- Off-Road Equipment & Machinery

- Gardening and Agriculture Equipment Market

Gardening and Agriculture Equipment Market Size, Share, and Growth Forecast, 2025 - 2032

Gardening and Agriculture Equipment Market By Product Type (Tractors & Implements, Harvesters & Combine Attachments, Others), Application (Commercial Agriculture, Horticulture & Orchards, Others), Technology, and Regional Analysis for 2025 - 2032

Gardening and Agriculture Equipment Market Size and Trends Analysis

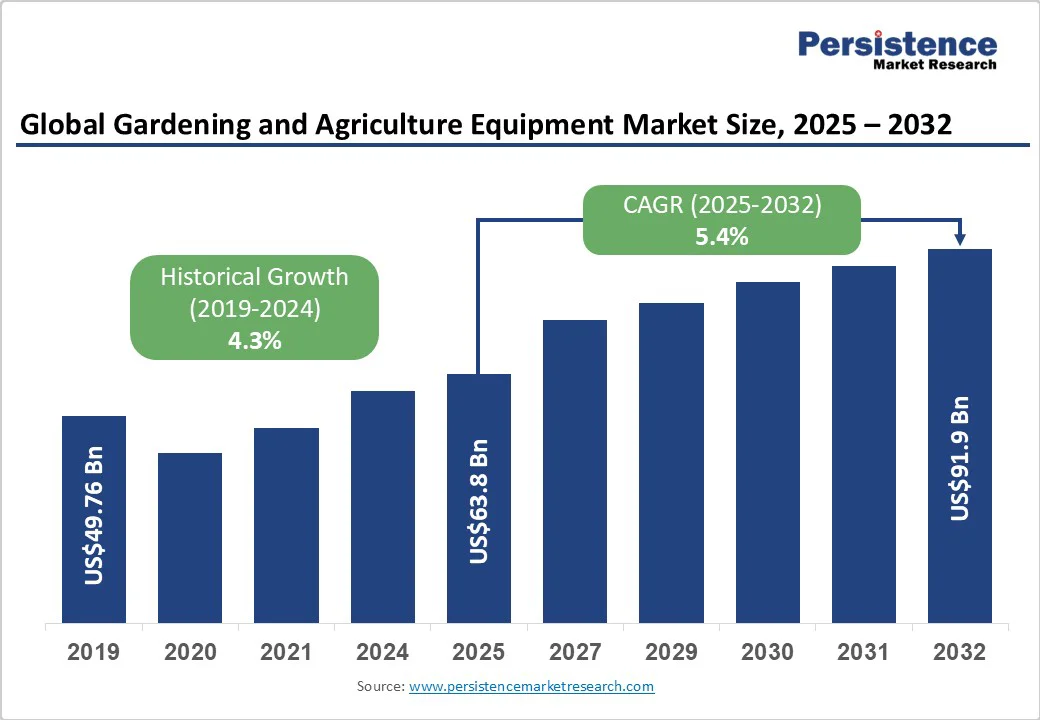

The global gardening and agricultural equipment market size is expected to be valued at US$63.8 billion by 2025. It is expected to reach US$91.9 billion by 2032, growing at a CAGR of 5.4% during the forecast period from 2025 to 2032, driven by precision agriculture adoption, electrification of outdoor power equipment (OPE), and expanding residential gardening/landscaping spend. Farm consolidation and larger capital budgets support demand for high-value tractors and implements.

Key Industry Highlights

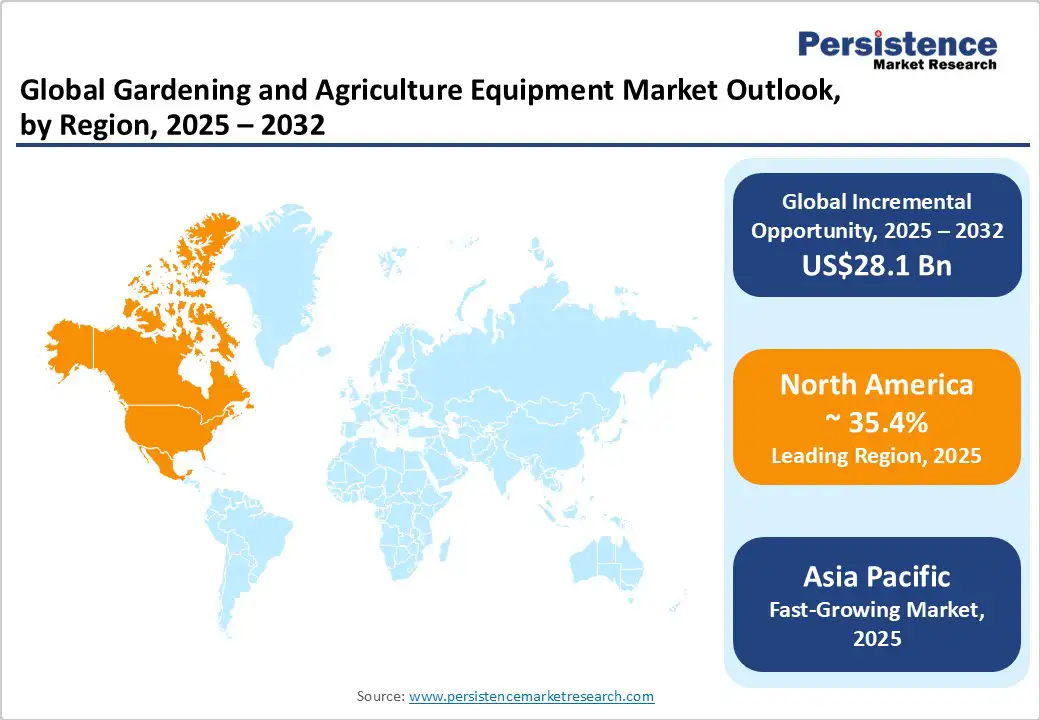

- Leading Region: North America dominates the market, accounting for 35.4% of the total market value in 2025, driven by high residential spending, the adoption of precision agriculture, and advanced farm mechanization.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, due to large-scale mechanization in China and India, strong government subsidy programs, and expanding horticultural activity across ASEAN countries.

- Investment Plans: The industry is witnessing a rise in investments in autonomous and electric machinery, with major OEMs such as John Deere, Kubota, and Mahindra collectively allocating over US$1.2 billion (2024–2025) toward R&D in robotics, telematics, and battery-powered systems.

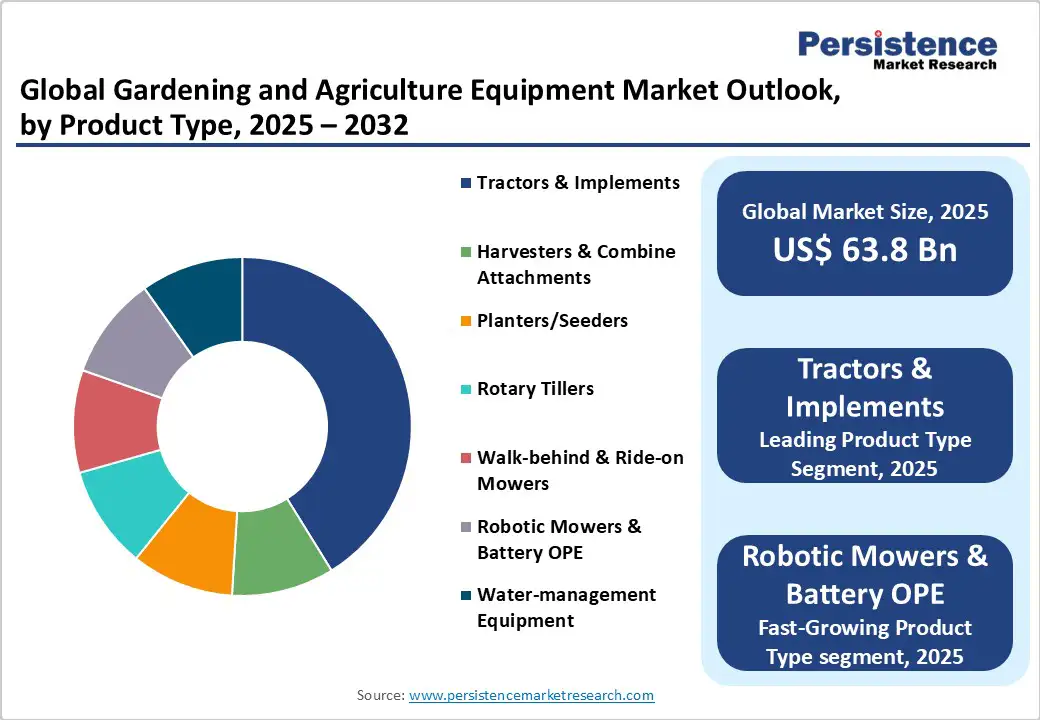

- Dominant Product Type: The tractors & implements equipment segment leads the market with a market share of 42.7% in 2025, supported by farm consolidation trends, precision guidance technologies, and high capital expenditure replacement cycles across major agricultural economies.

- Dominant Application Type: Commercial Agriculture is the largest revenue contributor across the global equipment market, holding a market share of 53.4% in 2025, driven by the extensive use of high-value machinery such as large tractors, combine harvesters, planters, and sprayers.

| Key Insights | Details |

|---|---|

|

Gardening and Agriculture Equipment Market Size (2025E) |

US$63.8 Bn |

|

Market Value Forecast (2032F) |

US$91.9 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Precision Agriculture and Automation Adoption

Farm operators and large agribusinesses are investing in precision agriculture systems, GPS guidance, variable-rate implements, telematics, and automation to raise yields per hectare and reduce input costs. This modernization increases replacement cycles for tractors and implements and raises average selling prices because equipment bundles now include hardware, sensors, and software. The integration of data services drives recurring revenue and strengthens OEM-customer lock-in. On a macro level, this driver correlates with farm consolidation, rising commodity demand, and a continuous need to improve operational efficiency, making precision tools a structural growth engine for commercial agricultural equipment.

Electrification of Outdoor Power Equipment

Battery-electric solutions are rapidly displacing small internal combustion engines in the residential and commercial landscaping segments. Declining battery costs, tighter emissions and noise regulations, and improved performance have driven up demand for battery-powered mowers, trimmers, and robotic mowers. Electrification increases the product mix value and drives aftermarket opportunities for batteries and charging infrastructure. For manufacturers, the shift creates margin pressure on legacy engine businesses while presenting higher-margin potential from integrated electric platforms and related services. The consumer preference for quieter, low-maintenance equipment has materially shifted buying patterns in advanced markets.

Residential Gardening and Landscaping Expansion

Urban greening, rising incomes, and lifestyle shifts toward home gardening are expanding the residential market, driving demand for compact, cordless, and smart garden tools. Alongside commercial landscaping and municipal projects, this dual demand fosters innovation, diversifies revenue streams, and balances high-value farm machinery with high-volume residential equipment.

Barrier Analysis - High Capital Intensity and Limited Financing for Smallholders

Large farms can fund modernization, but smallholders and many SMEs face affordability barriers. Where subsidy and financing programs are absent, the adoption of high-value tractors and precision systems remains constrained, causing uneven regional penetration. This financing gap limits the near-term addressable market in regions where smallholder agriculture predominates and reduces potential upsell into telematics and services. Manufacturers must therefore develop flexible financing and rental models, as well as lower-cost equipment tiers, to unlock growth among smaller operators.

Component Supply Volatility and Lead-Time Risks

Dependence on batteries, power electronics, and semiconductor components increases exposure to raw-material price swings and extended lead times. For electrified OPE and connected agricultural systems, procurement delays can push product launches and inventory replenishment by months and add material cost pressure. This volatility compresses margins and can force OEMs into defensive pricing or inventory build-ups. Effective risk mitigation requires diversified suppliers, longer-term purchase agreements, and clearer product roadmap prioritization.

Opportunity Analysis - Aftermarket Services and Telematics

Connected equipment provides manufacturers with a path to recurring revenue through telematics, predictive maintenance, and consumable products. Monetizing data services, remote diagnostics, and subscription-based software can shift business models from transactional to annuity-style revenue streams, thereby improving margin stability. If telematics penetration of the installed equipment base rises meaningfully, services could represent a notable percentage of the overall industry revenue, improving lifecycle profitability. This opportunity aligns with customer demand for uptime and total cost-of-ownership reduction, and it strengthens customer retention through integrated service offerings.

Robotics and Automation For High-Value Horticulture

Automation for orchards, vineyards, and horticulture, robotic pruning, autonomous harvesters, and micro-robots for precision tasks, addresses severe labor shortages and high manual costs in high-value crops. Early commercial pilots demonstrate viable ROI in select crops and geographies, and scaling these technologies would create a high-growth niche within the larger market. Manufacturers that commercialize reliable robotic solutions can capture premium pricing and recurring service contracts within tightly defined specialty markets.

Financing and Subscription Models

Offering equipment-as-a-service, subscription financing, and certified used equipment programs can unlock demand among cost-sensitive buyers. These models reduce upfront capital requirements, accelerate technology adoption, and expand the buyer pool to SMEs and cooperatives. From an investor perspective, such models create predictable cash flows and higher lifetime customer value. For OEMs, bundling hardware with service packages and flexible payment options helps differentiate offerings and smooth revenue across capex cycles.

Category-wise Insights

Product Type Insights

The tractors & Implements segment leads the market with a market share of 42.7% in 2025. These products include full-size tractors, ploughs, cultivators, and tillage equipment, and are purchased primarily by large commercial farms in North America, Europe, and China. High average selling prices, long replacement cycles, and integration with precision systems (GPS-guided tractors from John Deere, Kubota, or AGCO) contribute to their dominant share. The combination of hardware and optional telematics packages further enhances revenue per unit. For example, GPS-guided planter-tractor combinations provide yield optimization capabilities, which increase ROI for commercial operators and reinforce the purchase of premium equipment models.

Robotic and electrified outdoor power equipment (OPE) represents the fastest-growing sub-segment, driven by urban residential demand and commercial landscaping adoption. Products such as robotic mowers (Husqvarna Automower), battery-powered trimmers (Toro battery trimmers), and small autonomous farm platforms are gaining traction due to ease of use, low maintenance, and regulatory incentives to reduce emissions and noise. Growth is accelerated by declining battery costs, improved motor efficiency, and rising consumer awareness, contributing to both strong unit growth and higher-margin revenues from electrified platforms and associated service packages.

Application Insights

Commercial agriculture is the largest revenue contributor across the equipment market with a market share of 53.4%, primarily due to high-value machinery such as large tractors, combine harvesters, planters, and sprayers. Consolidated farms in the U.S., Germany, and China have the capital to purchase premium models from manufacturers such as Deere & Company, Kubota, and AGCO. These farms also invest in precision agriculture systems and telematics for yield optimization, resulting in significant aftermarket spending on software subscriptions, spare parts, and maintenance. Government subsidy programs, such as the U.S. Farm Bill and EU CAP modernization schemes, further support equipment acquisition, ensuring that this segment maintains a high market share.

Residential and DIY gardening equipment is expanding rapidly, fueled by urbanization, rising disposable income, and lifestyle trends favoring home gardening and small-scale landscaping. Products such as robotic lawn mowers (Husqvarna Automower, Robomow), battery-powered hedge trimmers (Stihl battery range), and compact irrigation systems have high adoption rates among urban homeowners. Although the average selling price is lower than commercial machinery, the large addressable consumer base enables meaningful unit volume growth and opens new distribution channels, including e-commerce, specialty retailers, and subscription rental platforms. Manufacturers leverage brand recognition and innovation to capture recurring revenue through battery replacements and maintenance services.

Regional Insights

North America Gardening and Agriculture Equipment Market Trends - High-Value Mechanization and Electrified Landscaping

North America leads the market in terms of value with a market share of 35.4%, driven by high residential spending and advanced commercial farm mechanization. The U.S. dominates the region, with Canada and Mexico contributing additional market diversity. High-value commercial tractors, combine harvesters, and precision implements account for the majority of revenue. In contrast, residential and commercial landscaping equipment, including robotic mowers, battery-powered trimmers, and compact utility machines, support a large consumer base in suburban and urban areas.

The U.S. market features high tractor prices and strong demand for aftermarket services, with widespread adoption of precision agriculture tools, including GPS-guided planters and telematics-enabled harvesters. Electrified OPE, including robotic mowers from Husqvarna and Toro, dominates suburban markets, while mid-sized landscaping equipment remains popular among commercial operators. Growth is driven by farm consolidation, capital expenditure cycles, and rising demand for battery-powered tools. Emission and noise regulations are accelerating the electrification of small engines, while subsidies and financing programs continue to support farm modernization and municipal investment in green infrastructure.

Asia Pacific Gardening and Agriculture Equipment Market Trends - Volume-Led Expansion Backed by Subsidies and Local Manufacturing

The Asia Pacific serves as the volume engine for the market, driven by its large agricultural base in China, India, and Southeast Asia, as well as regional manufacturing advantages. While average selling prices are generally lower than in North America or Europe, high unit volumes and rapid adoption rates drive significant market value. China and Japan lead in the manufacturing and adoption of advanced equipment, including large-scale tractors, harvesters, and precision implements. In contrast, India demonstrates rapid volume growth, supported by government subsidy programs, rural mechanization initiatives, and affordable financing solutions. ASEAN markets, including Thailand, Vietnam, and Indonesia, are expanding in horticulture, smallholder modernization, and the landscaping machinery sector.

Food-security priorities, government incentives for mechanization, and localized manufacturing that ensures competitive pricing are key growth drivers. Battery-powered lawn and garden equipment, including robotic mowers and compact tractors for small farms, is an emerging trend in rapidly urbanizing regions. In China, manufacturers such as Foton Lovol and YTO Group have invested in autonomous tractor platforms and electric garden machinery. Meanwhile, India is seeing growth in compact, battery-operated implements from brands like Mahindra and Sonalika. Regulatory maturity varies widely across the region, resulting in uneven adoption of high-value precision systems. Import tariffs, localization incentives, and government mechanization programs influence OEM strategy and market entry timing.

Europe Gardening and Agriculture Equipment Market - Innovation-Led Growth with Battery Tech and Precision Autonomy

Europe represents a significant segment of the market, with Germany, France, the U.K., and Spain accounting for the majority of revenue. The region combines strong engineering capabilities with robust demand for premium garden equipment among consumers. Germany dominates in high-value agricultural machinery, exporting advanced tractors, combine harvesters, and precision implements, while the U.K. and France maintain high activity in municipal landscaping and commercial garden equipment. Spain contributes through specialized horticultural machinery and small-scale harvesting solutions, reflecting diverse regional agricultural practices.

Strict environmental regulations and government incentives for low-emission machinery are fueling Europe’s market growth. Manufacturers are adopting battery-powered systems, robotics, and telematics across residential and commercial equipment. A robust aftermarket network in Germany and France supports the adoption of high-value machinery. Harmonized EU standards on emissions and safety spur innovation but raise compliance costs. National subsidies, such as Germany’s renewable energy and mechanization programs, shape technology choices. Recent trends include battery-powered robotic mowers, precision-autonomy tractors, and telematics-enabled farm management software, underscoring Europe’s innovation-led, sustainability-driven market landscape.

Competitive Landscape

The global gardening and agriculture equipment market is mixed in concentration, heavy machinery is consolidated among major OEMs, while gardening and small OPE remain fragmented across regional brands. Leaders dominate high-value segments such as tractors and precision systems, while smaller players serve niche markets. Consolidation opportunities exist in robotics and software.

Market leaders focus on electrification, telematics, and diversified channels, emphasizing integrated hardware-software solutions, financing options, and strong service networks. Emerging models highlight product-as-a-service and data-driven crop optimization strategies.

Key Industry Developments

- In January 2025, Deere & Company unveiled its second-generation autonomous tractors and a battery-electric commercial landscaping mower at CES, along with retrofit autonomy kits for existing equipment to accelerate adoption.

- In August 2025, AGCO announced it would showcase retrofit solutions, autonomous technology, and precision agriculture enhancements across its Fendt, Massey Ferguson, and PTx brands at the Farm Progress Show in Decatur, Illinois.

- In February 2025, Anker’s Eufy brand launched two new robotic lawn mowers -E15 and E18, featuring Vision Full-Self Driving (V-FSD 1.0) technology for object avoidance and edge detection.

Companies Covered in Gardening and Agriculture Equipment Market

- Deere & Company

- AGCO Corporation

- Kubota Corporation

- Husqvarna Group

- The Toro Company

- Honda Motor Co., Ltd.

- Andreas Stihl AG & Co. KG

- Briggs & Stratton

- Mahindra & Mahindra

- Generac Power Systems

- Robert Bosch GmbH

- Hitachi Construction Machinery

- Emak Group

- Yanmar Co., Ltd.

- Fendt

- Valtra

- Sonalika Tractors

- Alamo Group

- Ferris Industries

- Ecorobotix

Frequently Asked Questions

The market size was valued at US$63.8 Billion in 2025.

By 2032, the gardening and agriculture equipment market is projected to reach US$91.98 Billion.

Key trends include the growing adoption of battery-electric and autonomous solutions across residential and commercial segments, along with increasing integration of precision agriculture and telematics technologies to enhance yield, efficiency, and real-time operational control.

In end-use commercial agriculture holds the largest revenue share of 53.2% in 2025, due to high-value machinery such as tractors, harvesters, and precision implements.

The gardening and agriculture equipment market is expected to grow at a CAGR of 5.4% from 2025 to 2032.

Major companies include Deere & Company, AGCO Corporation, Kubota Corporation, Husqvarna Group, and The Toro Company.