- Medical Devices

- Disposable Plastic Blood Bags Market

Disposable Plastic Blood Bags Market Size, Share, and Growth Forecast 2026 - 2033

Disposable Plastic Blood Bags Market by Product (Collection Bags, Transfer Bags), by Channel (Tender Sales, Private Sales), by End User (Blood Banks, Hospitals, NGOs), by Regional Analysis, 2026–2033

Disposable Plastic Blood Bags Market Size and Trend Analysis

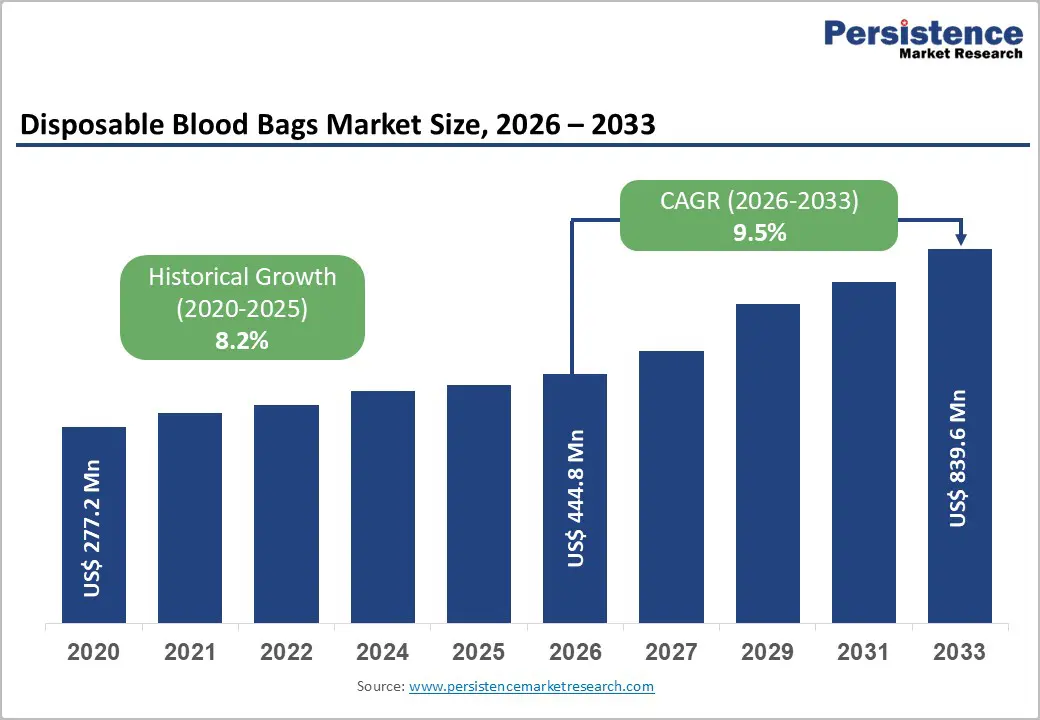

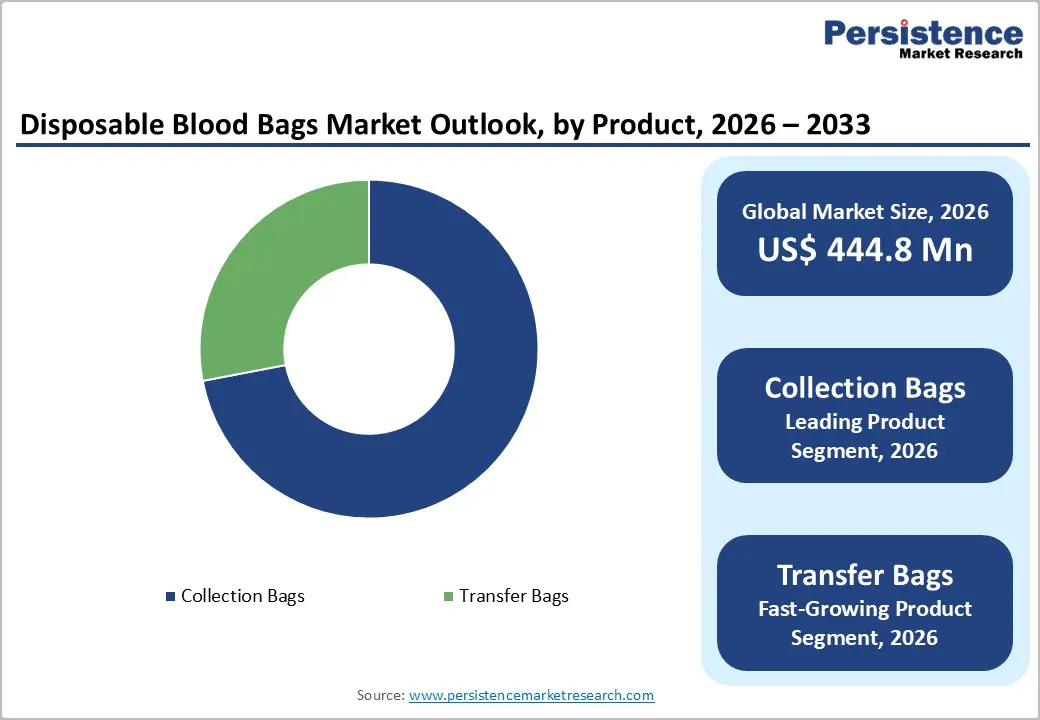

The global disposable plastic blood bags market size is expected to be valued at US$ 444.8 million in 2026 and projected to reach US$ 839.6 million by 2033, growing at a CAGR of 9.5% between 2026 and 2033. The market is expanding at an accelerating pace, driven by rising global blood collection volumes, expanding blood bank infrastructure across emerging economies, and increasing surgical and trauma care demand for safe blood transfusion products.

The World Health Organization (WHO) reports that ~118.5 million blood donations are collected globally each year, each requiring sterile, validated disposable plastic bags for collection, separation, and storage. Government initiatives to achieve voluntary blood donation targets, combined with growing NGO-led blood collection programs in underserved regions and rising surgical procedure volumes, are collectively reinforcing sustained double-digit demand growth for disposable blood bag solutions.

Key Industry Highlights

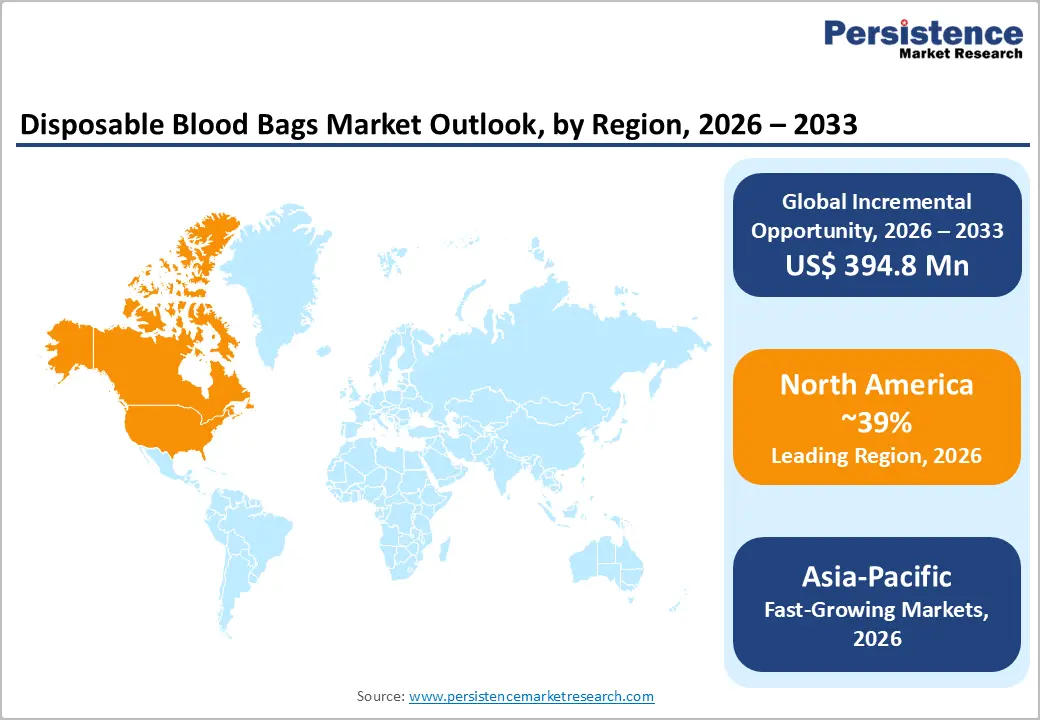

- Leading Region – North America leads the global disposable plastic blood bags market with ~36% revenue share, supported by high blood collection volumes, strict FDA compliance standards, advanced blood banking infrastructure, and widespread adoption of leukoreduction and multi-bag collection systems.

- Fastest Growing Region – Asia Pacific is the fastest-growing region due to rising blood donation awareness, expansion of licensed blood banks, government-led voluntary donation programs, and increasing healthcare investments across China, India, and Southeast Asia.

- Dominant Segment – Blood banks dominate the end-user segment due to high-volume institutional procurement, mandatory use of single-use blood bags, strong transfusion demand, and established collection systems managed by public and private healthcare organizations.

- Fastest Growing Segment – NGOs represent the fastest-growing end-user segment driven by expanding humanitarian healthcare programs, emergency transfusion support, rising blood shortage management initiatives, and increasing healthcare outreach in underserved regions.

- Key Market Opportunity – Major opportunities exist in pathogen reduction technology (PRT)-integrated multi-bag systems, improving blood safety, reducing contamination risks, supporting premium pricing, and strengthening advanced transfusion management solutions.

Market Dynamics

Drivers - Rising Global Blood Donation Volumes and Blood Bank Expansion Programs

The global increase in voluntary blood donations is the primary structural demand driver for disposable plastic blood bags. The WHO and International Federation of Red Cross and Red Crescent Societies (IFRC) report that ~118.5 million blood donations are collected annually worldwide, with low- and middle-income countries progressively expanding their national blood transfusion infrastructure. India's National Blood Transfusion Council (NBTC) targets 100% voluntary blood donation under the National Blood Policy, while the American Red Cross manages over 6.8 million units of red blood cells annually. Each blood collection unit requires a sterile, multi-compartment disposable plastic bag, creating direct, non-substitutable volume demand that scales proportionally with donation rates.

Increasing Surgical Procedures and Trauma Care Demand for Blood Components

The growing global volume of surgical procedures including cardiac, orthopedic, and oncological surgeries combined with rising road traffic accidents and trauma cases, is sustaining high demand for blood component transfusions that depend directly on disposable plastic blood bag availability. The WHO estimates over 313 million surgical procedures are performed globally each year, with transfusion requirements across intraoperative and post-operative care creating consistent institutional demand for packed red blood cell bags, platelet bags, and fresh frozen plasma bags. The Global Status Report on Road Safety by WHO documents ~1.35 million annual road traffic fatalities requiring emergency blood transfusion, further reinforcing consistent blood bag procurement demand across hospital and blood bank settings globally.

Restraints - Lack of Infrastructure to Collect and Store and Storing Blood

In terms of infrastructure for processing blood, blood collection centers in African countries, including Nigeria, Egypt, and Ethiopia, are falling behind. With this, single blood bags are far more in demand than other types in these countries.

The use of double, triple, and quadruple blood collection bags, which are frequently employed during the collection and storage of blood component, is further hampered in these areas by a lack of infrastructural facilities. Such a lack of facilities for blood collection and storage results in the loss of collected blood and widens the supply-demand gap in the market for blood bags globally.

One significant issue impeding the growth of the blood collection market in these regions is the lack of awareness regarding voluntary blood donation efforts. One of the main barriers to voluntary blood donation across the globe is false beliefs about the donation of blood. Reduced demand for blood collection bags because of the low level of awareness about blood donation activities is impeding market expansion.

Opportunities - Adoption of Sustainable and Eco-Friendly Blood Bags

One of the most transformative opportunities lies in developing and adopting biodegradable and eco-friendly disposable blood bags. With increasing global awareness about environmental concerns, manufacturers are innovating to produce phthalate-free and biocompatible blood bags. Such products align with the push for sustainable healthcare practices and are expected to witness growing demand from hospitals, blood banks, and governments aiming to reduce their environmental footprint.

Early adoption in developed markets could create a ripple effect, driving adoption in emerging regions. The said shift presents a significant opportunity for companies to differentiate themselves through sustainable solutions while addressing regulatory pressures to reduce plastic waste.

Category-wise Insights

Product Analysis

Collection bags represent the leading product segment in the disposable plastic blood bags market, accounting for ~62% of total product-based market share in 2025. Collection bags are the mandatory primary interface for every blood donation event, creating non-substitutable per-donation demand that scales directly with global blood collection volumes. Standard blood collection bag assemblies typically incorporating a primary collection bag, satellite transfer bags, and inline filters represent a complete multi-unit disposable system required for each donation. The WHO requirement for single-use, sterile collection systems under its Blood Safety and Availability guidelines mandates collection bag use at every accredited blood collection facility. Leading manufacturers including Poly Medicure Limited, TERUMO PENPOL Pvt. Limited, and Fresenius Kabi India Pvt. Ltd. hold strong collection bag portfolio positions.

End User Analysis

Blood banks constitute the dominant end-user segment in the disposable plastic blood bags market, accounting for ~65% of total end-user share in 2025. Blood banks encompassing both standalone regional blood centers and hospital-based transfusion services represent the core institutional buyer of collection and transfer blood bag products, requiring ongoing large-volume replenishment aligned with donor activity and component production needs. In the United States, the American Red Cross and America's Blood Centers collectively manage blood supply for ~40% and 60% of the national blood supply respectively, representing substantial institutional blood bag procurement volumes. Nationally certified blood banks in India, China, and across the EU operate under regulatory standards mandating WHO-compliant single-use blood bag procurement.

Regional Insights

North America Disposable Plastic Blood Bags Market Trends and Insights

North America led the global disposable plastic blood bags market with ~36% share in 2025, supported by advanced transfusion infrastructure, high blood collection volumes, strong regulatory compliance, and widespread adoption of premium blood storage and collection technologies. The region also benefits from strong healthcare spending, increasing trauma and surgical cases, and rising demand for leukoreduced and pathogen-safe blood products across hospitals and blood centers.

U.S. Disposable Plastic Blood Bags Market Size

The U.S. accounts for nearly 87% of the North American disposable plastic blood bags market in 2025, supported by one of the world’s most advanced blood transfusion infrastructures. Organizations such as the American Red Cross and independent blood centers collectively collect more than 13 million blood units annually, creating substantial demand for sterile disposable blood bag systems. Strict FDA regulations under 21 CFR Part 864 ensure high-quality safety standards for blood collection and storage products. Rising surgical procedures, trauma cases, and chronic disease prevalence continue supporting strong demand for premium multi-bag and leukoreduction-compatible blood collection systems nationwide.

Europe Disposable Plastic Blood Bags Market Trends and Insights

Europe is the second-largest market for disposable plastic blood bags, governed by the EU MDR 2017/745 and EU Blood Directive 2002/98/EC frameworks that mandate rigorous blood bag quality standards. The region demonstrates strong adoption of DEHP-free, pathogen-reduction-compatible multi-bag systems, reflecting European blood services' advanced transfusion safety priorities and sustainability-oriented procurement policies.

Germany Disposable Plastic Blood Bags Market Size

Germany holds ~21% of the European disposable plastic blood bags market in 2025, supported by its highly developed healthcare infrastructure and strong blood donation network. The German Red Cross and hospital-based transfusion centers manage one of Europe’s largest blood supply systems. Germany’s strict Transfusion Act (TFG) mandates the use of validated and high-quality single-use blood collection systems, driving consistent procurement demand. Increasing focus on infection prevention, blood safety, and advanced transfusion technologies continues supporting adoption of premium disposable blood bags from domestic and international suppliers across hospitals and blood banks.

UK Disposable Plastic Blood Bags Market Size

The UK represents nearly 16% of the European disposable plastic blood bags market in 2025, driven by centralized procurement systems and strong national blood collection programs. NHS Blood and Transplant manage nationwide blood collection and procures blood collection equipment through centralized tenders, creating stable large-volume demand for suppliers. The country collects around 1.6 million blood units annually to support transfusion requirements. Increasing demand for leukoreduced blood products, advanced blood safety systems, and efficient transfusion management technologies continue driving procurement of high-quality disposable blood bag systems across healthcare facilities.

France Disposable Plastic Blood Bags Market Size

France accounts for ~14% of the European disposable plastic blood bags market in 2025, supported by centralized blood collection and strong government-led transfusion safety programs. Établissement Français du Sang operates more than 140 blood collection sites nationwide and procures blood bag systems through public tenders. The country emphasizes leukoreduced and pathogen-reduced blood components, increasing demand for technologically advanced multi-bag collection systems. Growing adoption of automated blood processing technologies, strict healthcare quality standards, and rising surgical procedures continue supporting steady market growth across France’s transfusion and hospital infrastructure.

Asia Pacific Disposable Plastic Blood Bags Market Trends and Insights

Asia Pacific is the fastest-growing regional market for disposable plastic blood bags, driven by rapidly expanding national blood transfusion programs, rising surgical volumes, and government-mandated blood safety improvements. China's National Health Commission has significantly expanded blood collection center infrastructure, with China processing over 25 million units of blood annually the largest blood collection volume in Asia creating massive domestic blood bag demand.

China Disposable Plastic Blood Bags Market Size

China is one of the largest disposable plastic blood bags markets in Asia-Pacific, driven by rapidly expanding blood transfusion infrastructure and increasing healthcare investments. The National Health Commission of the People's Republic of China has significantly strengthened blood collection and safety programs nationwide, with China processing more than 25 million blood units annually. Rising surgical procedures, trauma cases, and chronic disease prevalence are further increasing demand for sterile blood collection systems. In addition, domestic manufacturing capabilities, government-led healthcare modernization initiatives, and growing adoption of advanced blood safety technologies continue supporting strong market growth across China.

India Disposable Plastic Blood Bags Market Size

India accounts for nearly 20% of the Asia-Pacific disposable plastic blood bags market in 2025, driven by expanding healthcare access, increasing blood donation programs, and rising surgical volumes. According to the National Blood Transfusion Council, the country has more than 3,200 licensed blood banks supporting national blood collection activities. Government initiatives promoting voluntary blood donation and safe transfusion practices are further strengthening demand for disposable blood bag systems. Domestic manufacturers such as Poly Medicure, TERUMO PENPOL, and HLL Lifecare play a significant role in supplying affordable blood collection products nationwide.

Japan Disposable Plastic Blood Bags Market Size

Japan holds ~18% of the Asia-Pacific disposable plastic blood bags market in 2025 due to its advanced healthcare infrastructure and stringent blood safety standards. The Japanese Red Cross Society centrally manages blood collection and transfusion services, collecting nearly 5 million blood units annually. Regulatory oversight under the Pharmaceutical and Medical Device Act (PMDA) supports adoption of premium DEHP-free and leukoreduced blood bag systems. Rising aging population, increasing chronic disease burden, and growing transfusion requirements continue driving demand for technologically advanced disposable blood collection and storage products across hospitals and blood centers nationwide.

Competitive Landscape

The disposable plastic blood bags market is competitive, with several global and regional players striving for market share. Terumo Corporation, Fresenius Kabi, and Macopharma lead the market, leveraging strong research and development capabilities and global distribution networks. Leading companies focus on innovating biocompatible, phthalate-free, and eco-friendly solutions to address sustainability concerns. Haemonetics Corporation and B. Braun Melsungen are notable players driving advancements in multi-bag systems for efficient blood component separation.

Regional manufacturers, particularly in Asia Pacific, are intensifying competition by offering cost-effective products tailored for emerging markets. Strategic collaborations with NGOs and government bodies for blood donation drives further enhance market reach. Technological advancements, sustainability initiatives, and increasing demand from underpenetrated markets shape the competitive landscape.

Key Developments

- In November 2024: Poly Medicure Limited received CE marking under EU MDR 2017/745 for its expanded blood collection bag portfolio, enabling direct entry into European blood service tender programs and strengthening its global export capabilities.

- In September 2023, Fresenius Kabi expanded its production facilities in Asia Pacific to meet the growing demand for disposable blood bags in emerging markets like India and China.

- In April 2023, Macopharma introduced a next-generation blood bag system with integrated sterile tubing and improved sterility indicators, enhancing ease of use and safety in transfusion practices.

Companies Covered in Disposable Plastic Blood Bags Market

- Poly Medicure Limited

- Grifols, S.A.

- Macopharma Bharat Transfusion Solution

- Fresenius Kabi India Pvt. Ltd.

- TERUMO PENPOL Pvt. Limited

- HLL Lifecare Limited

- Span Healthcare Private Limited

- Innvol

- Haemonetics Corporation

- Neomedic International

- Medsun Biomedical Technologies Pvt. Ltd.

- Hänsler Medical

- C.Y. Medical Co., Ltd.

- EasierWay Medical

- Others

Frequently Asked Questions

The global disposable plastic blood bags market is estimated to be valued at US$ 444.8 million in 2026.

Growing blood transfusion demand, rising healthcare awareness, and improved safety standards are driving the disposable blood bags industry's expansion.

North America leads the global disposable plastic blood bags market with ~36% of total market share in 2025.

Advancements in biodegradable materials, increasing healthcare investments, and expanding blood donation programs create significant growth opportunities in this market.

Poly Medicure Limited, Grifols, S.A., Macopharma Bharat Transfusion Solution, Fresenius Kabi India Pvt. Ltd., TERUMO PENPOL Pvt. Limited and Others.