- Industrial Goods & Service

- Industrial Racking System Market

Industrial Racking System Market Size, Share, and Growth Forecast, 2026 - 2033

Industrial Racking System Market by Design (Selective Racking, Cantilever Racking, Push Back Racking, Narrow & Wide Aisle Racking, Drive-In Racking, Pallet Flow Racking, Carton Flow Racking, Mobile Racking, Rack Supported Warehouse, Misc.), Carrying Capacity (Light Duty (40 to 200 kg), Medium Duty (0.25 to 1 Ton), Heavy Duty (2–4 Tons).), Ownership (Direct Ownership, Rentals), Industry, and Regional Analysis for 2026 - 2033

Industrial Racking System Market Size and Trends Analysis

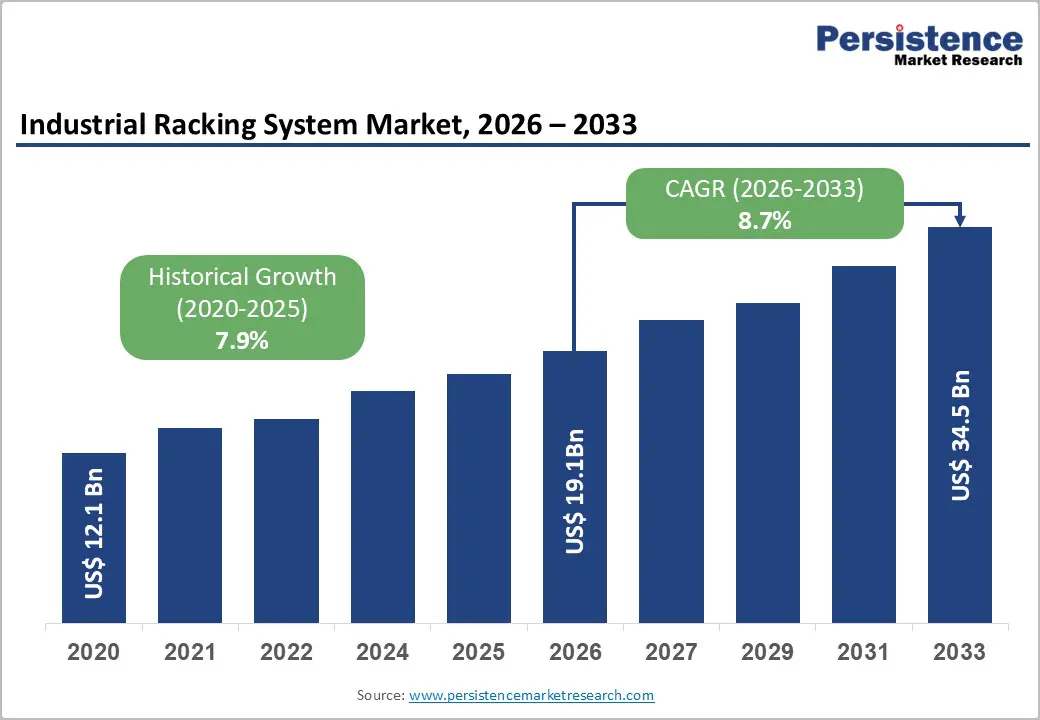

The global industrial racking system market size is likely to be valued at US$ 19.2 billion in 2026 and is projected to reach US$ 34.5 billion by 2033, growing at a CAGR of 8.7% between 2026 and 2033. The sector's upward trajectory reflects structural transformation in global supply chains, with businesses prioritizing storage-density optimization, operational throughput enhancement, and technology-enabled warehouse infrastructure to meet evolving consumer delivery expectations and inventory-management efficiency standards.

Key Industry Highlights:

- Regional Leadership: East Asia dominates the global market with 32% share, supported by China’s manufacturing concentration, export-driven logistics hubs, and rapid warehouse automation adoption.

- North America Market Scenario: North America holds 27% share, driven by robust e-commerce sales US$310B quarterly, cold-chain expansion, and continuous warehouse modernisation investments.

- Dominant Industry: Third-Party Logistics (3PLs) lead end-use demand with 27% share as operators expand multi-client, tech-enabled warehouses requiring scalable and flexible racking infrastructure

- Fastest-Growing Industry: E-commerce fulfilment centres represent the fastest-growing application, fueled by rising online retail penetration in the U.S., Canada, and India, accelerating high-density and automation-compatible storage deployments.

- Technology Shift: Automation-integrated solutions, including pallet shuttles, AMRs, AI-enabled WMS, and mobile racking, are redefining demand, evidenced by SSI SCHAEFER, Interlake Mecalux, and Steel King launching advanced high-density systems.

| Key Insights | Details |

|---|---|

|

Industrial Racking System Market Size (2026E) |

US$ 19.2 Bn |

|

Market Value Forecast (2033F) |

US$ 34.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.9% |

Market Dynamics

Drivers - Expansion of E-commerce Fulfilment Infrastructure and Warehousing Capacity

The explosive growth of digital commerce is fundamentally reshaping warehouse storage requirements and driving sustained demand for industrial racking solutions globally. According to the U.S. Census Bureau, retail e-commerce sales in the United States reached approximately US 310.3 Billion in Q3 2025, marking a 5.1 percent year-over-year increase, with e-commerce representing 16.4 percent of total retail sales on a seasonally adjusted basis.

In Canada, the e-commerce market achieved approximately US 89.4 Billion in gross merchandise value in 2024, with projections to reach US 104 Billion by 2029, sustaining above pre-pandemic growth levels. This expansion necessitates extensive warehouse infrastructure build-out, including high-density storage systems, automated retrieval solutions, and flexible racking configurations capable of accommodating diverse product dimensions and rapid inventory turnover.

The industrial racking system market benefits directly from this proliferation of fulfilment centres, as operators require scalable, durable storage systems to manage peak seasonal volumes, support multi-channel distribution strategies, and enable faster order processing cycles that meet consumer expectations for same-day or next-day delivery across urban and suburban markets.

Third-Party Logistics Expansion and Warehousing Modernisation

Third-party logistics providers have emerged as the dominant customer segment for industrial storage infrastructure, catalysing modernisation across warehouse real estate portfolios. In India, 3PL players accounted for 32 percent of H1 2025 leasing demand, which surged 63 percent year-over-year to a record 27.1 million square feet across eight major cities, according to CBRE. Between 2021 and H1 2025, 3PLs represented 40 to 50 percent of total warehouse leasing activity, particularly in Delhi-NCR, Mumbai, and Bengaluru, with multi-tenanted formats enabling faster scaling and reduced capital intensity.

The sector's evolution from basic transport and warehousing toward integrated, technology-enabled supply chain solutions has elevated infrastructure standards, with most players now deploying warehouse management software and increasingly adopting automation systems such as IoT sensors, conveyors, robotic picking, and automated storage and retrieval systems. North America's B2B e-commerce GMV share has maintained steady absolute growth despite regional share declining from 14.9 percent in 2017 to 13.7 percent in 2026 due to APAC's accelerated digitisation. This reflects mature yet robust demand for advanced racking systems that support eProcurement, cloud-based procurement platforms, and AI-powered supply chain optimisation.

The industrial racking system market experiences sustained momentum as 3PL operators transition legacy facilities to modern, code-compliant, automation-ready infrastructure featuring selective racking for inventory diversity, pallet flow racking for FIFO management, and drive-in systems for high-volume stock-keeping units.

Automation Integration and Smart Warehousing Technology Adoption

Warehouse automation is accelerating across global logistics networks, with storage infrastructure serving as the physical foundation for robotics, software-driven inventory management, and integrated materials handling systems. SSI SCHAEFER's deployment of the UAE's largest mobile pallet racking system for deep-freeze cold rooms at AD Ports Group's KLP21 hub in KEZAD boosted storage capacity by over 90 percent through PLC-controlled automation, demonstrating operational efficiency gains achievable through technology-enabled racking solutions.

In Qatar, Reitar Logtech and NEXX established the country's first Smart E-commerce Fulfillment Center in Milaha Logistics City, integrating Very Narrow Aisle racking systems reaching 16 meters high with 6,744 storage locations alongside advanced robotics and AI-based warehouse management systems. These deployments reflect broader industry adoption of warehouse management software, IoT sensors, conveyors, robotic picking systems, automated storage and retrieval systems, and goods-to-person solutions that require compatible racking infrastructure with precise dimensional tolerances, structural integrity, and integration compatibility.

The industrial racking system market is positioned to capture value from this automation wave, as operators prioritise storage frameworks that support seamless technology integration, enable higher storage densities through vertical space utilisation, and provide the mechanical reliability required for continuous automated operation across temperature-controlled, ambient, and high-throughput distribution environments.

Restraint - Capital Intensity and ROI Uncertainty

The deployment of industrial racking systems involves significant upfront capital expenditure, particularly for automated and high-density configurations, creating adoption barriers for small and mid-sized warehouse operators facing margin pressure and demand volatility. Investments in advanced racking infrastructure, such as automated storage and retrieval systems, rack-supported buildings, and integrated warehouse management platforms, require multi-million-dollar commitments with payback periods of three to seven years, depending on utilisation rates, labour cost savings, and throughput efficiency gains.

This capital intensity is compounded by uncertainty around e-commerce growth trajectories, inventory turnover patterns, and potential shifts in consumer behaviour that may render specialised racking configurations underutilised or obsolete before achieving projected returns. Economic downturns, supply chain disruptions, or regulatory changes affecting trade flows can further delay ROI realisation, making financial institutions cautious about funding warehouse infrastructure projects and prompting operators to defer upgrades or opt for lower-cost, less flexible racking alternatives that constrain future scalability.

Opportunity - Cold Storage and Temperature-Controlled Infrastructure Expansion

The proliferation of pharmaceutical distribution networks, fresh food supply chains, and cold-chain logistics is creating substantial opportunities for specialised racking solutions designed for temperature-controlled environments and for compliance with stringent storage protocols. SSI SCHAEFER's implementation of the largest mobile pallet racking system for deep-freeze cold rooms in the UAE, which increased storage capacity by over 90 percent while supporting critical vaccine infrastructure during the pandemic, demonstrates the operational and public health value of advanced cold-storage racking technologies.

The food and beverage manufacturing sector in the United States accounted for 16.8 percent of total manufacturing sales in 2021 and employed approximately 1.7 million workers across more than 42,700 establishments. Meat processing alone accounted for 26.2 percent of sector sales and generated sustained demand for refrigerated warehouse capacity.

The industrial racking system market can capitalise on this cold chain expansion by developing corrosion-resistant materials suitable for low-temperature environments, designs that maximise cubic storage efficiency within costly refrigerated space, and mobile or high-density configurations that reduce energy consumption per pallet position. Government regulations governing pharmaceutical storage, food safety compliance requirements, and consumer preferences for fresh and frozen product availability are further driving investments in cold storage infrastructure, creating a differentiated market segment with premium pricing potential and recurring upgrade cycles as operators modernize aging facilities to meet contemporary standards.

Geographic Expansion into High-Growth Emerging Markets

Emerging economies across the Asia-Pacific, Middle East, and Latin America regions are experiencing accelerating warehouse infrastructure development driven by manufacturing capacity additions, domestic consumption growth, and cross-border trade expansion that create substantial market opportunities for industrial racking providers. India's warehousing, industrial, and logistics ecosystem, which contributes approximately 14.4 percent to GDP and employs over 22 million people, witnessed record leasing demand of 27.1 million square feet in H1 2025, representing 63 percent year-over-year growth across eight major cities, with 3PL players and e-commerce firms accounting for 57 percent of absorption.

The country's logistics sector, valued at US 250 Billion in 2021 and projected to reach US 380 Billion by 2025, is undergoing systematic modernisation supported by government initiatives, including the National Logistics Policy, Digital India, BharatNet, and National Logistics Portal that aim to reduce logistics costs from 14 percent of GDP toward global benchmark levels by 2030.

The Industrial Racking System Market can capture value from this geographic expansion through strategic partnerships with local distributors and developers, customisation of product offerings to address regional building codes and seismic requirements, and positioning of solutions that support tier-II city expansion, where warehouse leasing activity is accelerating in locations such as Chandigarh, Hosur, Jaipur, and Kolkata.

The Middle East region is similarly advancing, with Kuwait's Zenith Group showcasing customised industrial racking solutions and UAE-based Dexion Gonvarri Material Handling appointing exclusive distribution partners across the Emirates and Kuwait to strengthen regional market access. These geographic markets offer first-mover advantages, lower competitive intensity than mature Western markets, and alignment with national infrastructure development priorities that provide policy support and investment incentives for logistics-sector modernization.

Category-wise Analysis

Design Insights

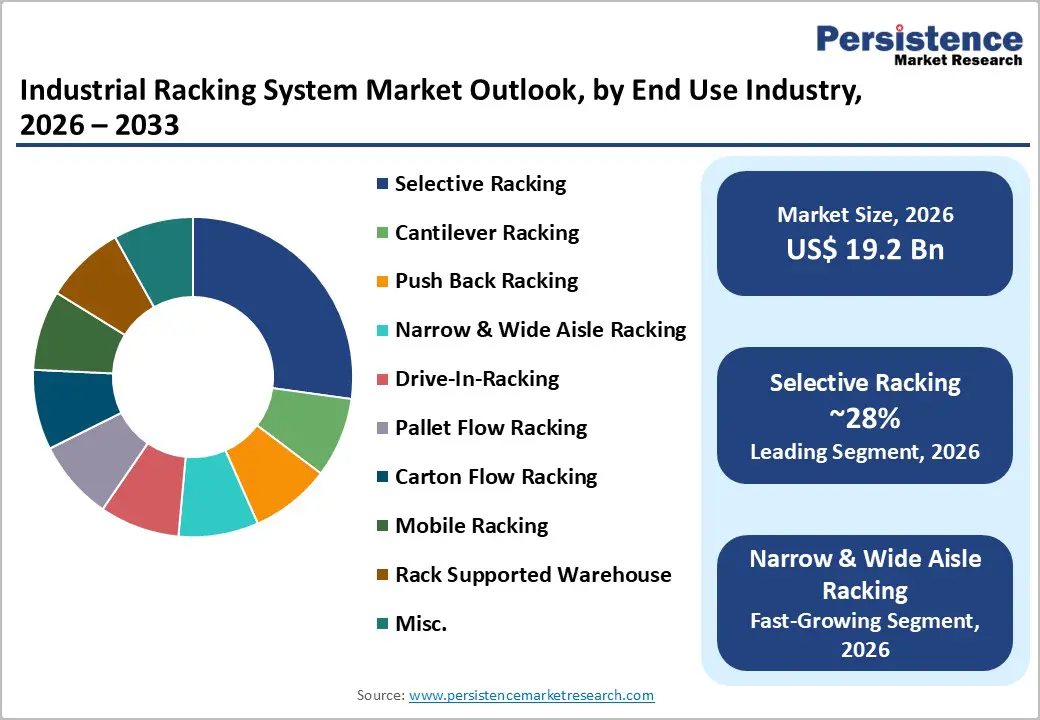

Selective racking maintained its position as the dominant design configuration, accounting for approximately 28% of market share in 2026, reflecting its versatility, cost-effectiveness, and universal applicability across diverse warehouse operations and industry verticals. This conventional pallet racking design provides direct access to every stored pallet position, enabling efficient inventory rotation management, simplified stock picking operations, and compatibility with standard forklift equipment without specialised handling systems or operator training requirements. The configuration's popularity stems from its adaptability to facilities with varying ceiling heights, straightforward installation processes, scalability for capacity expansion, and lower capital investment thresholds compared to specialised high-density or automated storage alternatives.

Selective racking systems serve as the foundational storage infrastructure for distribution centres managing diverse SKU portfolios with moderate inventory turnover rates, particularly in retail, automotive parts distribution, general manufacturing, and third-party logistics operations, where product variety and accessibility priorities outweigh maximum space utilisation considerations. The design's market leadership reflects its balance of functionality, economic accessibility, and operational flexibility that addresses mainstream warehouse storage requirements across small, medium, and large-scale facilities without necessitating substantial facility modifications or sophisticated materials handling equipment investments.

Narrow and Wide Aisle Racking has emerged as the fastest-growing design segment, driven by warehouse operators' intensifying focus on maximising storage density within existing facility footprints and optimising cubic space utilisation in markets with high real estate costs and limited expansion opportunities. This configuration enables significantly higher pallet positions per square foot than conventional selective racking by reducing aisle-width requirements, optimising vertical storage, and utilising specialised equipment, including very-narrow-aisle forklifts, turret trucks, and wire-guided or rail-guided handling systems that operate in aisles as narrow as 1.6 to 2.0 meters.

Industry Insights

Third-party logistics providers secured the largest end-use segment position, commanding approximately 27.0% of the market in 2026, reflecting their role as primary drivers of demand for warehouse infrastructure and storage systems across global logistics markets. 3PL operators manage extensive distribution networks serving multiple client industries simultaneously, requiring flexible, standardized racking configurations that accommodate diverse product characteristics, inventory rotation requirements, and service-level specifications across automotive, consumer goods, industrial manufacturing, and retail fulfilment contracts within the same facility footprint.

In India, 3PL companies accounted for 41 percent of industrial and logistics real estate leasing activity in 2024, reaching a record 39.5 million square feet across eight major cities, with CBRE research indicating that nearly 70 percent of Asia-Pacific occupiers expect to expand operations in the country within two years. This operational scale-up necessitates substantial investments in multi-tenanted warehouse formats and technology-enabled storage infrastructure that supports operational flexibility, client onboarding efficiency, and contract transition management.

E-commerce emerged as the fastest-growing end-use segment, driven by sustained online retail expansion, the proliferation of fulfilment centre networks, and evolving consumer delivery expectations that demand extensive investments in warehouse infrastructure and specialised storage configurations. According to the U.S. Census Bureau, e-commerce sales reached approximately US$310.3 billion in Q3 2025, representing 16.4 percent of total retail sales and reflecting sustained quarterly and annual growth. Canada's e-commerce market achieved US$89.4 billion in 2024, with projections to reach US$104 billion by 2029, while India's e-commerce ecosystem is projected to expand from US$125 billion in 2024 to US$345 billion by 2030 and US$550 billion by 2035.

Regional Insights and Trends

East Asia Industrial Racking System Market Trends

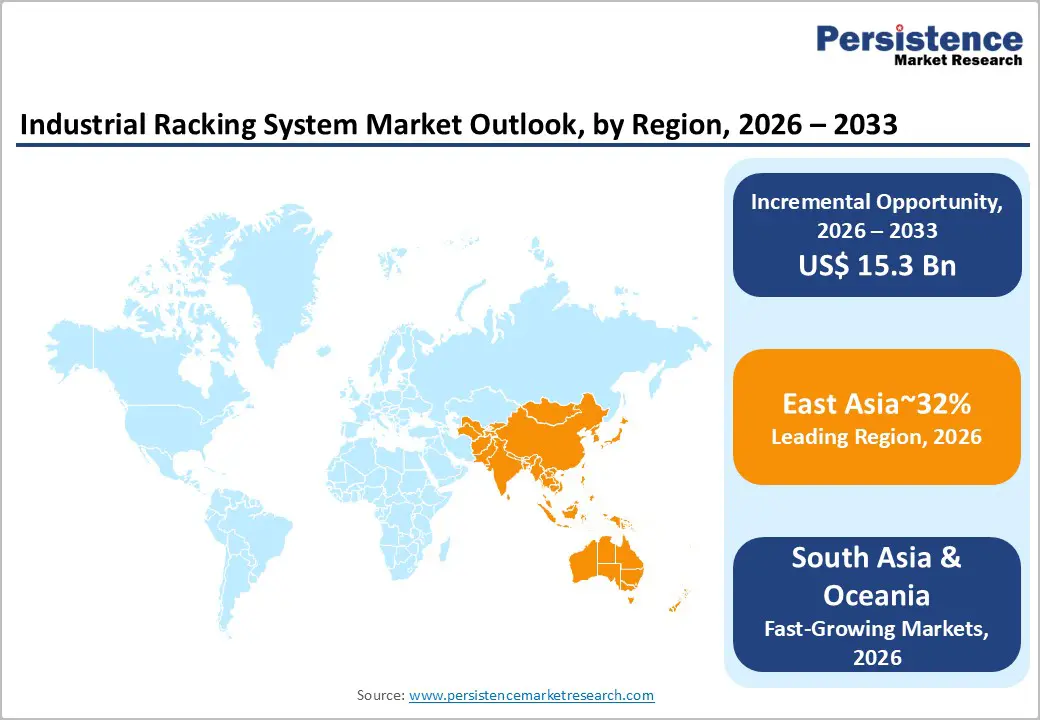

East Asia commanded approximately 32% regional market share, representing the largest geographic segment driven by manufacturing concentration, cross-border trade infrastructure, and accelerating logistics modernisation across China, Japan, and South Korea. The region serves as the epicentre of global manufacturing and export activities, with extensive port-proximate distribution centres, industrial park developments, and supply chain integration initiatives that require substantial warehouse storage capacity and investments in materials-handling infrastructure.

The dominance of the Asia-Pacific region in global B2B e-commerce, accounting for approximately 80.0 percent of total GMV projected for 2026, reflects the region's pivotal role in procurement digitalisation, manufacturing supply chain coordination, and cross-border trading platform adoption, which drive industrial warehouse infrastructure requirements.

China's position as the world's manufacturing hub sustains demand for racking systems across automotive, electronics, consumer goods, chemicals, and industrial components production and distribution networks, with ongoing warehouse automation investments and cold-chain logistics expansion supporting market growth. Japan and South Korea contribute through advanced manufacturing operations, technology-enabled logistics infrastructure, and sophisticated supply chain management practices that prioritise storage density optimization, earthquake-resistant structural specifications, and integration with automated materials handling systems.

North America Industrial Racking System Market Trends

North America maintained a substantial market presence, with approximately 27% regional share, supported by mature logistics infrastructure, extensive e-commerce penetration, and ongoing investments in warehouse modernization across the United States and Canada. The region demonstrated sustained market activity through strategic industry consolidations, technology integration initiatives, and capacity expansion programs addressing evolving supply chain requirements. According to the U.S. Census Bureau, retail e-commerce sales reached US 310.3 Billion in Q3 2025, marking 5.1 percent year-over-year growth and representing 16.4 percent of total retail sales, driving fulfillment center infrastructure investments and storage system upgrades. Canada's e-commerce market achieved US$89.4 billion in 2024, with continued expansion projected toward US$104 billion by 2029, sustaining warehouse demand above pre-pandemic baselines.

The food and beverage manufacturing sector contributed significantly to demand for racking systems, accounting for 16.8 percent of U.S. manufacturing sales in 2021, employing approximately 1.7 million workers across more than 42,700 establishments, and creating substantial refrigerated warehouse capacity requirements. Strategic acquisitions reshaped the competitive landscape, with Nucor Corporation's US 370 Million acquisition of Hannibal Industries in 2021 and US 75 Million acquisition of Elite Storage Solutions in 2022 expanding domestic racking manufacturing capabilities to serve e-commerce, food storage, and data center segments.

Technology integration accelerated through SSI SCHAEFER's partnership with Moffett Automation in January 2026, which integrated free-roaming pallet shuttle systems with warehouse management software, while Steel King Industries introduced its SK ADVANTX Structural Bolted Racking System at ProMat 2025, targeting automation and cold storage facilities with enhanced flexibility and on-site assembly capabilities. Speedrack Products Group's Made in USA Brand certification reinforced domestic manufacturing positioning through verified quality control and supply chain transparency aligned with ISO 9001 and RMI R-Mark standards.

Europe Industrial Racking System Market Trends

Europe accounted for approximately 24% regional market share, characterized by mature logistics networks, stringent regulatory frameworks, and ongoing warehouse modernisation addressing e-commerce fulfilment requirements and sustainability objectives. The region demonstrated continued infrastructure investment despite economic headwinds, with operators prioritising energy-efficient storage solutions, automated handling integration, and compliance with environmental performance standards embedded in green building certifications and corporate ESG commitments. European warehouse operators face distinctive market conditions, including high real estate costs in urban logistics hubs, labour availability constraints driving automation adoption, and regulatory requirements governing workplace safety, structural engineering standards, and environmental impact mitigation.

Dexion Gonvarri Material Handling's appointment of exclusive distribution partnerships and SSI SCHAEFER's continued technology deployments across the region reflect ongoing competitive activity and solution advancement in cold storage, pharmaceutical distribution, and e-commerce fulfilment applications. The market benefits from established automotive manufacturing clusters, food and beverage processing concentrations, and pharmaceutical production infrastructure that generate sustained demand for specialised racking configurations, including temperature-controlled environments, clean room storage, and hazardous materials handling systems.

Competitive Landscape

The global industrial racking system market exhibits a consolidated yet competitive structure, where a handful of large multinational integrators compete alongside regional manufacturers and service specialists. Leading players such as SSI SCHAEFER, Interlake Mecalux, Jungheinrich AG, Daifuku Co., Ltd., and Kardex AG command significant share through broad geographic reach, extensive product portfolios, and strong installation and after-sales capabilities. These companies differentiate on technology integration, offering automated storage solutions, intelligent pallet shuttles, and software-enabled warehouse management systems that address evolving customer demands for efficiency and scalability.

A second tier of influential players, such as Stow International and Gonvarri Material Handling, further enhances competition, particularly in regional markets with strong manufacturing and distribution bases. While the market is not fully fragmented, it is not strictly oligopolistic either; smaller specialist firms and local fabricators maintain relevance through niche offerings and regional strengths. Barriers to entry remain moderate due to the technical requirements of design, safety standards, and logistics integration, which favour established players but allow room for innovation from newer entrants.

Key Industry Developments

- In January 2026, SSI SCHAEFER and Moffett Automation announced a strategic partnership to integrate free-roaming pallet shuttle systems with warehouse management software and high-density pallet storage technologies. This cooperation enhances deployment of scalable, space-efficient pallet handling systems, a key requirement in modern North American warehouses facing automation, throughput, and layout constraints. The combined solution supports higher storage density and flexible system integration, aligning with ongoing automation adoption in the U.S. and Canadian racking environment.

- In September 2025, Reitar Logtech signed a strategic cooperation MoU with AI logistics firm NEXX to establish Qatar’s first Smart E-commerce Fulfilment Centre in Milaha Logistics City, Doha. The 5,000 sqm facility will integrate VNA (Very Narrow Aisle) racking systems reaching 16 meters high with 6,744 storage locations, alongside advanced robotics and AI-based warehouse management. This marks a significant enhancement in Qatar’s warehouse automation and storage infrastructure, strengthening demand for sophisticated industrial racking solutions across GCC logistics hubs.

Companies Covered in Industrial Racking System Market

- SSI Schaefer Systems International GmbH

- Interlake Mecalux, Inc.

- Jungheinrich AG

- Daifuku Co., Ltd.

- Kardex Holding AG

- Stow International NV

- Gonvarri Material Handling

- Ridg-U-Rak, Inc.

- Steel King Industries, Inc.

- Frazier Industrial Company

- UNARCO Material Handling, Inc.

- Hannibal Industries, Inc.

- Godrej & Boyce Manufacturing Company Limited

- Nilkamal Limited

- Kirby Building Systems LLC

Frequently Asked Questions

The global Industrial Racking System Market is projected to be valued at US$ 19.2 Bn in 2026.

The Selective Racking segment is expected to account for approximately 28.0% of the Global Industrial Racking System Market by Design type in 2026.

The market is expected to witness a CAGR of 8.7% from 2026 to 2033.

The Global Industrial Racking System Market growth is driven by rapid e-commerce fulfilment expansion, rising 3PL warehousing demand, and accelerating adoption of automation-integrated, high-density storage infrastructure across modern logistics and cold-chain facilities.

Key opportunities in the Industrial Racking System Market lie in expanding cold-storage and temperature-controlled warehouses, alongside rapid warehouse infrastructure development across emerging markets such as India, GCC, and Southeast Asia, where logistics modernisation, 3PL growth, and government-backed supply chain investments are accelerating demand for high-density, specialised racking solutions.