- Food Ingredients & Additives

- Alternative Proteins Market

Alternative Proteins Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Alternative Proteins Market is segmented by Product Type (Plant-Based Proteins, Microbial Proteins, Insect-Based Proteins, Cell-Based Proteins), End-user (Food & Beverage, Dietary Supplements & Sports Nutrition, Pharmaceutical, Animal Feed, Pet Food, Others), Sales Channel (B2B, B2C), and by Regional Analysis, 2026 - 2033

Alternative Proteins Market Share and Trends Analysis

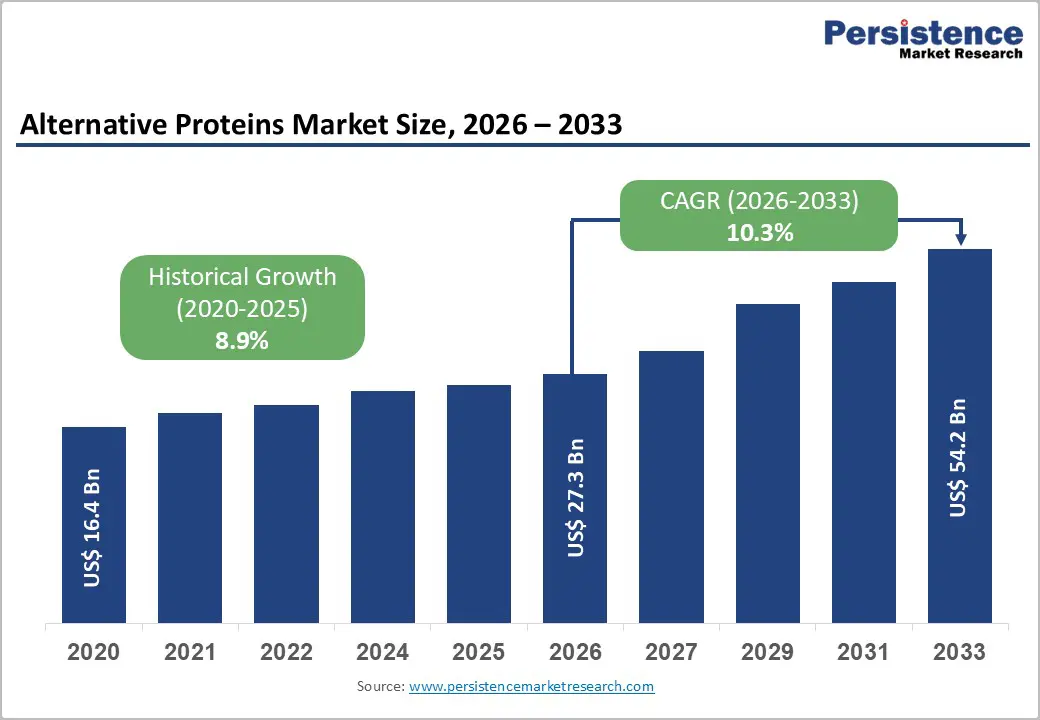

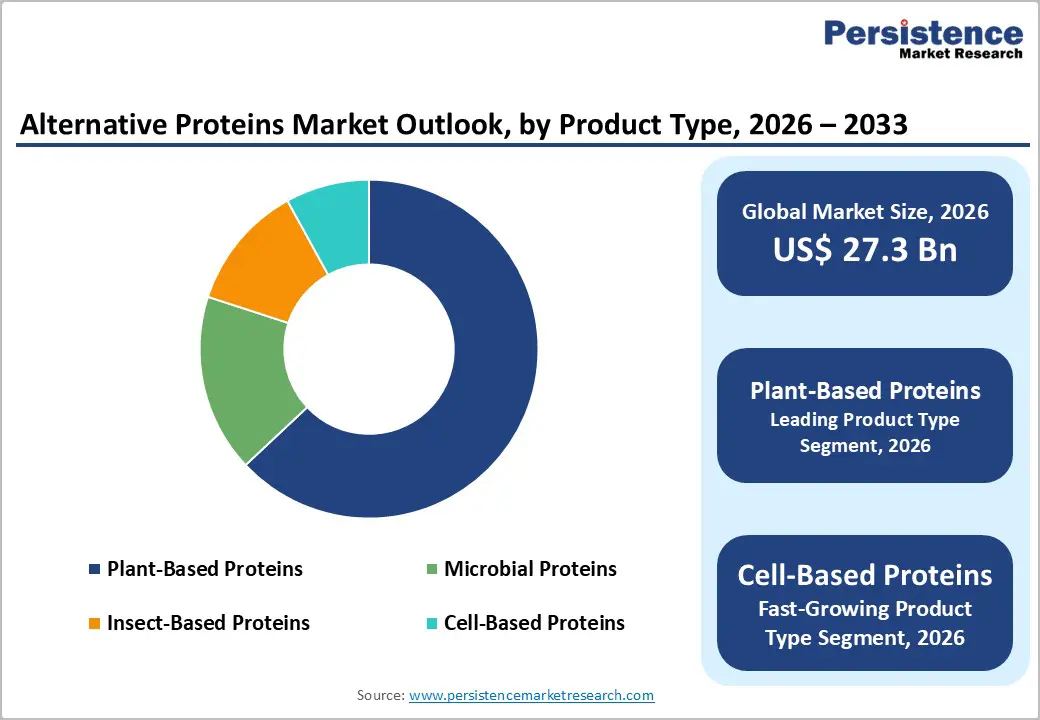

The global alternative proteins market size is expected to be valued at US$ 27.3 billion in 2026 and projected to reach US$ 54.2 billion by 2033, growing at a CAGR of 10.3% between 2026 and 2033.

A systemic global transition toward sustainable food systems and the rising consumer demand for nutrient-dense, ethical protein sources fundamentally drives this acceleration. As the global population approaches 9 billion by 2030, the conventional livestock industry faces significant environmental and logistical constraints. Consequently, investments from both government bodies and multinational food corporations into high-tech protein extraction and fermentation have intensified, creating a robust foundation for long-term market expansion across both developed and emerging economies.

Key Industry Highlights

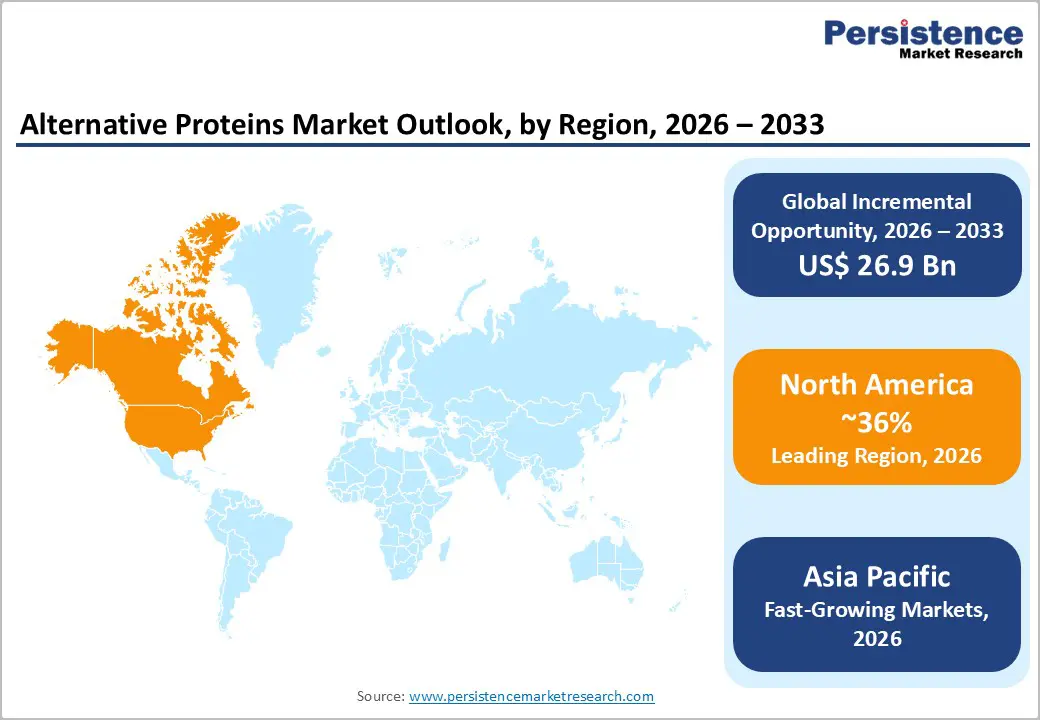

- Leading Region: North America, holding 36% market share, supported by a strong innovation ecosystem, advanced food technology startups, and significant investments from major ingredient companies expanding plant-protein processing and alternative protein product portfolios.

- Fastest-Growing Region: Asia Pacific, driven by rising population, increasing disposable incomes, strong government backing for food security, and expanding production of plant-based protein ingredients derived from pulses and soy.

- Fastest-Growing Product Type Segment: Cell-Based Proteins, gaining momentum with rapid technological advancements, declining production costs, and increasing regulatory approvals for cultivated meat products in markets such as the United States and Singapore.

- Growth Indicators: Increasing global focus on reducing the environmental impact of livestock production is accelerating the adoption of alternative proteins that require significantly lower land, water, and carbon resources compared to conventional animal farming.

- Opportunities: Expanding applications in animal feed and pet food are opening new revenue streams, as insect, microbial, and plant proteins offer sustainable, nutrient-dense alternatives to traditional feed ingredients.

- Key Developments: In March 2026, Louis Dreyfus Company announced the commissioning of its new pea protein isolate production facility in Yorkton, Saskatchewan, Canada. In December 2025, ADM showcased its plant-based protein innovations and functional ingredients at Fi Europe 2025.

| Key Insights | Details |

|---|---|

| Global Alternative Proteins Market Size (2026E) | US$ 27.3 Bn |

| Market Value Forecast (2033F) | US$ 54.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.9% |

Market Dynamics

Driver - Growing Environmental Awareness and Sustainability Mandates

The primary driver for the industry is the increasing global focus on reducing the environmental footprint of protein production. According to the Food and Agriculture Organization (FAO) of the United Nations, livestock farming contributes roughly 14.5% of global greenhouse gas emissions. Alternative proteins, particularly plant-based and microbial variants, offer a drastically reduced environmental impact in terms of land use, water consumption, and carbon emissions. This has led to the implementation of supportive policies such as the European Green Deal, which encourages the adoption of sustainable diets. Major players like ADM and Cargill, Incorporated are responding to these mandates by expanding their plant-processing capacities to meet the demand from eco-conscious consumers who prioritize the planets health alongside their own.

Restraints - Regulatory Hurdles and Consumer Perception Issues

The regulatory landscape for novel proteins, specifically cell-based and insect proteins, is complex and varies significantly by region. For instance, the European Food Safety Authority (EFSA) maintains rigorous Novel Food approval processes that can delay product launches. Additionally, consumer skepticism regarding ultra-processed foods and the ick factor associated with insect-based proteins poses a significant hurdle. Organizations such as the Good Food Institute emphasize the need for transparent labeling and public education to overcome these perceptions. Without a harmonized global regulatory framework and a shift in consumer acceptance, the commercialization of the most innovative segments, such as cell-based meat, may face localized bottlenecks despite their high technological potential.

Opportunity - Expansion into Animal Feed and Pet Food Applications

Cell-Based Proteins represent the fastest-growing segment in terms of potential, with a high projected CAGR through 2033. As research into cellular agriculture matures, there is an immense opportunity to produce real animal meat without the need for slaughter. Recent regulatory approvals in the United States by the FDA and USDA for cultivated chicken have signaled a green light for commercialization. This technology allows for the production of tailored protein profiles and eliminates the risk of zoonotic diseases and antibiotic resistance. Companies that invest in scalable bioreactor technology and affordable growth media will be at the forefront of a revolution that could eventually decouple meat production from industrial livestock farming, capturing a significant share of the global meat market.

Category-wise Analysis

By Product

The plant-based proteins is the leading segment in product type, accounting for a dominant 63% market share in 2025. Its leadership is justified by its long-standing presence, established supply chains, and high consumer familiarity with ingredients such as soy, pea, and wheat. Major food processors like Roquette Frères and Ingredion have perfected extraction techniques that provide excellent functional properties for food applications. Conversely, Cell-Based Proteins is identified as the fastest growing segment through 2033. While currently a niche market, the rapid decline in production costs and increasing regulatory approvals in major markets like the U.S. and Singapore are set to trigger an exponential growth phase as the technology moves from the laboratory to large-scale commercial facilities.

Form Insights

The food & beverage segment holds the leading market share in 2025, as alternative proteins are increasingly integrated into meat analogues, dairy alternatives, and ready-to-eat meals. This segment is the primary engine of the market, driven by retail consumer demand. However, the Pet Food segment is emerging as the fastest-growing end-use category. Pet owners are increasingly concerned about the carbon footprint of their pets' diets and are turning to insect and plant-based kibble to ensure ethical hydration and nutrition. Additionally, the Dietary Supplements & Sports Nutrition channel remains a high-value segment, with companies like IFF providing specialized protein isolates for high-performance powders and bars, catering to a global fitness community that is rapidly moving away from whey-based products.

Region-wise Insights

North America Alternative Proteins Market Trends and Insights

North America is the leading region in the global market, holding a 36% market share in 2025. The region's leadership is underpinned by a highly advanced innovation ecosystem, particularly in the United States and Canada, where the presence of venture-capital-backed startups is the highest in the world. The U.S. Food and Drug Administration (FDA) has been proactive in creating regulatory pathways for novel proteins, including cultivated meat.

Key trends in this region include the rapid mainstreaming of plant-based burgers in fast-food chains and the significant investment by traditional meat giants like Tyson Foods into alternative protein portfolios. Canadian agriculture is also a major contributor, with the government investing heavily in the Protein Industries Canada supercluster to promote pea and pulse processing. The maturity of the B2C retail market and the high concentration of health-conscious consumers in urban centers ensure that North America remains the primary engine for global market value and technological breakthroughs.

Asia Pacific Alternative Proteins Market Trends and Insights

Asia Pacific is identified as the fastest-growing market for alternative proteins through 2032. This rapid expansion is driven by the massive population bases in China and India, combined with rising disposable incomes and a growing middle class that is increasingly aware of food safety and health. The region benefits from a long-standing tradition of plant-based proteins, such as soy and pulses, which provides a strong foundation for modern innovation.

Growth dynamics in China are particularly noteworthy, as the government has included plant-based and cultivated meat in its official five-year agricultural plan for food security. Singapore remains the global living lab for the industry, being the first country to approve the commercial sale of cultivated meat. In India, the focus is on utilizing the country's massive pulse production to create affordable plant-based isolates. The region's manufacturing advantages and the urgent need to feed a growing population sustainably make Asia Pacific the most critical future battleground for global protein producers.

Competitive Landscape

The alternative proteins market is currently a hybrid of consolidated global ingredient giants and a fragmented landscape of high-tech startups. Market leaders like ADM, Cargill, Incorporated, and Ingredion dominate the B2B supply chain, leveraging their massive infrastructure to process plant proteins at scale. These incumbents are increasingly employing acquisition and partnership strategies to integrate innovative technologies from startups like Impossible Foods and Beyond Meat, Inc. Key differentiators for success include the ability to achieve sensory parity and the mastery of extrusion and fermentation technologies. Emerging business models are focusing on hyper-localization, where protein is produced closer to the point of consumption to reduce logistical costs and carbon footprints. As the market matures, we are seeing a shift toward specialized R&D centers that focus on next-generation sources like algae and mycelium.

Key Developments:

- In March 2026, Louis Dreyfus Company announced the commissioning of its new pea protein isolate production facility in Yorkton, Saskatchewan, Canada

- In December 2025, ADM showcased its range of functional ingredients and plant-based proteins at Fi Europe 2025, highlighting innovations that cater to the growing global wellness trend.

- In June 2025, Roquette expanded its NUTRALYS® plant protein portfolio with two new textured solutions, entering the textured wheat segment. The launch highlights the company’s focus on next-generation food innovation and diversified plant-based protein offerings.

Companies Covered in Alternative Proteins Market

- ADM

- Ingredion

- Cargill, Incorporated

- Kerry Group

- Beyond Meat, Inc.

- Tyson Foods

- IFF

- Protix

- Louis Dreyfus Company B.V.

- SunOpta

- Impossible Foods

- Roquette Frères

- Others

Frequently Asked Questions

The global Alternative Proteins market is projected to be valued at US$ 27.3 Bn in 2026.

Growing Environmental Awareness and Sustainability Mandates is a major factor driving the global Alternative Proteins market.

The Global Alternative Proteins market is poised to witness a CAGR of 10.3% between 2026 and 2033.

Expansion into Animal Feed and Pet Food Applications is a significant opportunity in the Alternative Proteins market.

Major players in the Global Alternative Proteins market include ADM, Ingredion, Cargill, Incorporated, Kerry Group, Beyond Meat, Inc., Tyson Foods, IFF, Louis Dreyfus Company B.V., Roquette Frères, and others.