- Healthcare Services

- AI in Clinical Trials Market

AI in Clinical Trials Market Size, Share, and Growth Forecast 2026 - 2033

AI in Clinical Trials Market by Component (Software, Services), by Technology (Machine Learning, Natural Language Processing (NLP), Deep Learning, Others), by Application (Patient Recruitment, Clinical Trial Design, Data Management & Monitoring, Safety Monitoring, Others), by End User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations (CROs), Academic & Research Institutes), and Regional Analysis, 2026 - 2033

AI in Clinical Trials Market Share and Trends Analysis

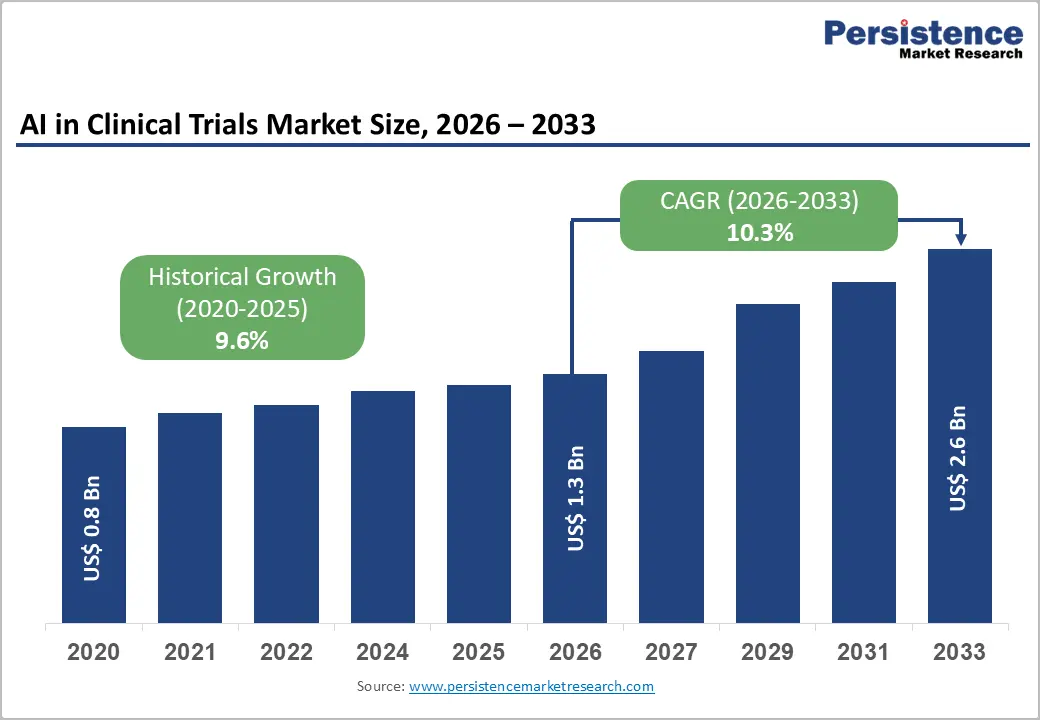

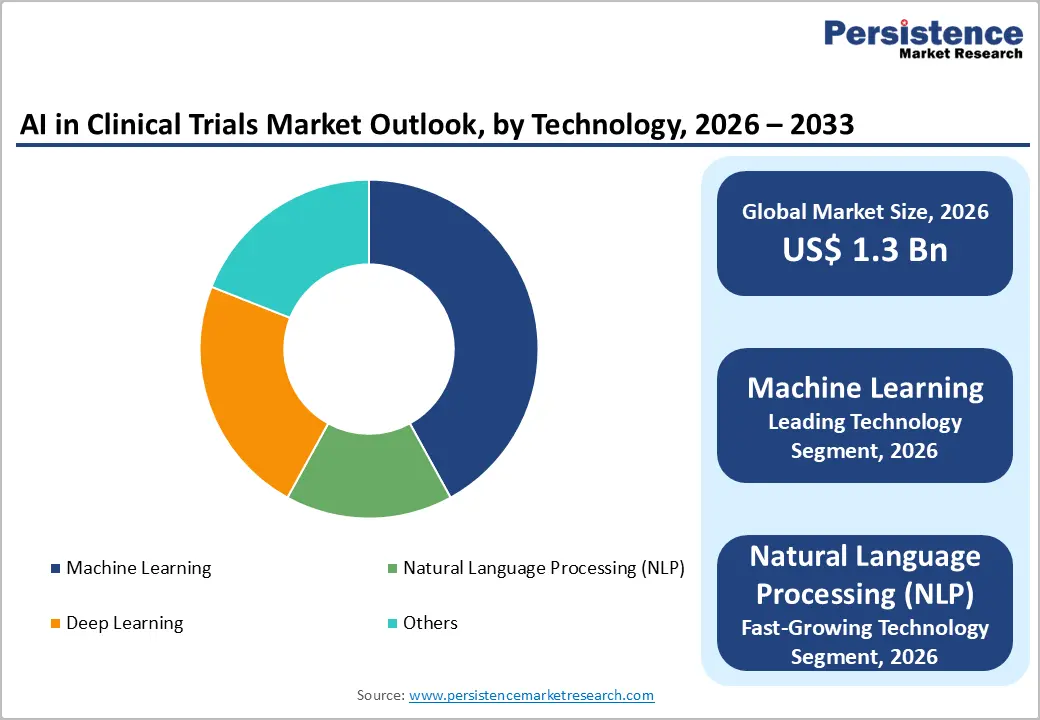

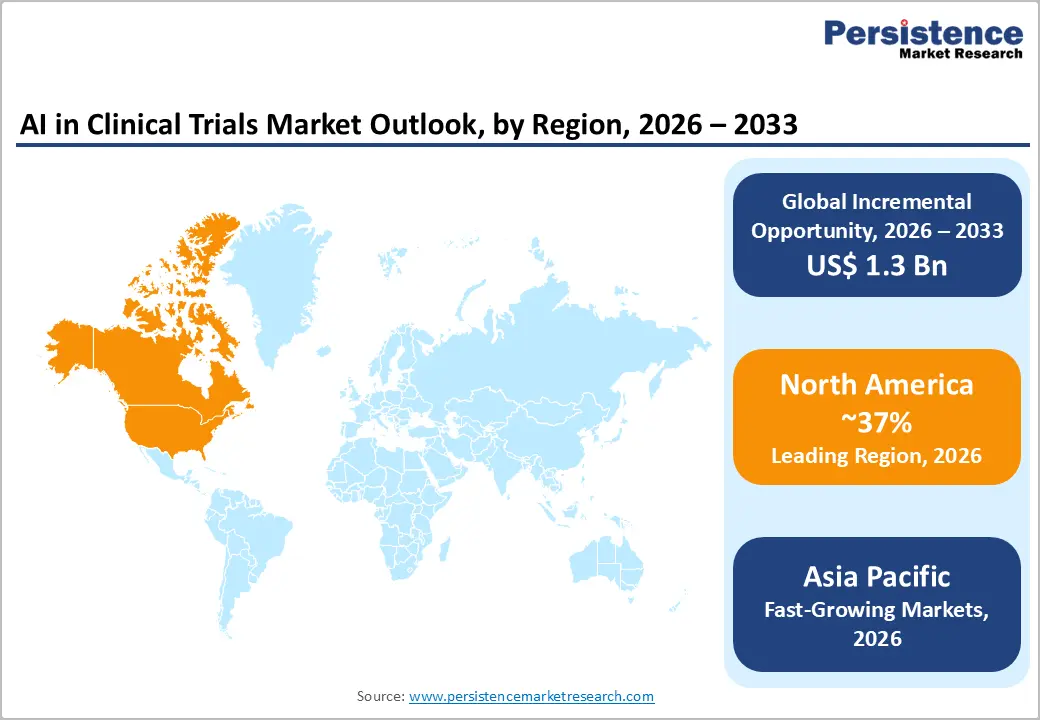

The global AI in clinical trials market size is expected to be valued at US$ 1.3 billion in 2026 and projected to reach US$ 2.6 billion by 2033, growing at a CAGR of 10.3% between 2026 and 2033.

The market expansion is propelled by the escalating complexity of clinical trial protocols and the urgent need to reduce development timelines, particularly as AI-powered patient recruitment tools have demonstrated the capacity to improve enrollment rates by up to 65% according to industry benchmarks published in 2026. Additionally, the FDA qualified its first AI drug development tool AIM-NASH in December 2025, signaling regulatory endorsement that validates AI's transformative potential to accelerate medical product development while maintaining rigorous safety and efficacy standards.

Key Industry Highlights:

- North America maintains a dominant regional position, capturing 37% market share in 2025, anchored by the United States' concentration of leading pharmaceutical enterprises, sophisticated innovation ecosystems, and progressive FDA regulatory frameworks that qualified the first AI drug development tool, AIM-NASH, in December 2025.

- Asia Pacific emerges as the fastest-growing regional market driven by substantial populations in China, India, and Japan, deliberate regulatory reforms encouraging clinical trial activity, and the region's hosting of 54% of global clinical trials planned in 2022.

- Machine learning technology dominates with 42% market share in 2025, reflecting proven track records across site selection optimization, patient stratification, and protocol feasibility analysis.

- Natural language processing represents the fastest-growing technology segment as organizations recognize the transformative potential for mining unstructured clinical narratives.

- Strategic expansion into Asia Pacific clinical trial infrastructure presents compelling growth opportunities as Japan's healthcare AI sector projects growth from USD 265 million in 2021 to USD 1,870 million by 2030.

| Key Insights | Details |

|---|---|

|

AI in Clinical Trials Market Size (2026E) |

US$ 1.3 billion |

|

Market Value Forecast (2033F) |

US$ 2.6 billion |

|

Projected Growth CAGR (2026-2033) |

10.3% |

|

Historical Market Growth (2020-2025) |

9.6% CAGR |

Market Dynamics

Drivers - Accelerated Drug Development Timelines Through AI-Enhanced Trial Efficiency

The pharmaceutical industry faces mounting pressure to compress drug development cycles, which traditionally span 10-15 years and cost billions of dollars while maintaining failure rates exceeding 90% in conventional discovery approaches. Artificial intelligence has emerged as a transformative solution, with early evidence demonstrating AI's capacity to slash development times by approximately half according to analyses published in 2025. AI-discovered molecules have achieved 80-90% success rates in Phase I trials, substantially surpassing the historical average of 52% for traditional methods as documented in comprehensive industry reviews. The FDA Modernization Act 3.0, reintroduced in April 2025, further accelerates preclinical timelines by encouraging alternatives to animal testing, while the NIH announced in July 2025 that research proposals must integrate validated human-relevant methods. Predictive analytics models now achieve approximately 85% accuracy in forecasting trial outcomes and site performance risks, enabling sponsors to optimize resource allocation and mitigate execution risks proactively. This convergence of technological capability and regulatory support creates compelling economic incentives for pharmaceutical companies to integrate AI-powered solutions throughout the clinical development lifecycle.

Transformation of Patient Recruitment and Retention Paradigms

Patient recruitment remains the most critical bottleneck constraining clinical trial execution, with 10-30% of activated sites failing to enroll any participants and traditional manual matching processes proving increasingly inadequate for complex trial protocols. AI-powered patient matching systems have revolutionized this landscape, as demonstrated by Mayo Clinic's deployment of IBM Watson for Clinical Trial Matching, which achieved measurably higher enrollment in breast cancer clinical trials following implementation in 2024. Industry benchmarks published in 2026 confirm that AI-powered recruitment tools improve enrollment rates by up to 65% while reducing screen failures through precision matching algorithms. Natural language processing technologies extract structured information from unstructured electronic health records with remarkable efficiency, enabling automated identification of eligible candidates across vast patient databases. The Clinical Program Productivity Index (CPPI) rose to 11.7 in 2024 from 10.9 in 2023, signaling marked improvement in clinical productivity driven substantially by data-centric strategies. As clinical trials increasingly target specialized indications and rare disease populations, AI's capacity to rapidly identify and engage eligible participants within diverse demographic groups has become indispensable for maintaining competitive enrollment timelines and achieving adequate statistical power.

Restraints - Data Quality and Interoperability Challenges Impeding Comprehensive AI Deployment

The effectiveness of AI algorithms in clinical trial applications fundamentally depends on access to high-quality, standardized datasets, yet pharmaceutical organizations grapple with fragmented data architectures and inconsistent data capture methodologies across research sites. Manual data entry errors exceed 28% in some studies according to research on clinical registry construction, while inter-rater reliability demonstrates considerable variability that undermines AI model training. Healthcare data remains trapped in proprietary electronic health record systems with limited interoperability, preventing seamless integration required for real-time monitoring and predictive analytics. The absence of universally adopted data standards across therapeutic areas forces sponsors to invest extensively in data cleaning and harmonization efforts before AI tools can generate reliable insights. Furthermore, retrospective clinical datasets often lack the longitudinal depth and comprehensive phenotypic characterization necessary for training sophisticated deep learning models, particularly for rare disease indications where patient cohorts are inherently limited. These structural impediments constrain the scalability of AI implementations and prolong the validation timeline for novel algorithms seeking regulatory acceptance.

Regulatory Uncertainty and Algorithm Transparency Requirements

Despite progressive guidance from regulatory authorities including the FDA's draft guidance issued in January 2025 titled "Considerations for the Use of Artificial Intelligence to Support Regulatory Decision-Making for Drug and Biological Products," sponsors face persistent uncertainty regarding acceptable AI standards for marketing authorization submissions. The EMA's Reflection Paper published in October 2024 emphasizes risk-based approaches for AI deployment throughout the medicinal product lifecycle, yet practical interpretation of these frameworks remains ambiguous for sponsors navigating late-stage applications. Algorithm transparency presents particular challenges, as proprietary machine learning models rely on complex neural network architectures that resist straightforward explanation of decision-making processes demanded by regulatory reviewers. The EU AI Act introduces four risk classification levels for AI systems in clinical research, creating additional compliance complexity for multinational trials spanning both European and North American jurisdictions. Industry stakeholders have noted that greater clarity is needed from medicines regulators to guide sponsors over acceptable AI applications that satisfy regulatory requirements, as evidenced by modest AI utilization for clinical outcomes analysis documented in systematic reviews. This regulatory ambiguity constrains sponsors' willingness to invest aggressively in AI capabilities, while questions persist regarding validation standards and post-market surveillance obligations for continuously learning algorithms.

Opportunities - Expansion into Natural Language Processing for Unstructured Clinical Data Mining

Natural language processing represents a particularly promising growth frontier as clinical trials generate vast quantities of unstructured textual data, including physician notes, adverse event narratives, patient-reported outcomes, and regulatory correspondence that remain underutilized for signal detection and decision-making. Advanced NLP techniques have progressed beyond simple text classification to facilitate extraction of nuanced clinical insights from narrative documentation, enabling automated risk-based quality management workflows that replace labor-intensive manual review processes. The technology's capacity to parse feedback, comments, and free-text entries captured across multiple systems unlocks previously inaccessible intelligence for compliance monitoring, safety surveillance, and protocol deviation analysis throughout the trial lifecycle.

Recent implementations demonstrate NLP's effectiveness in automating case processing for pharmacovigilance, extracting relevant information from medical literature and digital platforms to ensure faster adverse event monitoring while reducing manual workload. As regulatory authorities increasingly emphasize data-driven decision-making, NLP applications for literature extraction and biomarker identification from scientific publications position sponsors to accelerate drug repurposing initiatives and validate hypotheses with published evidence. The convergence of large language models with healthcare-specific training datasets promises to democratize access to sophisticated NLP capabilities, enabling smaller biotechnology firms and academic medical centers to leverage computational linguistics for investigator-initiated studies without requiring extensive in-house data science expertise.

Strategic Positioning for Asia Pacific Clinical Trial Expansion

The Asia Pacific region has crystallized as the fastest-growing market for AI-enabled clinical trial solutions, hosting 54% of global clinical trials planned in 2022 and maintaining this leadership position through 2025 according to multinational trial activity tracking. Countries including China, Japan, India, and Australia are implementing regulatory reforms specifically designed to attract clinical research while encouraging adoption of advanced technologies, including AI to accelerate trial approvals and improve operational efficiency. Japan's healthcare AI sector reached USD 265 million in 2021, with projections to achieve USD 1,870 million by 2030 at a 21.7% CAGR, reflecting systematic government investment through the "Society 5.0" initiative aimed at establishing AI-enhanced hospital networks nationwide.

The region's substantial and genetically diverse populations provide critical advantages for multinational trial enrollment, particularly as protocols increasingly target specialized indications and patient subpopulations requiring large candidate pools. Lokavant Holdings secured $8 million in strategic investment from Mitsui & Co. in 2024 specifically to expand AI-optimized clinical trial platforms across Asia Pacific, exemplifying growing capital allocation toward regional infrastructure. As pharmaceutical companies confront intensifying pressure to compress development timelines while controlling costs, Asia Pacific's combination of supportive regulatory frameworks, manufacturing cost advantages, and sophisticated digital health ecosystems positions the region as an indispensable partner for AI-powered trial execution strategies extending through the decade.

Category-wise Insights

Component Insights

Software solutions dominate the component landscape, capturing approximately 48% market share in 2025 as pharmaceutical and biotechnology companies prioritize investments in AI-powered platforms for electronic data capture, patient recruitment matching, and predictive analytics. The software segment's leadership stems from its capacity to deliver immediate operational value through cloud-based deployment models that minimize upfront capital expenditure while enabling rapid scalability across multiple trial sites simultaneously.

Electronic data capture platforms account for approximately 45% of market activity within the software category according to regional analyses, driven by the rising complexity of clinical data and imperative for real-time insights that traditional manual systems cannot accommodate. Medidata Solutions, a Dassault Systèmes brand, exemplifies this trend through its AI-powered Clinical Trial Management System that has scaled across 500 clinical studies in the last decade, including more than 120 AI-supported studies initiated in 2025 alone.

The software segment benefits from continuous enhancement of machine learning algorithms and integration with wearable devices for remote monitoring, positioning vendors to capture recurring subscription revenue while establishing technology lock-in effects. Services encompass consulting, implementation support, algorithm customization, and managed analytics offerings that complement software deployments, particularly valuable for smaller biotechnology firms lacking internal data science capabilities required to operationalize sophisticated AI tools effectively across their clinical development portfolios.

End User Insights

Pharmaceutical and biotechnology companies represent the dominant end-user segment, generating approximately 52% of revenue in 2025 as large integrated organizations invest heavily in proprietary AI capabilities to gain competitive advantages in drug development efficiency and portfolio optimization. These enterprises maintain substantial internal data science teams and possess the financial resources required to license comprehensive AI platforms while developing specialized algorithms tailored to their therapeutic focus areas and compound libraries.

Insilico Medicine's AI-designed candidate Rentosertib approaching Phase III trials following positive Phase IIa results published in Nature Medicine during June 2025 exemplifies how innovative biotechnology companies leverage AI throughout the drug development cascade from target identification through clinical validation. Contract research organizations emerge as the fastest-growing end user category, expanding at 26% CAGR through 2032 as these service providers amortize AI tool development costs across multiple client sponsors to achieve economies of scale impossible for individual companies to replicate.

CROs package turnkey AI platforms within global site networks, enabling rapid deployment cycles and offering compelling value propositions for sponsors seeking to externalize clinical development risks while accessing best-in-class technological capabilities.

The Boston Consulting Group estimates that advanced technology adoption including AI could disrupt approximately US$18 billion or 40% of current CRO value pools spanning clinical monitoring, project management, and patient recruitment through productivity improvements and radical speed enhancements. Academic and research institutes represent stable user groups exploiting AI primarily for investigator-initiated studies and translational research applications, contributing to algorithm validation efforts and publishing peer-reviewed evidence that builds broader stakeholder confidence in AI reliability for regulatory decision-making contexts.

Regional Insights

North America AI in Clinical Trials Market Trends and Insights

North America leads the AI in clinical trials market driven by a mature pharmaceutical and biotechnology ecosystem, strong R&D investments, and early adoption of advanced digital tools. The United States, in particular, accounts for a substantial share of global AI clinical trial activity, supported by favorable regulatory frameworks and proactive initiatives from agencies like the FDA that encourage integration of AI in trial design, patient recruitment, data analytics, and real-world evidence generation.

The widespread availability of electronic health records and large patient databases in North America further enhances the region’s ability to deploy predictive models and machine learning solutions effectively. Strong collaboration between academic institutions, technology companies, and life sciences organizations accelerates innovation, while decentralized trial models and wearable technologies create new opportunities for AI to improve trial efficiency and outcomes. As a result, North America continues to expand its lead, with ongoing digital transformation reinforcing its dominant position in the global AI in clinical trials landscape.

Asia Pacific AI in Clinical Trials Market Trends and Insights

Asia Pacific is rapidly emerging as a key growth region in the AI in clinical trials market, driven by expanding pharmaceutical R&D, large and diverse patient populations, and increasing investments in healthcare digitalization. Countries like China, India, Japan and South Korea are witnessing a notable rise in clinical trial activity, which in turn fuels demand for AI technologies to optimize patient recruitment, enhance data management, accelerate trial design and improve real-time monitoring.

Government support through favorable policies, healthcare infrastructure upgrades, and collaboration between local research institutions and global technology providers further strengthen regional growth. The cost-efficiency of conducting trials in Asia Pacific compared with Western countries, coupled with high unmet medical needs from chronic and rare diseases, attracts both domestic and international sponsors to adopt AI-driven solutions. As a result, Asia Pacific is projected to record one of the highest compound annual growth rates globally, positioning it as a fast-expanding hub for AI-enabled clinical research.

Competitive Landscape

The AI in clinical trials market exhibits a moderately fragmented competitive structure characterized by diverse participants ranging from established healthcare information technology vendors and large pharmaceutical service providers to specialized AI-focused biotechnology startups developing innovative algorithms for specific applications. Market leaders pursue differentiation strategies emphasizing comprehensive platform capabilities spanning multiple trial lifecycle stages, proprietary datasets enabling superior algorithm training, and established relationships with regulatory authorities that facilitate client navigation of approval processes.

Technology vendors increasingly emphasize cloud-native architectures and application programming interface ecosystems that enable seamless integration with sponsor electronic data capture systems and clinical trial management platforms, reducing implementation friction while creating switching costs through data accumulation effects. Strategic partnerships between pharmaceutical companies and AI specialists have intensified dramatically, with deals in AI-driven drug discovery surging 14-fold from 2019 to 2023 reaching $12.8 billion in transaction value, reflecting industry conviction that computational approaches will fundamentally reshape competitive dynamics. Contract research organizations aggressively invest in proprietary AI capabilities to differentiate service offerings and improve operational margins, with major players including IQVIA leveraging vast proprietary datasets combining claims records, electronic medical records, and longitudinal patient information to train predictive models unavailable to competitors lacking comparable data assets. Emerging business model trends include consumption-based pricing aligned with client value realization, outcome-based contracting where vendors assume partial execution risk, and platform-as-a-service architectures enabling sponsors to customize algorithms for proprietary applications while benefiting from vendor-managed infrastructure and continuous model enhancement.

Key Developments:

- In March 2026, Scott Weidley introduced an AI-powered clinical trial build platform within the Captivate® system developed by ClinCapture. The platform embedded artificial intelligence directly into the architecture of clinical trial design, enabling sponsors and contract research organizations to automatically generate and configure major parts of a study using structured protocol specifications.

- In February 2026, Evinova announced a strategic collaboration with Bristol Myers Squibb to optimize clinical development using artificial intelligence. Under the agreement, Bristol Myers Squibb planned to deploy Evinova’s AI-native clinical development platform, including the Study Designer and Cost Optimizer modules, across its global clinical trial portfolio.

- In October 2025, Thermo Fisher Scientific and Lundbeck announced separate collaborations with OpenAI to advance the use of artificial intelligence in drug development and clinical research. Thermo Fisher integrated OpenAI APIs into its Accelerator Drug Development platform and its PPD clinical research operations to improve clinical trial efficiency, shorten development timelines, and help identify drug candidates that are less likely to succeed early in the process, enabling better allocation of resources toward promising therapies.

Companies Covered in AI in Clinical Trials Market

- Exscientia Ltd.

- IBM Watson Health

- Insilico Medicine, Inc.

- IQVIA Holdings Inc.

- Medidata Solutions (Dassault Systèmes)

- AiCure LLC

- Antidote Technologies, Inc.

- Saama Technologies, Inc.

- Owkin Inc.

- Deep 6 AI

- Phesi

- Unlearn.ai Inc.

- Recursion Pharmaceuticals

- Iambic Therapeutics

- Absci Corporation

- Lokavant Holdings

- Caidya

Frequently Asked Questions

The global AI in clinical trials market is expected to be valued at US$ 1.3 billion in 2026, driven by pharmaceutical companies' escalating investments in artificial intelligence capabilities.

The market is propelled by AI's demonstrated capacity to slash drug development times by approximately half while AI-discovered molecules achieve 80-90% success rates in Phase I trials.

North America commands 37% market share in 2025, anchored by the United States' concentration of leading pharmaceutical enterprises and progressive FDA regulatory frameworks.

Strategic positioning for Asia Pacific clinical trial expansion presents compelling opportunities as the region hosts 54% of global clinical trials planned in 2022.

Key market players include Exscientia Ltd., IBM Watson Health, Insilico Medicine, Inc., IQVIA Holdings Inc., Medidata Solutions (Dassault Systèmes).