- Power Generation, Transmission, & Distribution

- Digital Substation Market

Digital Substation Market Size, Share, and Growth Forecast, 2026 - 2033

Digital Substation Market by Component (Hardware, Fiber Optic Communication Networks, Others), Substation Type (Transmission Substation, Distribution Substation, Others), Voltage Level, End-user Industry, and Regional Analysis for 2026 - 2033

Digital Substation Market Size and Trends Analysis

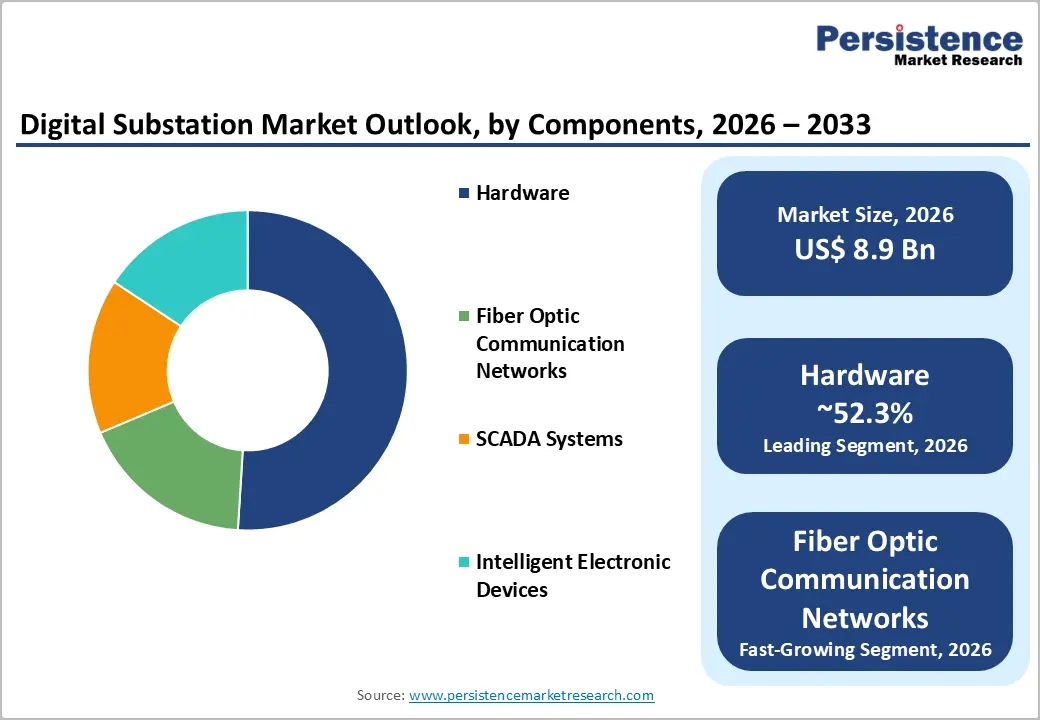

The global digital substation market size is likely to be valued at US$8.9 billion in 2026 and is expected to reach US$14.1 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033, driven by accelerated grid modernization, increasing renewable energy integration, and the transition from conventional substations to IEC 61850-based digital architectures that enhance operational efficiency, visibility, and resilience.

Rising electricity demand and infrastructure investments are driving the adoption of automated, intelligent substations. IEC 61850 standards form the core of digital substations, enabling seamless device interoperability. Advancements in virtualization, software-defined protection, and cybersecurity-focused automation are reducing physical infrastructure needs while improving efficiency and lifecycle performance.

Key Industry Highlights:

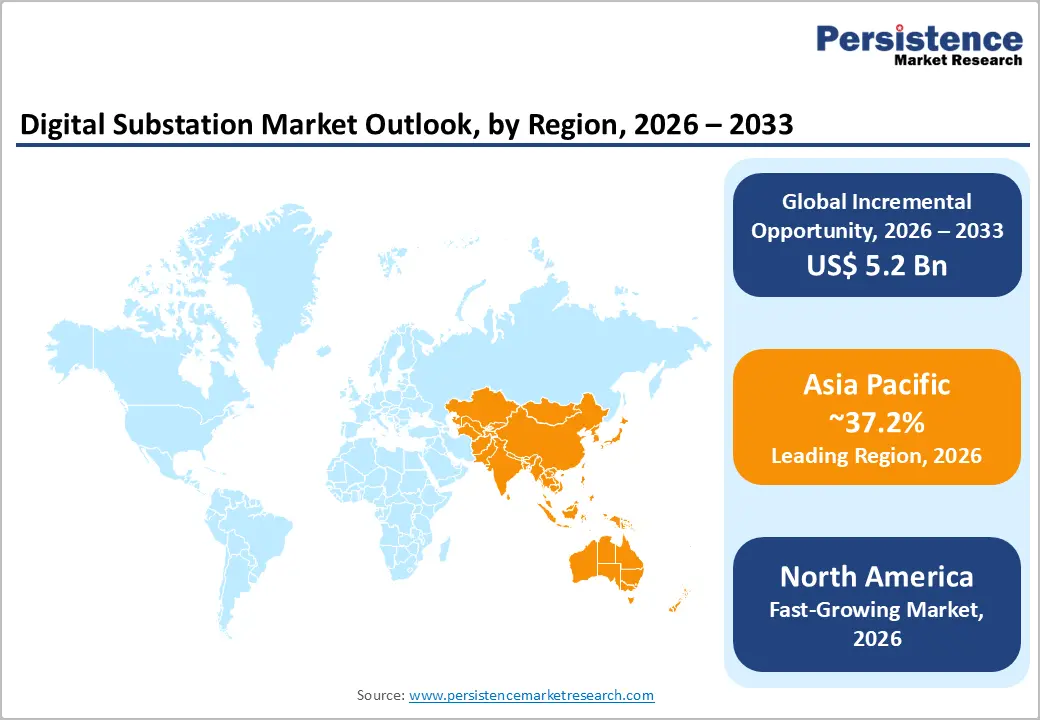

- Leading Region: Asia Pacific is projected to account for approximately 37.2% of the market share, driven by large-scale grid expansion, ultra-high-voltage transmission projects, and strong government-backed infrastructure investments.

- Fastest-growing Region: North America is expected to be the fastest-growing region, supported by increasing investments in grid modernization, resilience enhancement, and digital infrastructure upgrades.

- Investment Plans: Significant investments are being directed toward grid digitalization, renewable energy integration, and cybersecurity infrastructure, with major players expanding manufacturing capabilities and deploying advanced digital substation solutions across high-growth regions such as the Asia Pacific and North America.

- Dominant Components: Hardware is expected to dominate, holding an anticipated 52.3% market share, supported by the critical role of protection systems, relays, and communication devices in ensuring substation reliability and performance.

- Leading Voltage Levels: The 220-500 kV segment is estimated to account for 44.1% market share, driven by its critical role in high-capacity transmission networks, renewable energy evacuation, and interregional power connectivity.

| Key Insights | Details |

|---|---|

| Digital Substation Market Size (2026E) | US$8.9 Bn |

| Market Value Forecast (2033F) | US$14.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.2% |

DRO Analysis

Driver Analysis - Grid Modernization and Rising Electricity Demand

The steady rise in global electricity demand is a primary driver of digital substation adoption. Electrification across sectors, including electric vehicles, industrial automation, and data centers, is placing increasing pressure on transmission and distribution networks. Utilities are investing heavily in grid modernization to ensure reliability, reduce outages, and improve operational efficiency. Digital substations enable real-time monitoring, predictive maintenance, and faster fault detection, making them essential for modern grid infrastructure. This results in sustained demand across new installations, upgrades, and retrofit projects, particularly in developed economies with aging infrastructure.

Renewable Energy Integration and Grid Complexity

The integration of renewable energy sources such as wind and solar is significantly increasing grid complexity. Intermittent generation patterns require advanced monitoring, fast-response mechanisms, and improved coordination among grid components. Digital substations provide enhanced data visibility and control, allowing utilities to manage variable power flows efficiently. The expansion of long-distance transmission networks and cross-border interconnections further amplifies the need for intelligent substations. This trend is driving demand for intelligent electronic devices (IEDs), SCADA systems, and fiber-optic communication networks, which support dynamic and decentralized energy systems.

Adoption of IEC 61850 and Digital Architectures

Standardization through IEC 61850 is accelerating the transition from conventional to digital substations. The standard enables seamless communication between devices, reduces engineering complexity, and enhances system interoperability. Digital architectures significantly reduce copper wiring, physical panels, and installation time, leading to lower capital and operational costs over the lifecycle.

Vendors are increasingly deploying virtualized protection systems and software-defined control platforms, improving scalability and flexibility. This shift is transforming substations into data-driven, intelligent nodes within the broader smart grid ecosystem.

Restraint Analysis - High Upfront Investment and Integration Complexity

Digital substations require substantial initial investment, particularly in retrofit scenarios involving legacy infrastructure. Utilities must replace traditional wiring with fiber-optic systems, integrate new communication protocols, and ensure compatibility across multiple vendors. Engineering complexity and extended project timelines increase implementation risk. In regions with budget constraints or limited technical expertise, adoption may be slower despite long-term cost benefits. This creates a barrier for smaller utilities and emerging markets.

Cybersecurity Risks and Interoperability Challenges

The increased reliance on digital communication and networked devices introduces significant cybersecurity risks. Substations are critical infrastructure assets, making them potential targets for cyberattacks. Ensuring secure communication, data integrity, and system resilience requires continuous investment in cybersecurity solutions. Interoperability issues between devices from different vendors further complicate deployment. Utilities must adopt robust cybersecurity frameworks and standardized protocols, which can increase costs and delay project execution.

Opportunity Analysis - Expansion of High-Voltage Transmission Infrastructure in the Asia Pacific

Asia Pacific represents the largest and most dynamic opportunity for digital substations, driven by large-scale grid expansion and industrial growth. Countries such as China and India are investing heavily in ultra-high-voltage (UHV) transmission networks and in integrating renewable energy. The region accounts for approximately 37.2% of the global market, supported by strong policy frameworks and infrastructure investments. Digital substations play a critical role in managing high-capacity transmission systems, ensuring efficiency, and reducing transmission losses.

Resilience-Focused Upgrades in North America

North America offers significant opportunities in grid modernization and resilience enhancement. Aging infrastructure, extreme weather events, and increasing electricity demand are driving utilities to adopt advanced digital solutions. Investments are focused on improving outage management, strengthening grid reliability, and integrating distributed energy resources. Digital substations enable utilities to achieve these objectives through real-time monitoring, automation, and predictive analytics, making them a key component of modernization strategies.

Digitalization and Decarbonization Initiatives in Europe

Europe’s energy transition policies are creating strong demand for digital substations. Governments are prioritizing renewable energy integration, grid flexibility, and emissions reduction. Digital substations support these goals by enabling efficient energy management and improved system reliability. The adoption of digital twins, advanced analytics, and AI-driven grid management solutions is further enhancing the value proposition of digital substations in the region.

Category-wise Analysis

Components Insights

Hardware is anticipated to account for approximately 52.3% of the market share in 2026, maintaining its dominance due to its critical role in core substation functionality. This segment includes protection relays, merging units, switchgear interfaces, intelligent electronic devices (IEDs), and communication hardware that collectively ensure operational reliability and safety in high-voltage environments.

For instance, ABB Ltd.’s Relion protection relays and Siemens AG’s SIPROTEC series are widely deployed in transmission substations to enable precise fault detection and system protection. In large-scale transmission projects, such as ultra-high-voltage (UHV) grid expansions in China and India, hardware accounts for a substantial share of capital expenditure due to stringent performance, durability, and regulatory compliance requirements.

Fiber optic communication networks are expected to be the fastest-growing component segment, driven by their foundational role in enabling process-bus architectures under IEC 61850 standards. These networks replace traditional copper wiring, delivering higher bandwidth, low latency, improved reliability, and immunity to electromagnetic interference.

For example, Hitachi Energy Ltd integrates fiber-optic-based process bus systems in its digital substation solutions to support real-time data exchange between IEDs, while Schneider Electric SE deploys advanced Ethernet-based communication networks in EcoStruxure Grid platforms. As utilities transition toward fully digital and software-defined substations, fiber infrastructure is becoming indispensable for scalable, secure, and high-speed communication, positioning this segment for sustained high growth.

Voltage Levels Insights

The 220-500 kV segment is anticipated to hold around 44.1% of the market share in 2026, making it the leading voltage category. This dominance is attributed to its critical role in high-capacity transmission networks, including interregional power transfer and the evacuation of renewable energy. Digital substations operating within this voltage range are essential for maintaining grid stability and minimizing transmission losses.

For instance, GE Vernova has deployed advanced grid automation solutions in 400 kV transmission projects, while Hitachi Energy Ltd supports high-voltage digital substations for long-distance power transmission systems. These deployments highlight the importance of digitalization in enhancing operational efficiency and ensuring reliability in large-scale transmission infrastructure.

The Up to 220 kV segment is anticipated to be the fastest-growing, driven by increasing adoption in distribution networks, urban infrastructure, and industrial facilities. This segment benefits from lower implementation costs, modular deployment capabilities, and faster project timelines compared to higher voltage levels.

For example, ABB Ltd.’s compact digital substation solutions are widely used in urban distribution grids, while Schneider Electric SE provides digital substations for industrial campuses and smart city projects. These applications demonstrate how digital substations in the sub-220 kV range are improving grid efficiency, enabling real-time monitoring, and supporting the integration of distributed energy resources at the local level.

Regional Insights

North America Digital Substation Market Trends - Grid Resilience and Cybersecure Modernization Initiatives

North America is a key market characterized by strong investment in grid modernization and resilience, with the U.S. leading regional growth. Aging transmission and distribution infrastructure, rising electricity demand, and increasing frequency of extreme weather events are pushing utilities to upgrade grid systems. Digital substations are central to these efforts, enabling real-time monitoring, predictive maintenance, and faster fault isolation, which directly reduce outage durations and operational risks. Utilities are also integrating renewable energy and distributed energy resources, further increasing the need for intelligent substation architectures.

The regulatory environment continues to support modernization through funding programs and policy frameworks that encourage grid digitization and resilience upgrades. Investment trends show a clear shift toward cybersecure, software-defined, and automated substation solutions. For example, GE Vernova has introduced its GridBeats portfolio to enhance grid orchestration and digital control across North American utilities, improving operational visibility and flexibility.

Siemens AG has also been advancing virtualized protection systems that reduce hardware dependency and lifecycle costs. ABB Ltd has also expanded its digital grid solutions across U.S. utility networks, focusing on resilience and reliability. These developments highlight how leading vendors are aligning with utility priorities, accelerating the adoption of digital substations across the region.

Europe Digital Substation Market Trends - Regulated Energy Transition and Interoperable Grid Digitalization

Europe represents a mature yet evolving market driven by strong regulatory support for energy transition, decarbonization, and digitalization. Countries such as Germany, the U.K., France, and Spain are at the forefront due to their aggressive renewable energy targets and ongoing grid modernization programs. Digital substations are increasingly critical for managing intermittent renewable generation, cross-border electricity flows, and complex grid balancing requirements, ensuring system stability across interconnected markets.

Regulatory harmonization across the European Union is facilitating the adoption of standardized technologies such as IEC 61850, enabling interoperability and reducing deployment complexity. Investments are concentrated on retrofitting aging infrastructure, integrating offshore wind and solar capacity, and enhancing energy efficiency.

For instance, Hitachi Energy Ltd has been actively deploying digital substation solutions across European transmission networks, supporting renewable integration and grid flexibility. Schneider Electric SE is advancing its EcoStruxure Grid platform to enable digital monitoring and control for utilities, while Siemens AG continues to expand its digital twin and automation capabilities for substations. These developments are strengthening Europe’s position as a technology-driven market focused on sustainability and grid intelligence.

Asia Pacific Digital Substation Market Trends - Large-Scale Infrastructure Expansion and UHV-Driven Growth

Asia Pacific is expected to dominate, accounting for approximately 37.2% of global share in 2026, supported by rapid industrialization, urbanization, and large-scale infrastructure investments. China, Japan, and India are the primary growth engines, with extensive deployment of transmission and distribution networks to support economic expansion and rising electricity demand. The region is also leading in ultra-high-voltage (UHV) transmission projects, which require advanced digital substation technologies for efficient operation and grid stability.

The region benefits from strong manufacturing ecosystems, government-backed infrastructure programs, and increasing renewable energy capacity. Investments in smart grids and digital substations are accelerating to support large-scale renewable integration and improve grid reliability. For example, Hitachi Energy Ltd has been involved in supplying advanced GIS and digital substation technologies for UHV projects in China, enabling efficient long-distance power transmission.

GE Vernova has expanded its electrification manufacturing and engineering capabilities in India to support growing grid demand, while Siemens AG has partnered on digital substation deployments in Australia, integrating cloud-based grid simulation and automation. These developments illustrate how large-scale infrastructure expansion and technological adoption are reinforcing Asia Pacific’s leadership in the global digital substation market.

Competitive Landscape

The global digital substation market is moderately consolidated, with leading players accounting for a significant share of global revenue. Major companies leverage their technological expertise, global presence, and strong customer relationships to maintain a competitive advantage. The presence of numerous regional and niche players contributes to a competitive and dynamic market environment.

Market leaders are focusing on digital transformation, software-defined solutions, and lifecycle service models. Key strategies include investment in R&D, expansion into emerging markets, and the development of cybersecurity-focused solutions. Companies are also emphasizing partnerships and localization to enhance competitiveness.

Key Industry Developments:

- In February 2026, GE Vernova announced an expansion of its grid automation manufacturing and R&D facilities in South Carolina, focusing on intelligent substation systems and digital protection technologies to strengthen domestic supply and innovation capabilities.

- In January 2026, Hitachi Energy Ltd. secured a contract to deploy IEC 61850-based digital substation automation solutions for a large utility modernization project in Texas, accelerating the transition toward intelligent and efficient grid operations.

Companies Covered in Digital Substation Market

- ABB Ltd

- Siemens AG

- Hitachi Energy Ltd.

- Schneider Electric SE

- GE Vernova

- Eaton Corporation

- Schweitzer Engineering Laboratories

- S&C Electric Company

- Toshiba Corporation

- Mitsubishi Electric Corporation

- Fuji Electric Co., Ltd.

- NR Electric Co., Ltd.

- Hyundai Electric & Energy Systems Co., Ltd.

- Cisco Systems, Inc.

- General Electric Company

- Larsen & Toubro Limited

Frequently Asked Questions

The digital substation market is estimated to be valued at US$8.9 billion in 2026.

The digital substation market is projected to reach US$14.1 billion by 2033.

Key trends include the adoption of IEC 61850-based architectures, increasing deployment of fiber optic communication networks, growing focus on software-defined and virtualized substations, and rising emphasis on cybersecurity and grid resilience.

The hardware segment is the leading component category, accounting for approximately 52.3% of the market share, supported by strong demand for protection systems, relays, and communication devices.

The digital substation market is expected to grow at a CAGR of 6.8% from 2026 to 2033.

Major players include ABB Ltd, Siemens AG, Hitachi Energy Ltd, Schneider Electric SE, and GE Vernova.