- Sensors & Controls

- Compact Inverter Technology Market

Compact Inverter Technology Market Size, Share, and Growth Forecast 2025 - 2032

Compact Inverter Technology Market by Power Output (Up to 0.5 kW, 0.5 to 1 kW, 1 to 5 kW, 5-10 kW, Above 10 kW), Phase (Single Phase, Three Phase), Output Voltage (Up to 240 V, Above 240 V), by Applications (Residential, Commercial, Industrial), by Regional Analysis, 2025 - 2032

Compact Inverter Technology Market Size and Trend Analysis

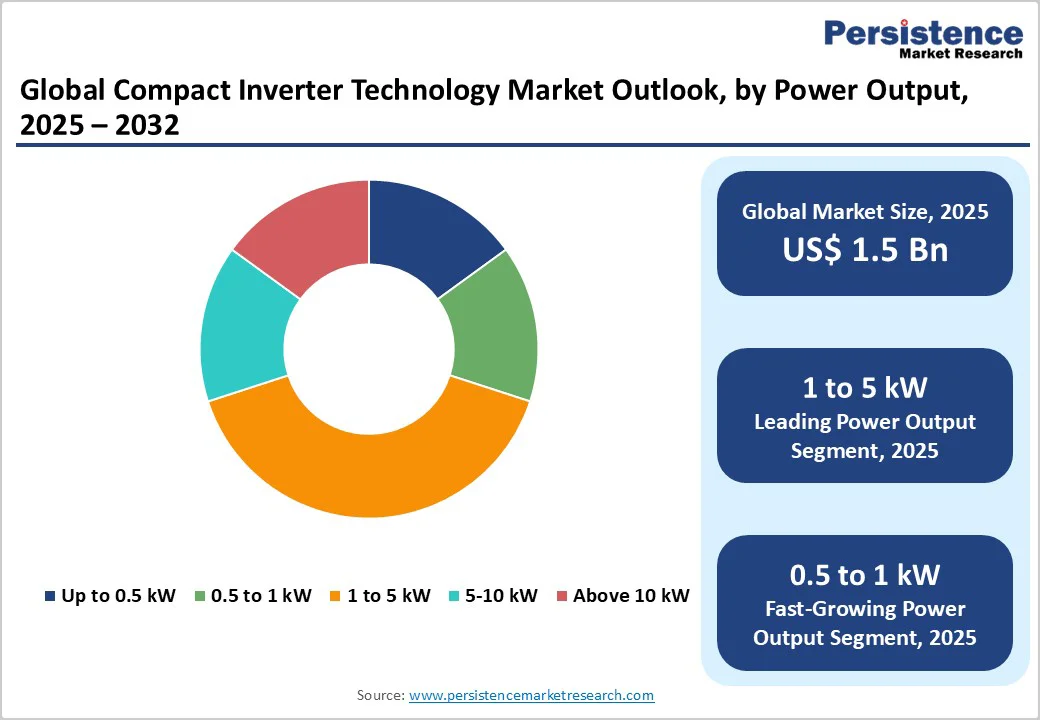

The global compact inverter technology market size is valued at US$ 1.5 billion in 2025 and is projected to reach US$ 2.9 billion by 2032, growing at a CAGR of 9.8% between 2025 and 2032.

This remarkable trajectory reflects the deployment of renewable energy infrastructure, particularly solar and wind power systems, which require efficient DC-to-AC conversion technologies. The market expansion is further accelerated by the proliferation of electric vehicles requiring advanced charging infrastructure, increasing adoption of portable power solutions for emergency preparedness and remote applications, and the rising consumer preference for energy-independent systems.

Key Market Highlights

- Leading Region: North America dominates compact inverter technology demand with 34% global market share in 2025, driven by extraordinary renewable energy deployment in U.S. and Canada.

- Fastest Growing Region: Asia Pacific expands at 12% CAGR through 2032, substantially outpacing other geographic regions due to accelerated renewable energy infrastructure investment to meet rising electricity demand.

- Dominant Segment: 1 to 5 kW Power Output commands 40% market share across all applications, driven by residential rooftop solar adoption and small commercial installations where this power rating optimally aligns with customer electricity consumption patterns.

- Fastest Growing Segment: Commercial Applications expand at 11% CAGR through 2032, reflecting business sector adoption of solar-plus-storage systems and advanced inverter technologies enabling grid services, carbon footprint reduction, and energy cost optimization.

- Key Market Opportunity: Battery Energy Storage Integration creates exceptional growth prospects as BESS requiring compact bidirectional inverters enabling vehicle-to-grid functionality, demand response participation, and peak shaving applications.

| Key Insights | Details |

|---|---|

| Compact Inverter Technology Market Size (2025E) | US$ 1.5 Billion |

| Market Value Forecast (2032F) | US$ 2.9 Billion |

| Projected Growth CAGR (2025 - 2032) | 9.8% |

| Historical Market Growth (2019 - 2024) | 8.6% |

Market Dynamics

Drivers - Rising Renewable Energy Adoption and Grid Integration Requirements

The global renewable energy landscape is undergoing transformative change, with solar and wind power installations achieving record capacity additions. According to the International Renewable Energy Agency (IRENA), global renewable energy capacity grew by 15.1% in 2024 to reach 4,448 gigawatts (GW), with solar accounting for over three-quarters of the new capacity additions.

India alone added 24.54 GW of solar capacity in 2024, representing a remarkable 145% increase from 2023, while the United States installed 31 GW of solar capacity in 2023, comprising 5% of total electricity demand.

Compact inverters play a pivotal role in these renewable energy systems, converting direct current generated by solar panels and battery storage into alternating current suitable for residential consumption, commercial operations, and grid distribution.

The escalating deployment of distributed energy resources, microgrids, and decentralized power generation systems necessitates increasing quantities of compact, efficient inverter solutions that can seamlessly integrate with existing electrical infrastructure and support bidirectional power flow.

Technological Advancements in Semiconductor Materials and Power Density Improvements

Wide-bandgap semiconductor technologies, including silicon carbide (SiC) and gallium nitride (GaN), are revolutionizing compact inverter performance by enabling significantly higher efficiency, faster switching frequencies, and superior thermal management capabilities.

Unlike traditional silicon-based components, SiC MOSFETs demonstrate conduction losses up to 30-40% lower than silicon IGBTs while enabling operation at higher voltages and temperatures without performance degradation. GaN devices achieve switching frequencies exceeding 100 kHz, compared to 20 kHz for conventional silicon devices, resulting in dramatic reductions in inverter size, weight, and cooling requirements.

These semiconductor advancements facilitate the development of compact inverters with power density improvements exceeding 200% relative to previous-generation designs, enabling manufacturers to create highly portable, lightweight solutions for residential, commercial, and industrial applications.

The continuous refinement of wide-bandgap semiconductor manufacturing processes is progressively reducing component costs, making advanced inverter technology economically accessible to broader market segments.

Restraints - High Manufacturing Costs and Semiconductor Supply Chain Vulnerabilities

The compact inverter market continues to face elevated production costs due to persistent semiconductor shortages and concentrated global supply chains. Manufacturers rely heavily on critical components such as IGBTs, PCBs, and discrete semiconductors sourced primarily from Taiwan, South Korea, and Mainland China, making the industry highly sensitive to geopolitical and logistics disruptions.

Capacity constraints at major foundries have pushed component procurement costs up by 15-25% annually. Additionally, manufacturing in developed economies remains significantly more expensive, with U.S. fabrication costs roughly 35% higher than Asia. These cost pressures raise end-user prices, restricting adoption in cost-sensitive markets and slowing penetration in emerging economies.

Complex Integration Challenges and Grid Interconnection Regulatory Requirements

Integrating compact inverters into existing electrical networks poses technical challenges due to variations in global grid standards, voltage classes, and protection requirements. Manufacturers must design region-specific inverter models to comply with diverse interconnection regulations, including increasingly strict European grid codes focused on stability, harmonic control, and advanced grid-support functions.

Achieving grid-forming capabilities requires sophisticated control software and real-time monitoring systems, raising development complexity and cost. Installers and system integrators also require specialized training to configure and maintain advanced inverter systems, creating labor shortages in markets with limited technical expertise. These barriers delay deployment timelines and restrict broader technology adoption.

Opportunity - Explosive Growth in Battery Energy Storage Systems Integration and Vehicle-to-Grid Applications

Battery energy storage systems are expanding at extraordinary growth rates, with the global Energy Storage Systems (ESS) market valued at US$ 92.7 billion in 2025 and projected to reach US$ 181.8 billion by 2032, expanding at 10.2% CAGR. In India specifically, BESS installations increased sixfold in 2024 to 341 MWh, with projections reaching 15 GWh by 2027.

Compact inverters serve as critical enabling technologies for BESS applications, managing bidirectional power flow between battery systems and electrical grids while optimizing energy arbitrage opportunities and demand response capabilities.

The integration of advanced inverter technology with energy storage solutions creates synergistic market opportunities as residential and commercial consumers increasingly adopt solar-plus-storage systems to achieve greater energy independence and resilience against grid disruptions.

Electric vehicle infrastructure expansion presents additional substantial opportunities; grid-forming inverter applications in EV charging stations enable vehicles to provide ancillary grid services through vehicle-to-grid (V2G) and smart charging (V1G) capabilities, transforming EV chargers into controllable energy resources that enhance grid stability while generating revenue streams for charging station operators.

Accelerating Microinverter Adoption in Residential Solar and Decentralized Energy Systems

The solar microinverter market is experiencing exceptional growth with a projected CAGR of 18% through 2032. Microinverters optimize energy production at the individual solar panel level, enabling each module to operate independently and maximizing system efficiency under real-world conditions characterized by shading, soiling, and non-uniform panel orientations.

North American residential rooftop solar PV installations increasingly incorporate microinverters; approximately 36% of new U.S. residential solar systems in 2024 utilized microinverter technology. This shift reflects consumer demand for enhanced monitoring, longer warranties, faster ROI, and reduced single-point failure risks.

Supportive policies-such as net metering, investment tax credits, and feed-in tariffs-continue strengthening project economics. The modularity and scalability of microinverter systems also allow homeowners to expand installations over time, generating recurring revenue opportunities for installers and manufacturers.

Category-wise Analysis

Power Output Insights

The 1 to 5 kW power output segment holds about 40% market share in 2025, driven by strong adoption in residential rooftop solar installations and small commercial systems. This range aligns well with typical household electricity consumption patterns, enabling users to reduce grid dependence while keeping system costs manageable.

Residential solar costs have dropped by nearly 80% over the last decade, making compact inverters in this segment attractive for mass-market consumers. String inverters remain widely used due to their affordability and ease of installation. Although microinverters and energy storage systems are gaining traction, the 1 to 5 kW segment continues to dominate because of established market familiarity and its suitability for most residential solar applications.

Phase Analysis

The three-phase inverter segment leads the market with around 65% share in 2025 due to extensive use in commercial, industrial, and utility-scale renewable energy systems. These inverters support balanced power distribution, lower harmonic distortion, and greater grid stability.

The United States added over 25 GW of new utility-scale solar capacity in 2024, which significantly boosted demand for three-phase systems. Commercial and industrial users increasingly rely on three-phase inverters to meet sustainability goals, reduce energy costs, and integrate large solar arrays efficiently.

Established technology maturity and compliance with standards such as IEEE 1547 and IEC 61727 further support adoption. Single-phase solutions remain important for residential installations but grow at a slower rate.

Output Voltage Insights

The above 240 V output voltage segment accounts for roughly 72% market share in 2025, supported by extensive deployment in industrial and utility-scale solar applications requiring higher voltage distribution. Industrial facilities often operate electrical systems above 400 V, increasing demand for compact inverters that deliver high-voltage output with reduced transmission losses.

Utility-scale solar farms typically use centralized inverters with output voltages between 380 V and 480 V, enabling efficient grid interconnection and economic power transmission. Governments worldwide continue to invest in large renewable energy projects to meet long-term energy transition targets, strengthening the segment’s dominance. Lower-voltage inverters remain relevant for residential and small commercial systems but face slower growth prospects.

Applications Insights

The commercial application segment is the fastest-growing category with an expected CAGR of 11% from 2025 to 2032. Businesses are rapidly adopting rooftop solar systems to reduce electricity expenses, support sustainability commitments, and enhance operational resilience. Commercial buildings offer large roof spaces and benefit from daytime energy use that aligns with solar production.

In 2024, nearly 80% of new U.S. commercial solar projects used advanced inverters with grid support and reactive power capabilities. Incentives under the U.S. Inflation Reduction Act, including a 30% investment tax credit, have strengthened project economics. Industrial applications also expand at a strong pace, driven by energy-intensive sectors such as manufacturing, data centers, and processing industries seeking cost reduction and higher reliability.

Regional Insights

North America Compact Inverter Technology Trends

North America commands nearly 34% of the global compact inverter market in 2025, supported by strong residential and commercial solar adoption. The U.S. installed more than 32 GW of new solar capacity in 2024 (SEIA), marking 28% YoY growth, while residential systems accounted for roughly 40% of additions.

Over 4 million U.S. homes had solar PV installations by mid-2024, with monthly additions averaging 60,000 systems, reinforcing sustained demand for compact residential inverters. The 30% Investment Tax Credit remains the region’s primary policy catalyst, strengthening long-term cost competitiveness across the U.S. Renewable Energy landscape.

Market momentum continues to build through advanced inverter capabilities including real-time monitoring, hybrid PV-storage management, and grid-interactive operation. Utility-scale solar is expanding at remarkable growth rate through 2032, supported by corporate PPAs and increasing electricity prices. Microinverters now account for nearly 35% of U.S. residential installations, driven by demand for module-level optimization and improved performance under shading.

Europe Compact Inverter Technology Trends

Europe accounts for roughly 28% of global compact inverter demand in 2025, driven by some of the world’s most ambitious renewable energy policies. The EU’s legally binding targets require at least 42.5% renewable penetration by 2030, with momentum toward 45%, accelerating distributed solar and storage adoption.

Germany leads Europe with over 14 GW of solar additions in 2024 and cumulative capacity nearing 70 GW, while Spain exceeded 3.5 GW of new capacity amid persistently high electricity prices. The United Kingdom’s Smart Export Guarantee (SEG) continues to incentivize residential PV investments by compensating exported power.

Europe’s regulatory environment demands advanced inverter capabilities-including reactive power control, dynamic frequency response, and LVRT-aligning with evolving EN 50549 standards. These requirements push suppliers to develop grid-forming, high-efficiency compact inverters. Europe’s mature manufacturing base, supported by strong R&D ecosystems, sustains regional leadership in durable, high-performance inverter technologies.

Asia Pacific Compact Inverter Technology Trends

Asia Pacific is the fastest-growing regional market, projected to expand at 12% CAGR through 2032 on the back of extraordinary renewable energy expansion. China remains the dominant contributor, accounting for over half of regional BESS installations and driving massive inverter demand as it advances its 2060 carbon-neutrality roadmap.

India is the second-largest growth engine, with solar additions jumping from 10 GW in 2023 to 24.54 GW in 2024, according to the Ministry of New and Renewable Energy. The CEA projects 74 GW / 411 GWh of storage capacity required by 2032, supporting large-scale inverter deployment.

Japan continues to pioneer advanced grid-forming inverter technologies and intelligent energy management solutions. Rapid renewable growth in Vietnam, Thailand, and Indonesia is fueled by rising energy demand and reduced dependence on imported fossil fuels. Asia’s semiconductor manufacturing dominance and cost-efficient production enable globally competitive pricing, strengthening the regional supply chain advantage.

Competitive Landscape

The global compact inverter technology market remains moderately concentrated, shaped by global leaders and fast-growing regional specialists. Established multinational players hold strong competitive positions through recognized brands, broad product portfolios, and extensive distribution networks serving residential, commercial, and utility segments.

Their sustained R&D investments in advanced semiconductors, grid-interactive capabilities, and integrated energy-management features allow them to maintain premium pricing and long-term customer loyalty despite rising competition.

New Entrant manufacturers are expanding their presence by targeting niche applications, offering cost-competitive solutions, and rapidly innovating in compact, high-efficiency architectures. Companies from China, in particular, dominate price-sensitive segments due to manufacturing scale and streamlined supply chains.

Premium market participants continue to differentiate through high reliability, digital monitoring platforms, and hybrid solar-storage system compatibility. Strategic focus across the industry increasingly centers on wide-bandgap semiconductor adoption, software-defined energy optimization, and application-specific designs suitable for harsh industrial, off-grid, and maritime environments, although large-scale consolidation remains limited.

Key Market Developments

- January 2025: Schneider Electric expanded its home energy ecosystem in January 2025 with the launch of Schneider Charge Pro, a connected Level-2 EV charger offering real-time monitoring and remote diagnostics. While not tied to a new compact inverter release, the update strengthens integration across residential electrification and energy management systems.

- September 2024: Growatt presented its latest residential solar and storage products-including hybrid inverters and microinverters-at RE+ 2024 in September. The company highlighted cloud-based energy management features and wider U.S. availability but made no formal announcements on new partnerships or market-share gains.Key Market Highlights

Companies Covered in Compact Inverter Technology Market

- Eaton Corporation PLC

- Toshiba Schneider Inverter Corporation

- Ring Automotive Limited

- Mitsubishi Electric Corporation

- Hitachi Global

- Zucchetti Centro Sistemi S.p.a.

- YASKAWA Europe GmbH

- Fuji Electric Corp. of America

- MoTek S.r.l.

- TDK Electronics

- Growatt New Energy

- CE+T Power

- Xantrex LLC

- Samlex America Inc.

- Wagan Tech

- SMA Solar Technology AG

- Fronius International GmbH

- Enphase Energy Inc.

- ABB Ltd

- Schneider Electric SE

Frequently Asked Questions

The global compact inverter technology market is valued at US$ 1.5 billion in 2025 and is projected to reach US$ 2.9 billion by 2032 at a 9.8% CAGR, supported by accelerating renewable energy and storage adoption.

Demand is driven by rapid renewable energy expansion, rising BESS integration, growing EV-charging infrastructure, increasing consumer energy independence, and strong policy support such as tax credits and renewable mandates.

The 1-5 kW segment leads with 40% market share, driven by its suitability for residential solar systems, small commercial uses, and widespread adoption of string and emerging microinverter technologies.

North America leads with 34% market share in 2025 fueled by major renewable additions in U.S. and Canada.

Battery energy storage integration offers the largest opportunity creating demand for bidirectional inverters and advanced energy-management software.

Major players include Eaton, Schneider Electric, Mitsubishi Electric, Hitachi, Growatt, SMA, Fronius, Enphase, and ABB, supported by strong portfolios, R&D capabilities, and expanding Chinese competitors.