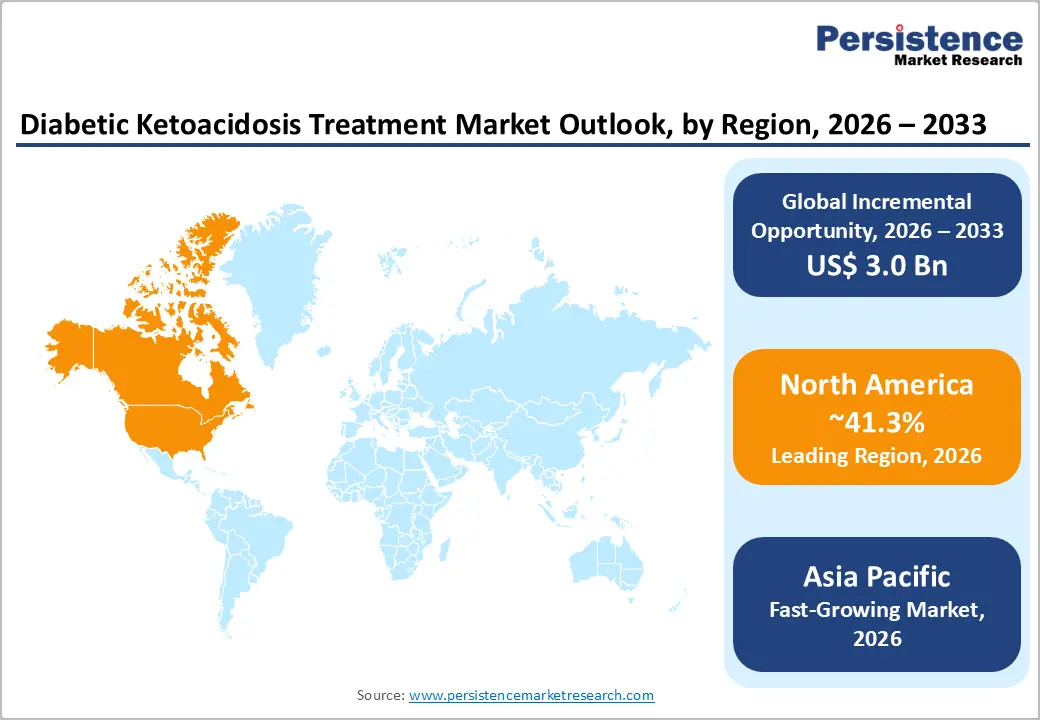

- Leading Region: North America, with about 36.8% share in 2026, owing to increasing DKA-related clinical research and comprehensive insurance coverage for insulin.

- Fast-growing Region: Asia Pacific, spurred by improving diagnostic infrastructure across India and China.

- FDA Approvals: In April 2026, the U.S. Food and Drug Administration (FDA) approved Foundayo (orforglipron), while in March 2026, it approved Awiqli (insulin icodec-abae) for diabetes management. These approvals are anticipated to support novel glucose control strategies and lower the long-term risk of severe diabetic complications, including diabetic ketoacidosis.

DRO Analysis

Driver - Increasing Prevalence of Diabetes Worldwide

As diabetes spreads globally, Diabetic Ketoacidosis (DKA) hospitalizations are climbing in parallel. In the U.S. alone, DKA-related hospital admissions increased by nearly 54% between 2000 and 2014, according to the Agency for Healthcare Research and Quality (AHRQ). The Centers for Disease Control and Prevention’s (CDC) 2023 National Diabetes Statistics Report confirmed over 38 million Americans currently live with diabetes, each carrying inherent DKA risk.

Type 1 diabetes patients face a lifetime DKA risk exceeding 50%. This rising patient pool directly pressures healthcare systems to expand DKA treatment infrastructure. It is pushing demand for intravenous insulin therapies, fluid replacement protocols, and electrolyte management solutions.

Better Symptom Recognition to Propel Early Treatment Uptake

Improved public and clinical education around DKA warning signs, including excessive thirst, fruity breath, and confusion, is prompting speedy diagnosis and treatment initiation. The American Diabetes Association's (ADA) updated 2023 Standards of Care explicitly strengthened DKA screening guidelines for emergency settings.

Campaigns such as the JDRF's ‘Know Your Numbers’ initiative have meaningfully raised awareness among Type 1 patients. Early recognition reduces severe DKA cases, but simultaneously increases the volume of patients entering treatment pathways at mild-to-moderate stages. It is further broadening the addressable treatment window and boosting demand for standardized DKA management protocols.

Restraint - High Entry Barriers to Limit New Treatment Options

Bringing a new DKA therapy to market is neither quick nor cost-effective. Developing a novel insulin or fluid replacement product typically demands extensive clinical trials spanning nearly a decade. Regulatory bodies such as the FDA and the European Medicines Agency (EMA) require rigorous safety and efficacy data before approving any new injectable therapy. It is a process that can, on its own, add 2 to 3 years to launch timelines.

Beyond approvals, manufacturing sterile injectables requires highly specialized facilities that are costly to build and certify. A 2022 FDA guidance document on drug manufacturing quality further tightened sterile production standards, raising compliance costs for new entrants. Established therapies such as Eli Lilly's Humalog carry decades of clinical familiarity. Physicians rarely switch from trusted brands, making market penetration for new alternatives difficult.

Opportunity - Venous Blood Testing to Replace Painful Arterial Sampling

Traditionally, Arterial Blood Gas (ABG) sampling was the standard for monitoring acid-base status in patients with DKA. It is painful, carries an infection risk, and requires skilled handling. Venous Blood Gas (VBG) testing is now emerging as a reliable, less invasive alternative.

A study published in Diabetic Medicine confirmed that venous pH closely correlates with arterial pH in DKA monitoring, making ABG largely unnecessary in routine cases. The American Diabetes Association's 2023 guidelines also acknowledge VBG as an acceptable monitoring method. This shift simplifies care protocols and opens opportunities for point-of-care venous testing devices. It also helps reduce the procedural burden on patients and clinical staff alike.

Telemedicine to Enable Smart Post-Discharge DKA Management

DKA recurrence is a serious problem, often caused by missed follow-ups and poor insulin adherence after discharge. Telemedicine is changing this scenario. Remote monitoring tools allow clinicians to track glucose trends, ketone levels, and medication compliance in real time. A 2020 study in PMC (NCBI) confirmed that telehealth interventions significantly improved glycemic outcomes in high-risk patients with diabetes.

Post-COVID, the Centers for Medicare & Medicaid Services (CMS) permanently expanded reimbursement for remote patient monitoring services. It validated telemedicine as a mainstream care model. For DKA specifically, this creates new opportunities for connected glucose monitors and telehealth platforms targeting frequent hospitalizers.

Category-wise Analysis

Treatment Type Insights

Insulin therapy is expected to be the most preferred treatment type in 2026, with approximately 29.5% of share, as it sits at the core of every DKA treatment protocol. It directly addresses the root cause, i.e., absolute or relative insulin deficiency, by suppressing ketogenesis and restoring normal glucose metabolism. No other therapy can replicate this mechanism. The ADA's 2023 Standards of Care recommends continuous low-dose intravenous insulin infusion as the first-line approach for moderate-to-severe DKA.

Fluid replacement therapy is expected to be the fastest-growing over the forecast period. Severe dehydration is a hallmark of DKA. Patients can lose 3 to 6 liters of fluid before reaching the hospital. Fluid replacement is hence initiated even before insulin in most protocols. What's pushing renewed interest is the ongoing debate around optimal fluid choice. Normal saline has long been standard, but surging evidence links it to hyperchloremic acidosis. Balanced crystalloids such as Lactated Ringer's are gaining clinical preference.

End-user Insights

In 2026, the hospitals segment is expected to account for nearly 76.4%. Moderate-to-severe DKA demands close monitoring. Tasks include arterial or venous blood gases, continuous insulin drips, hourly electrolyte checks, and cardiac monitoring for arrhythmias caused by potassium shifts. This level of care is simply not replicable outside a hospital. ICU admission is required in complicated cases involving altered consciousness or hemodynamic instability. New protocols requiring frequent lab turnarounds and real-time dose titration also keep hospitals central to DKA care.

The home care settings segment is set to rank second. Frequent DKA recurrence, often propelled by poor insulin adherence and delayed symptom recognition, is prompting care teams to extend monitoring beyond hospital walls. Continuous Glucose Monitors (CGMs) such as Dexcom G7 and Abbott's FreeStyle Libre 3 now allow patients to track glucose and receive alerts at home. The Centers for Medicare & Medicaid Services (CMS) permanently expanded remote physiologic monitoring reimbursement codes post-2020, making home-based DKA prevention economically viable for providers.

Regional Insights

North America Diabetic Ketoacidosis Treatment Market Trends

North America is projected to dominate in 2026 by holding a share of about 36.8%, attributed to high diabetes prevalence, well-established healthcare infrastructure, and favorable reimbursement frameworks. The U.S. has one of the highest Type 1 diabetes rates globally. Its hospitals follow rigorously updated DKA protocols from bodies such as the ADA and the Endocrine Society.

Insurance coverage for insulin, CGMs, and hospital stays remains far more structured than in several other regions. The U.S. also leads in clinical trial activity for DKA-related therapies. As of 2024, ClinicalTrials.gov listed over 80 active or recently completed studies on DKA management, reflecting the region's superior research pipeline.

U.S. Diabetic Ketoacidosis Treatment Market Trends

The U.S. outlook remains steady, bolstered by rising Type 1 and insulin-dependent Type 2 diabetes cases. DKA hospitalizations cost the U.S. healthcare system billions annually. It is creating ongoing pressure to improve both acute treatment and preventive strategies. The FDA's accelerated approval of Automated Insulin Delivery (AID) systems, such as Insulet's Omnipod 5, directly reduces DKA risk in high-risk patients while simultaneously expanding the treatment technology ecosystem. The Inflation Reduction Act's insulin pricing cap at US$35/month for Medicare beneficiaries, introduced in 2023, aims to improve access to insulin. It is expected to help prevent DKA triggered by cost-related insulin rationing.

Asia Pacific Diabetic Ketoacidosis Treatment Market Trends

Asia Pacific is anticipated to be the fastest-growing region in the forecast period. The region is witnessing an ongoing diabetes epidemic, particularly across South and Southeast Asia. India and China together account for nearly 40% of global diabetes cases, per the IDF Diabetes Atlas 2023. Historically underdiagnosed, DKA cases are now surfacing more frequently as diagnostic infrastructure improves.

Governments across the region are expanding diabetes care. India's National Program for Non-Communicable Diseases (NP-NCD) has broadened diabetes screening at primary health centers. Surging medical tourism, rising insurance penetration, and the increasing availability of insulin analogs in urban centers are further contributing to the swift adoption of DKA treatment across the region.

China Diabetic Ketoacidosis Treatment Market Trends

China's DKA burden is significant, mainly due to its large population of both Type 1 and Type 2 diabetic patients with ketosis-prone characteristics. Interestingly, local patients with Type 2 diabetes show a relatively higher susceptibility to DKA compared to Western populations, a pattern documented in multiple studies in Journal of Diabetes Investigation.

The government's Healthy China 2030 initiative has prioritized chronic disease management, including diabetes, propelling investment in endocrinology departments and insulin supply chains. Domestic insulin manufacturers such as Gan & Lee Pharmaceuticals are broadening production. They are constantly improving local access to affordable DKA treatment options beyond imported brands.

Japan Diabetic Ketoacidosis Treatment Market Trends

Japan has a well-organized diabetes care system backed by universal health insurance. DKA incidence, while lower than in Western countries due to Japan's lower Type 1 diabetes prevalence, is rising steadily with increasing Type 2 diabetes rates. Japan's Ministry of Health, Labor and Welfare has consistently updated clinical guidelines for diabetes emergencies, including DKA.

The country is also an early adopter of CGM technology. Dexcom and Abbott products hold a superior market presence here. Japan's aging population increases the risk of diabetes-related complications, indirectly sustaining demand for both DKA acute treatment and prevention-focused monitoring tools.

Europe Diabetic Ketoacidosis Treatment Market Trends

Europe benefits from well-established public healthcare systems and high clinical awareness of DKA protocols. The Joint British Diabetes Societies (JBDS) in the U.K. and equivalent bodies across Germany, France, and the Nordics publish regularly updated DKA management guidelines that hospitals strictly follow.

Europe also has a high Type 1 diabetes prevalence, particularly in Scandinavia. Finland has one of the highest Type 1 diabetes rates in the world, per the IDF. The European Medicines Agency (EMA) continues approving new insulin analogs and delivery devices, keeping treatment options current. EU-wide diabetes awareness campaigns further support early detection and treatment of DKA.

U.K. Diabetic Ketoacidosis Treatment Market Trends

The U.K. has one of the more structured DKA management ecosystems globally. The JBDS guidelines, last updated in 2023, are widely regarded as a gold standard for DKA treatment protocols and are followed by NHS hospitals nationally. NHS Digital data shows DKA-related hospital admissions have been rising year-on-year, placing pressure on the system to optimize treatment efficiency.

The NHS also actively funds CGM devices for all Type 1 diabetes patients. It is a policy that both reduces DKA incidence and promotes the adoption of monitoring technology. The U.K.'s sturdy academic research base, mainly at institutions such as Oxford's OCDEM, continues advancing DKA clinical understanding.

Germany Diabetic Ketoacidosis Treatment Market Trends

Germany combines high healthcare spending, constant pharmaceutical manufacturing, and a well-insured population, all of which are favorable for DKA treatment growth. The country’s statutory health insurance (GKV) system covers insulin therapies and monitoring devices comprehensively. It is also a key manufacturing hub for insulin. Sanofi's Frankfurt operations and Novo Nordisk's regional presence ensure strong product availability.

Local hospitals follow S3-level clinical guidelines for diabetes emergencies, demonstrating high standardization of care. Germany's increasing Turkish and Middle Eastern immigrant populations, groups with elevated Type 2 diabetes risk, are contributing to a broad diabetic patient base, sustaining DKA treatment demand.

Competitive Landscape

The global diabetic ketoacidosis treatment market is moderately consolidated. A few large diabetes care companies dominate the market, while regional and generic players compete mainly on pricing and hospital supply contracts. Novo Nordisk, Eli Lilly and Company, and Sanofi are the leading players worldwide. These companies have strong insulin portfolios, large manufacturing capacity, and deep relationships with hospitals and emergency care providers.

The competition is currently centered on quick insulin action, AI-based insulin delivery systems, and continuous glucose monitoring integration. Companies are no longer competing only through insulin products. They are also investing in connected diabetes management platforms. For example, automated insulin delivery systems such as Omnipod 5 and MiniMed 780G are gaining impetus for helping patients manage glucose levels more accurately and reduce severe DKA episodes.

Key Industry Developments:

- In November 2025, researchers from Mahidol University published a systematic review and meta-analysis supporting early subcutaneous basal insulin use alongside intravenous insulin infusion for diabetic ketoacidosis treatment. The findings strengthened clinical evidence for combination insulin therapy in DKA management.

- In May 2025, researchers published the CRABI-DKA study evaluating a new subcutaneous insulin treatment protocol for mild-to-moderate diabetic ketoacidosis. The approach combined rapid-acting and basal insulin therapies to reduce ICU dependency and simplify hospital treatment procedures.

- In May 2025, Sequel Med Tech entered a commercial development agreement with Abbott to integrate Abbott’s future dual glucose-ketone sensor with the twiist automated insulin delivery system. The collaboration aims to improve early ketone detection and reduce the risk of diabetic ketoacidosis in patients with type 1 diabetes.

Companies Covered in Diabetic Ketoacidosis Treatment Market

- Novo Nordisk

- Eli Lilly and Company

- Sanofi

- Pfizer Inc.

- Baxter International Inc.

- B. Braun Melsungen AG

- Hikma Pharmaceuticals

- Teva Pharmaceutical Industries Ltd.

- Fresenius Kabi

- Biocon

Frequently Asked Questions

The global diabetic ketoacidosis treatment market is projected to be valued at US$4.7 billion in 2026.

The diabetic ketoacidosis treatment market is expected to reach US$7.7 billion by 2033.

Shift toward less invasive monitoring and the emergence of home-based early detection platforms are the key market trends.

Insulin therapy is expected to lead with around 29.5% of share in 2026, due to increasing clinical validation of subcutaneous rapid-acting analogs for mild DKA.

The diabetic ketoacidosis treatment market is expected to grow at a CAGR of 7.4% from 2026 to 2033.

Novo Nordisk, Eli Lilly and Company, Sanofi, and Pfizer Inc. are a few key market players.