- Advanced Materials

- Thermal Insulation Materials Market

Thermal Insulation Materials Market Size, Share, and Growth Forecast, 2025 - 2032

Thermal Insulation Materials Market by Material Type (Glass Wool, Mineral Wool, Expanded Polystyrene (EPS), Calcium-Magnesium-Silica (CMS) Fibers, Others), End-Use Industry (Construction, Automotive, HVAC, Industrial, Others), and Regional Analysis for 2025 - 2032

Thermal Insulation Materials Market Share and Trends Analysis

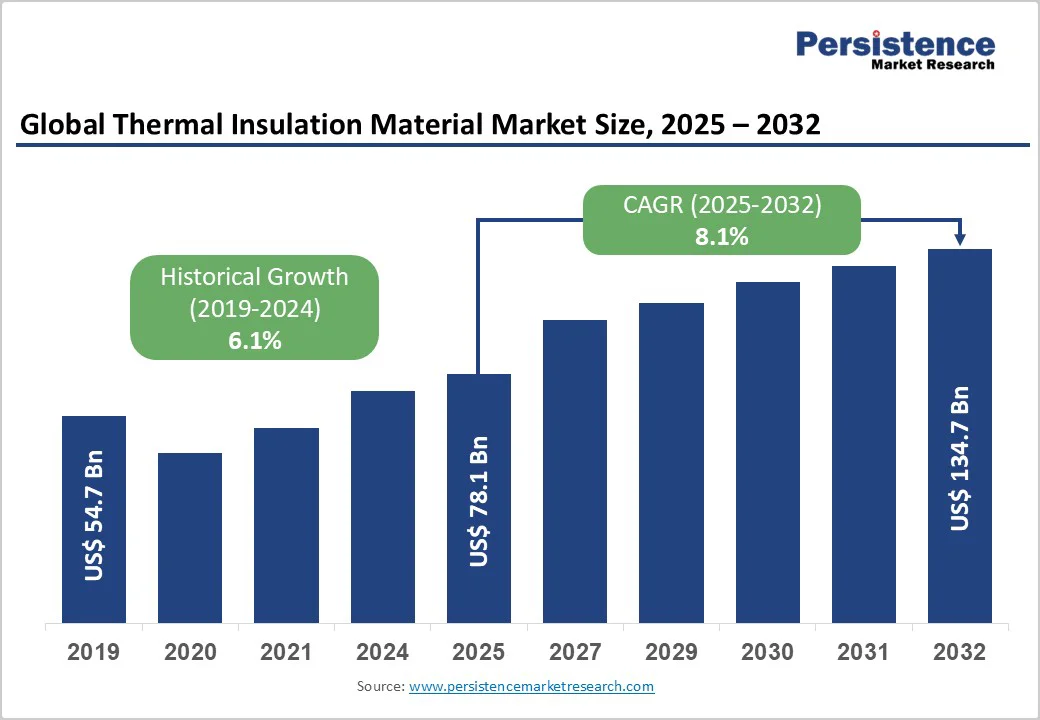

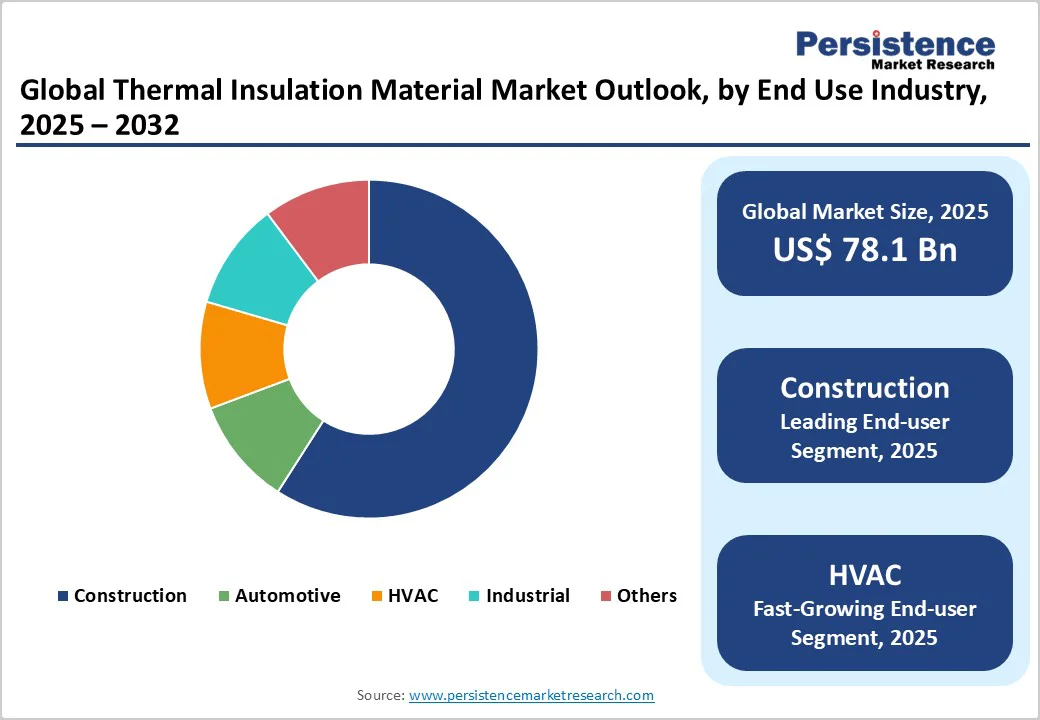

The global thermal insulation materials market size is likely to be valued at US$78.1 billion in 2025, and is projected to reach US$134.7 billion by 2032, growing at a CAGR of 8.1% during the forecast period 2025-2032. Surging urbanization, stricter regulatory mandates for energy efficiency, and an accelerated transition toward sustainable building standards globally are key factors driving market growth.

Supportive government incentives, alongside the momentum for green building in both developed and emerging economies, are further strengthening demand for thermal insulation materials.

Key Industry Highlights

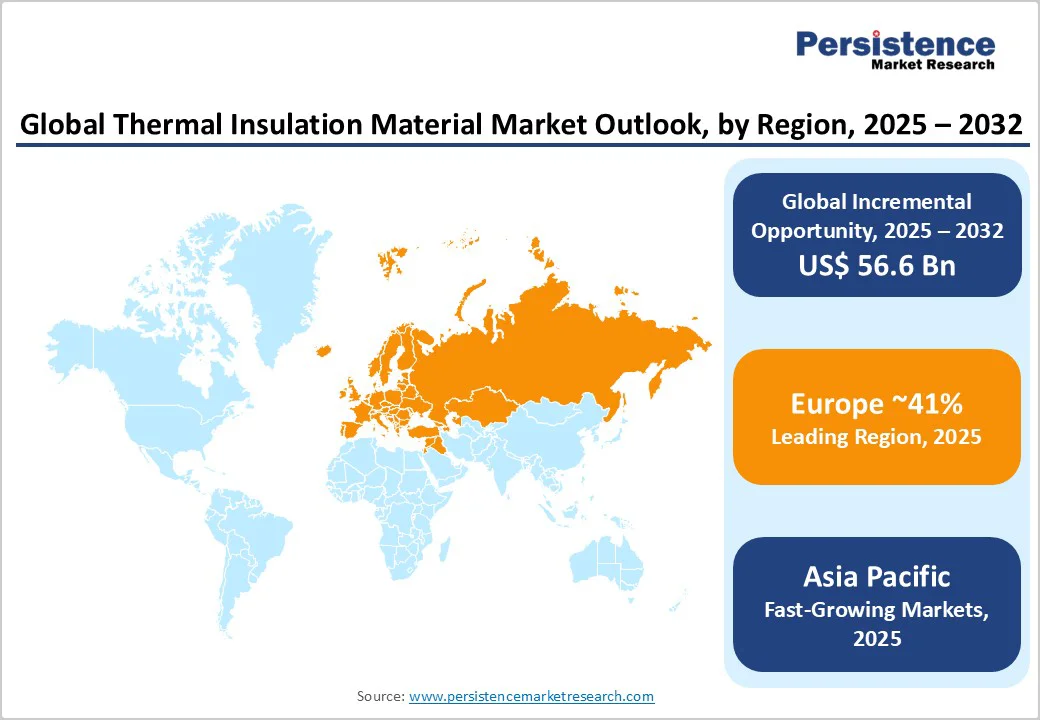

- Regional Leader: Europe is set to be the largest thermal insulation materials market in 2025, driven by stringent government energy efficiency regulations and the wide adoption of green building standards.

- Fastest-growing Regional Market: Asia Pacific is expected to be the fastest-growing regional market through 2032, with innovation-driven adoption fueled by smart retrofitting, regulatory upgrades, and expanding heating, ventilation, and air conditioning (HVAC) and cold-chain sectors.

- Leading Material: Glass wool is likely to dominate the thermal insulation materials market share in 2025, owing to its energy efficiency, acoustic benefits, and wide suitability across residential and commercial projects.

- Fastest-growing End-Use Industry: HVAC insulation and retrofitting applications represent the fastest-growing opportunity, responding to decarbonization and energy management imperatives.

- Market Drivers: Government regulations, green building codes, and corporate ESG commitments are boosting demand for insulation in new constructions and retrofits.

- Market Opportunity: Smart insulation systems and green retrofits offer the greatest opportunity, driven by emerging technologies in materials science and rising ESG-related investments.

| Key Insights | Details |

|---|---|

|

Thermal Insulation Materials Market Size (2025E) |

US$78.1 Bn |

|

Projected Market Value (2032F) |

US$ 34.7 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

8.1% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

6.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Energy-Efficient and Sustainable Buildings

The growing global emphasis on energy efficiency is a key driver of the thermal insulation materials market. Buildings account for a significant share of global energy consumption, often accounting for over 30% of total energy and generating close to 40% of annual carbon emissions. Stringent energy codes, such as the European Union (EU)’s Energy Performance of Buildings Directive (EPBD) and various national mandates, are enforcing minimum insulation standards, driving the adoption of advanced thermal insulation in both new construction and renovation projects. These regulations frequently mandate higher insulation thickness and performance, supported by incentives such as tax credits and rebates. This has made energy-efficient insulation not just a compliance measure, but a critical strategy for enhancing asset value, reducing utility bills, and meeting green building certifications such as Leadership in Energy and Environmental Design (LEED) and Building Research Establishment Environmental Assessment Methodology (BREEAM).

Another robust market driver is the rapid pace of innovation in materials and technology. Manufacturers and research bodies have been developing insulation solutions with enhanced thermal efficiency, improved durability, increased fire resistance, and improved environmental profiles. Recent advancements include high-performance products such as vacuum-insulated panels (VIPs), aerogels, phase change materials (PCMs), and rare-earth nanoinulations. Advancements in nanotechnology are enabling insulation materials with ultra-low conductivity and enhanced fire-retardant properties at reduced thickness, supporting the needs of modern, high-density construction.

High Initial Capital Costs for Advanced Materials and Retrofitting

Notwithstanding their significant long-term operational savings, the upfront investment in cutting-edge thermal insulation, especially for aerogels, VIPs, and other advanced materials, remains a barrier, particularly in cost-sensitive regions and retrofit scenarios.

Advanced insulation technologies often require specialized installation and incur higher material costs than traditional options such as glass wool or expanded polystyrene. Such price differences are more pronounced in developing economies, slowing replacement cycles and the penetration of next-generation insulants. Retrofitting older buildings, which often lack the structural readiness for modern materials, further escalates costs, sometimes leading to delays or less comprehensive upgrades, despite strong government incentives and mandatory requirements in some regions.

Emergence of Sustainable and Bio-Based Insulation Materials: Unlocking Market Potential

The concerted movement toward sustainability and circular economy principles is opening significant growth avenues for eco-friendly and bio-based insulation materials. Increasing regulatory pressure to reduce carbon footprints, combined with rising consumer awareness of environmental impacts, is accelerating the replacement of petrochemical-based insulators with renewable and recyclable alternatives. Manufacturers are actively developing natural fiber insulation made from hemp, cellulose, wool, cork, and recycled textiles, offering excellent thermal performance, low embodied carbon, and superior indoor air quality.

Moreover, the proliferation of HVAC and industrial insulation applications represents a major opportunity for the thermal insulation materials market players. Rising demand for energy-efficient HVAC systems, driven by urbanization, infrastructure modernization, and stricter energy codes, is accelerating the adoption of advanced insulation materials. In both residential and commercial construction, effective insulation is essential to minimize energy losses, enhance indoor comfort, and meet green building certification standards such as LEED and BREEAM. The industrial sector, too, is ramping up investments in thermal management and process insulation to reduce operational costs and comply with carbon reduction mandates. High-temperature insulation solutions, including mineral wool, aerogels, and microporous silica, are gaining prominence in equipment, pipelines, and storage facilities.

Category-wise Analysis

Material Type Insights

Glass wool is projected to maintain its leading position in the thermal insulation materials market, accounting for about 25% of total revenue in 2025, owing to its thermal efficiency, acoustic damping, low combustibility, and cost-effectiveness. Its versatility and superior insulation properties make it a popular choice for new constructions and retrofit projects across residential, commercial, and industrial sectors. With energy-efficient building initiatives rising globally, glass wool is increasingly selected for walls, roofs, floors, and HVAC applications, delivering significant reductions in heating and cooling costs and enhancing indoor comfort.

The intensifying emphasis on green building certifications and sustainability has further driven innovation in the segment, with manufacturers prioritizing eco-friendly production processes, increasing recycled glass content, and improving fire resistance to comply with stricter safety regulations. As rapid urbanization and stricter building codes fuel demand for efficient, sustainable insulation, easy installation and high energy performance of glass wool will continue to reinforce its industry leadership.

End-Use Industry Analysis

The construction sector is poised to dominate in 2025, capturing approximately 55% of the thermal insulation materials market. This includes both residential and commercial buildings, where rising urbanization, energy codes, and sustainability mandates are driving large-scale adoption of insulation. Government incentives and rising consumer awareness of thermal comfort and energy savings are advancing the segment, with residential construction particularly outpacing traditional industrial use. Notably, building insulation materials are increasingly specified to reduce heat loss, optimize HVAC performance, and comply with stringent certification systems worldwide.

The HVAC segment is forecasted to be the fastest-growing from 2025 to 2032, driven by a soaring demand for energy-efficient heating, ventilation, and air conditioning systems across residential, commercial, and industrial buildings. Stricter energy efficiency regulations, coupled with the expansion of cold-chain logistics and industrial facilities, are fueling the adoption of high-performance insulation solutions.

Regional Insights

North America Thermal Insulation Materials Market Trends

North America is expected to hold a prominent position in the market, led by the United States and propelled by rigorous building codes, advanced innovation ecosystems, and diversified end-use segments such as construction, industrial, and HVAC. Federal and state government initiatives, including incentives for home retrofitting and compliance with the International Energy Conservation Code (IECC), are set to accelerate market penetration. Recent years have seen substantial investments in energy-efficient building upgrades, with manufacturers aligning R&D activity toward smart and eco-friendly solutions to sustain a competitive edge and regulatory alignment.

Expanding cold chain logistics for pharmaceuticals and renewables have also broadened market horizons in North America. The capacity of the U.S. to commercialize innovations, such as smart insulation monitors and climate-adaptive materials, positions North America as a key contributor to global insulation technologies.

Europe Thermal Insulation Materials Market Trends

Europe is predicted to maintain a commanding hold on the thermal insulation materials market share in 2025, powered by a well-established policy framework, spearheaded by Germany, the U.K., and France. Harmonization of energy efficiency regulations, such as the Energy Performance of Buildings Directive, and deepening integration of green building certifications, mainly BREEAM and LEED, have enabled consistent insulation standards across member states. Germany’s strict renovation mandates and incentives for energy upgrades, as well as the U.K.’s multi-billion-pound insulation schemes, continue to propel demand.

Local manufacturers have been investing heavily in recyclability and bio-based advancements, while innovation in nanotechnology, fire-resistant insulation, and digital construction practices catalyze differentiation in mature markets. The successful alignment of sustainability policy and industry innovation across the EU has become a template for other developed and developing economies.

Asia Pacific Thermal Insulation Materials Market Trends

Asia Pacific, led by China, India, and ASEAN nations, is slated to be the fastest-growing regional market, projected to secure roughly 37% of the market share in 2025. Surging urbanization, escalating energy prices, and a robust pipeline of residential and industrial projects fuel growth. National policies, such as China's energy transition initiative and India’s Housing for All, have been strongly promoting the uptake of insulation materials across building types. The regional market can make significant gains from cost-effective labor, abundant primary resources, and proximity to high-growth end-user industries, in particular, manufacturing and electronics.

Technology transfer, green building adoption, and government mandates for energy management in public infrastructure have created fertile ground for new product launches, international partnerships, and domestic production scale-ups. Increased investment in smart cities and urban infrastructure further boosts the APAC insulation market outlook.

Competitive Landscape

The global thermal insulation materials market structure is moderately fragmented, with a mix of multinational leaders and regional contenders. Saint-Gobain S.A., Owens Corning, Rockwool International A/S, Kingspan Group, BASF, Knauf Insulation, and Johns Manville form the backbone of the competitive structure, each leveraging extensive R&D, global supply chains, and diversified product portfolios. Strategic mergers, cross-border acquisitions, and continuous innovation in eco-friendly and smart insulation solutions are key differentiation strategies. The emergence of low-carbon insulation manufacturing processes and circular economy models marks a pivotal trend in competitive dynamics.

Key Industry Developments

- In October 2025, Primaloft introduced Ultrapeak, its latest next-generation insulation material designed to deliver enhanced warmth, lightweight performance, and durability. Ultrapeak offers superior thermal retention even in wet conditions, making it ideal for outdoor and activewear applications. This innovation uses advanced fiber technology to provide improved compressibility and breathability, supporting consumer demand for high-performance, eco-friendly insulation solutions.

- In September 2025, Chinese researchers at Tsinghua University developed a breakthrough carbon nanotube insulation material, named super-aligned carbon nanotube films (SACNT-SF), which can withstand temperatures up to 2,600°C, surpassing all existing high-temperature thermal insulation materials. This ultra-thin, flexible insulator exhibits exceptionally low thermal conductivity, effectively blocking heat transfer while remaining lightweight and durable through repeated heating cycles. Its unique structure, with tiny gaps blocking gas molecule movement, makes it ideal for extreme applications such as spacecraft heat shields and industrial furnaces.

- In August 2025, Promix Solutions launched a new Microcell technology that enhances plastic foam production by creating microcellular structures within polymer materials. This innovation improves material strength, reduces weight, and offers better thermal insulation, benefiting automotive, packaging, and construction industries. The Microcell technology also supports sustainability by lowering raw material usage and improving recyclability. Through this advancement, Promix aims to deliver high-performance, lightweight plastic solutions aligned with industry demands for efficiency and environmental responsibility.

Companies Covered in Thermal Insulation Materials Market

- Dow Inc.

- Knauf Insulation

- Saint-Gobain S.A

- Armacell

- Rockwool International A/S

- Owens Corning Inc.

- KCC Corporation

- Covestro AG

- Kingspan Group Plc.

- Recticel Group

- Cabot Corporation

- Aspen Aerogels Inc.

- CNBM Group Co. Ltd.

- Huntsman International LLC

Frequently Asked Questions

The global thermal insulation materials market is projected to reach US$ 78.1 billion in 2025.

Surging construction activities for energy-efficient buildings, government mandates for sustainability, and technological advancements in eco-friendly and smart insulation systems are major market drivers.

The market is poised to witness a CAGR of 8.1% from 2025 to 2032.

Development of smart, retrofit-ready insulation systems for HVAC and energy upgrades, aligned with ESG investments and green building mandates, presents an excellent business opportunity.

Saint-Gobain S.A., Owens Corning, Rockwool International, and Kingspan Group are some of the key players in the market.