- Bulk Chemicals

- Synthetic Gypsum Market

Synthetic Gypsum Market Size, Share, and Growth Forecast 2026 - 2033

Synthetic Gypsum Market by Product Type (Flue Gas Desulfurization Gypsum, Citrogypsum, Fluorogypsum, Phosphogypsum, Others), End-use (Cement, Drywall, Plaster, Soil Amendments, Others), by Regional Analysis, 2026 - 2033

Synthetic Gypsum Market Size and Trend Analysis

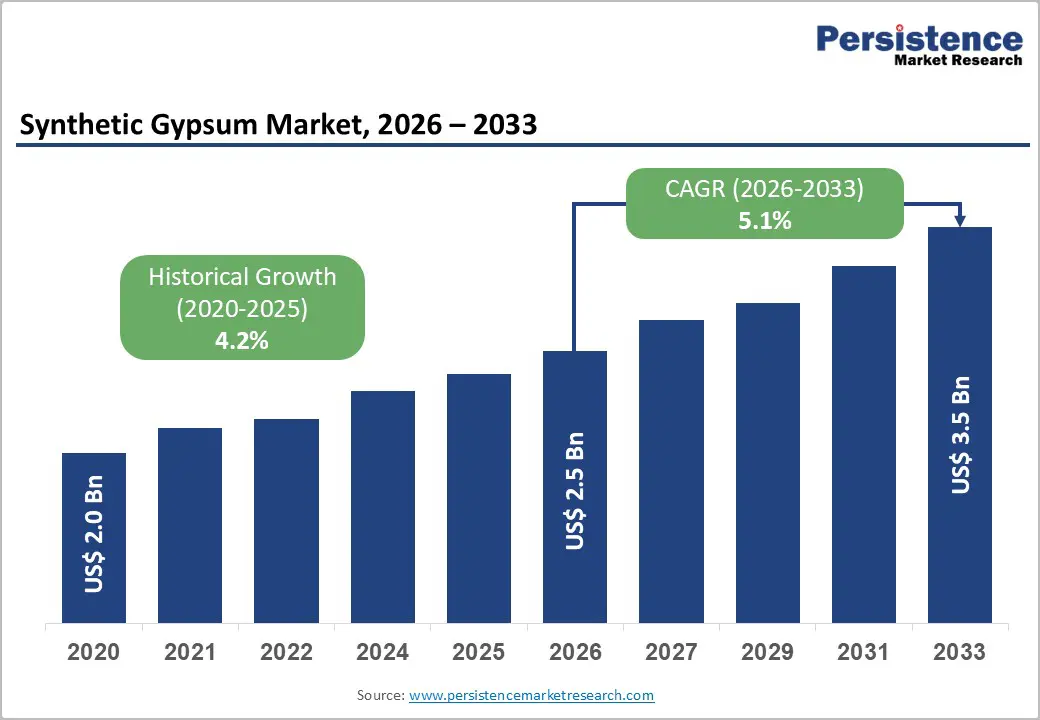

The global synthetic gypsum market size is expected to be valued at US$ 2.5 billion in 2026 and projected to reach US$ 3.5 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

This consistent growth is driven by the expanding global construction industry's demand for sustainable building materials, the progressive phase-out of natural gypsum mining in favor of industrial byproduct use, and circular economy policies mandating industrial waste valorization across major economies.

Key Industry Highlights

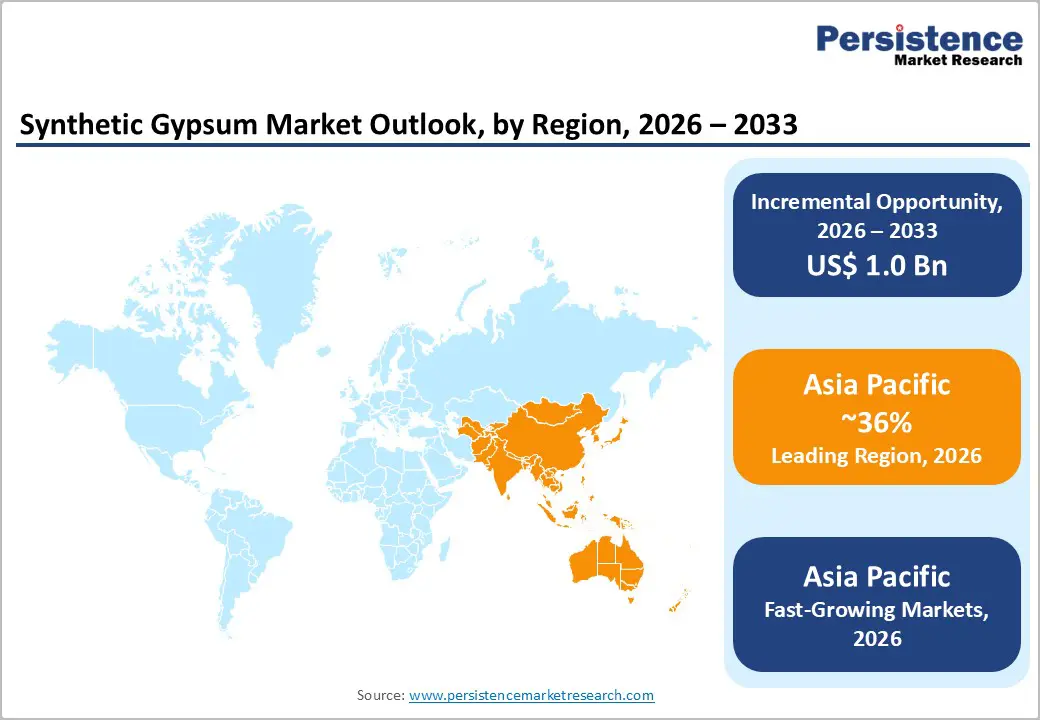

- Leading Region: Asia Pacific commands ~36% global synthetic gypsum market share in 2026, led by China's 58% intra-regional dominance through its massive coal FGD gypsum production, integrated drywall manufacturing base, and GCCA-documented cement sector consuming over 4 billion tons annually.

- Fastest Growing Region: MEA is the fastest growing synthetic gypsum region through 2026–2033, driven by GCC construction mega-projects under Vision 2030, growing drywall adoption replacing traditional plaster in modern construction, and expanding FGD gypsum availability from Gulf power plant desulfurization programs.

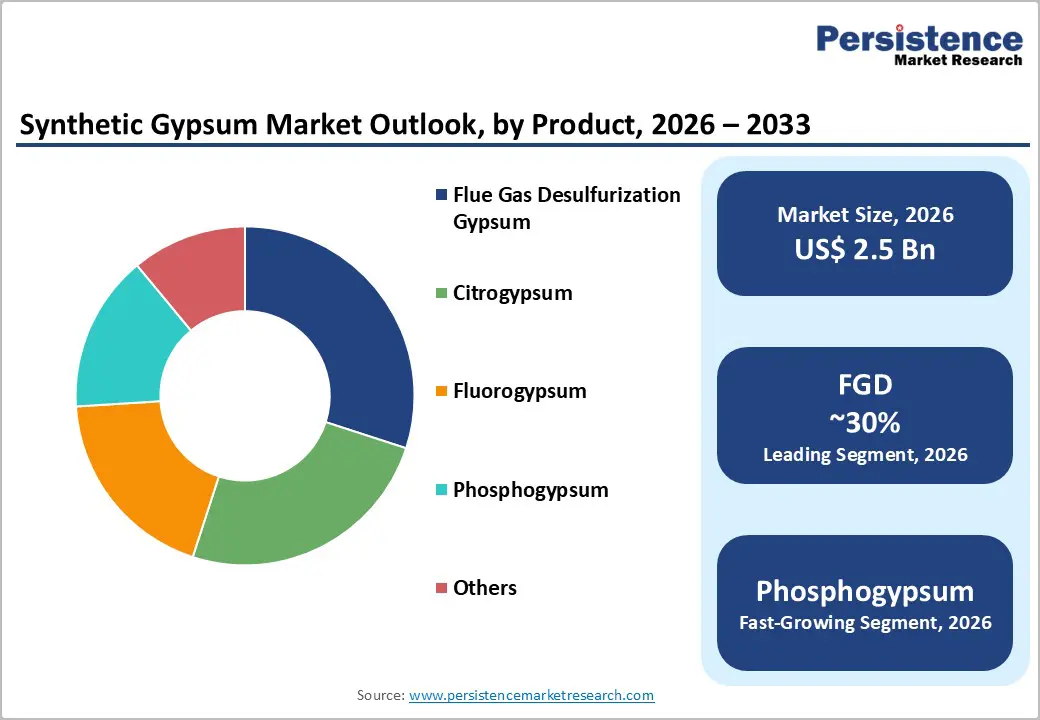

- Dominant Segment: FGD gypsum holds ~30% product type market share in 2026, dominating through 95%+ calcium sulfate purity exceeding natural gypsum quality, ACAA-documented 18+ million tonne U.S. annual beneficial use, and regulatory-mandated coal power plant SO2 scrubbing ensuring continuous supply generation.

- Fastest Growing Segment: Phosphogypsum is the fastest growing segment at ~8% CAGR (2026–2033), driven by Brazil's millions-of-hectare soil amendment programs, IPNI-documented agricultural productivity improvements, and growing regulatory acceptance in India and Australia for broader agricultural application.

- Key Opportunity: USGBC's 100,000+ LEED-certified buildings globally and BREEAM Mat 03 recycled content credits are creating premium demand for FGD gypsum-based synthetic wallboard, enabling above-average margin realization for certified synthetic gypsum wallboard producers meeting green building documentation standards.

DRO Analysis

Drivers - Global Construction Boom Driving Drywall and Cement Demand for Synthetic Gypsum

The expanding global construction industry is the primary demand driver for synthetic gypsum, as drywall (wallboard) and cement production represent the two largest end-use applications consuming synthetic gypsum at industrial scale. According to the Global Cement and Concrete Association (GCCA), global cement production exceeds 4 billion tons annually, with gypsum added at 3–5% by weight as a setting retarder, creating enormous baseload demand for synthetic gypsum in markets where FGD production is plentiful.

The U.S. Geological Survey (USGS) documents synthetic gypsum, predominantly FGD gypsum, accounting for over 70% of total U.S. gypsum wallboard production raw material, demonstrating the material's established industrial dominance in mature markets. Rapid urbanization in India, Southeast Asia, and Latin America is generating new construction activity that drives expanding drywall and cement demand, directly pulling synthetic gypsum consumption upward.

Environmental Regulations Mandating FGD Byproduct Utilization and Circular Economy Adoption

Stringent environmental regulations governing industrial waste disposal are creating non-negotiable utilization incentives for synthetic gypsum, particularly FGD gypsum generated at coal-fired power plants. The U.S. EPA's Coal Combustion Residuals (CCR) Rule and EU Directive 2010/75/EU (Industrial Emissions Directive) impose strict controls on landfill disposal of FGD gypsum, compelling power utilities to pursue beneficial reuse in construction materials.

The American Coal Ash Association (ACAA) reports that beneficial use of FGD gypsum in wallboard manufacturing exceeded 18 million tons in recent reporting years, demonstrating the regulatory-driven adoption scale. Circular economy frameworks under the EU Green Deal and national waste reduction targets further incentivize industrial byproduct valorization, elevating synthetic gypsum's status from a waste liability to a commercially valuable secondary raw material across construction supply chains.

Restraints - Declining Coal Power Generation Reducing FGD Gypsum Supply in Mature Markets

The accelerating global energy transition away from coal power generation, a primary source of FGD gypsum, is creating a structural supply constraint for FGD gypsum availability in markets pursuing rapid decarbonization. The IEA projects significant coal power capacity retirement across Europe and North America through 2035 as renewable energy replaces fossil fuel generation.

Each retired coal plant eliminates a local FGD gypsum supply source, compelling drywall manufacturers in coal phase-out markets to either develop alternative synthetic gypsum supply chains or revert to higher-cost natural gypsum sourcing, adding procurement cost pressure.

Phosphogypsum Radioactivity Concerns Limiting Agricultural and Construction Application Adoption

Phosphogypsum, generated as a byproduct of phosphoric acid production from phosphate rock, contains naturally occurring radioactive materials (NORM), including radium-226 at concentrations that exceed regulatory thresholds in many jurisdictions. The U.S. EPA restricts phosphogypsum use under the Toxic Substances Control Act (TSCA), permitting it only for certain agricultural applications meeting specific radioactivity criteria.

This regulatory constraint significantly limits U.S. phosphogypsum valorization potential and creates barrier asymmetry versus unregulated markets, constraining the product's addressable end-use spectrum and suppressing demand growth in regulated markets.

Opportunities - Phosphogypsum: Fastest Growing Segment with Growing Agricultural and Construction Acceptance

Phosphogypsum represents the fastest growing synthetic gypsum segment at approximately 8% CAGR by 2033, driven by growing scientific consensus on the benefits of phosphogypsum soil amendments for agricultural productivity improvement and expanding regulatory acceptance in markets with lower radioactivity concerns.

The International Plant Nutrition Institute (IPNI) documents consistent evidence that phosphogypsum application improves soil structure, calcium and sulfur nutrient availability, and reduces soil aluminum toxicity, generating agricultural demand that is growing rapidly in Brazil, India, and Australia where regulatory frameworks permit broader use.

Brazil, the world's largest agricultural economy, has implemented phosphogypsum soil amendment programs across millions of hectares of cerrado farmland to address soil acidity, making it the global leader in phosphogypsum valorization and providing a model for other markets to expand beneficial use programs.

Green Building Standards and LEED Certification Driving Premium Synthetic Gypsum Drywall Demand

The rapid global adoption of green building certification standards, particularly LEED (Leadership in Energy and Environmental Design) by the U.S. Green Building Council (USGBC) and BREEAM in Europe, is creating premium demand for synthetic gypsum drywall products, as industrial byproduct gypsum contributes to recycled content credit compliance under green building certification frameworks. LEED v4 and BREEAM's Mat 03 criteria reward sourcing of materials with high recycled or industrial byproduct content, incentivizing specification of FGD gypsum-based wallboard in certified commercial and residential construction projects.

The USGBC reports over 100,000 LEED-certified buildings globally, with consistent annual growth sustaining demand for sustainable building materials, including recycled-content synthetic gypsum wallboard. This green building premium channel supports above-average margin realization for synthetic gypsum producers meeting relevant quality and documentation standards.

Category-wise Analysis

Product Type Insights

Flue Gas Desulfurization (FGD) Gypsum is the leading product type segment, accounting for approximately 30% market share in 2026. FGD gypsum, produced when sulfur dioxide emissions from coal-fired power plant flue gases react with limestone slurry in wet scrubber systems, is the highest-purity form of synthetic gypsum, with calcium sulfate dihydrate content typically exceeding 95% purity, surpassing natural mined gypsum quality.

The ACAA documents FGD gypsum as one of the most commercially successful coal combustion byproduct utilization streams in the United States, with drywall manufacturers including USG Corporation, National Gypsum, and Georgia-Pacific Gypsum building entire production facilities around FGD supply chain integration near power plants. The product's chemical purity, consistent particle size distribution, and established quality acceptance by drywall and cement manufacturers sustain its dominant market position.

End-user Insights

Drywall (wallboard) production is the leading End-use segment, accounting for approximately 42% of total synthetic gypsum consumption in 2026. Drywall represents the most technically demanding synthetic gypsum application, requiring consistent high-purity gypsum with specific moisture content and particle size characteristics, and the highest-volume single application globally. The Gypsum Association reports that U.S. gypsum wallboard production consistently exceeds 20 billion square feet annually, with synthetic FGD gypsum supplying most of the raw material for major domestic drywall manufacturers.

Growing residential and commercial construction activity globally, combined with energy efficiency building codes mandating thicker insulated wall systems, sustains consistent drywall volume growth. Knauf Gips KG, Saint-Gobain, and USG Corporation are the primary global drywall producers consuming synthetic gypsum at scale.

Regional Analysis

North America Synthetic Gypsum Market Trends and Insights

North America is a highly mature synthetic gypsum market, characterized by deep integration between coal power plant FGD systems and drywall manufacturing supply chains, active EPA regulatory frameworks governing beneficial reuse, and established quality standards administered by the Gypsum Association. The region is transitioning toward alternative synthetic gypsum sources as coal power retirements reduce FGD supply, with growing interest in citrogypsum and desulfogypsum alternatives to maintain supply chain continuity.

U.S. Synthetic Gypsum Market Size

The United States accounts for approximately 82% of the North American synthetic gypsum market revenue in 2026. Per USGS data, synthetic gypsum accounts for over 70% of U.S. wallboard raw material, with ACAA-documented annual FGD gypsum beneficial use exceeding 18 million tons. Hence, strong demand for drywall in residential construction, renovation of commercial buildings, and emergence of new industrial construction sustains the U.S. as the world's second-largest synthetic gypsum market.

Europe Synthetic Gypsum Market Trends and Insights

Europe is a technologically advanced synthetic gypsum market, with Central and Western European drywall and cement manufacturers having decades of experience integrating FGD gypsum from their domestic coal power sectors. The EU Industrial Emissions Directive mandating SO2 controls ensures continued FGD gypsum availability even as coal generation declines, while the EU Green Deal building renovation wave sustains drywall demand. Knauf Gips KG and Saint-Gobain dominate European synthetic gypsum wallboard production with integrated supply chains.

Germany Synthetic Gypsum Market Size

Germany holds approximately 23% of European synthetic gypsum market revenue in 2026. Germany operates Europe's largest FGD gypsum production base from its extensive coal power fleet, supplying integrated drywall manufacturers, including Knauf Gips KG (headquartered in Iphofen) and specialist FGD gypsum marketing firms, including BauMineral. Germany's EU Renovation Wave building renovation program sustains demand for drywall.

U.K. Synthetic Gypsum Market Size

The United Kingdom represents approximately 14% of the European synthetic gypsum market revenue in 2026. The UK's Drax and other coal/biomass power stations supply FGD gypsum to domestic drywall manufacturers. British Gypsum (part of Saint-Gobain) is the primary UK drywall producer utilizing synthetic gypsum.

France Synthetic Gypsum Market Size

France accounts for approximately 10% of European synthetic gypsum market revenue in 2026. France's RE2020 building standard and active building renovation programs sustain drywall and plaster demand. Compagnie de Saint-Gobain, headquartered in Paris, operates major French synthetic gypsum wallboard production and is a leading global authority on synthetic gypsum technical specifications.

Asia Pacific Synthetic Gypsum Market Trends and Insights

Asia Pacific leads global synthetic gypsum production and consumption, anchored by China, which accounts for approximately 58% of Asia Pacific synthetic gypsum demand, through its massive coal power fleet generating enormous FGD gypsum volumes and its extensive cement and drywall manufacturing base. China's Ministry of Ecology and Environment mandates SO2 emission controls at power plants, ensuring continued FGD gypsum production. India, Japan, and Southeast Asia are secondary but growing markets driven by construction expansion and coal power FGD compliance programs.

India Synthetic Gypsum Market Size

India represents approximately 12% of Asia Pacific synthetic gypsum market revenue in 2026. India's massive coal power fleet, generating significant FGD gypsum under CPCB emission norms, and rapidly expanding construction sector driving cement and drywall demand position India for strong growth. India is projected at approximately 7.0% CAGR through 2033, among the fastest in the region, supported by PMAY housing programs and smart city infrastructure investment.

Japan Synthetic Gypsum Market Size

Japan contributes approximately 8% of Asia Pacific synthetic gypsum market revenue in 2026. Japan has one of the world's highest FGD gypsum utilization rates, with virtually 100% of coal and oil power plant desulfurization gypsum beneficially reused in wallboard and cement production per METI data. Leading Japanese producers including Yoshino Gypsum have built entire supply chains around FGD gypsum integration. Japan is projected at approximately 4.2% CAGR through 2033.

Southeast Asia Synthetic Gypsum Market Size

Southeast Asia collectively accounts for approximately 10% of Asia Pacific synthetic gypsum market revenue in 2026. Vietnam, Thailand, Indonesia, and Malaysia are experiencing growing drywall and cement demand from rapid urbanization and construction activity. Regional coal power fleets generating increasing FGD gypsum volumes, combined with improving regulatory frameworks for industrial byproduct utilization, are driving both synthetic gypsum supply development and consumption growth across the sub-region.

Competitive Landscape

The global synthetic gypsum market exhibits a moderately fragmented competitive structure, with a mix of large integrated building materials companies and specialized synthetic gypsum processors competing across regional markets. LafargeHolcim, Compagnie de Saint-Gobain, and Knauf Gips KG dominate the drywall end-market as the largest integrated synthetic gypsum consumers, while specialized processors including BauMineral, FEECO International, and Synthetic Material LLC serve niche processing and trading roles.

Key competitive differentiators include proximity to FGD gypsum supply sources, processing technology quality, and downstream integration into wallboard or cement production. Growing demand for LEED-compliant recycled-content drywall is elevating quality documentation and traceability as competitive factors.

Key Developments:

- In February 2025, Knauf Gips KG announced an expansion of its German synthetic gypsum processing capacity, adding new drying and quality control infrastructure to serve the growing European demand for FGD gypsum in LEED-certified and EU Green Deal renovation projects requiring documented recycled content.

- In September 2024, USG Corporation (a Knauf company) expanded its FGD gypsum supply agreements with multiple U.S. power utilities, securing long-term raw material supply for its North American wallboard manufacturing network ahead of anticipated FGD gypsum supply tightening from coal power retirements.

- In March 2023, LafargeHolcim announced incorporation of increased phosphogypsum volumes in its cement production at select facilities in Brazil and India, leveraging the material's sulfate content as a performance-enhancing cement additive while supporting circular economy waste valorization commitments.

Global Synthetic Gypsum Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 2.0 Billion |

|

Current Market Value (2026) |

US$ 2.5 Billion |

|

Projected Market Value (2033) |

US$ 3.5 Billion |

|

CAGR (2026–2033) |

5.1% |

|

Leading Region |

Asia Pacific, ~36% market share (2026) |

|

Dominant Category – Product Type |

FGD Gypsum, ~30% share (2026) |

|

Top-Ranking Category – End-use |

Drywall, ~42% share (2026) |

|

Incremental Opportunity (2026–2033) |

US$ 1.0 Billion |

Companies Covered in Synthetic Gypsum Market

- AdvanSix Inc.

- Alpek S.A.B. de C.V.

- The Aquafil Group

- BASF SE

- Capro Co.

- China Petrochemical Development Corporation

- Domo Chemicals

- Grupa Azoty

- Gujarat State Fertilizers & Chemicals Limited

- Highsun Group

- KuibyshevAzot PJSC

- Lanxess AG

- Luxi Chemical Group Co., Ltd.

- China Petroleum & Chemical Corporation (Sinopec)

- Spolana

Frequently Asked Questions

The global synthetic gypsum market is projected to be valued at US$ 2.5 billion in 2026, growing from US$ 2.0 billion in 2020. The market is forecast to reach US$ 3.5 billion by 2033 at a CAGR of 5.1%, representing an absolute dollar opportunity of US$ 1.0 billion.

Primary drivers include the global cement sector consuming over 4 billion tons annually per GCCA data, with 3–5% gypsum content as a setting retarder, and USGS-documented synthetic gypsum accounting for 70%+ of U.S. wallboard raw material.

Asia Pacific leads with approximately 36% market share in 2026, anchored by China, accounting for ~58% of Asia Pacific demand, through its massive coal power FGD gypsum production and integrated cement and drywall manufacturing base.

The phosphogypsum segment at ~8% CAGR represents the fastest-growing opportunity, with Brazil's millions-of-hectare soil amendment programs and IPNI-documented yield improvements driving Latin American agricultural adoption.