- Electrical Equipment & Services

- Composite Line Post Insulators Market

Composite Line Post Insulators Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Composite Line Post Insulators Market by Voltage (Low, Medium, High), Application (Substations, Transmission & Distribution Lines, Railways, Others), End-User (Utilities, Industrial, Commercial), and Regional Analysis for 2026-2033

Composite Line Post Insulators Market Share and Trends Analysis

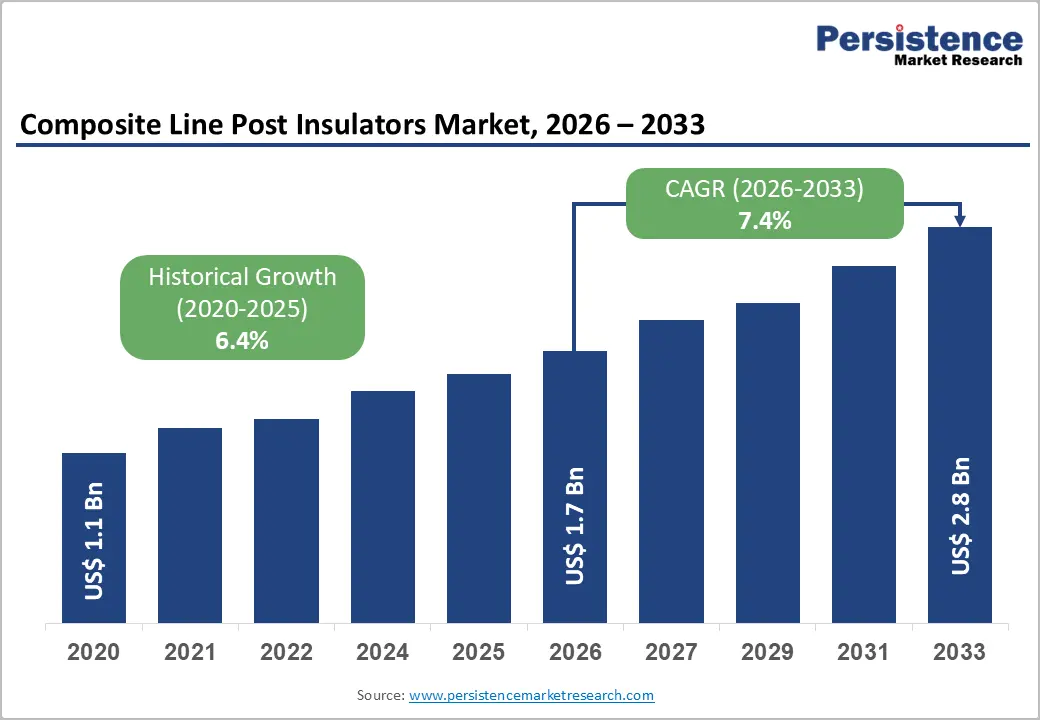

The global composite line post insulators market size is likely to be valued at US$ 1.7 billion in 2026, and is projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 7.4% during the forecast period 2026−2033. This sustained expansion is underpinned by accelerating investment in electricity transmission and distribution (T&D) infrastructure worldwide, driven by grid modernization mandates, renewable energy integration requirements, and a structural shift away from conventional ceramic and glass insulators. Utilities and grid operators across North America, Europe, and the Asia Pacific are actively upgrading aging transmission corridors, deploying high-voltage direct current (HVDC) and ultra-high-voltage (UHV) lines that necessitate advanced composite insulation solutions. Composite line post insulators, with their superior mechanical strength, lower weight, and resistance to vandalism and pollution flashover, have emerged as the preferred solution for both retrofit projects and new transmission line deployments.

Key Industry Highlights

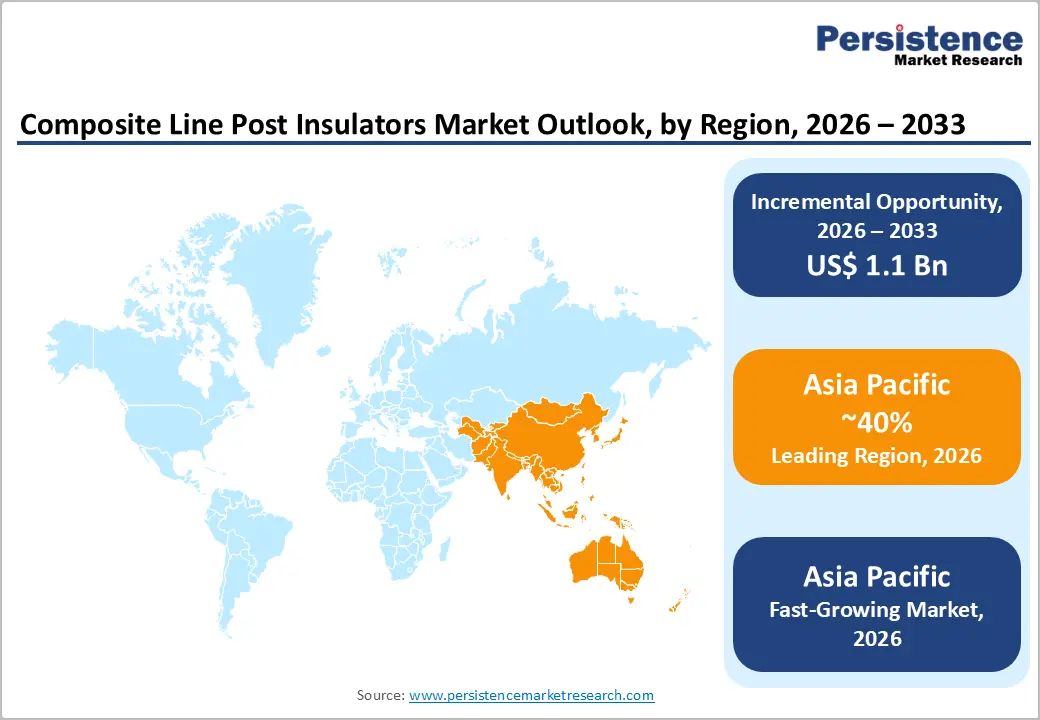

- Regional Leadership: Asia Pacific is likely to be both the leading and fastest-growing market from 2026 to 2033, accounting for approximately 40% of the market share in 2026.

- Leading & Fastest-growing Voltage: High-voltage is slated to command approximately 45% of total market revenue in 2026, with medium voltage growing the fastest segment during the 2026-2033 forecast period.

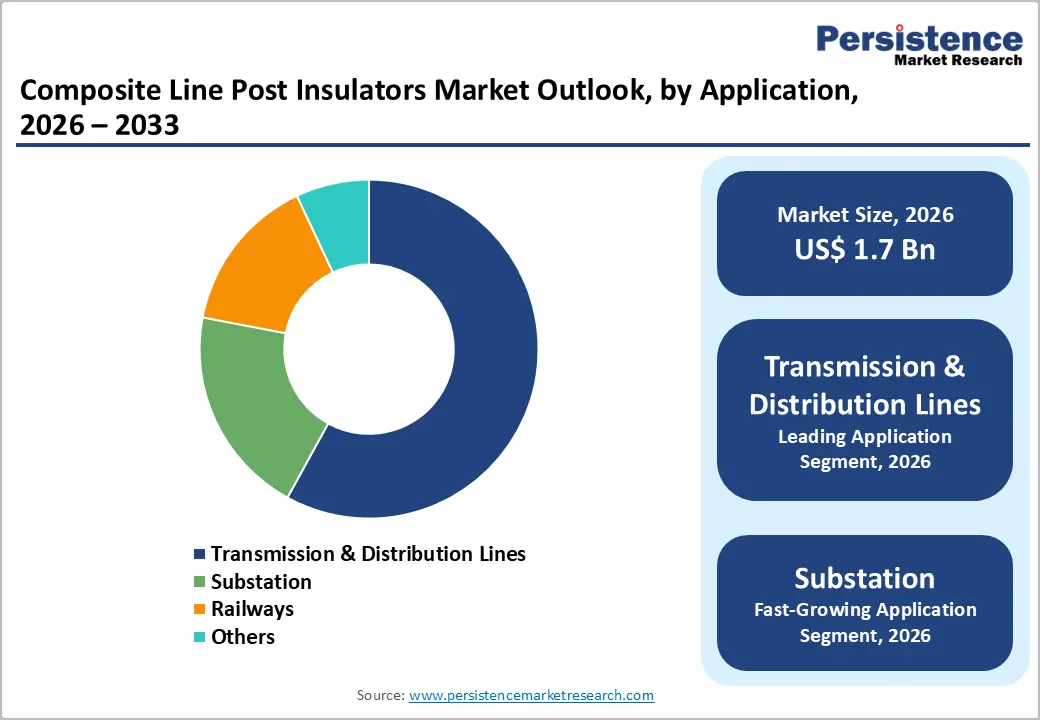

- Leading & Fastest-growing Application: Transmission and distribution lines are poised to secure roughly 58% of market revenue share in 2026, while sub-station is expected to be the fastest-growing segment over the 2026-2033 forecast period.

- Prominent Trend: Integrating IoT sensors for real-time monitoring, utilizing advanced silicone rubber for superior hydrophobicity and self-cleaning, and adopting hybrid models for enhanced mechanical strength in harsh environments.

| Key Insights | Details |

|---|---|

| Composite Line Post Insulators Market Size (2026E) | US$ 1.7 Bn |

| Market Value Forecast (2033F) | US$ 2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

DRO Analysis

Grid Modernization and T&D Infrastructure Investment

Government-led grid modernization programs are emerging as a primary force shaping demand for composite line post insulators. Policymakers are prioritizing the reinforcement of transmission and distribution networks to support growing electricity consumption and the integration of renewable energy sources. Agencies such as the United States Department of Energy (DOE) are directing structured efforts toward upgrading aging infrastructure, while regulatory frameworks such as the Trans-European Networks for Energy (TEN-E) are enabling cross-border grid expansion. National utilities are also accelerating investments to strengthen grid reliability and resilience. These initiatives are requiring advanced components that can perform consistently under higher voltage levels and challenging environmental conditions.

Utilities are increasingly replacing traditional porcelain and glass insulators with composite alternatives to achieve long-term operational efficiency. Composite materials are reducing weight, simplifying installation, and lowering the risk of mechanical failure in critical applications. Maintenance teams are benefiting from reduced inspection frequency and lower lifecycle costs, which are improving overall asset management strategies. Grid operators are also focusing on minimizing outages and enhancing system stability, which is reinforcing the shift toward high-performance insulation solutions. Continuous investments in smart grid technologies are further strengthening the need for durable and adaptable components.

Rapid Integration of Renewable Energy Sources

The global energy transition is transforming transmission grid design and redefining insulator performance requirements. Power systems are increasingly integrating renewable sources, which is shifting generation away from centralized plants toward dispersed locations. Organizations such as the International Energy Agency (IEA) and the International Renewable Energy Agency (IRENA) are highlighting how this shift is reshaping infrastructure priorities. Developers are installing wind and solar assets in environments that are exposing equipment to salt, moisture, and industrial pollution. These conditions are demanding insulation solutions that can maintain reliability under continuous electrical and environmental stress. Composite line post insulators are addressing these challenges by using silicone rubber housings that are preserving hydrophobic properties and limiting leakage currents.

Grid operators are simultaneously expanding high-voltage transmission corridors to connect renewable generation sites with urban demand centers. HVDC systems are playing a central role in this expansion due to their efficiency over long distances. These systems are requiring insulators that can handle elevated voltage ratings while maintaining mechanical stability. Composite designs with fiberglass reinforced polymer (FRP) cores are delivering the required strength and flexibility for such applications. Engineers are prioritizing solutions that reduce failure risks and improve long-term durability. This evolving landscape is strengthening the role of advanced composite insulators in modern transmission networks.

Limited Standardization and Long-Term Performance Data

Standardization gaps are creating a critical barrier to the wider adoption of composite line post insulators. Ceramic insulators are benefiting from long-established testing frameworks defined under the International Electrotechnical Commission (IEC) standard for artificial pollution tests on high-voltage insulators (IEC 60305) and the American National Standards Institute insulator standards (ANSI C29). Composite alternatives are following multiple guidelines, including the IEC standard for line post composite insulators (IEC 61952) and the Institute of Electrical and Electronics Engineers (IEEE) guide for polymer insulators (IEEE 1523). This fragmented structure is limiting consistency in performance validation. Utility engineers are facing difficulty in comparing products across suppliers because testing approaches are varying across regions.

Technical uncertainty is also shaping risk assessment practices within transmission projects. Engineers are evaluating long-term reliability concerns such as ultraviolet exposure, corona discharge effects, and material behavior under cyclic environmental stress. The absence of unified aging protocols is extending qualification timelines and increasing dependence on field performance data. Utilities are prioritizing proven solutions to avoid operational failures in critical grid infrastructure. Conservative procurement environments are continuing to favor established technologies due to these uncertainties. Manufacturers are responding by investing in advanced testing capabilities and material research to build confidence among stakeholders and accelerate acceptance.

Supply Chain Concentration and Raw Material Volatility

The production of composite line post insulators is relying on specialized raw materials that are facing supply constraints and pricing pressure. Manufacturers are sourcing high-grade silicone rubber and E-glass fiber, which are essential for ensuring electrical insulation and mechanical strength. Silicone materials are also serving industries such as semiconductors, automotive systems, and healthcare equipment, which is intensifying competition for limited supply. This cross-industry demand is pushing procurement teams to secure long-term contracts and diversify sourcing strategies. At the same time, E-glass fiber, which forms the core reinforcement structure, is experiencing fluctuations in availability due to energy costs and production bottlenecks. These factors are increasing input costs and creating challenges in maintaining stable pricing for finished insulators.

Supply chain concentration is further complicating procurement and manufacturing decisions. A significant share of raw material production is based in China, which is shaping global supply dynamics. Non-domestic manufacturers are depending on imports for critical inputs, which is exposing them to trade restrictions, logistics delays, and policy changes. Companies are responding by exploring regional supply partnerships and investing in localized production capabilities. Strategic sourcing is becoming a key priority as firms are aiming to reduce dependency risks and improve supply resilience. This evolving landscape is encouraging manufacturers to strengthen supplier networks while maintaining product quality and cost efficiency.

HVDC and Ultra-High-Voltage Transmission Expansion

The expansion of HVDC transmission networks is creating a distinct growth avenue for advanced composite insulator manufacturers. Energy systems are increasingly adopting HVDC technology to transfer electricity across long distances with minimal losses and improved grid stability. Major infrastructure programs in regions such as China, Europe, and the United States are accelerating the deployment of ultra-high voltage corridors and offshore interconnections. These projects are requiring insulation systems that can operate reliably under continuous direct current stress, which differs from conventional alternating current conditions. Composite line post insulators are meeting these requirements by offering superior resistance to electrical tracking, enhanced hydrophobic performance, and stable behavior under high electric field intensity.

Engineering requirements for HVDC applications are becoming more complex, which is elevating the role of specialized material science and product design. Manufacturers are developing insulators with optimized profiles to control electric field distribution and reduce surface degradation. Silicone rubber formulations are improving resistance to contamination and moisture, while reinforced cores are ensuring mechanical integrity under heavy loads. Utilities and project developers are prioritizing solutions that deliver long service life and consistent performance in demanding environments. This shift is positioning premium composite insulator suppliers to capture higher-value opportunities within transmission infrastructure, supported by increasing investment in next-generation power networks.

Replacement and Retrofit Programs for Aging Porcelain Infrastructure

A large installed base of aging porcelain and glass insulators is creating a long-term replacement cycle across mature transmission networks. Utilities in North America and Western Europe are operating infrastructure that is approaching the end of its designed service life. Organizations such as the North American Electric Reliability Corporation (NERC) are identifying insulator degradation as a growing reliability concern. Maintenance teams are observing increased failure rates due to contamination, mechanical wear, and environmental exposure. These conditions are prompting utilities to initiate structured replacement programs to maintain grid stability and reduce outage risks. Composite line post insulators are emerging as a preferred option because they are offering improved durability, lower weight, and better resistance to environmental stress.

Manufacturers are designing composite insulators that can integrate seamlessly with existing transmission hardware. Direct-fit solutions are allowing utilities to replace legacy units without extensive modifications to towers or cross-arm assemblies. This compatibility is reducing installation time and minimizing operational disruptions during upgrades. Procurement teams are also evaluating lifecycle benefits, as composite materials are requiring less frequent maintenance and inspections. Utilities are prioritizing cost-effective retrofit strategies that enhance performance while controlling capital expenditure. Market participants are positioning themselves to capture this demand by expanding product portfolios tailored for replacement applications.

Category-wise Analysis

Voltage Insights

High-voltage is set to capture approximately 45% of the composite line post insulators market revenue share in 2026, due to utilities are expanding long-distance transmission infrastructure and upgrading grid capacity. Transmission operators are prioritizing high voltage networks to support bulk power transfer across regions and integrate renewable energy sources into centralized grids. Composite line post insulators are gaining strong preference in this segment because they are delivering superior electrical strength, reduced weight, and improved resistance to pollution. Utilities are also focusing on minimizing transmission losses and enhancing system reliability, which is reinforcing demand for advanced insulation solutions.

Medium voltage is likely to be the fastest-growing segment during the 2026-2033 forecast period. Urbanization and industrial development are increasing electricity demand at the distribution level, which is driving investments in medium voltage infrastructure. Utilities are deploying composite insulators to improve operational efficiency and reduce maintenance requirements in densely populated and high-load areas. Renewable energy integration at the distribution level is further accelerating this growth, particularly through decentralized generation systems. Grid operators are strengthening distribution resilience, which is pushing demand for reliable and cost-effective insulation solutions in this segment.

Application Insights

Transmission and distribution lines represent the dominant application, capturing an estimated 58% of market revenue share in 2026. Power operators are strengthening interregional connectivity and integrating renewable energy sources, which is increasing reliance on long-distance transmission infrastructure. Composite line post insulators are playing a critical role in this segment by providing high mechanical strength, better contamination resistance, and improved performance under varying environmental conditions. Utilities are also focusing on reducing outages and maintenance costs, which is reinforcing the adoption of advanced insulation solutions across overhead line applications.

Sub-station is expected to be the fastest-growing segment over the 2026-2033 forecast period, driven by grid modernization efforts are accelerating across both developed and emerging economies. Utilities are investing in digital substations and compact designs to improve operational efficiency and space utilization. Composite insulators are gaining traction in this segment because they are offering lightweight construction, enhanced safety, and reliable performance in high-stress electrical environments. Increasing renewable energy integration is also driving the need for new substations and upgrades to existing facilities. This trend is supporting rapid demand growth for composite line post insulators in substation applications.

Regional Insights

Asia Pacific Composite Line Post Insulators Market Trends

Asia Pacific is likely to be both the leading and fastest-growing regional market for composite line post insulators in 2026, accounting for approximately 40% of the market share. China is driving regional demand through extensive transmission and distribution expansion led by the State Grid Corporation of China and China Southern Power Grid. National planning frameworks such as the Fourteenth Five Year Plan are prioritizing ultra-high voltage networks, which are requiring advanced insulation systems for reliable performance. Domestic manufacturers are strengthening production capabilities and are supplying both local and international markets.

India is emerging as a key growth engine as power sector reforms and renewable energy targets are accelerating grid expansion. Government initiatives such as the Revamped Distribution Sector Scheme (RDSS) and Green Energy Corridors are driving demand for modern transmission components. Utilities are deploying composite insulators to support new lines and improve system efficiency. Countries such as Japan and South Korea are focusing on upgrading aging infrastructure with solutions that enhance seismic resilience and operational safety. Southeast Asian nations including Vietnam, Indonesia, and the Philippines are expanding grid networks with support from multilateral institutions such as the Asian Development Bank (ADB) and the World Bank. This regional momentum is strengthening Asia Pacific’s position as a central hub for production and demand.

Europe Composite Line Post Insulators Market Trends

Europe is maintaining a strong position in the composite line post insulator market as countries are accelerating energy transition and grid modernization efforts. Key economies such as Germany, the United Kingdom, France, Spain, and Italy are investing in transmission upgrades to support renewable integration. Policy frameworks such as the European Green Deal and REPowerEU are driving expansion of clean energy capacity, which is increasing the need for reliable grid infrastructure. Organizations such as the European Network of Transmission System Operators for Electricity (ENTSO-E) are coordinating cross-border planning to strengthen interconnections across member states. These initiatives are requiring advanced insulation solutions that can ensure performance under higher electrical loads and variable environmental conditions.

Germany is leading regional demand through its energy transition strategy, which is focusing on offshore wind integration and reinforcement of high voltage networks. The United Kingdom is advancing large-scale transmission projects under the Accelerated Strategic Transmission Investment (ASTI) framework to connect offshore generation assets. Regulatory alignment under the European Union Electricity Market Regulation and standardized grid codes is simplifying procurement processes across countries. Utilities are also prioritizing sustainability by selecting materials that reduce environmental impact and support long-term operational efficiency. Composite insulators are gaining preference due to their lightweight design and improved lifecycle performance, which is aligning with Europe’s focus on resilient and sustainable energy systems.

North America Composite Line Post Insulators Market Trends

North America is holding a significant position in the global composite line post insulator market, with the United States driving most of the regional demand. The market is benefiting from a large base of aging transmission infrastructure that is requiring systematic upgrades and replacement. Federal initiatives such as the Bipartisan Infrastructure Law and regulatory reforms introduced by the Federal Energy Regulatory Commission (FERC) are accelerating investment in grid expansion and modernization. Utilities are planning new transmission corridors to support renewable integration and improve network reliability. These developments are increasing the need for advanced insulation systems that can operate efficiently under higher voltage conditions and diverse environmental stresses.

Replacement of legacy porcelain insulators is becoming a central driver of demand across utility networks. Grid operators are addressing reliability risks by upgrading components installed several decades ago, while also preparing for future capacity requirements. Project pipelines are expanding as new generation sources are connecting to the grid, which is creating additional demand for transmission infrastructure. Canada is contributing through investments in hydroelectric export systems and wind energy transmission corridors. Regulatory frameworks established by the North American Electric Reliability Corporation (NERC) and environmental approval processes are guiding equipment selection. Utilities are increasingly adopting composite insulators due to their durability, lower maintenance needs, and strong performance in critical applications.

Competitive Landscape

The global composite line post insulators market structure is consolidated, dominated by leading players such as TE Connectivity, Hubbell Power Systems, ABB Ltd., Jingyuan Group and Dalian Insulator Group. These players collectively capture 35-40% of the market share. The competitive landscape is being shaped by large-scale power system manufacturers that are actively strengthening their presence through long-term agreements with federal and state authorities. These companies are participating in grid modernization programs and are securing preferred supplier status for transmission and distribution projects. Strategic partnerships are enabling manufacturers to align product development with evolving regulatory and technical requirements. Firms are also expanding integrated capabilities across design, manufacturing, and installation to offer end-to-end solutions. This approach is improving customer retention and project visibility, while reinforcing competitive positioning in large infrastructure upgrade cycles.

Key Industry Developments

- In January 2026, Ensto launched a new generation of pin insulators designed to meet modern?network requirements and the updated IEC 60383?1:2023 standard, with increased creepage distance, thicker insulation, and semiconductive coatings that reduce electric?field stress and partial?discharge risk.

- In June 2025, Power Grid Components (PGC) announced an exclusive partnership between its subsidiary Newell and GAMMA Insulators for composite distribution insulators in the North American market. Under this agreement, Newell will add GAMMA’s high?quality composite distribution insulators to its product line, leveraging GAMMA’s manufacturing in Colombia to strengthen nearshoring.

- In June 2025, Ensto’s new composite line post insulators marked a shift toward more modern, resilient overhead distribution networks, offering higher durability and easier installation than traditional porcelain insulators. Designed mainly for 24 kV overhead lines, these insulators use a silicone?coated fiberglass core that provides excellent resistance to UV, electrical stress, and harsh weather.

Companies Covered in Composite Line Post Insulators Market

- TE Connectivity

- Hubbell Power Systems

- ABB Ltd.

- NGPC

- Jingyuan Group

- Dalian Insulator Group

- Seves Group

- K Line Insulators Ltd.

- MacLean Power Systems

- Tyco Electronics

- Lapp Insulators

- Arteche Group

- PPC Insulators

- Orient Group

- Jiangsu Shemar Electric

Frequently Asked Questions

The global composite line post insulators market is projected to reach US$ 1.7 billion in 2026.

The market is driven by grid‑modernization, aging‑infrastructure replacement, and the expansion of renewable‑energy‑linked transmission and distribution networks.

The market is poised to witness a CAGR of 7.4% from 2026 to 2033.

Major opportunities lie in emerging‑market grids, supplying high‑voltage and UHV corridors, and introducing smart / sensor‑enabled composite line post insulators.

TE Connectivity, Hubbell Power Systems, ABB Ltd., Jingyuan Group and Dalian Insulator Group are some of the key players in the market.