- Industrial Goods & Service

- Cladding System Market

Cladding System Market Size, Share, and Growth Forecast 2026 - 2033

Cladding System Market by Product (Steel, Aluminum, Composite Material, Fiber Cement, Terracotta, Ceramic, Others), Application (Residential, Industrial, Commercial, Offices, Institutional), and Regional Analysis for 2026 - 2033

Cladding System Market Size and Trend Analysis

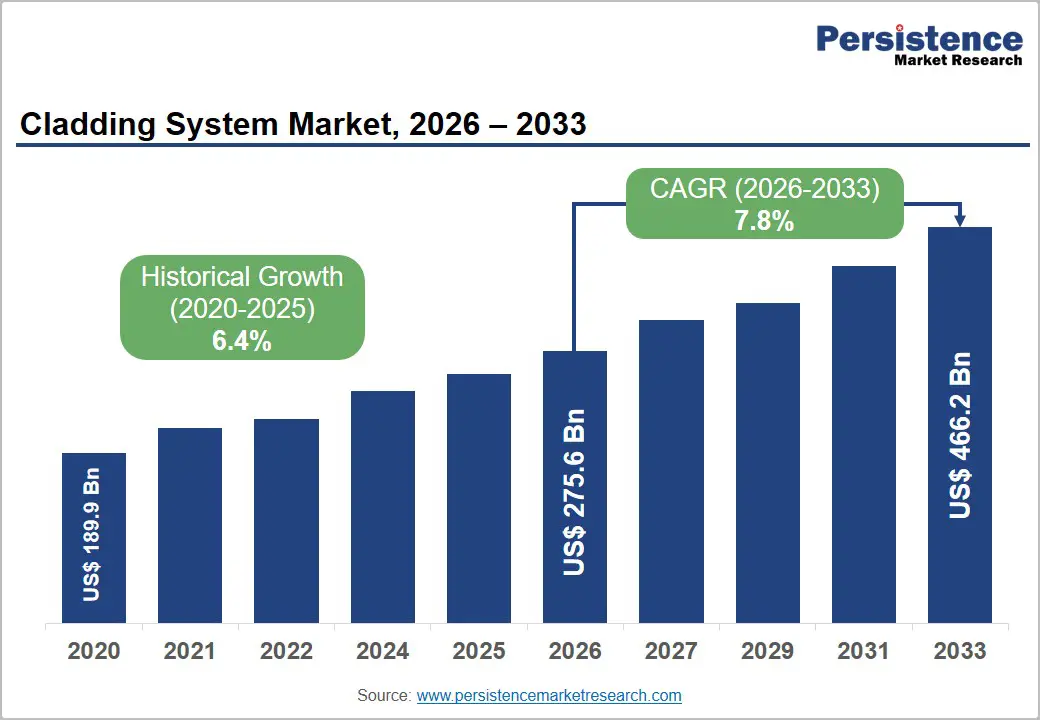

The global cladding system market size is supposed to be valued at US$ 275.6 Bn in 2026 and is projected to reach US$ 466.2 Bn by 2033, growing at a CAGR of 7.8% between 2026 and 2033. Unprecedented levels of urbanization, infrastructure modernization, and the global shift toward energy-efficient building envelopes are collectively propelling the cladding system market.

According to the United Nations, approximately 68% of the world's population is expected to live in urban areas by 2050, creating sustained demand for new residential and commercial construction.

Key Market Highlights

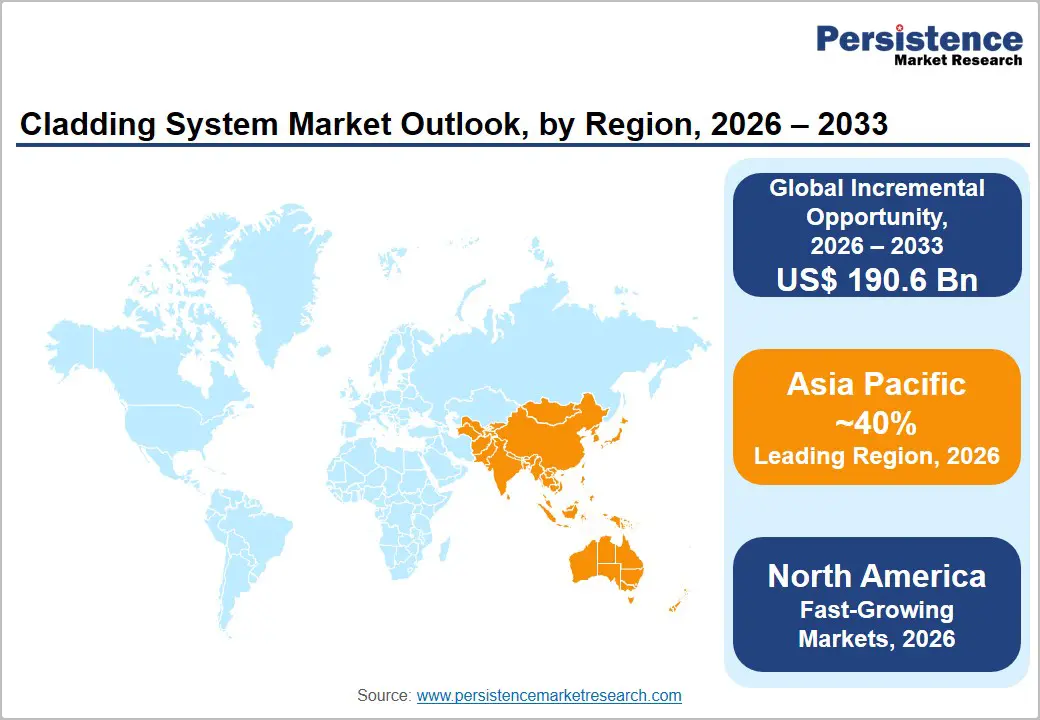

- Leading Region: Asia Pacific leads the global cladding system market, driven by extraordinary urbanization rates, large-scale government housing programs, and rapid expansion of commercial real estate in China, India, and Southeast Asia.

- Fastest Growing Region: Asia Pacific is also the fastest growing region, with India and Southeast Asian nations posting the highest growth rates, fueled by policy-backed affordable housing initiatives and smart city investments.

- Dominant Segment (Product): Aluminum cladding dominates the product segment with approximately 28% market share, prized for its lightweight properties, durability, recyclability, and architectural versatility across commercial and high-rise applications.

- Fastest Growing Segment (Application): The commercial segment is among the fastest growing application areas, driven by the global office construction boom, green building certifications, and rising demand for architecturally distinctive, high-performance facade systems.

- Key Market Opportunity: Large-scale renovation of energy-inefficient building stock across Europe and North America, backed by EU Renovation Wave funding and the U.S. Inflation Reduction Act, offers a multi-decade, policy-secured demand pipeline for cladding manufacturers.

DRO Analysis

Drivers - Rapid Urbanization and Surge in Construction Activity

The relentless pace of global urbanization continues to be a primary catalyst for cladding system adoption. The World Bank estimates that the construction sector accounts for nearly 13% of global GDP, and urban housing demand alone is expected to require the construction of over 2 billion new homes globally by 2050. In rapidly developing economies across Asia and Africa, governments are rolling out large-scale housing and smart city projects that inherently require modern facade systems.

For instance, India's Pradhan Mantri Awas Yojana (PMAY) targets the construction of over 20 million affordable housing units, considerably expanding demand for cost-effective yet durable cladding materials such as fibre cement and composite panels. This sustained construction momentum underscores the structural, long-term growth of the global cladding market.

Stringent Building Energy Codes and Green Construction Standards

Escalating regulatory pressure on building energy performance is driving the widespread uptake of advanced cladding solutions that contribute to improved thermal efficiency. The European Union's revised Energy Performance of Buildings Directive (EPBD 2024) mandates that all new buildings in member states achieve net-zero emissions by 2030, directly fuelling investment in high-performance cladding and rainscreen facade systems.

Similarly, the U.S. Department of Energy (DOE)'s adoption of the ASHRAE 90.1-2022 energy standard compels commercial building developers to enhance building envelopes significantly. Cladding systems incorporating insulation layers, ventilated facades, and reflective coatings are at the forefront of compliance strategies. This regulatory tailwind is expected to remain a consistent and powerful growth driver through the forecast period, particularly in developed markets.

Restraints - High Installation Costs and Shortage of Skilled Labor

Despite strong demand dynamics, the high upfront installation cost of advanced cladding systems remains a significant impediment, particularly in price-sensitive emerging markets. Premium systems such as terracotta rainscreen facades or architectural composite panels can cost upwards of US$ 150-300 per square meter installed, limiting adoption among low-to-mid income housing developers.

The chronic shortage of skilled facade installers and certified cladding technicians. According to the UK Construction Industry Training Board (CITB), the sector faces a 225,000-worker shortfall by 2027, pushing labour costs higher and extending project timelines. These dual pressures on project budgets constrain the market's full growth potential.

Fire Safety Regulations and Compliance Complexities Post-Grenfell

The 2017 Grenfell Tower fire in the United Kingdom exposed critical risks associated with combustible aluminum composite material (ACM) cladding, triggering a sweeping overhaul of building safety legislation globally. The subsequent Building Safety Act 2022 (UK) mandates the replacement of unsafe cladding on high-rise buildings, imposing substantial retrofit costs estimated at over £15 billion across the country.

While this spurs some replacement demand, heightened compliance scrutiny has raised specification timelines, increased testing costs, and created supply uncertainty for certain cladding product categories. Manufacturers are compelled to invest heavily in product certifications and fire testing, elevating barriers to entry and pressuring profit margins throughout the supply chain.

Opportunities - Expanding Demand for Sustainable and Green-Certified Building Facades

The global green building sector represents a compelling growth frontier for cladding system manufacturers. According to the World Green Building Council (WorldGBC), the number of green-certified buildings is growing at over 20% annually, driven by LEED, BREEAM, and Green Star certification frameworks. Cladding systems incorporating recycled content, low embodied carbon, and end-of-life recyclability are gaining preferred status in green building specifications.

Fiber cement and terracotta cladding have emerged as standout materials in this context, offering both aesthetic versatility and environmental credentials. Governments in the EU, Australia, and Canada are increasingly mandating minimum sustainability standards for public infrastructure, creating a durable institutional pipeline for green-compliant cladding suppliers.

Large-Scale Renovation of Aging Building Stock in Europe and North America

An estimated 75% of the European Union's existing building stock, which is one of the most energy-inefficient in the developed world, was built before modern energy codes were enacted, according to the European Commission. The EU Renovation Wave Strategy aims to at least double annual energy renovation rates by 2030, covering over 35 million buildings.

Similarly, in North America, the U.S. Inflation Reduction Act (IRA, 2022) allocates US$ 369 billion toward energy and climate programs, part of which incentivizes commercial and residential building retrofits. These renovation programs represent a massive addressable market for over cladding and re-cladding solutions, particularly aluminum, composite, and insulated facade systems, offering manufacturers a multi-decade, policy-backed revenue opportunity with predictable demand cycles.

Category-wise Analysis

Product Insights

Aluminum cladding dominates the global cladding system market by product type, accounting for approximately 28% of total market revenue. This leadership is primarily attributed to aluminium’s exceptional combination of lightweight properties, high durability, corrosion resistance, and architectural flexibility.

Aluminum composite panels (ACPs) and solid aluminum panels offer virtually unlimited design possibilities available in a wide range of finishes, colours, and profiles, making them the preferred choice for high-rise commercial facades and institutional buildings worldwide. According to the International Aluminum Institute (IAI), over 75% of all aluminum used in construction applications is eventually recycled, making it an increasingly preferred choice in green building projects.

Application Insights

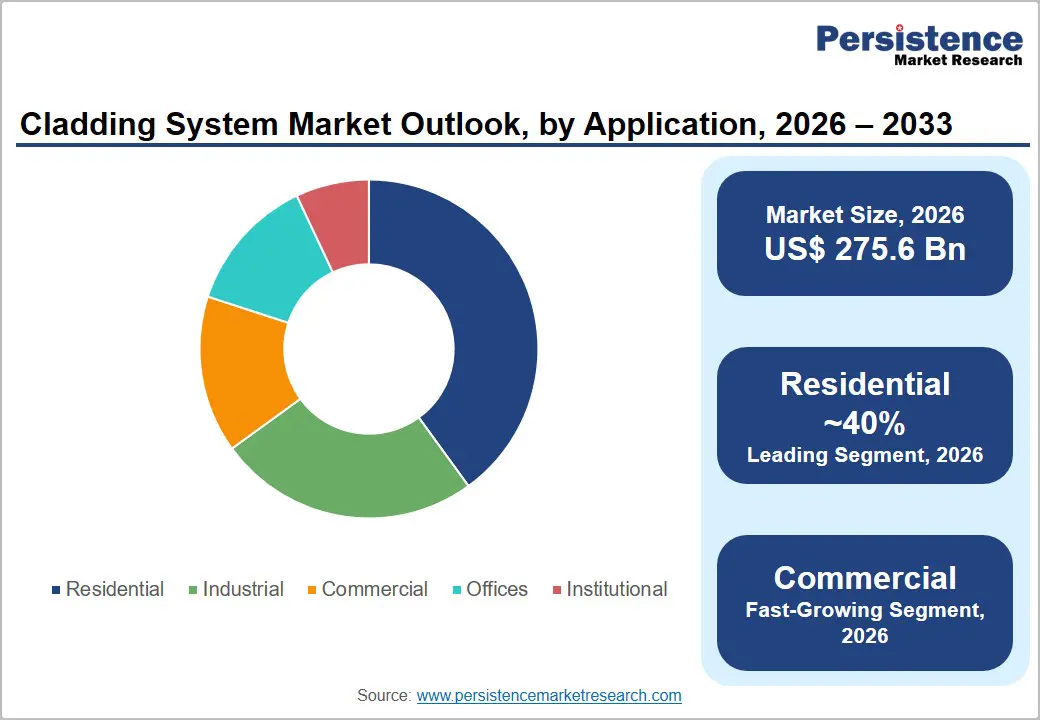

The residential segment commands the largest share of the global cladding system market by application, representing approximately 37% of total demand. This dominance is underpinned by the global surge in residential construction driven by urbanization and population growth. In Asia Pacific alone, countries such as China and India are adding hundreds of thousands of new housing units annually, with fibre cement and composite cladding increasingly specified for mid-rise multi-family residential projects due to their cost-effectiveness and low maintenance requirements.

Government-backed affordable housing programs in India, China, and across Southeast Asia continue to generate substantial cladding procurement volumes.

Regional Analysis

North America Cladding System Market Trends & Analysis

North America holds a significant share of the global cladding system market, driven primarily by large-scale commercial construction, active renovation of aging building stock, and progressively tightening building energy codes across the United States and Canada. The region is characterized by strong demand for fibre cement, aluminum composite panels, and insulated metal panels (IMPs) across commercial offices and institutional buildings. The U.S. Infrastructure Investment and Jobs Act and the Inflation Reduction Act (IRA) collectively provide significant fiscal incentives for energy-efficient building retrofits, generating sustained demand for high-performance cladding solutions.

U.S. Cladding System Market

The United States represents the largest individual country market in North America, accounting for over 82% of the regional market share. Robust commercial construction pipelines in states such as Texas, Florida, and California, combined with a massive office and mixed-use building renovation wave in major metropolitan areas, underpin strong and consistent demand for cladding systems.

Europe Cladding System Market Trends, Drivers & Insights

Europe represents the most regulation-driven cladding market globally, shaped by the EU Renovation Wave Strategy, the revised Energy Performance of Buildings Directive (EPBD), and stringent post-Grenfell fire safety legislation. These frameworks are simultaneously driving the replacement of non-compliant cladding and the installation of new high-performance facades on both public and private sector buildings. The region shows particularly strong demand for natural and sustainable materials such as terracotta, fibre cement, and high-pressure laminate (HPL) cladding, reflecting both regulatory imperatives and consumer preferences for low-carbon construction materials.

Germany Cladding System Market

Germany leads the European market, supported by its Energieeffizienzgesetz (Energy Efficiency Act 2023) and a mature, technically demanding construction industry that consistently specifies premium ventilated facade and rainscreen cladding systems.

U.K. Cladding System Market

The United Kingdom market is substantially influenced by the post-Grenfell regulatory overhaul. The Building Safety Act 2022 mandates the removal and replacement of unsafe ACM cladding on high-rise buildings, creating a multi-billion-pound remediation market that is expected to sustain elevated demand through 2030.

France Cladding System Market

France is experiencing growing adoption of bio-sourced and low-carbon cladding materials, aligned with its RE2020 thermal regulation. Government-led urban renewal programs in major cities like Paris and Lyon are generating significant demand for architectural facade systems.

Asia Pacific Cladding System Market Drivers & Analysis

Asia Pacific is the largest and fastest-growing regional market for cladding systems globally, underpinned by extraordinary urbanization rates, massive infrastructure investment, and burgeoning middle-class demand for quality housing. The region accounts for the largest share of new residential and commercial construction worldwide, with China and India being the primary growth engines.

Government-backed housing schemes, smart city programs, and mega-infrastructure projects are generating prodigious volumes of cladding demand across the region. Growing construction quality standards and increasing awareness of building energy efficiency are progressively shifting demand toward higher-performance cladding materials, including aluminum composite panels and insulated facade systems.

China Cladding System Market Trends

China is the single largest country market globally, accounting for the dominant share of Asia Pacific cladding demand. Driven by the 14th Five-Year Plan emphasis on new urbanization, affordable housing, and green building standards, the market continues to post robust growth despite real estate sector headwinds.

India Cladding System Market Trends

India is the fastest growing major market in the region, propelled by PMAY (Pradhan Mantri Awas Yojana), the Smart Cities Mission, and the rapid expansion of commercial real estate in metropolitan centres. The country is experiencing rapid uptake of fiber cement and aluminum cladding for both new construction and facade renovation projects.

Japan Cladding System Market Insights

Japan's cladding market is characterized by high technical sophistication and emphasis on seismic resistance, fire safety, and longevity. Demand is driven by ongoing renovation of aging commercial buildings and the 2050 Carbon Neutrality Declaration, which mandates zero-emission buildings, spurring adoption of high-performance insulated facade systems.

Competitive Landscape

The global cladding system market exhibits a moderately fragmented structure, featuring a mix of large multinational building material conglomerates and specialized regional manufacturers. Leading players such as James Hardie Industries, Saint-Gobain, and Kingspan Group command significant market shares through diversified product portfolios, global manufacturing footprints, and well-established distribution networks. Key competitive differentiators include product innovation in fire-rated and sustainable cladding systems, digital design tools for facade specification, and certifications aligned with international green building standards.

Key Developments:

- In January 2025, James Hardie Industries announced the expansion of its fibre cement manufacturing facility in Prattville, Alabama, USA, adding over 200 million square feet of additional annual production capacity to meet rising North American residential cladding demand.

- In September 2024, Saint-Gobain completed its acquisition of CSR Limited (Australia), significantly strengthening its presence in the Asia Pacific building materials market and expanding its portfolio of lightweight facade and cladding solutions across the region.

Companies Covered in Cladding System Market

- James Hardie Industries plc

- Saint-Gobain S.A.

- Kingspan Group plc

- Etex Group

- Arconic Corporation

- Trespa International B.V.

- ROCKWOOL International A/S

- Sika AG

- Wienerberger AG

- Knauf SE

- Nichiha Corporation

- Sto SE & Co. KGaA

- Cembrit Holding A/S

- Equitone (Eternit Group)

- 3A Composites GmbH

- Vitrabond (Fairview Architectural)

Frequently Asked Questions

The global Cladding System market is estimated to be valued at US$ 275.6 Billion in 2026 and is projected to reach US$ 466.2 Billion by 2033, expanding at a compound annual growth rate (CAGR) of 7.8% over the 2026 - 2033 forecast period.

The primary growth drivers include rapid global urbanization generating strong construction activity demand, and increasingly stringent building energy performance regulations such as the EU's Energy Performance of Buildings Directive (EPBD) and the U.S. ASHRAE 90.1-2022 standard that mandate high-performance facade and cladding solutions to meet net-zero building targets.

Aluminum cladding leads the global market by product type, commanding approximately 28% of total market revenue. Its dominance is attributable to exceptional lightweight properties, high corrosion resistance, architectural versatility, and strong recyclability credentials that align with growing green building certification requirements globally.

Asia Pacific holds the largest regional share of the global Cladding System market and is simultaneously the fastest growing region. This is driven by unprecedented urbanization in China and India, large-scale government-backed housing programs including India's PMAY, and significant commercial real estate expansion across Southeast Asian markets.

Leading companies in the global Cladding System market include James Hardie Industries plc, Saint-Gobain S.A., Kingspan Group plc, Etex Group, Arconic Corporation, Trespa International B.V., ROCKWOOL International A/S, Sika AG, Wienerberger AG, and Knauf SE, among others.