- Electric Mobility

- India Electric Vehicles Market

India Electric Vehicles Market Size, Share, and Growth Forecast 2026 - 2033

India Electric Vehicles Market by Vehicle Type (Electric Scooters, Electric Motorcycles, Electric Passenger Cars, Electric Light Commercial Vehicles, Electric Buses, Electric Heavy Commercial Vehicles, Others), Range (Up to 150 Km, 151-300 Km, 301-500 Km, Above 500 Km), Propulsion Type (Battery Electric Vehicles, Hybrid Electric Vehicles, Plug-in Hybrid Electric Vehicles, Fuel Cell Electric Vehicles), Battery Type (Lithium-ion Battery, Lead-acid Battery, Solid-state Battery, Others), and Regional Analysis for 2026 - 2033

India Electric Vehicles Market Size and Trend Analysis

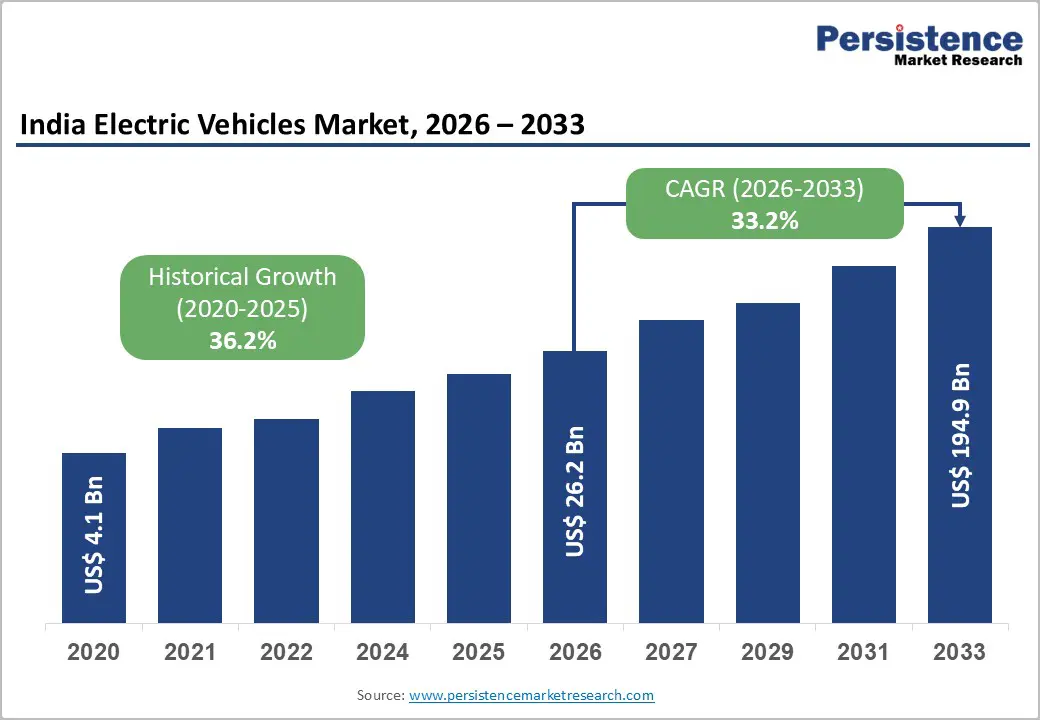

The India electric vehicles market is valued at US$ 26.2 Bn in 2026 and is projected to reach US$ 194.9 Bn by 2033, growing at a CAGR of 33.2% between 2026 and 2033.

This extraordinary expansion is driven by India's landmark government policy commitments including the FAME II scheme, the PM e-DRIVE scheme, and PLI incentives for advanced cell chemistry batteries that are collectively reducing EV sticker prices and accelerating adoption across two-wheelers, passenger cars, and commercial fleet segments.

Surging fuel costs, a rapidly expanding public charging infrastructure network, and aggressive electrification strategies by domestic OEMs such as Ola Electric, Tata Motors, and Bajaj Auto are reinforcing this momentum, positioning India as one of the world's fastest-growing EV markets through the forecast decade.

The India electric passenger vehicle market demonstrated strong growth momentum in FY2025-26, with EV penetration reaching 4.5% across the passenger car category. Out of 4.84 million passenger vehicles registered, nearly 219,484 units were electric, reflecting rising consumer adoption, supportive government policies, and expanding charging infrastructure. Telangana emerged as the leading state in EV penetration with 11.6% share, followed by Chandigarh (9.1%) and Delhi (8.4%), highlighting the effectiveness of state-level EV incentives and urban electrification initiatives. In terms of sales volume, Maharashtra remained the largest electric car market, accounting for 15.5% of total e-4W sales, followed by Karnataka and Kerala.

From a manufacturer's perspective, Tata Motors continued to dominate the electric four-wheeler segment, registering 85,367 unit sales and a 38.9% market share in FY2025-26. JSW MG Motors secured the second position with 26.7% market share, while Mahindra Electric accounted for 21.6% share. Competitive intensity in the market increased significantly as manufacturers expanded EV portfolios, charging partnerships, and connected mobility features. Among key players, Mahindra Electric recorded the strongest growth with an exceptional 434% increase in sales, while MG Motor achieved 79.1% year-on-year growth, indicating rapidly strengthening competition in India’s evolving electric passenger vehicle market.

Key Industry Highlights:

- Explosive Market Expansion: India’s electric vehicle market is expected to grow from US$ 26.2 Bn in 2026 to US$ 194.9 Bn by 2033, registering a remarkable CAGR of 33.2%, supported by government incentives, charging infrastructure expansion, and OEM electrification strategies.

- Passenger EV Penetration: Electric passenger vehicles achieved 4.5% penetration in FY2025-26, with nearly 219,484 units registered, reflecting strong consumer adoption driven by policy support, urban mobility demand, and improved charging accessibility across major states.

- Tata’s Market Leadership: Tata Motors maintained leadership in the electric passenger vehicle segment with a 38.9% market share and 85,367 unit sales, benefiting from affordable models, wide distribution networks, and strong brand positioning.

- Government Incentive Support: FAME II, PM e-DRIVE, and PLI ACC schemes together contributed more than INR 39,000 crore toward EV subsidies, battery manufacturing, and charging infrastructure, significantly improving affordability and accelerating nationwide EV adoption.

- Scooter Segment Dominance: Electric scooters accounted for approximately 42% of total EV sales volume in 2025, supported by India’s strong two-wheeler dependency, economical pricing, and increasing adoption among urban commuters and delivery operators.

- Electric Bus Momentum: Electric buses are projected to be the fastest-growing vehicle category with an estimated CAGR of 42% through 2033, driven by state transport electrification programs, large fleet tenders, and public sustainability initiatives.

- Battery Technology Shift: Lithium-ion batteries dominated the market with nearly 78% share in 2025, while solid-state batteries are projected to expand at over 45% CAGR, creating major opportunities in advanced battery innovation and localization.

- Leadership Dynamics in South India: South India accounted for nearly 34% of India’s total EV registrations in 2025, supported by Bengaluru’s EV startup ecosystem, Tamil Nadu’s manufacturing investments, and Telangana’s aggressive electrification targets.

- Commercial Fleet Opportunity: Commercial fleet electrification across logistics, public transport, and last-mile delivery is emerging as a significant growth opportunity, supported by large procurement contracts and sustainability commitments from major operators and e-commerce companies.

Market Dynamics

Market Growth Drivers

Government Policy Catalysts: FAME II, PM e-DRIVE, and PLI Scheme Driving Rapid EV Adoption

India's EV revolution is fundamentally policy-driven, with the central government deploying a layered set of demand and supply-side incentives that are materially reducing EV total cost of ownership. The Faster Adoption and Manufacturing of Electric Vehicles Phase II (FAME II) scheme, with a total outlay of INR 10,000 crore (approximately US$ 1.2 billion), provided direct purchase incentives for over 1.3 million electric two-wheelers, three-wheelers, and buses by 2024 per the Ministry of Heavy Industries.

Its successor, the PM e-DRIVE scheme (approved with an outlay of INR 10,900 crore for 2024-2026), expands support to e-ambulances, e-trucks, and public charging infrastructure. Concurrently, the Production Linked Incentive (PLI) scheme for Advanced Chemistry Cell (ACC) batteries, with an incentive of INR 18,100 crore, is building domestic battery manufacturing capacity, reducing India's import dependency and structurally lowering battery pack costs the largest single cost component of any EV.

Surging Two-Wheeler Electrification and Expanding Urban Charging Infrastructure

India is the world's largest two-wheeler market, with over 21 million units sold annually per the Society of Indian Automobile Manufacturers (SIAM). The cost parity between electric and ICE two-wheelers driven by battery cost deflation and FAME subsidies has unlocked mass-market adoption, with electric two-wheelers accounting for over 57% of total EV registrations in India in FY2024 per Vahan portal data.

The Ministry of Power's National Electric Mobility Mission Plan (NEMMP) targets 500,000 public charging stations by 2030, with over 12,000 operational stations as of 2024. Companies such as Ola Electric, Ather Energy, and TVS Motor are simultaneously expanding proprietary charging networks, further reducing range anxiety and driving consumer confidence in EV transition across Tier-1 and Tier-2 Indian cities.

Restraints - Limited Public Charging Infrastructure and Range Anxiety in Rural and Semi-Urban Areas

Despite progress in metropolitan EV charging deployment, India's rural and semi-urban regions remain severely underserved. The International Energy Agency (IEA) notes that India's charging infrastructure density measured as EVs per public charger remains significantly below that of China and Europe. As of 2024, the ratio of EVs to public chargers in India exceeded 25:1 per NITI Aayog estimates, compared to approximately 7:1 in China. This infrastructure deficit perpetuates range anxiety among prospective buyers in non-metropolitan markets, constraining EV adoption to urban corridors and limiting the geographic reach of India's EV transition.

High Battery Costs and Dependence on Imported Lithium and Cell Components

Despite global lithium-ion battery price declines, battery packs still represent 35-45% of an EV's ex-factory cost in India per NITI Aayog data. India imports over 70% of its lithium-ion cell requirements primarily from China and South Korea, creating structural cost exposure and supply chain vulnerability. The Geological Survey of India (GSI) confirmed lithium deposits in Jammu & Kashmir in 2023, but commercial extraction remains years away. Until domestic battery manufacturing under the PLI scheme achieves scale, import dependency will continue to weigh on EV cost competitiveness, particularly for mass-market passenger car segments.

Opportunities - Electric Commercial Vehicle Fleet Electrification: Logistics, Last-Mile, and Public Transport

India's commercial vehicle electrification opportunity spanning last-mile delivery fleets, intercity buses, and intra-city logistics is among the fastest-growing demand pockets in the India EV market. NITI Aayog's report on 'India's Electric Vehicle Transition' projects that electric three-wheelers and light commercial vehicles alone could eliminate over 1.3 gigatonnes of CO2 by 2030 if fleet electrification achieves target penetration.

The PM e-DRIVE scheme specifically earmarks INR 4,391 crore for electric buses across state transport undertakings. Companies such as Tata Motors, Olectra Greentech, and PMI Electro Mobility are securing large state-level bus fleet tenders, while logistics operators including Amazon India, Flipkart, and Zomato have committed to fully electrified delivery fleets, creating large, recurring, and commercially attractive EV procurement volumes.

Domestic Battery Manufacturing Scale-Up and the Solid-State Battery Technology Opportunity

The PLI scheme for Advanced Chemistry Cell (ACC) battery manufacturing with approved capacity of 50 GWh is catalyzing domestic investment by Ola Electric (Gigafactory, Krishnagiri), Amara Raja Energy & Mobility, Exide Industries, and international partners. Beyond lithium-ion, solid-state battery technology represents a transformational opportunity offering 2-3x higher energy density, faster charging, and superior safety profiles versus conventional Li-ion cells.

The Department of Science and Technology (DST) has funded solid-state battery R&D under the National Mission on Transformative Mobility, and Tata Motors (through its partnership with Agratas) is actively investing in next-generation cell technology. As solid-state batteries approach commercial viability in the late 2020s, Indian EV manufacturers with early supply relationships will gain decisive cost and performance advantages in the passenger car and commercial vehicle segments.

Category-wise Analysis

Vehicle Type Insights

Electric Scooters dominate the vehicle type category in India EV market, commanding approximately 42% of total EV sales by volume in 2026. Their leadership is rooted in India's structural two-wheeler dependence, with over 75% of Indian households own a two-wheeler rather than a car and the economic logic of EV conversion being most compelling at the lower price points of scooters.

The Vahan portal registered over 900,000 electric scooters in FY2024, making it the highest-volume segment by a significant margin. Leading players including Ola Electric, TVS iQube, Bajaj Chetak, and Ather 450X are driving rapid technology advancement with improved battery management systems, connected features, and extended range capabilities that are steadily eroding the ICE scooter market share.

Electric Buses represent the fastest-growing Vehicle Type segment, expanding at an estimated CAGR of 42% through 2033. State transport undertakings across Maharashtra, Karnataka, and Delhi are awarding large fleet tenders under the PM e-DRIVE and FAME II schemes, with Tata Motors and Olectra Greentech among primary beneficiaries of this accelerating public transit electrification push.

Range Insights

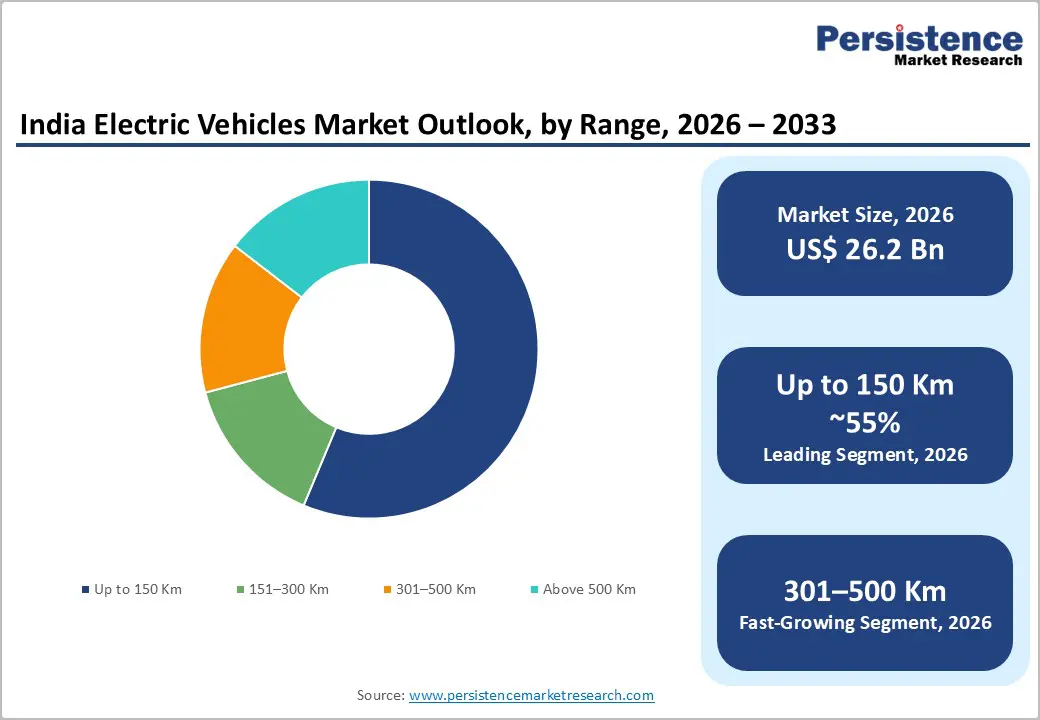

The Up to 150 Km range segment holds the leading position in the India EV market by volume, accounting for approximately 55% of total EV sales in 2026. This segment's dominance directly reflects the composition of India's EV market, dominated by electric two-wheelers and three-wheelers that primarily serve intra-city commuting use cases with typical daily travel distances of 30-70 km per the Ministry of Road Transport and Highways (MoRTH) mobility survey.

Leading electric scooters such as the Ola S1 Pro, TVS iQube ST, and Ather 450X all fall within this range category and collectively account for the majority of India's registered EV fleet. Urban ride density and short average trip lengths make range below 150 km sufficient for the majority of India's urban and peri-urban commuters.

The 301-500 Km range segment is the fastest growing, advancing at an estimated CAGR of 38% through 2033, driven by the rapid expansion of premium electric passenger cars particularly the Tata Nexon EV Max, MG ZS EV, and Hyundai IONIQ 5, serving aspirational buyers seeking highway-capable range that reduces charge stop frequency on intercity journeys.

Propulsion Type Insights

Battery Electric Vehicles (BEV) are the dominant propulsion type in the India EV market, commanding approximately 68% of total EV sales in 2026 by volume. BEV's market leadership is driven by policy alignment FAME II and PM e-DRIVE exclusively incentivize pure battery-electric vehicles and by the economic appeal of zero direct fuel costs in a country where petrol prices frequently exceed INR 100/litre in major cities. The Bureau of Energy Efficiency (BEE) has published standardized star ratings for EV charging efficiency, further reinforcing BEV infrastructure alignment.

India's two-wheeler segment where ICE hybridization is economically impractical structurally, tilts overall market propulsion composition decisively toward pure BEV architecture.

Plug-in Hybrid Electric Vehicles (PHEV) are the fastest-growing propulsion segment, at an estimated CAGR of 36% through 2033, as premium OEMs including Jeep (Stellantis), BMW, and Volvo introduce PHEV variants catering to consumers seeking extended range flexibility while transitioning away from full ICE dependence in the emerging premium SUV segment.

Battery Type Insights

Lithium-ion Batteries (LiB) dominate the India EV battery type landscape, accounting for approximately 78% of EV battery installations in 2025. Li-ion's dominance is attributable to its favourable energy density (150-250 Wh/kg), declining cell costs falling from approximately US$ 150/kWh in 2023 toward US$ 100/kWh by 2026 per BloombergNEF estimates and an established supply ecosystem from Panasonic, CATL, Samsung SDI, and domestic producers. The PLI ACC scheme is specifically anchored around NMC and LFP lithium-ion chemistries, ensuring continued dominance of Li-ion through the medium-term forecast horizon.

Solid-state Batteries represent the fastest-growing battery type segment with a projected CAGR of 45%+ from a small base through 2033. Backed by investments from Tata Group (Agratas) and DST-funded R&D programs, solid-state batteries are expected to enter initial commercial deployment in India's premium EV segments by the late 2020s, offering step-change improvements in safety, energy density, and cycle life.

Zone Insights

South India Electric Vehicles Market Trends

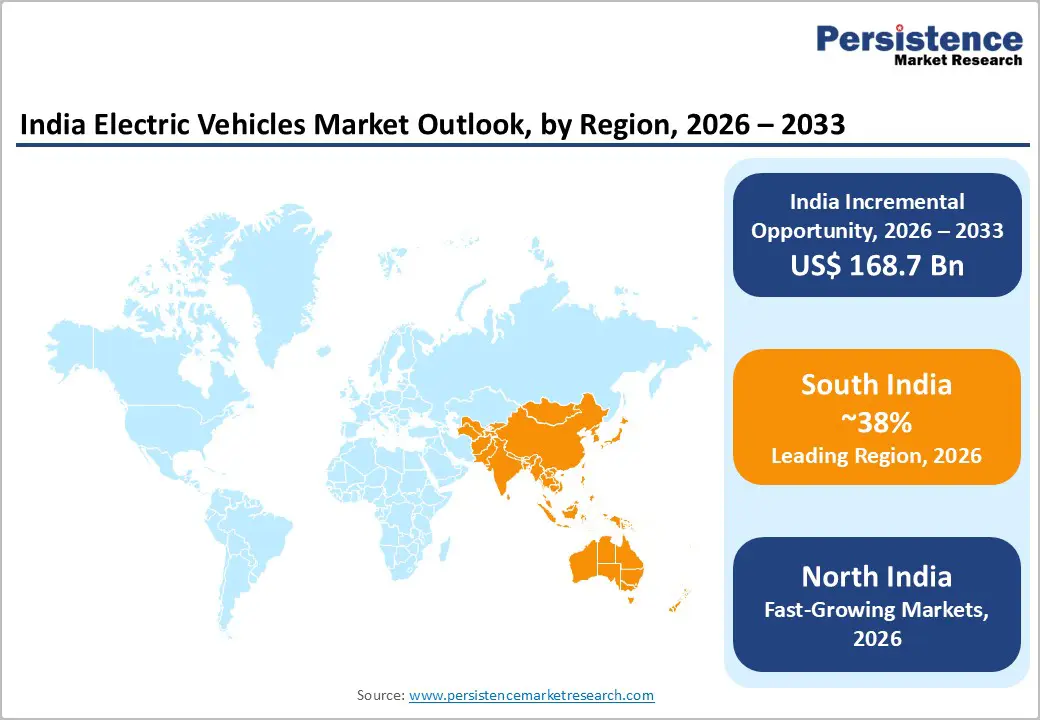

South India, encompassing Karnataka, Tamil Nadu, and Telangana is the leading EV zone in India, accounting for approximately 34% of national EV registrations in 2025 per Vahan portal data. Karnataka's Bengaluru is India's EV startup capital, hosting Ola Electric, Ather Energy, and Bounce Infinity alongside major R&D centers for global EV players. The Karnataka government's Electric Vehicle and Energy Storage Policy 2017 (extended through 2025) offers capital subsidies and road tax exemptions that have driven Bengaluru's EV two-wheeler penetration to among the highest in India.

Tamil Nadu has emerged as a manufacturing powerhouse, with Ola Electric's Gigafactory in Krishnagiri representing the largest single EV manufacturing investment in India. Telangana is aggressively positioning itself as an EV hub through its EV Policy 2020-2030, which targets 50% of all new vehicle registrations to be electric by 2030 in Hyderabad. The zone's strong IT sector workforce also correlates with higher EV affordability and early technology adoption rates.

North India Electric Vehicles Market Trends

North India comprising Delhi NCR, Uttar Pradesh, and Haryana is the second-largest EV zone and the fastest growing, driven by acute air quality crises and aggressive state-level policy interventions. Delhi has the most comprehensive EV policy in India under the Delhi EV Policy 2020, which provides purchase incentives of up to INR 30,000 per electric two-wheeler and has driven Delhi's EV share of new vehicle registrations to approximately 12% in FY2024 per Delhi Transport Department data.

Uttar Pradesh India's most populous state represents the largest untapped EV demand pool in the country, with the UP EV Manufacturing and Mobility Policy 2022 attracting investments from Hero Electric, Yulu, and Greaves Cotton. Haryana hosts major EV supplier manufacturing facilities and is a critical component in the Delhi NCR EV supply chain ecosystem, contributing precision components to multiple two-wheeler and four-wheeler EV programs.

West India Electric Vehicles Market Trends

West India encompassing Maharashtra and Gujarat is a strategically critical EV zone combining India's financial capital with its most EV-manufacturing-intensive state. Maharashtra's EV Policy 2021 targets 10% EV penetration by 2025 and 30% by 2030, providing purchase incentives and waiving road tax on EVs. Mumbai and Pune are seeing rapid electric three-wheeler and e-bus fleet deployments, with the Pune Municipal Corporation operating India's largest city-level e-bus fleet under PMPML contracts.

Gujarat has positioned itself as India's premier EV manufacturing destination, hosting Tata Motors' electric passenger car assembly lines in Sanand and Suzuki Motor Corporation's upcoming EV facility in Hansalpur. The state's Gujarat Electric Vehicle Policy 2021 offers capital subsidies up to INR 10,000 per kWh of battery for EVs manufactured in the state, reinforcing Gujarat's attractiveness as an EV production hub that will serve both domestic and export demand.

East India Electric Vehicles Market Trends

East India comprising Odisha and West Bengal is an emerging EV zone with significant growth potential underpinned by improving infrastructure and state-level policy momentum. West Bengal's EV Policy 2021 exempts EVs from registration fees and road tax, and Kolkata has committed to full electrification of its city bus fleet by 2030 under the Smart Cities Mission. The state's dense urban population and high two-wheeler usage create a natural EV adoption base, with Hero Electric and Greaves Cotton expanding dealership networks in Kolkata and Howrah.

Odisha is increasingly attracting EV component manufacturing investment due to its rich mineral resources including lithium and cobalt deposits identified in the Nayagarh district and the state government's Odisha EV Policy 2021, which waives motor vehicle tax and provides capital investment subsidies of up to INR 5 crore for EV manufacturers establishing operations in the state. Odisha's strategic location and improving logistics connectivity are positioning it as a future supply chain node for East India's EV ecosystem.

Competitive Landscape

The competitive landscape of the India electric vehicle market is moderately fragmented, with domestic manufacturers accounting for more than 65% of total EV registrations in 2025. Tata Motors remains the clear leader in the electric passenger vehicle segment, holding over 50% market share, supported by its strong product portfolio, extensive dealership presence, and first-mover advantage in affordable EVs. MG Motor India is rapidly strengthening its market position through technologically advanced and premium electric vehicle offerings.

The electric two-wheeler segment is highly competitive, led by Ola Electric, followed by TVS Motor Company and Bajaj Auto, collectively dominating overall E-2W sales. Competition among manufacturers is increasingly driven by battery range, charging infrastructure integration, connected vehicle technologies, software capabilities, pricing strategies, and aftersales service network expansion.

Manufacturers are also heavily investing in localized battery manufacturing, charging ecosystem development, and OTA-enabled smart mobility platforms to strengthen competitive positioning. Emerging business models such as battery swapping, battery-as-a-service (BaaS), fleet electrification partnerships, and subscription-based ownership models are gaining traction as companies aim to reduce upfront ownership costs and accelerate mass-market EV adoption. Additionally, the rapid growth of electric two-wheelers continues to remain the primary growth engine of India’s EV industry.

Key Developments:

- In 2026, Maruti Suzuki will launch the e-Vitara electric SUV with localized manufacturing, battery rental solutions, improved affordability, and Toyota collaboration to strengthen its position in India’s growing passenger EV market.

- In 2026, Royal Enfield plans to introduce the Flying Flea electric motorcycle, combining retro-inspired styling, lightweight architecture, premium positioning, and advanced connected technologies for electric motorcycle enthusiasts.

- In 2026, Ola Electric will expand its affordable Gen-3 electric scooter lineup with improved battery efficiency, software-driven features, lower production costs, and stronger penetration into India’s mass-market EV segment.

- In 2026, Tata Motors plans to expand its Prima electric truck portfolio to support fleet electrification, logistics decarbonization, connected vehicle technologies, and sustainable freight transportation across India’s commercial vehicle industry.

- In 2025, Mahindra & Mahindra partnered with Volkswagen Group to access MEB electric platform components and accelerate next-generation electric SUV development and manufacturing capabilities in India.

- February 2025: Ola Electric launched its Roadster electric motorcycle series at the Bharat Mobility Global Expo, targeting India's large commuter motorcycle segment with a range of up to 579 km and plans for 50 GWh battery cell production at its Krishnagiri Gigafactory by 2026.

- January 2025: Tata Motors unveiled the Harrier EV and Sierra EV at Bharat Mobility 2025, reinforcing its SUV-segment EV leadership with claimed ranges of 500+ km and V2G (vehicle-to-grid) bi-directional charging capability for the Indian market.

- March 2024: Bajaj Auto launched the Chetak 2901 electric scooter with enhanced 123 km range and expanded its charging partner network to over 100 cities, targeting Tier-2 and Tier-3 city EV adoption in India.

Companies Covered in India Electric Vehicles Market

- Tata Motors Limited

- Ola Electric Mobility Pvt. Ltd.

- Bajaj Auto Limited

- Hero Electric Vehicles Pvt. Ltd.

- TVS Motor Company Limited

- Ather Energy Pvt. Ltd.

- Mahindra Electric Mobility Limited

- MG Motor India (SAIC Motor)

- Hyundai Motor India Limited

- Maruti Suzuki India Limited

- Olectra Greentech Limited

- Greaves Cotton Limited (Ampere Electric)

- Sun Mobility

- Bounce Infinity (Bounce Mobility Pvt. Ltd.)

- Revolt Intellicorp Pvt. Ltd. (Hero MotoCorp)

- BYD India Pvt. Ltd.

- Volvo Auto India

- Amara Raja Energy & Mobility Ltd.

Frequently Asked Questions

India Electric Vehicles market is valued at US$ 26.2 Bn in 2026 and is projected to reach US$ 194.9 Bn by 2033, growing at a CAGR of 33.2%. This represents an incremental opportunity of approximately US$ 168.7 Bn, making India one of the world's most significant EV market expansion stories of the decade.

The primary drivers are India's comprehensive government policy framework FAME II, PM e-DRIVE, and PLI ACC battery schemes that collectively subsidize EV purchases and build domestic manufacturing capacity. Surging fuel costs, rapid two-wheeler electrification (electric scooters comprising over 57% of EV registrations in FY2024 per Vahan data), and expanding urban charging infrastructure are reinforcing organic consumer-led demand alongside policy support.

Electric Scooters are the dominant Vehicle Type segment with approximately 42% of total EV registrations in 2025. Their leadership reflects India's structural two-wheeler dependence over 75% of Indian households own a two-wheeler and the economic attractiveness of EV scooters at cost parity with ICE equivalents under FAME subsidy regimes. Ola Electric, TVS iQube, and Bajaj Chetak lead this segment.

South India leads with approximately 34% of national EV registrations in 2025. Karnataka's Bengaluru hosts Ola Electric and Ather Energy headquarters alongside major R&D centers; Tamil Nadu houses Ola Electric's Gigafactory; and Telangana's EV Policy 2020-2030 targets 50% EV registration share in Hyderabad by 2030. The zone's IT sector affluence also supports higher EV affordability and early adoption rates.

The most significant opportunity is the scale-up of domestic battery cell manufacturing under the PLI ACC scheme (50 GWh target). With Ola Electric's Gigafactory and Amara Raja's facilities operationalizing through 2026-2028, domestic production will reduce India's 70%+ lithium cell import dependency, structurally lowering EV battery costs and unlocking mass-market passenger car and commercial vehicle electrification at price points accessible to the Indian middle class.

Leading companies include Tata Motors (65%+ electric passenger car share), Ola Electric (35%+ electric scooter share), Bajaj Auto (Chetak platform), TVS Motor (iQube), Hero Electric, Ather Energy, Mahindra Electric Mobility, MG Motor India (BYD-powered platforms), Hyundai India (Creta EV, IONIQ 5), Olectra Greentech (electric buses), and Amara Raja Energy & Mobility (battery manufacturing), among others.