- Advanced Materials

- Thermal Interface Materials Market

Thermal Interface Materials Market Size, Share, and Growth Forecast 2026 - 2033

Thermal Interface Materials Market by Product Type (Tapes and Films, Elastomeric Pads, Greases and Adhesives, Phase Change Materials, Metal, Others), Application (Telecom, Computer, Medical Devices, Industrial Machinery, Consumer Durables, Automotive Electronics, Others), and Regional Analysis for 2026 - 2033

Thermal Interface Materials Market Size and Trend Analysis

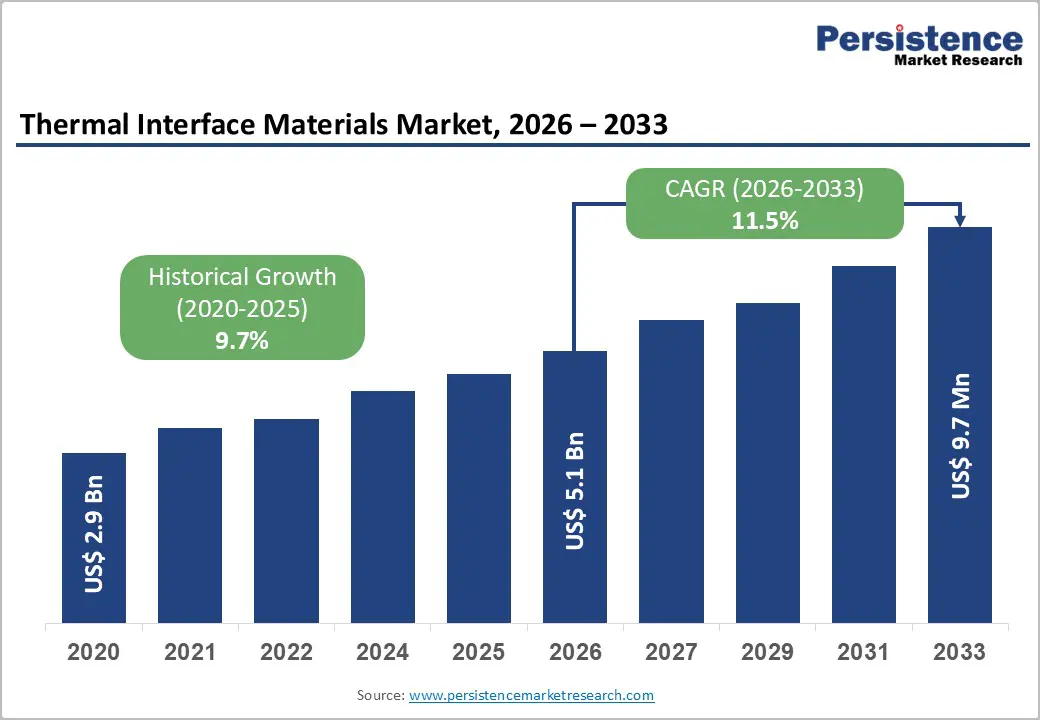

The global Thermal Interface Materials market size is valued at US$ 5.1 Bn in 2026 and is projected to reach US$ 11.0 Bn by 2033, growing at a CAGR of 11.5% between 2026 and 2033.

This exceptional growth is principally driven by surging demand for advanced thermal management solutions across AI-powered data centers, electric vehicle battery systems, and 5G telecommunications infrastructure. The proliferation of AI accelerators where processors such as the NVIDIA B200 GPU operate at a Thermal Design Power (TDP) of 1,200W has created unprecedented requirements for ultra-high-conductivity TIM formulations.

Key Industry Highlights:

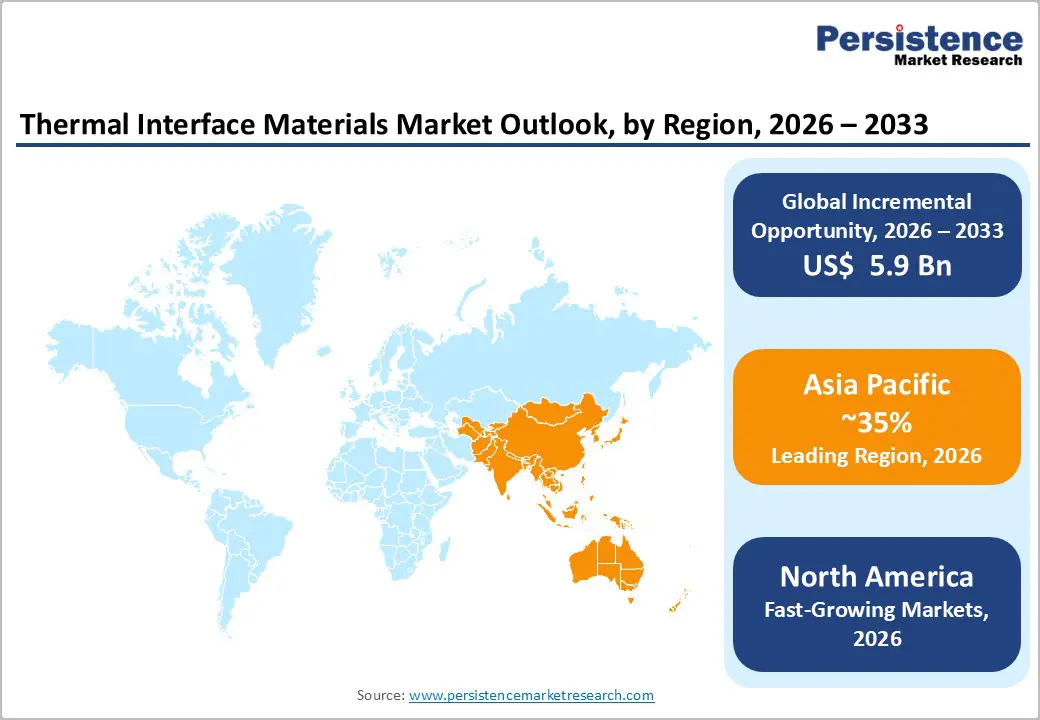

- Leading Region: Asia Pacific leads the global Thermal Interface Materials market, with China accounting for approximately 60% of EV battery demand and anchoring 5G equipment production globally. The region's electronics manufacturing base makes it the world's largest TIM consumption center through 2033.

- Fastest Growing Region: The United States leads North America's thermal interface materials market, propelled by a world-class semiconductor manufacturing ecosystem, the explosive expansion of hyperscale AI data centers, and accelerating domestic electric vehicle production.

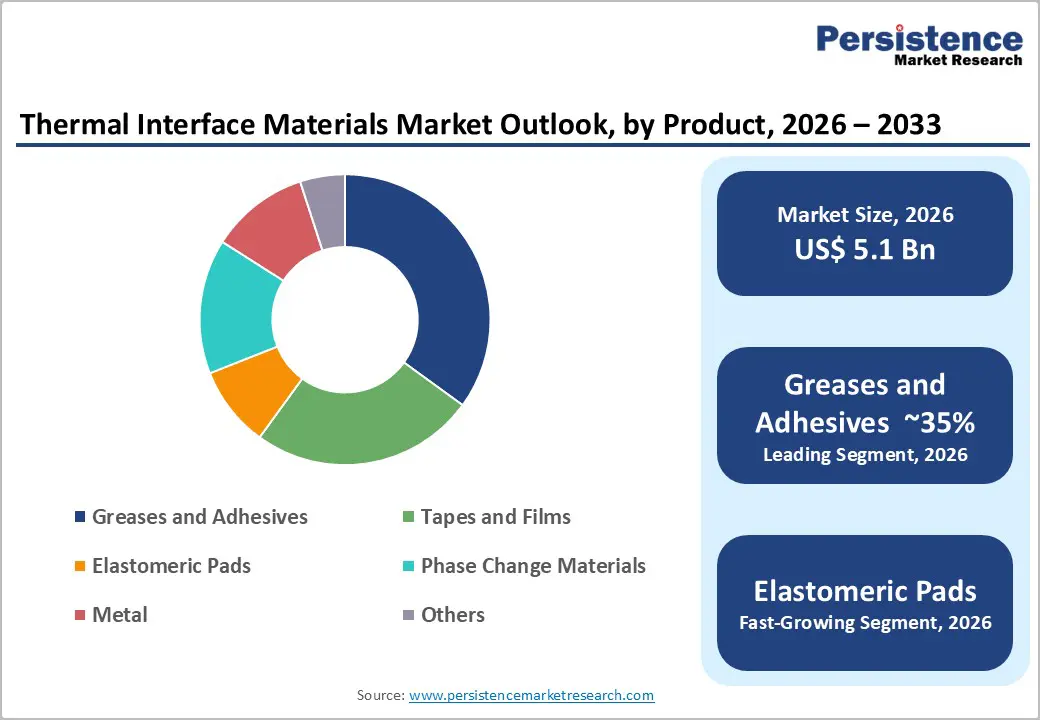

- Dominant Segment: Greases and Adhesives is the dominant Product Type segment, holding approximately 35% revenue share, driven by superior thermal conformability, reworkability in high-value electronics assembly, and broad adoption in AI chip packaging and EV battery thermal management applications across all regions.

- Fastest Growing Segment: Phase Change Materials (PCMs) represent the fastest-growing product segment, gaining rapid traction in AI data centers and EV battery assemblies due to superior conformability and adaptive thermal conductance, supported by institutional validation through TDK Ventures' ARPA-E COOLERCHIPS program investment in January 2025.

- Key Market Opportunity: The commercialization of ultra-high-conductivity liquid TIMs achieving 14.5 W/m·K led by Henkel's Loctite TCF 14001 for 800G AI data center optical transceivers define a transformational premium product tier opportunity for materials companies investing in AI infrastructure and next-generation GPU thermal management.

| Key Insights | Details |

|---|---|

|

Thermal Interface Materials Market Size (2026E) |

US$ 5.1 Bn |

|

Market Value Forecast (2033F) |

US$ 11.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

11.5% |

|

Historical Market Growth (CAGR 2020 to 2024) |

9.7% |

Market Dynamics

Drivers - AI Data Centers and High-Performance Computing Generating Unprecedented TIM Demand

The rapid global expansion of artificial intelligence infrastructure is the most transformative near-term growth catalyst for the Thermal Interface Materials market. Modern AI accelerators generate extreme heat densities that conventional cooling approaches cannot manage without premium TIM solutions positioned between chips, heat sinks, and cold plates. NVIDIA's B200 GPU carries a TDP of 1,200W, and upcoming chip architectures from Intel's Falcon Shores platform are projected to exceed 1,500W TDP, as documented by IDTechEx research published in 2024. In October 2025, Henkel AG & Co. KGaA responded by commercializing Loctite TCF 14001, a silicone liquid TIM achieving 14.5 W/m·K thermal conductivity, the highest among commercially available liquid TIM products, specifically engineered for 800G and 1.6T AI data center optical transceiver applications.

Electric Vehicle Adoption Scaling Battery and Powertrain Thermal Management Requirements

The accelerating global electrification of the automotive sector represents a foundational long-term growth drive for the thermal interface materials market. Global battery manufacturing capacity reached approximately 3.3 TWh in 2024 nearly 30% year-over-year growth and EV-specific battery demand surpassed 950 GWh in 2024, growing more than 25% year-over-year, according to industry data. TIMs are integral to EV battery modules, power inverters, onboard chargers, and ADAS control units, dissipating heat to prevent thermal runaway and ensuring operational safety. The emergence of 800-volt high-voltage EV platforms introduces elevated thermal loads requiring materials with exceptional conductivity, electrical insulation, and mechanical resilience under repetitive thermal cycling.

Restraints - Raw Material Cost Volatility and Specialty Filler Supply Concentration

The Thermal Interface Materials market faces significant cost pressure from its dependence on specialty thermally conductive fillers including aluminum nitride, hexagonal boron nitride, and silver flakes, alongside silicone polymer binders. Boron nitride production is heavily concentrated in China, Turkey, and the United States, making formulated TIM product costs highly sensitive to geopolitical developments and export policy shifts. Post-2020 supply chain disruptions across the specialty chemicals sector demonstrated the capacity for raw material shortages to delay product availability and inflate input costs, compressing margins for formulators. These dynamics disproportionately affect smaller TIM producers without vertically integrated raw material access, creating competitive disadvantages and limiting their ability to maintain consistent product supply to automotive and electronics OEM customers.

Technical Performance Ceilings in Ultra-High-Power Applications

Despite significant formulation advances, a performance gap persists between currently available commercial TIMs and the requirements of next-generation ultra-high-power applications. Conventional silicone greases and elastomeric pads typically deliver thermal conductivity values in the 1–8 W/m·K range, which are increasingly insufficient for AI chip packages and power electronics exceeding 1,000–1,500W TDP. Grease-based TIMs are prone to long-term degradation mechanisms including pump-out, dry-out, and phase separation under extended thermal cycling, progressively reducing interface conductance and device reliability. The trade-off between reworkability and adhesion strength in phase change and adhesive TIM formulations further complicates material qualification for safety-critical medical device and aerospace applications, limiting addressable market penetration in these high-value end-use segments.

Opportunities - Global 5G Infrastructure Expansion Creating High-Growth TIM Application Streams

The worldwide rollout of 5G telecommunications infrastructure represents a rapidly growing and structurally durable revenue opportunity for thermal interface materials market participants. Global 5G infrastructure investment reached USD 26.4 billion in 2023 and was forecast to grow 30% in 2024, creating a significant pull on TIM demand in base stations, massive MIMO antenna arrays, and mm Wave network equipment all operating at substantially higher power densities than legacy 4G infrastructure. Henkel AG & Co. KGaA specifically developed its Bergquist GAP PAD® TGP 10000ULM a formulation delivering 10.0 W/m·K thermal conductivity within an ultra-low-modulus design to address the high-power density challenges of new 5G telecom infrastructure. The Asia Pacific region, home to 5G equipment manufacturers across China, South Korea, Japan, and India, is the primary growth epicenter.

Phase Change Materials and Next-Generation Formulations Opening Premium Market Tiers

The growing commercialization of Phase Change Materials (PCMs) and nano-enhanced TIM formulations presents a compelling strategic opportunity for market participants seeking differentiation beyond commodity gap-fillers and greases. PCMs transition between solid and semi-liquid states at operating temperatures, delivering superior surface conformability, reduced interface thermal resistance, and simplified compatibility with automated dispensing processes in high-volume EV and electronics manufacturing. In January 2025, TDK Ventures announced an investment in NovoLINC, a startup developing next-generation thermal interface materials for AI computing applications, with technology incubated through the U.S. Department of Energy's ARPA-E COOLERCHIPS program and National Science Foundation (NSF) funding support. This institutional endorsement validates the commercial readiness of advanced TIM architectures for data center applications.

Category-wise Analysis

Product Type Insights

The Greases and Adhesives segment commands the leading position in the global Thermal Interface Materials market by product type, accounting for approximately 35% of total revenue share. This dominance is rooted in the segment's unmatched conformability across micro-scale surface irregularities between chip packages and heat sinks, delivering consistent low thermal resistance at the interface. Thermal greases and dispensable adhesives are particularly critical in high-power semiconductor packaging, AI server boards, EV battery modules, and power electronics, where reliable conformal coverage directly determines device longevity and performance stability. The reworkability of grease-based TIMs a key differentiator in premium electronics assembly where component repair or replacement is required further reinforces segment adoption.

Application Insights

The Automotive Electronics application segment holds a commanding and fast-growing position in the global Thermal Interface Materials market, reflecting the structural electrification of the global vehicle fleet. TIMs are integral to EV battery packs, power inverters, onboard chargers, SiC-based power modules, and ADAS control units, where reliable heat dissipation is critical for both safety and performance. The automotive electronics segment is estimated to represent approximately 28% of total application-based market revenue globally as of 2026, underpinned by EV adoption scaling and the increasing thermal complexity of electrified drivetrain systems. Global battery demand from EVs surpassing 950 GWh in 2024 with over 25% year-over-year growth directly amplifies TIM consumption along automotive assembly lines. The computer application segment, driven by AI data center GPU deployments and personal computing demand, holds significant market share alongside automotive electronics.

Regional Insights

North America Thermal Interface Materials Market Trends

The United States leads North America's thermal interface materials market, propelled by a world-class semiconductor manufacturing ecosystem, the explosive expansion of hyperscale AI data centers, and accelerating domestic electric vehicle production. The U.S. CHIPS and Science Act of 2022 committed over USD 52 billion in funding for domestic semiconductor manufacturing, directly increasing downstream demand for advanced TIMs in chip packaging and assembly processes.

The U.S. innovation ecosystem is also driving technology differentiation in next-generation TIM development. In January 2025, TDK Ventures backed NovoLINC for AI computing TIM development supported by the U.S. Department of Energy's ARPA-E COOLERCHIPS program and National Science Foundation funding. Carnegie Mellon University researchers published findings in February 2025 on TIM formulations capable of significantly reducing AI data center cooling costs and GPU/CPU power usage.

Europe Thermal Interface Materials Market Trends

Europe's thermal interface materials market is structurally shaped by the European Union's binding regulatory commitments to carbon neutrality, vehicle electrification, and energy efficiency. The European Green Deal targets net-zero greenhouse gas emissions by 2050, while the EU's Renewable Energy Directive (RED III) mandates at least 42.5% renewable energy consumption by 2030 both driving demand for TIMs in EV drivetrain systems and renewable energy power electronics.

Henkel AG & Co. KGaA, headquartered in Düsseldorf, Germany, is the region's dominant TIM supplier, with multiple high-profile product launches in 2025 targeting automotive electrification, telecom hardware, and AI data center applications. Wacker Chemie AG (Munich, Germany) contributes advanced silicone-based TIM chemistry to the regional supply base.

Asia Pacific Thermal Interface Materials Market Trends

Asia Pacific is unequivocally the dominant and fastest-growing region in the global Thermal Interface Materials market, anchored by China's commanding position across EV battery production, 5G infrastructure deployment, and consumer electronics manufacturing. China accounts for approximately 60% of total global EV battery demand and is home to the majority of global 5G equipment manufacturers, making it the single largest TIM end-use market globally.

Japan's contribution through Shin-Etsu Chemical Co., Ltd. and Fujipoly delivers significant advanced TIM manufacturing and formulation expertise within the regional value chain. India is emerging as a high-growth TIM market, driven by its Production Linked Incentive (PLI) Scheme for Advanced Chemistry Cells with a budget of INR18,100 crore aimed at establishing domestic battery manufacturing a direct enabler of TIM demand from battery assembly facilities.

Competitive Landscape

The global Thermal Interface Materials market exhibits a moderately consolidated competitive structure, with a core group of global specialty chemical and advanced materials corporations led by Henkel AG & Co. KGaA, 3M, Parker Hannifin Corporation, The Dow Chemical Company, and Shin-Etsu Chemical Co., Ltd. commanding dominant combined revenue share alongside a wider ecosystem of specialized regional formulators. Key competitive differentiators include proprietary formulation chemistry, ultra-high-conductivity product portfolios, application engineering support for EV and AI end-users, and deep OEM supply chain integration.

Key Developments:

- In December 2025, Henkel introduced Bergquist TGF 10000, a 10 W/mK liquid gap filler positioned for high-power electronics across automotive, telecom, computing and network infrastructure.

- In November 2025, Parker Chomerics introduced THERM-A-GAP GEL 120, a dispensable thermal gap filler gel positioned as a very-high-conductivity option for demanding electronics cooling.

Companies Covered in Thermal Interface Materials Market

- 3M

- Henkel

- Indium Corporation

- Fujipoly

- The Dow Chemical Company

- Honeywell International Inc.

- SIBELCO

- Shin-Etsu

- Parker Hannifin Corporation

- Wacker Chemie

- Others Key Players

Frequently Asked Questions

The global Thermal Interface Materials market is valued at US$ 5.1 Bn in 2026 and is projected to reach US$ 11.0 Bn by 2033, registering a CAGR of 11.5% over the 2026–2033 forecast period.

The primary growth drivers include surging demand from AI-powered data centers where NVIDIA B200 GPUs generate 1,200W TDP requiring advanced TIM solutions and rapid EV battery production scaling that reached 3.3 TWh manufacturing capacity in 2024 with 30% year-over-year growth.

The Greases and Adhesives segment leads with approximately 35% revenue share, driven by superior conformability across micro-scale chip-to-heatsink interfaces, reworkability in high-value electronics assembly, and broad compatibility across automotive, computing, and telecom applications.

Asia Pacific dominates, led by China, which accounts for approximately 60% of global EV battery demand and hosts the majority of global 5G equipment production.

Key market participants include Henkel AG & Co. KGaA, 3M, Parker Hannifin Corporation, The Dow Chemical Company, and Panasonic Holdings Corporation, among others active across global TIM supply and innovation ecosystems.